Market Movers: Solstice

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

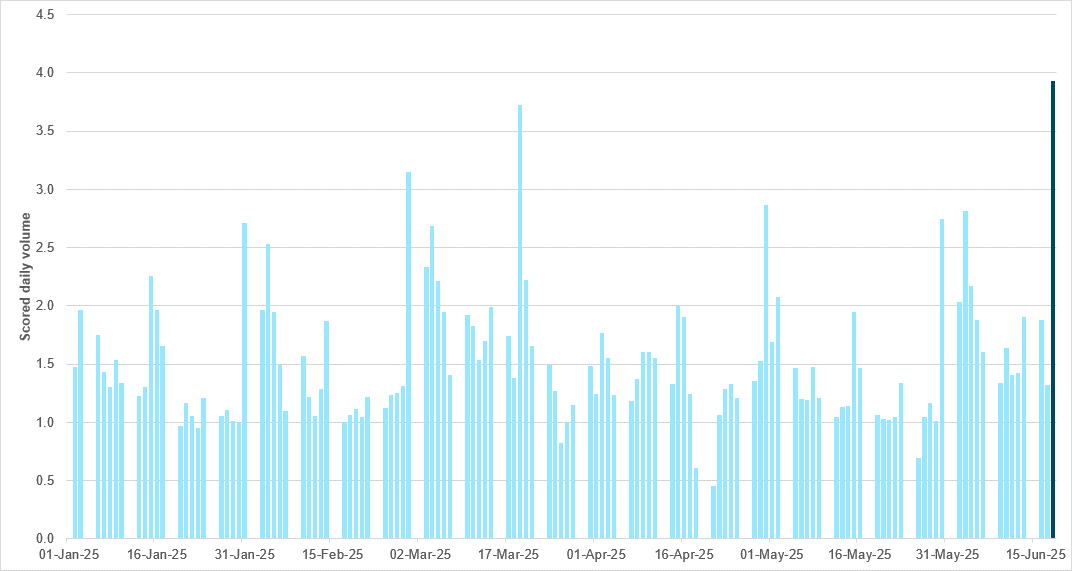

EXHIBIT #1: FOMC/IMM DAY REGISTERS A NEW VOLUME HIGH FOR 2025

Source: BNY

The June FOMC decision itself may not have been exceptional, but the broader macro context for markets coupled with the usual overlapping FOMC and IMM dates meant that flows were. Our data showed a near-4.0 volume score day – the biggest since June 2024 – and certainly one of the strongest over the past three years. Normal hedging needs on an FX-only basis aside, the events over the past quarter, compounded by current geopolitical issues, have likely amplified flow interest. As things stand, June stands to be a far higher-volume month than May, and recent volume scores have consistently moved above 1.5. How do investors separate the dollar story from the broader sentiment story? It was broadly anticipated that correlations would continue to shift, leading to a rise in hedging interest against the dollar on trade and fiscal concerns. The past week has challenged these assumptions, as the dollar has rediscovered its safe-haven status amid geopolitical risk, and we believe that the flows generated on Wednesday were broadly in line with the dollar-positive/defensive theme rather than the drivers in April.

Risk sentiment is mixed, amid relief that immediate U.S. action in Iran has a “two-week” reprieve. Cynics will argue that President Trump’s decision not to take military action on Iranian nuclear sites for two weeks simply pushes the conflict back onto Israel to resolve. Optimists see it as an opportunity for diplomacy. Oil, which acts as a barometer, remains at a five-month high, and the risk premium will likely hurt growth globally over the summer. Next up are the NATO meetings and more defense spending pushes. We are at a crossroads for markets: today’s summer solstice marks the hedging turning point for risk, as investors balance home bias, energy supply shock risks and trade tariffs against policy fixes. Overnight events and news from yesterday matter as well, with Norges Bank delivering a surprise 25bp cut and Brazil’s Copom a surprise 25bp hike, while the SNB moved to zero rates; the economic data show higher inflation in Japan and lower retail sales in the U.K. The potential stagflation worries are global and will be the center of the summer’s trading focus as bonds wobble in their safe haven role, CHF and gold remain favorites, and equities look stuck in the confessional season ahead of Q2 earnings – warnings on margins and earnings look more likely than relief from the summer heat. There is no easy way to balance uncertainty from geopolitical and political risks in a market conditioned by years of monetary support and fiscal largesse. For many, today is the longest day of the year; for others, the lack of clarity makes it just the start of a longer, dry, hot journey. The dollar will likely become the key barometer for judging risk along the way.

Japan’s annual inflation rate edged down to 3.5% in May 2025 from 3.6% in the previous two months, marking the lowest level since November. Meanwhile core inflation accelerated to 3.7% from 3.5% in April, reaching its highest level in over two years. Price growth eased for clothing (2.6% vs. 2.7% in April), household items (3.6% vs. 4.1%) and healthcare (2.0% vs. 2.2%), while education costs fell further (-5.6%). In contrast, inflation held steady for transport (2.7%) and miscellaneous items (1.3%), but accelerated for housing (1.1% vs. 1.0%), recreation (3.0% vs. 2.7%) and communications (1.9% vs. 1.1%). Meanwhile, price inflation for electricity (11.3% vs. 13.5%) and gas (5.4% vs. 4.4%) remained elevated. On the food side, prices increased by 6.5%, staying at the slowest pace in four months, though rice prices soared 101.7%, underscoring the limited impact of government efforts to rein in staple food costs. Nikkei -0.221% to 38403.23, USDJPY -0.069% to 145.35, 10y JGB -2.1bp to 1.398%.

Japan’s Finance Ministry plans to cut super-long bond issuance by ¥3.2tn through March 2026, exceeding earlier expectations of a ¥2.3tn reduction. The decision follows heightened market concerns after record volatility in super-long yields. The proposed cuts will affect 20y, 30y and 40y bonds, and were outlined during a meeting with primary dealers on Friday.

The U.K.’s public sector borrowing reached £17.7bn in May 2025, £0.7bn higher than a year earlier and the second-highest May figure since records began in 1993. For the financial year to May, borrowing totaled £37.7bn, up £1.6bn y/y and the third-highest April-May figure on record. The current budget deficit stood at £12.8bn in May, £1.7bn lower than in May 2024, while the April-May total was £27.4bn, down £1.3bn y/y. Public sector net debt excluding banks was 96.4% of GDP, up 0.5 percentage points from May 2024. Net financial liabilities stood at 83.9% of GDP. The central government’s net cash requirement was £24.1bn in May, down £0.4bn from a year earlier. FTSE 100 +0.528% to 8838.18, GBPUSD +0.156% to 1.3486, 10y gilt -0.1bp to 4.529%.

In a speech in Kyiv today, Bank of England Governor Andrew Bailey stressed the importance of central bank independence, grounded in democratic accountability and objectives set by Parliament. He argued that recent economic shocks have validated modern monetary frameworks, particularly inflation-targeting as a nominal anchor, so long as they are applied with flexibility and transparency. Bailey emphasized the need to preserve the “singleness of money” and highlighted growing risks from the non-bank financial sector, calling for closer scrutiny of its links to the banking system. On digital money, he distinguished between unbacked crypto assets and stablecoins, urging high standards to ensure monetary stability, and encouraged commercial banks to take the lead in digital payment innovation.

In another sign of soft growth, China’s national general public budget revenue totaled ¥96.62tn from January to May 2025, down 0.3% y/y. Tax revenue was ¥79.16tn, a 1.6% decline, while non-tax revenue rose 6.2% to ¥17.47tn. Central government revenue fell 3% to ¥41.49tn, while local government revenue grew 1.9% to ¥55.14tn. During the same period, total public budget expenditure reached ¥112.95tn, up 4.2%. Central government spending rose 9.4% to ¥15.79tn, and local government spending increased 3.4% to ¥97.16tn. CSI 300 +0.092% to 3846.64, USDCNY -0.059% to 7.1836, 10y CGB -0.3bp to 1.639%.

U.S. June Philadelphia Fed Business Outlook is expected to improve further to -1.5 from -4 in May; this is key for convergence of soft to hard data.

U.S. May Leading Index is expected to post the sixth straight monthly decline, at -0.1%.

Canada April retail sales are forecast to slow to 0.4% from 0.8%, while retail sales ex-auto are projected to improve to -0.2% from -0.7%. The strength of the Canadian consumer continues to matters.

Mood: iFlow Mood dropped into negative territory amid heightened geopolitical uncertainties. Equity flows slowed sharply, against a further pick-up in core sovereign bond buying.

FX: APAC FX came under increasing outflow pressure, led by HKD and IDR. Elsewhere, G10 and LatAm were mildly sold, against buying in EMEA.

FI: Notable flows included buying in Japanese government bonds, followed by Hungarian and South African sovereign bonds. U.K. gilts and Colombian government bonds were most sold.

Equities: DM APAC was the only region with inflows, led by Japan, against selling flows in the rest of the world, especially in EM EMEA and EM APAC. South Africa, South Korea, Malaysia and Norway saw the most significant outflows from equities.

“Swim through the serene summer sky.” Virgil

“Let a man walk ten miles steadily on a hot summer’s day along a dusty English road, and he will soon discover why beer was invented.” – G.K. Chesterton

Great Britain’s retail sales volumes fell by 2.7% in May 2025, reversing a 1.3% rise the previous month. All sectors recorded monthly declines, with food store volumes down 5.0% – the sharpest drop since May 2021 – following strong April sales attributed to good weather. Supermarkets reported lower demand due to inflation-related cutbacks and weaker alcohol and tobacco sales. Non-food store volumes fell 1.4%, mainly due to falls in clothing and household goods, as earlier-than-usual home improvement purchases tapered off. Online spending dropped 1.0% m/m and 2.5% y/y, marking a second consecutive monthly contraction. Overall spending fell 2.4% in May, with the online share rising slightly to 27.2%, from 26.8% in April. FTSE 100 +0.528% to 8838.18, GBPUSD +0.156% to 1.3486, 10y gilt -0.1bp to 4.529%.

China kept its loan prime rates (LPRs) unchanged on June 20, with the 1y LPR at 3.0% and the 5y-plus LPR at 3.5%. Both rates were held steady after being cut in May, when policy rate reductions were passed through to LPR quotes. Market participants noted that with June policy rates remaining stable and no major changes in LPR spread-setting factors, the latest result aligned with expectations. Analysts anticipate a near-term observation period, during which LPR rates may remain steady. Given limited external and domestic pressures, further monetary easing is seen as unnecessary for now. Some expect that new easing measures may come in August or Q4, focusing on fiscal stimulus and cost reduction. Others see scope for further LPR cuts later in the year, especially to support domestic demand and stabilize the property market. CSI 300 +0.092% to 3846.64, USDCNY -0.059% to 7.1836, 10y CGB -0.3bp to 1.639%.

Türkiye’s non-domestic producer price index (ND-PPI) rose by 25.34% y/y in May 2025, with a monthly increase of 2.40%. Manufacturing ND-PPI increased by 25.40% y/y and 2.36% m/m. Among industrial sectors, mining and quarrying prices rose by 22.08% y/y and 4.66% m/m. By goods category, durable consumer goods saw the sharpest annual rise at 30.80%, followed by capital goods at 30.73% and non-durable consumer goods at 28.39%. Energy prices edged up only 0.40% y/y. Monthly increases were led by metal ores (+7.16%), wearing apparel (+4.32%) and beverages (+4.31%), while computer and electronics products saw a 1.39% decline. The next ND-PPI release is scheduled for July 21, 2025. BI 100 +1.355% to 9225.38, USDTRY +0.145% to 39.6807, 10y TGB +3bp to 33.36%.

Türkiye’s average house sale price rose 25.4% y/y in January-May 2025, according to total transaction volumes. In May alone, house sales reached 130,025 units, up 17.6% y/y. Mortgaged house sales surged 95.9% y/y to 19,412 units, while other house sales rose 9.9% to 110,613. First-time sales increased by 11.2% to 39,546, and second-hand sales rose 20.6% to 90,479. Cumulatively, sales in the first five months of 2025 reached 584,170, up 25.4% from a year earlier. Mortgaged sales accounted for 88,606 units, a 98.7% increase y/y. Sales to foreigners fell by 14.2% y/y in May to 1,771 and were down 13.7% y/y over the January-May period to 7,789. Russian, Iranian and German buyers led foreign demand.

Türkiye’s consumer confidence index edged up to 85.1 in June 2025 from 84.8 in May, marking a 0.3% monthly increase. Sub-index changes were modest: the financial situation outlook for households rose 0.6% to 85.8, while the present financial situation improved by 0.4% to 69.3. The general economic situation expectation increased by 0.3% to 82.4, after a slight drop in May. The durable goods spending outlook rose just 0.1% to 102.6; it remains the only sub-index above 100, which indicates optimism. The next consumer confidence data release is scheduled for July 23, 2025.