Market Movers: Small Steps

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 9 minutes

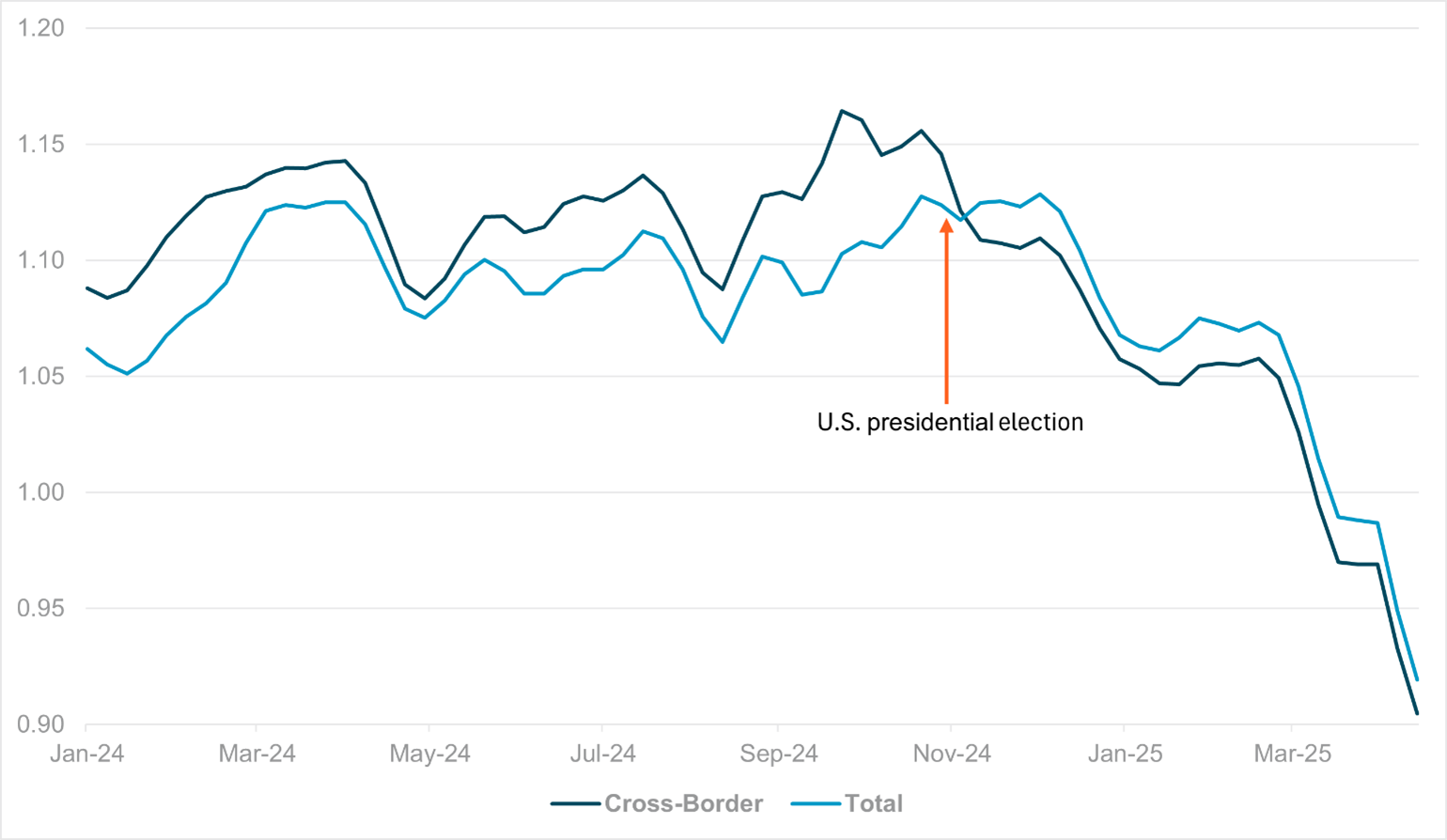

EXHIBIT #1: WEEKLY CROSS-BORDER VS. AGGREGATE HOLDINGS OF U.S. EQUITIES, 2024 TO PRESENT

Source: BNY

Risk on as small steps on tariffs deals between China and the U.S. and President Trump walking back threats to remove Fed Chairman Powell have helped to offset ongoing concerns about growth, especially as European PMIs all surprise to the downside. Meanwhile, as U.S. earnings season proceeds apace, we find that cross-border investors remain more cautious on U.S. equity positioning compared to dollar-denominated investors. While it would be tempting to attribute the gap to reduced exposures since the escalation of tariffs, we note that the change in leadership of holdings switched just after the U.S. presidential election. In contrast, before the election cross-border investors appear to have had an even bigger belief in U.S. exceptionalism in equities markets. In hindsight, valuation concerns were already emerging at that point across U.S. assets, and we held the view that the gap between holdings in U.S. allocations versus the rest of the world would begin to narrow. Given home-bias for U.S. investors, having higher allocations domestically relative to cross-border investors should also represent an equilibrium state. More recently, holdings among both investor categories have fallen with the market, but for now there is no sign of stronger liquidation by cross-border clients. This supports our view that declines in levels and greater defensiveness by international investors is incremental now and there is little sign, across all asset classes, of broader diversification away from the U.S. How the IMF meetings portray the U.S. position on talks and the small steps toward a new tariff approach matter today along with the ongoing U.S. data as weaker PMI reports globally add to the urgency of policy shifts.

U.K. public sector borrowing once again overshot estimates, coming in at £16.4bn for March 2025 (consensus: £15.8bn). The central government’s net cash requirement surged to £21.1bn, the highest level since July 2024. This means total borrowing for the 2024-2025 fiscal year has overshot the Office for Budget Responsibility forecast by £14.6bn, to £151.9bn. The current budget deficit was provisionally estimated at £74.6bn, £12.6bn more than FY’23/24 and £13.9bn more than the £60.7bn forecast by the OBR. FTSE 100 +1.57% to 8459.38, 10y gilt 33bp to 4.516%, GBPUSD -0.16% to 1.3311.

German manufacturing PMI for April showed further contraction, but at 48.0 the print was slightly better than expected. The bigger surprise was in services, which also fell below the critical threshold of 50, to 48.8, in contrast to expectations for marginal expansion. The composite PMI also moved back into contraction as a result. S&P stressed that “tariff concerns and uncertainty weighed on business confidence and demand. Firms’ growth expectations sank to their lowest in six months and the labor market remained under pressure, albeit with employment falling only fractionally and at the slowest pace in almost a year.” DAX +2.86% to 21904.42, 10y Bund +3.4% to 2.47%, EURUSD -0.12% to 1.1407.

French manufacturing PMI surprised to the upside at 48.2 (consensus: 47.9), but services PMI fell more than expected to 46.8, pushing the composite figure lower to 47.3. S&P noted that “French manufacturers also continue to reduce the volume of their purchases and inventory levels in April. On a more positive note, production saw a slight increase this month, although it is far from indicating a sustained trend reversal.” Combined with the softer German manufacturing PMI figure, Eurozone composite PMI has fallen to 50.1 (consensus: 50.2). CAC40 +2.05% to 3205.45, 10y OAT +1.6bp to 3.226%, EURUSD -0.12% to 1.1407.

South African consumer price inflation rose 2.7% y/y (estimate: +3.0%) in March, according to Statistics South Africa. Core consumer prices rose 3.1% y/y (estimate: +3.2%). Biggest contribution to the softening in price growth came from durable goods, which contracted by 0.1%m/m. However, core CPI ex-energy remains robust at +0.5m/m. TOP40 +0.94% to 83494.38, 10y SAGB -7.6bp to 10.84%, USDZAR -0.61% to 18.5023.

Iran’s semi-official Mehr news agency, citing Foreign Minister Araghchi, reported that “U.S. talks are on right track” and the country was “cautiously optimistic” of reaching an accord. Araghchi stressed that “a good deal is possible if the U.S. avoids unrealistic demands.”

Chinese Premier Li Qiang sent a letter to his Japanese counterpart, stressing the need to “fight protectionism together,” according to Japan’s Kyodo news agency. The news comes amid reports that the U.S. has agreed on a framework of a trade deal with Japan and India. CSI 300 +0.08% to 3786.88, 10y CGB +1.0bp to 1.657%.

U.S. April flash composite PMI expected 51 from 53.5, with manufacturing off 49.4 from 50.2 and services 52.8 from 54.4 – watching for bigger weakness along with jobs and prices.

U.S. March new home sales expected up 0.2% to 680,000 after 676,000 – how rates and prices play against supply key focus.

U.S. Treasury sells $70bn in 5y notes – given weaker demand of 2y note yesterday this matters to views on foreign buying of U.S. treasuries.

U.S. Beige Book – important district-by-district evidence for FOMC on slowdown in economy and higher price pressure.

Fed Speakers: Chicago Fed Goolsbee, St. Louis Fed Musalem, Gov. Waller, Cleveland Fed Hammack speaks on balance sheet.

ECB Speakers: ECB Villeroy speaks at Atlantic Council. ECB Lane speaks at IIF in Washington.

Mood: iFlow Mood retraced marginally but remains in risk-off mode. Equities selling continues but pace of sovereign bond buying eased.

FX: USD, EUR, JPY and SGD the main outflows against good inflows in AUD and HKD. Save-haven bid on CHF eases but remains significant. Relatively muted FX flows in LatAm.

FI: Muted FI slows. Notable flows are buying in Mexico and Australia bonds against selling in Chinese and New Zealand government bonds.

Equities: APAC as a region is most sold against demand in both EM and DM EMEA region. Chinese equities selling momentum continues. Mixed G10 flows with light selling in the U.K., Europe, Canada and Japan equities against light buying in Australia and U.S. equities.

"Great things are not done by impulse, but by a series of small things brought together." – Vincent Van Gogh

“It is better to take many small steps in the right direction than to make a great leap forward only to stumble backward.” – Chinese proverb

The Eurozone reported a trade balance of €21bn for February, in what is likely another sign of front-loading of exports ahead of tariffs. This was well above estimates of €15.0bn and a strong increase from a revised €14.4bn in January. Eurostat highlighted that compared to February 2024, the chemicals sector witnessed a remarkable increase, with its balance rising from €17.3bn to €28.6bn. Meanwhile, sectors such as machineries and vehicles experienced a balance decrease from €23.7 bn to €19.4 bn. Other manufactured goods shifted from a surplus of €2.6 bn to a deficit of €0.6 bn. Unsurprisingly, exports to the U.S. surged by 22.4% y/y, while exports to China contracted slightly by 0.2%. EuroStoxx 50 +2.62% to 5091.41, EURUSD -0.12% to 1.1407.

U.K. PMIs fell more than expected to 48.2 (consensus: 50.4), led by a sharp fall in services to 48.9 (consensus: 51.5). This was the first decline in private sector output in 18 months. S&P noted that “weaker demand from international markets weighed on business activity in both the manufacturing and service sectors. The latest figures indicated that total new work from abroad decreased sharply and at the fastest pace for nearly five years. Survey respondents widely commented on the negative impact of U.S. tariffs and a subsequent slump in confidence among clients.” FTSE 100 +1.57% to 8459.38, 10y gilt 33bp to 4.516%, GBPUSD -0.16% to 1.3311.

Australia April PMI indices dented by geopolitical and tariff uncertainties despite strong domestic business activity. PMI manufacturing eases to 51.7 (March: 52.1), with non-manufacturing at 51.4 (51.6). Improvements across both the manufacturing and service sectors led to the fastest rise in new work since April 2022. In turn, outstanding business accumulated at the sharpest pace in nearly three years. This was despite another solid rise in headcounts. Higher demand also enabled firms to raise selling prices at a quicker pace in April as costs continued to rise at a steep rate. That said, confidence moderated among Australian companies while exports further contracted following tariff uncertainties in April. ASX200 up 1.3%, 10y ACGB 0.6bp higher at 4.27%, AUD up 0.2% at 0.6411.

Japan April flash PMI composite back to expansion zone at 51.1 after a brief one month of contraction in March (48.9), led by strong PMI services at 52.2 (50.0) while PMI manufacturing remains in contraction for the 10th straight month at 48.5. Factories saw new orders decline at the steepest rate in over a year amid a stronger deterioration in foreign demand, as well as reports of subdued client spending and concerns over tariffs. In contrast, services companies reported the strongest rise in new work since January. Inflationary pressures remained acute across both sectors, however, with overall input costs rising at the fastest rate in two years. As part of efforts to protect margins, firms raised their selling prices at a solid pace. Nikkei up 1.9%, 10y JGB 1.9bp higher at 1.33%, USDJPY off -1.1% at 141.87.

India April flash PMI rose for both PMI manufacturing at 58.4 (Mar: 58.1) and services at 59.1 (March: 58.5). PMI survey showed new export orders increased at the fastest pace since the series started in September 2014 and quicker expansions in aggregate output and employment. Ongoing increases in cost burdens, private sector firms continued to lift their selling prices. April's rise was marked, faster than in March and stronger than seen on average across the survey history. Manufacturers led the upturn with the steepest rate of inflation in over 12 years. NIFTY up 0.4%, 10y IGB -0.2bp lower at 6.33%, USDINR off -0.3% at 85.

South Korea April consumer confidence improved from 93.4 to 93.8. Expectation components rose the most with expectations of domestic economic situation and employment condition up 3 and 4 points to 73 and 76, respectively, but remain below November 2024 levels prior to the “martial law” saga. One-year ahead inflation expectation ticked higher at 2.8% y/y from 2.7% y/y while 3- and 5-year ahead expected inflation remain unchanged at 2.6%. KOSPI up 1.6%, 10y KTB -0.8bp lower at 2.61%, USDKRW up 0.1% at 1425.

Lower commodity prices and easing demand led to downside inflation in APAC region. Malaysia headline CPI at 1.4%, the lowest since 2021 and likely to encourage easing policy on first signs of growth slowdown. Singapore March core inflation at 0.5% y/y with multiple subcomponents in negative y/y growth affirming recent MAS back-to-back easing in April. Further easing could come as early as July policy meeting. Hong Kong March CPI also fell to 1.4%y/y, against estimates of 1.5%y/y. KLCI +0.66% to 1496.14, 10y MGS -0.7bp to 3.651%, USDMYR +0.1252 at 4.3920.