Market Movers: Silver Linings

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

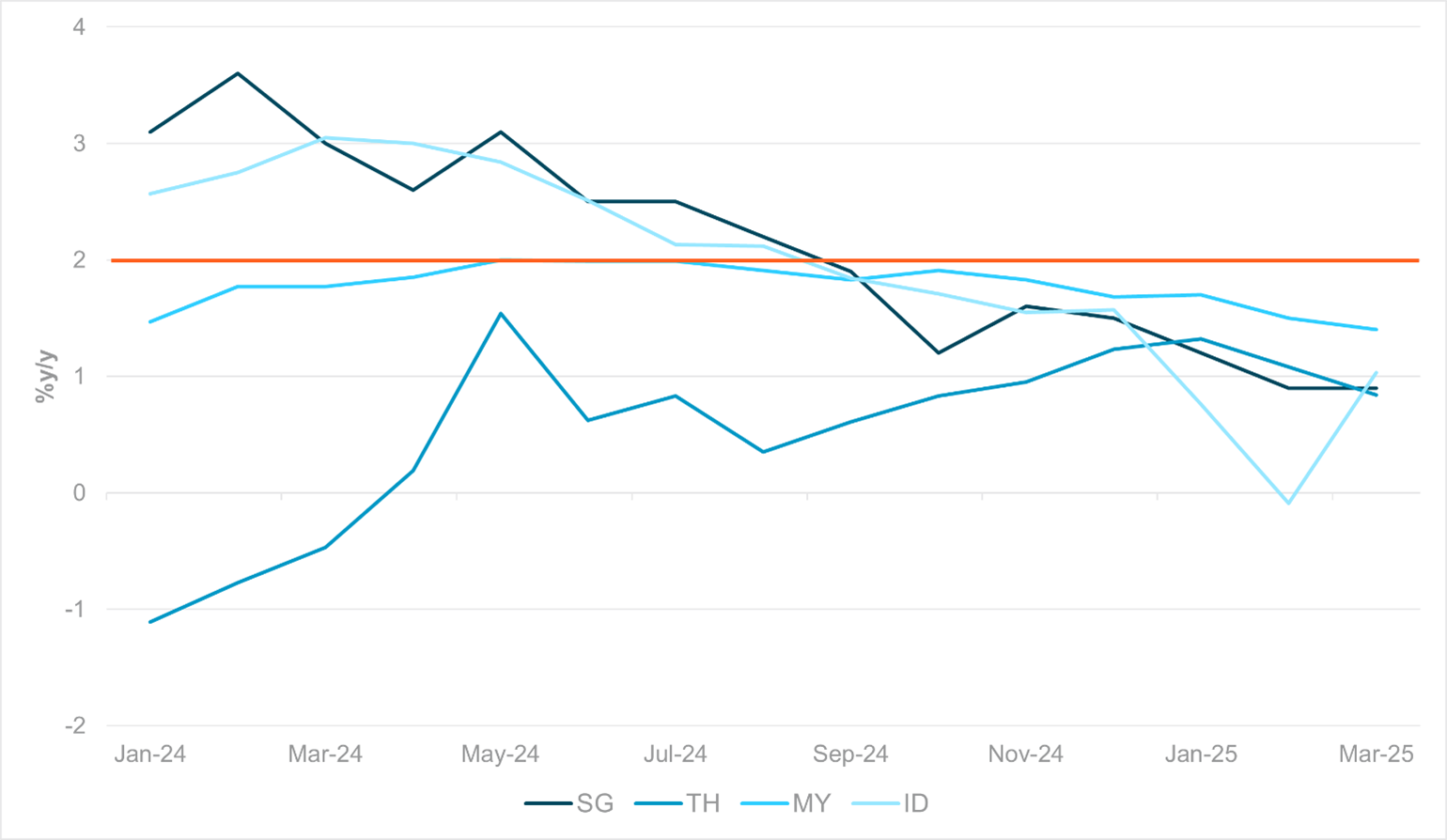

EXHIBIT #1: COMPREHENSIVE DECLINES IN ASEAN INFLATION SUPPORT REAL RATES DESPITE CENTRAL BANK DOVISHNESS

Source: BNY

Risk sentiment sours with further twists in tariff policy spooking the recent rally back in equities globally. With about 25% of the S&P 500 earnings reported, 90% of the outlooks for Q2 warn on tariffs. There may be a silver lining. The USD continues to sag, as U.S. bond markets see a modest bull-steepening in their curve. Rates no longer drive markets, with focus returning to the dollar and risks of further downside. In the wake of Bank Indonesia’s policy decision yesterday, markets are looking for signs that EM central banks are in a better position to cut rates in the months ahead. All key ASEAN economies now have annualized inflation rates below 2% y/y, driven by lower energy costs as oil prices continue to decline. While core prices are generally higher, expectations remain in the region and globally that the damage to sentiment caused by tariffs will start to have an impact on private sector demand. APAC is more worried about growth than inflation. The thinking goes that USD weakness helps. As currency markets stabilize, central banks globally will be in a better position to cut rates and provide stimulus to the economy. More importantly for asset allocation, falling inflation will continue to support real yields and continue to support EM currencies (albeit at lower levels) and encourage external inflows into bond markets in search of improvement in real yields, in addition to diversification away from U.S. assets. These flows may also help complement domestic savings for surplus economies in funding fiscal stimulus up ahead. Away from APAC, we note that CEE central banks are now looking to recommence easing cycles, not only to provide monetary stimulus but also to take advantage of less pressure on their own exchange rates due to ECB cuts and elevated euro valuations. For the U.S. session, the focus on LatAm continues as a region seen as being less hurt by tariffs excluding Mexico, where the focus today will be on April mid-month inflation. As for U.S. rates, the focus on hard data vs. soft will continue with the key being durable goods orders and what these mean for business investment ahead. Growth worries are still key along with a host of earnings, with Alphabet at the close being the main focus.

The April German Ifo Business Climate surprises up to 86.9 from 86.7, against expectations of a decline to 85.2. The current assessment also improved to 86.4, while expectations only dipped marginally to 87.4 from 87.7. The figures broadly align with the manufacturing components for April’s Purchasing Manager Indices (PMI), which also showed limited drag for manufacturers, as opposed to a significant decline for the services sector. Ifo Institute’s Clemens Fuest noted that a strong euro was adding to competitiveness concerns. While ECB Governing Council Member Rehn says the central bank should not rule out larger interest cuts up ahead. He notes that “economic risks are starting to materialise” as financial conditions tighten, and it was “really important that we maintain full freedom of action.” DAX +0.83% to 21922, 10y Bund -1.3bp to 2.481%, EURUSD -0.5% to 1.1372.

Japan 2-year JGB auction had strong demand with bid/cover ratio at 3.58 and tailed at the bottom of the range of 0.3bp. Overall a strong JGB auction month, except for the 4.3bp wide tail for 30-year auction in early April at the peak of market volatilities. Nikkei up 0.5% to 35030, 10y JGB -1.3bp lower at 1.31%, JPY off -0.4% at 142.63.

South Korea advance Q1 GDP drops into contraction at -0.2% q/q, -0.1% y/y from +0.1% q/q, 1.2% y/y in Q4 2024. In terms of production, manufacturing shrank by -0.8% q/q (+0.2% in Q4 2024) while construction shrank by -1.5% q/q (Q4 2024: -4.1% q/q). Utilities (electric, gas & water supply) production grew strongly at 7.9% q/q (Q4 2024: -5.8%). Elsewhere, South Korea’s April manufacturing industry sentiment rose to 93.1 (previous forecast of 89.9), the highest since Aug 2024, led by surge in new orders. Non-manufacturing industry sentiment remains relatively sluggish at 84.5. Business remains cautious with a projected May outlook at 90 for the manufacturing sector and 83.8 for the non-manufacturing industry. KOSPI off -0.1% to 2522.33, 10y KTB 2.0bp higher at 2.62%, KRW off -0.7% at 1436.75.

In a surprise climbdown, South Africa’s National Treasury announced it would scrap a proposed VAT tax increase, which had threatened to bring down the Government of National Unity (GNU) due to opposition from the Democratic Alliance (DA) – the key partner of the African National Congress in the GNU. While the move has eased the pressure on the GNU itself, the Treasury will need to resolve a ZAR 75bn budget deficit. The Treasury has also approached the DA requesting a cessation of court proceedings launched by the party with the aim of preventing the tax rise. DA leader Helen Zille confirmed that the ANC and DA will meet on Friday, but warned the GNU was operating in a “very low-trust environment.” TOP40 -0.43% to 346.10, 10y SAGB -5.3bp to 10.727%, USDZAR +0.026% to 18.6587.

In a meeting with foreign executives today, Chinese Deputy Trade Representative Ling Ji called upon firms to “fight unilateralism.” He also stated that Beijing will be highly attentive to resolving the problems faced by international firms operating in China. The Ministry of Commerce said that the U.S. should “revoke all unilateral tariffs” and “show sincerity.” CSI 300 off 0.07%, 10y CGB +0.6bp to 1.658%, CNH off 0.1% to 7.2915.

U.S. March Chicago Fed National Activity Index expected 0.12 after 0.18 – not usually watched by the market but a useful future growth tool, with the bounce from February expected to continue.

U.S. March preliminary durable goods orders expected +2% m/m after +1% with more evidence of pre-tariff loading. Ex- transports expected up 0.3% after 0.7% but key focus is on capex with cap goods ex air/defense expected up just 0.1% after -0.2%.

U.S. weekly jobless claims expected up 5k to 220k with continuing claims expected -16k to 1.869mn – both matter but unless “shocking” unlikely to change markets.

U.S. March existing home sales expected -3.1% to 4.13mn rate after +4.2% at 4.26mn rate – after the surprise new home sales some moderation here expected. Rates and supply key.

U.S. April Kansas City Fed Manufacturing Activity Index expected -6 from -2 – with focus on weakness in oil industry key.

U.S. Treasury sells $44bn in 7-year notes – after the successful demand in 5y yesterday – pressure off on this auction but with recent rally back concessions maybe an issue.

Fed Speaker – only Minneapolis Fed Kashkari at University of Minneapolis in moderated conversation.

Mood: Sentiment improved with positive news on tariffs. iFlow Mood remains in risk-off zone but is off the lows driven by both decreased equities selling and lower sovereign bond demand.

FX: Within G10, AUD posted the most inflows, followed by CHF and NZD against outflows in USD, EUR and JPY. Elsewhere, inflows momentum continues in APAC against outflows in LatAm against mixed flows in EMEA region.

FI: Notable sovereign bond flows were selling in Australia and Chinese government bonds. Cross-border investors bought in both U.S. Treasurys and Eurozone government bonds.

Equities: Broadly mixed and light flows, except for strong demand in Indian and Polish equities, followed by light buying in Europe, the U.K., Japan and the U.S. APAC was biased to sell flows, including Chinese equities.

“You have to do everything you can, you have to work your hardest, and if you do, if you stay positive, you have a shot at a silver lining.” – Silver Linings Playbook

“Too many people miss the silver lining because they’re expecting gold.” – Maurice Setter

French April consumer confidence steady at 92 – better than 91 expected. Sentiment around personal finances remained unchanged, with the assessment of past financial situations steady at -20 and expectations staying weak at -11. Intentions to make major purchases improved slightly (-23 vs. -26), while households’ willingness to save dipped (35 vs. 39). However, consumers remained deeply pessimistic about living standards, both past (-67 vs. -69) and future (-53 vs. -50). Unemployment concerns increased (51 vs. 47), and while inflation expectations eased (-37 vs. -41), perceptions of past consumer prices worsened (-13 vs. -8). CAC 40 off 0.6%, 10y OATS off 4bp to 3.195%.

Polish unemployment fell to 5.3% in March from 5.4% in February, according to the Polish Statistics Office. Expectations for rate cuts in Poland continue to build despite a tight labor market. NBP Monetary Policy Committee Member Wnorowski said there was even a chance for a 50bp cut in May. This underscores the change in views, as he said on April 7 that there wasn’t much room for rate cuts this year at all. WIG -0.90% to 98779.13, 10y PGB -0.9bp to 5.228%, EURPLN -0.07% to 4.2787.

New Zealand April ANZ Consumer Confidence up 5.5% m/m to 98.3 (March: 93.2). The highlight of the survey is the rise in the proportion of households thinking it’s a good time to buy a major household item and the unexpected rise of household inflation expectations by 0.5 points to 4.7%. The dislocation between consumer confidence index and NZD normalized in April, which is more a function of global currency movement than domestic condition. NZD is up 6% ytd after a sharp 11% sell-off in Q4 2024. NZX50 up 0.5%, 10y NZGB -3.0bp lower at 4.51%, NZD off -0.3% at 0.597.

Czech Consumer and Business Confidence registered broad-based declines in April, based on the latest business cycle survey. The composite figure fell to the lowest level since August 2024. Similar to surveys elsewhere in Europe, household expectations are far worse than business sentiment. The balance of Czech consumer confidence remains negative at -12.5, but business confidence has also fallen back to October lows, led by a sharp drop in industrial expectations. Prague SE -0.46% to 2064.23, 10y -1.9bp 4.017%, EURCZK +0.036% to 25.00.

Turkey April manufacturing confidence slows to 103.2 from 104.1 – retreating from 10-month highs. The decline was driven by weaker expectations for production (118.2 vs. 124) and employment (102.1 vs. 104.3) over the next three months. Sentiment regarding general business conditions also deteriorated (86 vs. 96.5). On the other hand, views improved for current order volumes (85.8 vs. 84.4), stocks of finished goods (102.1 vs. 99.7), export expectations (118.2 vs. 117.7) and fixed investment spending (107.9 vs. 107.1). BIST 100 flat, TRY off 0.05% to 38.319.

Japan March PPI Services posted 0.7% m/m gain, the strongest monthly gain since April 2024. On the year, PPI Services at 3.1% y/y. Nikkei up 0.5%, 10y JGB -1.3bp lower at 1.31%, JPY off -0.4% at 142.63.