Market Movers: Signals and Noise

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

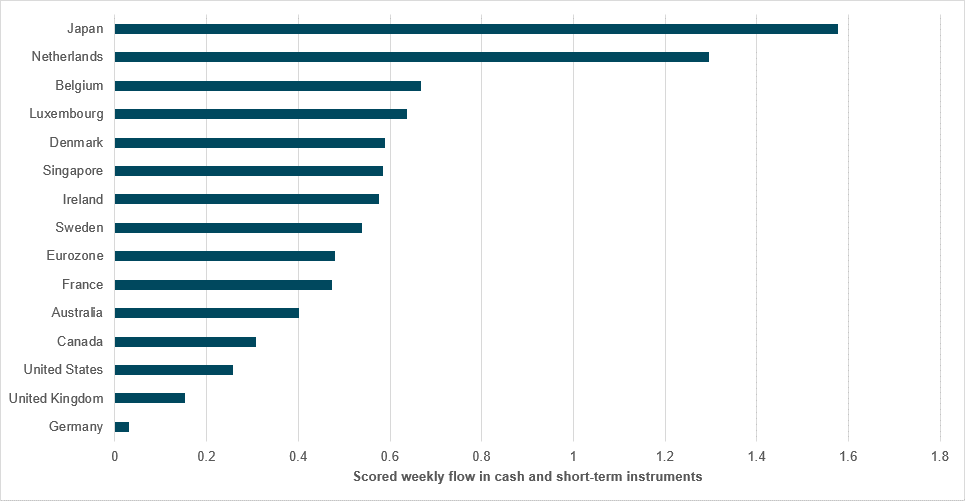

EXHIBIT #1: CASH DEMAND SURGES IN ANOTHER SIGN OF RISK AVERSION

Source: BNY

Looking for further confirmation of greater defensive positioning? The surge in flows into cash markets is an early sign. This market is sensitive to changes in front-end interest rates, and we acknowledge that the pullback in easing expectations globally is contributing to higher cash interest. However, with every single major market seeing inflows, this points to a broader liquidity preference taking place. There were similar flows around the severe surge in risk aversion last August, and more recently in the weeks after “Liberation Day”. On a weekly average flow basis, flows into Japan and the Netherlands – two very different markets – were exceptionally strong last week. The Benelux region performed strongly in general, and high cash demand in Luxembourg and Belgium could indirectly indicate a high level of asset liquidation taking place in major custody and clearing centers. Smaller “super-AAA” markets such as Denmark and Singapore also show cash performing well, which points to ongoing interest in fiscal sustainability. In contrast, U.S. and U.K. cash markets are struggling more, though Germany is the outlier in this sense, failing to benefit from both good liquidity and fiscal strength.

Risk sentiment is positive, with equities and commodities gaining on the back of U.S./China trade talk hopes. The China CPI and trade data overnight were weaker than expected, adding to hopes of greater stimulus there, as the minimum wage was pushed up after the close. Japanese data were revised up, boosting rate hike expectations. The next big event there is June 20, when the MoF meets primary dealers to discuss the JGB market. USD is lower, most bond yields are lower and equities globally are higher, but sentiment is mixed. The focus on long-dated bond yields remains, with Japan and India at different angles: the RBI is nearing the end of its rate easing, while the BoJ is far from ending its hiking cycle. The monetary policy noise is drowning out the fiscal and trade policy debates. Politics is a mixed bag, with the U.S. focused on California, the tax bill and the ongoing deregulation drive, which are providing conflicting signals. The U.S. week ahead revolves around CPI and more evidence of economic slowing; trade and the speed of talks and deals will dominate, with speed key to fixing the tariff uncertainty. The day ahead has little news for U.S. markets, leaving the inflation focus and the trade talk story on the two side of the seesaw for volatility. The risks for the day are in the noise not the signal of positions: after May was spent catching up to benchmark positions, June could be about unwinding them.

Japan’s economy stagnated in Q1 2025, with real GDP flat q/q (0.0%), revised up from the initial estimate of -0.2%. At an annualized rate, GDP fell 0.2%, in a notable upward revision from the previous -0.7%. Private consumption was marginally stronger at +0.1%, while business investment rose 1.1% (up from 0.9%). Public investment was revised to -0.4%. Net exports added 0.2 percentage points to growth, driven by a 3.0% jump in exports and a 0.7% decline in imports. Nominal GDP rose 0.9% q/q, equating to an annualized 3.6% gain. Compensation of employees (real) fell 0.9% q/q, continuing its weak trend. Overall, the revisions paint a slightly more resilient picture, but underlying domestic demand remains subdued. Nikkei +0.919% to 38088.57, USDJPY -0.539% to 144.07, 10y JGB +1.3bp to 1.468%.

In another sign of unease over the behavior of long-dated yields, wires reported that the Japanese government is now mulling buybacks of past-issued super-long JGBs. Earlier on Monday, Japanese Prime Minister Ishiba warned that the country was shifting to “a phase where interest rates rise as a trend.” Noting that such gains could raise the cost of funding government debt, spending will be affected as a result. The BoJ is expected to stick with its decreases in JGB purchases after April 2026, but the central bank may slow down the pace of reduction to prevent rates from spiking.

China May CPI and core CPI were unchanged at -0.1% y/y and 0.5% y/y, respectively. On the month, the headline rate was down -0.2% m/m, while core inflation was flat at 0%, from +0.2% m/m in April. Overall, food inflation remains a drag, coming in negative for the fourth straight month at -0.4% y/y, while non-food inflation was unchanged at a flat 0% y/y. Consumables inflation was down to -0.5% y/y from -0.3% y/y, but services inflation ticked up to 0.5% y/y vs. 0.3% y/y in April. Looking into the breakdown, “other articles” posted the highest gains, at +7.3% y/y, while transport and communications was down the most at -4.3% y/y. Beijing announced it is to hold a multi-ministry press conference on Tuesday to “introduce policies to further safeguard and improve people’s livelihoods.” CSI 300 +0.291% to 3885.25, USDCNY -0.128% to 7.1834, 10y CGB -0.4bp to 1.689%.

China’s exports to the U.S. dropped 34% y/y in May – the steepest fall since February 2020 – amid ongoing trade tensions. This was despite overall exports rising 4.8%. Imports from the U.S. also declined by 18%, shrinking China’s trade surplus with the U.S. by 41.6% to $18bn. Total imports fell 3.4% y/y, reflecting weak domestic demand. However, exports to ASEAN, the EU and Africa rose 15%, 12% and 33%, respectively, helping to lift China’s overall trade surplus by 25% to $103.2bn. Rare earth exports fell 5.7% y/y amid tightened controls (but rose 23% m/m), while car and ship exports were up 22% and 5%, respectively. Smartphone and appliance exports decreased, as did U.S.-bound trade overall.

A Seoul court said on Monday it will indefinitely postpone a trial of President Lee Jae-myung on charges of violating election law in 2022, originally scheduled for 18 June 2025. The delay follows a Supreme Court ruling in May confirming Lee’s violation of election law but referring the case back to the appeals court. Citing Article 84 of the Constitution, which protects a sitting president from prosecution, the court opted not to set a new date. Legal experts are divided over whether the immunity extends to trials initiated before a president took office. Meanwhile, Lee’s Democratic Party is pushing legislation to suspend ongoing trials against incumbent presidents, though it may face constitutional scrutiny. KOSPI +1.555% to 2855.77, USDKRW -0.211% to 1352.9, 10y KTB -0.2bp to 2.89%.

U.S./China trade talks expected to bring some progress toward lower tariffs.

U.S. April final wholesale inventories expected to come in unchanged vs. flash at 0% m/m; wholesale trade forecast up 0.2% m/m from 0.6% m/m – watching for a further surge on tariff pause.

U.S. May New York Fed 1y consumer inflation expectations expected to come in at 3.6% y/y from 3.63% y/y; keeping inflation anchored is key for FOMC policy.

Mexico May CPI expected to come in at 4.1% y/y after 3.93% y/y; this is key for the pace of further Banxico cuts.

Mood: Risk-on mood continues, with iFlow Mood edging higher, driven by easing flight-to-quality bid in core sovereign bonds, while strong demand for equities maintained.

FX: Notable flows were MXN, THB and AUD outflows against KRW and DKK inflows. iFlow showed broad easing in G10 currency scored holdings, against increments for LatAm and EMEA currencies. Holdings in APAC were mixed, with narrowing CNY underheld while TWD shifted deeper into underheld territory.

FI: U.S. Treasurys and New Zealand, Brazil and Mexico government bonds recorded the most demand, while euro and Australian sovereign bonds were most sold.

Equities: U.S., Czech and South African equities were sold, against strong buying for Poland, New Zealand, South Korea, Hungary and Türkiye. Globally, consumer discretionary and industrial sectors were most sold, against greatest demand for the utilities and financials sectors.

“The signal is the truth. The noise is what distracts us from the truth.” – Nate Silver

“Ten people who speak make more noise than ten thousand who are silent.” – Napoleon Bonaparte

Sweden’s central government recorded a surplus of SEK 51.5bn in May, slightly above the Debt Office’s forecast of SEK 50.1bn, which was primarily due to lower net lending. The primary balance was SEK 5.3bn below expectations, as several agencies disbursed more funds than anticipated, though tax revenues exceeded estimates by SEK 1bn. Net lending to government bodies was SEK 6.5bn less than forecast, partly because agencies like the Defence Materiel Administration and Pensions Agency made larger-than-expected deposits. Interest payments were SEK 0.2bn below projections. Over the past 12 months, the government posted a SEK 88.5bn deficit, with total debt at SEK 1,105.8 bn. OMX -0.003% to 2521.435, EURSEK -0.137% to 10.9734, 10y Swedish GB +2.5bp to 2.333%.

Swedish households’ home price expectations remained stable in June, with SEB’s house price indicator rising slightly from +34 to +35. The proportion expecting prices to rise increased to 49%, while 14% foresee a fall. Households now forecast a Riksbank policy rate of 2.39% in one year, down 0.04 percentage points from May. The proportion planning to fix their mortgage rate dropped to 9%, reflecting expectations of lower interest rates. Regionally, sentiment was mixed. The overall result reflects resilient price optimism despite broader economic concerns and shifting interest rate expectations.

Japan posted a current account surplus of ¥2.26tn in April 2025, up 3.2% y/y. This was driven mainly by a solid primary income surplus of ¥3.59tn, despite a 9.6% y/y contraction. The goods and services balance recorded a deficit of ¥800.9bn, widening 41.5% y/y. Exports rose 4.0% y/y to ¥8.77tn, while imports fell 2.9% y/y to ¥8.80tn. The services deficit remained deep at ¥768.1bn, as outbound travel receipts improved but were offset by persistent deficits in other services. The financial account showed net outflows of ¥2.51tn, with large portfolio investment outflows offset by strong inflows from other investments. Seasonally adjusted, the current account narrowed to ¥2.31tn from March’s ¥2.72tn. Nikkei +0.919% to 38088.57, USDJPY -0.539% to 144.07, 10y JGB +1.3bp to 1.468%.

Japan May Eco Watchers current conditions improved from 42.6 to 44.4, where sentiment on housing sectors was up the most, at 46.0 (April: 39.7). Eco Watchers expectations rose to 44.8 (April: 42.7) with a solid rebound in the manufacturing sector to 44.9 (April: 40.3) and non-manufacturing sector expectations at 45.9 (April: 43.2). Elsewhere, Japan May Bank lending excluding trust grew 2.6% y/y.

New Zealand Q1 volume of total manufacturing sales surged 2.4% q/q, the best quarterly gain since Q3 2022. At 3.67% y/y, this is the best y/y growth since Q1 2021. The value of total manufacturing rose $1.7bn or 5.1% q/q vs. an upwardly revised 3% in Q4 2024. New Zealand Q1 total actual filled jobs were 2.26 million, down -0.1% q/q vs Q4 2024. This is the fourth quarterly decline in filled jobs. Elsewhere, the Reserve Bank of New Zealand’s Chief Economist Paul Conway gave a dovish assessment of the New Zealand economy, saying that the labor market is a bit softer than that when you look across a whole range of labor market indicators, including people changing jobs. NZX 50 -0.193% to 12539.26, NZDUSD +0.832% to 0.6063, 10y NZGB +2.5bp to 4.648%.

China May PPI dropped more than expected, from -2.7% y/y to -3.3% y/y. Within production, PPI was -11.9% y/y for mining and quarry excavations, -5.4% y/y for raw materials and -2.8% y/y for processing. On the consumer goods side, PPI came in at -1.4%, with food at -1.4% y/y, daily use articles at +0.6% y/y and durable consumer goods at -3.3% y/y. The NBS highlighted that prices of high-tech items are on the rise. CSI 300 +0.291% to 3885.25, USDCNY -0.128% to 7.1834, 10y CGB -0.4bp to 1.689%.