Market Movers: Shaken

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

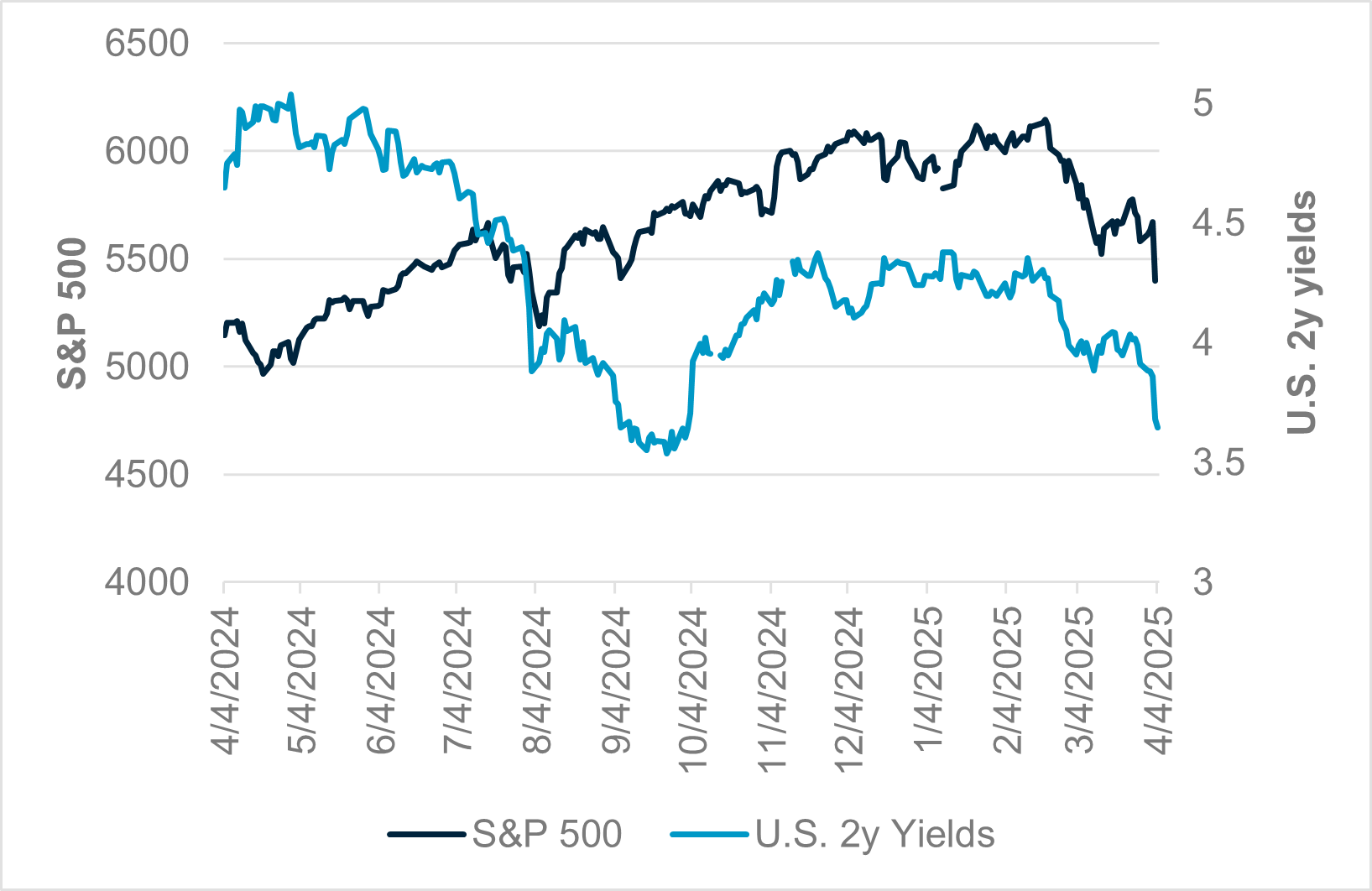

EXHIBIT #1: S&P 500 AND U.S. 2Y YIELDS BOTH MOVE IN SAME DIRECTION

Source: BNY

The return of risk aversion globally shifts the focus from inflation to growth, with the S&P 500 downturn driving up expectations for Fed rate cuts. This will be the focus on the day for Powell’s speech.

Risk sentiment has worsened as U.S. tariffs drive global growth expectations lower. Markets have been shaken by the announcement of tariffs and the reactions to them are ongoing. Banks in Japan suffered notably overnight despite the Asahi report of a government extra-budget plan to counter tariff pain. And despite some relief at the confirmed impeachment of Yoon Suk Yeol, South Korea saw shares lower while holidays in Hong Kong, Thailand and Singapore keep liquidity light in APAC. Europe opens weaker and waits for EU retaliation to U.S. tariffs with Macron urging companies to halt investments in the U.S. European banks led the decline across the regional bourses. The offset of bonds continues to play out on hopes central banks will ease and make some difference on growth. The notable overnight leader comes from U.S. yields down by 7.5bp to 3.95% for 10-year notes. The open talk of a target yield of 3.60% and FOMC easing in May is connected to U.S. jobs data being released today. Some are asking whether the data matter if they are strong and if they will add to fears of a recession if they prove weaker. The uncertainty over tariffs and the risk to growth vs. inflation make Chair Powell’s speech on the economy the main event for closing out a historic week for all asset classes.

South Korea Constitutional Court unanimously upholds the impeachment of President Yoon Suk Yeol over his declaration of martial law on December 3, 2024. The impeachment took effect immediately, which require the country to hold a snap presidential election within 60 days or by June 3, 2025. KOSPI -1.8%, 10y KTB -2bp lower at 2.71%, KRW +1% at 1437.

India March final HSBC Services PMI 58.5 from 59.0 – better than 57.7 flash – the 44th consecutive month of growth, but with inflationary pressure slowing. Output charges fell to 3½-month lows with international orders weakest gains in 15 months. RBI easing will continue. Sensex off 0.96%, GIND 10y off 1.7bp to 6.48%, INR up 1% to 85.216.

Japan February real household spending declined by -0.5% y/y from +0.8% y/y in January. Spending on food was down 4.5%y/y, while spending on fuel, light and water charges and transportation and communications were higher at 7.6% y/y and 4.6% y/y, respectively – inflation still hitting households, tariff pain showing up in bank shares, Nikkei off -4%, 10y JGB 18bp lower at 1.19%, JPY +0.9% 145.4.

Australia February household spending grew at 3.3% y/y from an upwardly revised 3.2% y/y in January 2025. It is also the fifth straight monthly gain. The top contributing sectors are Health (+7.8% y/y) and Recreation and Culture (+5.1% y/y). Services spending was 5.2%y/y while goods spending was up 1.7% y/y – supports RBA easing pause. ASX200 off -2.4%, 10y ACGB -6bp at 4.20%, AUD -1.5% at 0.624.

German February factory orders stabilize 0% m/m, +0.7% m/m with bounce back in big transport – ships, trains and aircraft. But orders lower for consumer goods. Domestic orders fell 1.2% while foreign orders were up 0.8% – recovery in German manufacturing still in early stages with outside demand dominating, put at risk by tariffs. DAX off 1%, Bund 10y off 9.5bp to 2.555%, EUR off 1.2% to 1.1005.

The CPIF -0.5% m/m, 2.3% y/y from 2.9% y/y – also better than the 2.6% y/y expected – the first drop since August. The headline CPI fell to 0.5% y/y – lowest since December 2020. Riksbank has room to act on tariffs if it needs to. OMX off 1.05%, SGB2 off 13.5bp to 2.43%, SEK 9.9070 up 1%.

US March nonfarm payrolls expected up 140k after 151k with a focus on unemployment, with the rate expected to be flat at 4.1%, average hourly earnings up 0.3% m/m and the participation rate unchanged at 62.4%.

Fed Chair Powell speaks on the economic outlook at noon.

Mood: Heightened risk aversion with aggressive equities outflows. iFlow Mood moves further into negative territory – nearing extremes again.

FX: Volatile FX flows surrounding U.S. tariff announcement. Large CAD, GBP and MXN outflows were observed against significant USD and JPY inflows.

FI: Muted U.S. Treasurys flow. Eurozone, Chinese and Indian government bonds posted the strongest demand against selling pressure in LatAm and EMEA.

Equities: Aggressive selling across developed market against lighter outflows in emerging markets. All sectors were sold in global equities, led by the Communication Services and Consumer Discretionary sectors.

“Without craftsmanship, inspiration is a mere reed shaken in the wind.” – Johannes Brahms

“You can not shake hands with a clenched fist.” – Indira Gandhi

World FAO food prices in March flat m/m, up 6.9% y/y – wheat prices drop despite trade worries and tighter supplies. Declines in cereals and sugar price indices offset increases in those of meat and vegetable oils, while the dairy price index remained stable.

Philippines March Inflation posted second month-on-month drop at 0.2% m/m. Year-on-year, March inflation dropped to 1.8% y/y, the lowest since May 2020 while core inflation eased from 2.4% y/y to 2.2% y/y. Food (2.2% y/y) and transportation (-0.1% y/y) posted the largest declined compared with February. Rice inflation continues to drop to -7.7% y/y from as high as 24.4% y/y in early 2024.

Singapore February retail sales and ex-auto retail sales both posted sharp decline at –3.6% y/y and -6.7% y/y from 4.7% and 5.1% y/y in January 2025, respectively. STI down -3%, 10y SIGB 8bp lower at 2.47%, SGD +0.4% at 1.332.

Thailand March headline and core inflation dropped below 1% at 0.84% y/y and 0.86% y/y, respectively, primarily led by lower transportation component at 0.5% y/y (February: 2.1% y/y).

India March final HSBC Services PMI 58.5 from 59.0 – better than 57.7 flash – the 44th consecutive month of growth in services activity. The slowdown reflected a softer increase in services activity, with foreign sales growing the least since December 2023. Output continued to grow, supported by buoyant underlying demand and ongoing increases in new business. Employment increased, albeit at the weakest rate in close to a year, while outstanding business rose slightly. On the price front, input cost inflation eased to a five-month low. As a result, output cost inflation slowed to the weakest level since September 2021 amid competitive pressures. Looking ahead, business sentiment remained positive but slightly weakened compared to February.

German February factory orders stabilize at 0% m/m, +0.7% m/m after -5.5% m/m, -0.5% y/y – weaker than the 3.5% m/m, 0.3% y/y expected. Gains in demand for aircraft, ships, trains, military vehicles (3.8%), mechanical engineering (3.4%) and the automotive industry (0.6%) were offset by declines in metal products (-7.4%), electrical equipment (-5.9%), and pharmaceuticals (-5.9%). New orders shrank for consumer goods (-5.2%), and intermediate goods (-1.3%) but increased for capital goods (1.5%). Domestic orders dropped by 1.2%. However, foreign orders rose 0.8%, with demand declining from the euro area (-3.0%) while expanding from outside the euro area (3.4%). Excluding large orders, incoming orders edged down 0.2% from January. In a three-month comparison, new orders from November 2024 to January 2025 were 1.6% lower than in the previous three months.

French March industrial production rose 0.7% m/m, -1% y/y after -0.5% m/m – better than 0.3% m/m expected – the first growth in French industrial activity in six months, driven by a sharp recovery in manufacturing output (+1.4% vs. -0.5% in January), particularly in machinery and equipment goods (+3.1% vs. -3.2%) and other manufacturing products (+1.2% vs. -0.4%). At the same time, construction activity rebounded by 1.6%, following a 1.7% decline in the previous month. Meanwhile, output in mining and quarrying, energy, water supply, and waste management continued to fall, slipping 2.2% after a 0.1% drop in January.

Sweden March CPI off -0.7% m/m, +0.5% y/y after 0.6% m/m, 1.3% y/y – less than the -0.4% m/m, +0.8% y/y expected. The CPIF -0.5% m/m, 2.3% y/y from 2.9% y/y – also better than the 2.6% y/y expected – the first drop since August for monthly CPIF. This marks the lowest reading since December 2020 and the eighth consecutive period with inflation below the Riksbank’s 2% target. On a monthly basis, consumer prices fell 0.7%, the first decline since last August, exceeding the expected 0.4% drop and reversing a 0.6% gain in February. Meanwhile, the CPI with a fixed interest rate (the Riksbank’s target measure), eased to 2.3% in March from a one-year high of 2.9% in the prior period, falling short of market expectations of 2.6%.