Market Movers: Running Out

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

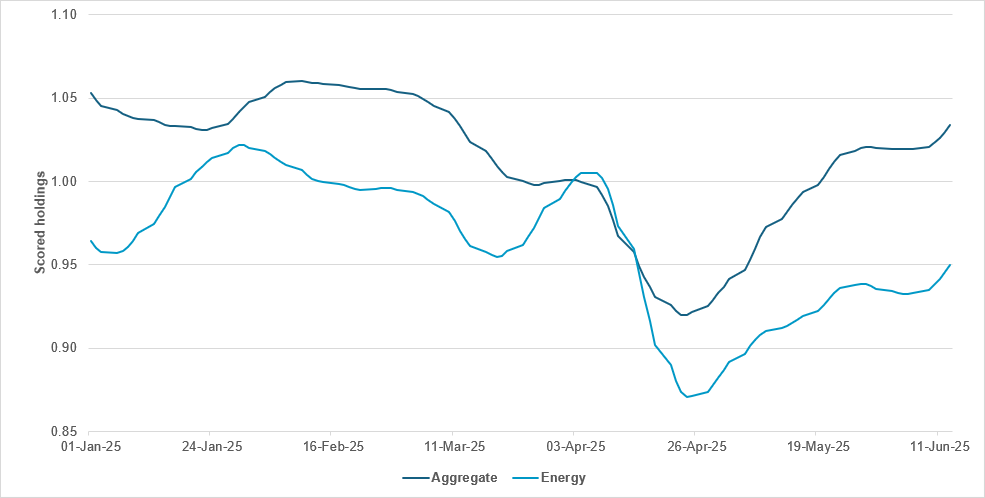

EXHIBIT #1: DESPITE OIL PRICE CONCERNS, GLOBAL ENERGY SECTOR HOLDINGS GAP VS. TOTAL NOW WIDEST YEAR-TO-DATE

Source: BNY

Oil prices remain volatile due to the situation in the Middle East, but the equity market is not anticipating any meaningful re-rating of the sector. The equity markets are looking through the conflict for now. The potential OPEC+ supply expansion has helped anchor prices. In the event of major logistical disruptions for sea-based oil tankers, the potential shock to growth at a time when sentiment-related data is already deteriorating could be severe. The corresponding demand weakness could limit the net effect on prices and leave limited scope for energy companies to look for an earnings lift; the current environment is very different to the 2022 supply shock, when the global economic cycle was still in the early stages of an upswing. The slight recovery in prices in recent sessions has helped lift holdings of energy companies globally, but this is also taking place amid a global recovery in risk appetite as high-beta sectors such as technology and communication sectors recover to pre-“Liberation Day” highs. Consequently, the holdings gap between the energy sector and aggregate equity holdings has hit its highest level in a year. The only point of convergence this year was around “Liberation Day”, when other high-performing sectors corrected aggressively. A shift in global demand dynamics remains a necessary condition for the energy sector to start performing of its own accord. With the IEA announcing overnight that oil demand growth will slow to “a trickle” beyond 2026, such prospects are not great.

Risk sentiment is lower, as the conflict between Israel and Iran extends into its fifth day. Oil is higher, global bonds lower and USD higher after President Trump left the G7 summit early. The BoJ is on hold, with the expected bond roll-off taper not enough to help JGB rally. The improved German and EU ZEW sentiment kept Bund yields higher, but did not help shares. Meanwhile the US Senate’s version of the tax bill expands business tax breaks, repeals some clean energy tax credits, leaves SALT at $10k and cuts more from Medicaid – all of which suggests a tougher reconciliation with the U.S. House. Beyond watching oil prices and the political drama, markets are also keeping a close eye on rates. The FOMC meeting starts today, with the focus on the dot plot and risks of a subtle shift-up; just one cut is expected this year. Despite this, bond yields are lower, as demand worries beat out a wait-and-see stance. Finally, and perhaps most importantly, trade continues to rise back up the list of worries, as the EU spurns the planned economic dialogue with China given the lack of progress on trade issues. Throw in that Japan’s talks with the U.S. haven’t yet produced a deal, and many are watching July 9 as another event risk for tariff troubles. The overall mood seems unlikely to improve given expectations of weaker economic data, with both U.S. retail sales and industrial production forecast to have been soft in May. U.S. inventories are perhaps most important for understanding whether the storyline of trading risk around U.S. growth will shift: the expectations is for flat numbers, but negative surprises could shift inflation fears as cheaper supplies run out. This sense of urgency around markets today suggests something bigger is brewing, driving a running out of previous positioning for melt-ups and status quo complacency across markets.

Donald Trump left the G7 summit in Canada early amid escalating conflict between Israel and Iran, stating his departure was unrelated to ceasefire efforts despite claims by French President Emmanuel Macron. Trump dismissed Macron’s comments and hinted at a larger, unspecified reason for returning to Washington. Speaking later, Trump said he sought a “real end” to the crisis with Iran abandoning its nuclear ambitions. His exit came just before the G7 issued a joint call for regional de-escalation. Trump had initially resisted the G7’s statement and warned Tehran to evacuate. Meanwhile, Israel continued missile strikes on Iran, prompting Iranian retaliation, with casualties on both sides. S&P Mini -0.554% to 6056, DXY +0.198% to 98.192, 10y UST -2bp to 4.426%.

As expected, the Bank of Japan has announced that it is to slow the pace of tapering its bond purchases to avoid destabilizing the JGB market. Monthly purchases are currently being cut by ¥400bn every three months until March 2026; reductions will now slow to ¥200bn per quarter from April 2026, targeting ¥2.1tn/month by March 2027. BoJ Governor Ueda stated overnight that he couldn’t comment “on the likelihood of a near-term rate hike,” expressing a preference to monitor “hard data” before mulling the next hike. He also emphasized the need for yields to reflect market forces, while warning against moving too quickly. The BoJ kept short-term rates at 0.5% and pledged to respond “nimbly” to sharp rises in long-term yields. Despite the slower pace of tapering, bond holdings are projected to fall 17% by March 2027. Nikkei +0.588% to 38536.74, USDJPY +0.097% to 144.89, 10y JGB +2.7bp to 1.465%.

The IEA forecasts global oil demand to rise by 2.5mn b/d between 2024 and 2030, reaching a plateau of 105.5mn b/d by the end of the decade. It expects China’s oil consumption to peak in 2027 due to surging electric vehicle sales, expanded high-speed rail and a shift to natural gas. The IEA projects that EVs will displace 5.4mn b/d of oil demand by 2030. It also sees demand from fossil fuel combustion peaking as early as 2027, while petrochemicals emerge as the main driver of oil demand growth from 2026. As petrochemical feedstocks rely less on refined products, the IEA expects refinery overcapacity and further closures by 2030. Brent +1.448% to 74.29, WTI +1.352% to 72.74.

Investor confidence in Germany surged in June, with the ZEW expectations index jumping to 47.5 from 25.2 in May. This was well above the Bloomberg survey median of 35. The ZEW’s current conditions index also improved. ZEW President Achim Wambach attributed the optimism to anticipated fiscal stimulus from the new German government, which he said could finally end nearly three years of economic stagnation. He also highlighted the recent ECB rate cuts as a contributing factor. Markets appear to be looking past potential headwinds, including possible U.S. tariffs, in favor of a domestic public spending boost. DAX -1.108% to 23436.42, EURUSD -0.061% to 1.1554, 10y Bund +1.4bp to 2.541%.

U.S. May retail sales are expected to fall -0.6% m/m from +0.1%, while the ex-auto figure is expected to come in at 0.2% m/m from 0.1% in April.

U.S. May import prices index and ex-petroleum prices are expected to ease -0.2% and 0.1% m/m from 0.1% and 0.4% m/m, respectively.

U.S. May industrial production expected to be flat for the second month running; manufacturing production is forecast to rebound from -0.4% in April to +0.1% in May.

U.S. April business inventories are forecast to shrink to 0% from 0.1% in March.

U.S. June NAHB Housing Market Index is expected to edge higher to 36 from 34.

BCC decision – the Central Bank of Chile is expected to keep its benchmark rate steady at 5.00%, maintaining a cautious stance amid persistent inflation and external uncertainties.

Mood: iFlow Mood eased for the second day as risk aversion took hold, with a pick-up in core sovereign bond demand. Equity buying slowed slightly.

FX: Outflows in APAC and EMEA against buying in G10 and LatAm. The most significant flow was PLN outflows, while NOK and JPY saw good buying.

FI: Mixed sovereign bond flows. There was demand for U.S. Treasurys and euro and Japanese government bonds, while selling pressure was observed in U.K. gilts and Colombian and South Korean government bonds. Corporate bonds were broadly sold.

Equities: Mixed flows, with a selling bias in EM EMEA and EM America against buying flows in developed markets. South African, Norwegian and Malaysian equities were most sold.

“We didn’t lose the game; we just ran out of time.” – Vince Lombardi

“The only time you run out of chances is when you stop taking them.” – Alexander Pope

Sweden’s unemployment rate rose to 9.7% in May 2025, up 1.0 percentage points from a year earlier, with 561,000 people unemployed. Among women, the rate surged 2.0 percentage points to 10.3%, while the rate for men was 9.1%. Youth unemployment remained elevated at 28.6%, with 158,000 full-time students among the 203,000 jobless aged 15-24. Seasonally adjusted data showed a national unemployment rate of 8.7% and youth unemployment at 23.3%, both down from recent months. Employment rose to 5.23 million, up 75,000 y/y, driven by an 81,000 increase in permanent employees to 4.19 million. The labor force expanded by 110,000 to 5.79 million, with participation up 1.1 percentage points to 76.0%. Total weekly hours worked averaged 167.4 million. OMX -0.868% to 2463.739, EURSEK +0.059% to 10.9725, 10y Swedish GB +1.5bp to 2.357%.

Statistics Norway published its latest economic forecasts showing steady unemployment and moderating inflation ahead. The unemployment rate is expected to hold at 4.1% through 2025-2026 before easing to 4.0% in 2027 and 3.9% in 2028. The money market rate is forecast to fall from 4.4% in 2025 to 3.8% in 2026 and stabilize at 3.5% in 2027-2028, reflecting expectations of monetary easing. Mainland GDP growth is projected at 1.7% in 2025, slowing slightly in 2026 (1.5%) before picking up to 2.1% in 2027. Wage growth is set to decelerate from 4.4% to 3.5% over the forecast horizon, while CPI inflation eases from 2.8% to 2.4%. House price growth is also expected to slow significantly, from 5.5% in 2025 to 3.1% by 2028. OSE +0.074% to 1634.67, EURNOK -0.144% to 11.4422, 10y NGB +1.1bp to 4.109%.

Hungary’s average gross earnings rose by 9.8% y/y in April 2025 to HUF 708,300, while net earnings increased by 9.6% to HUF 486,500. Real earnings were up 5.2%, reflecting a 4.2% rise in consumer prices. Regular gross earnings (excluding bonuses) grew by 10.3% to HUF 657,800, with rises of 10.7% in the business sector, 8.4% in the budgetary sector and 11.8% in the non-profit sector. Median gross and net earnings also climbed by 10.2%, reaching HUF 564,800 and HUF 392,700, respectively. Overall, wage growth remained robust across sectors, outpacing inflation and driving solid real income gains. Budapest SI +0.993% to 96748.32, EURHUF +0.199% to 403.08, 10y HGB -4bp to 7.12%.

South Korea’s export and import prices declined sharply in May 2025, with the export price index falling 3.4% m/m and 2.4% y/y and the import price index down 3.7% m/m and 5.0% y/y. Amid lower prices, trade volumes rose, with the export volume up 2.5% y/y and import volume up 1.3%. However, export value fell 1.9% y/y and import value declined more steeply, down 6.3%. As a result, the net barter terms of trade index improved by 3.4% y/y, while the income terms of trade figure rose 6.0%. The falls in import prices were particularly sharp for raw materials (-14.1% y/y), especially coal and petroleum products. KOSPI +0.124% to 2950.3, USDKRW +0.475% to 1365.55, 10y KTB +2.5bp to 2.87%.

New Zealand May food prices were up 0.5% m/m and surged to 4.4% y/y from 3.7%. This will likely exert upward pressure on the upcoming Q2 CPI release (last reading at 2.5%). Higher prices for the grocery food group and the meat, poultry and fish group contributed most to the annual rise in food prices, up 5.2% and 5.4%, respectively. NZX 50 -0.4% to 12639.34, NZDUSD +0.099% to 0.6067, 10y NZGB -1.8bp to 4.605%.