Market Movers: Rulings

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 10 minutes

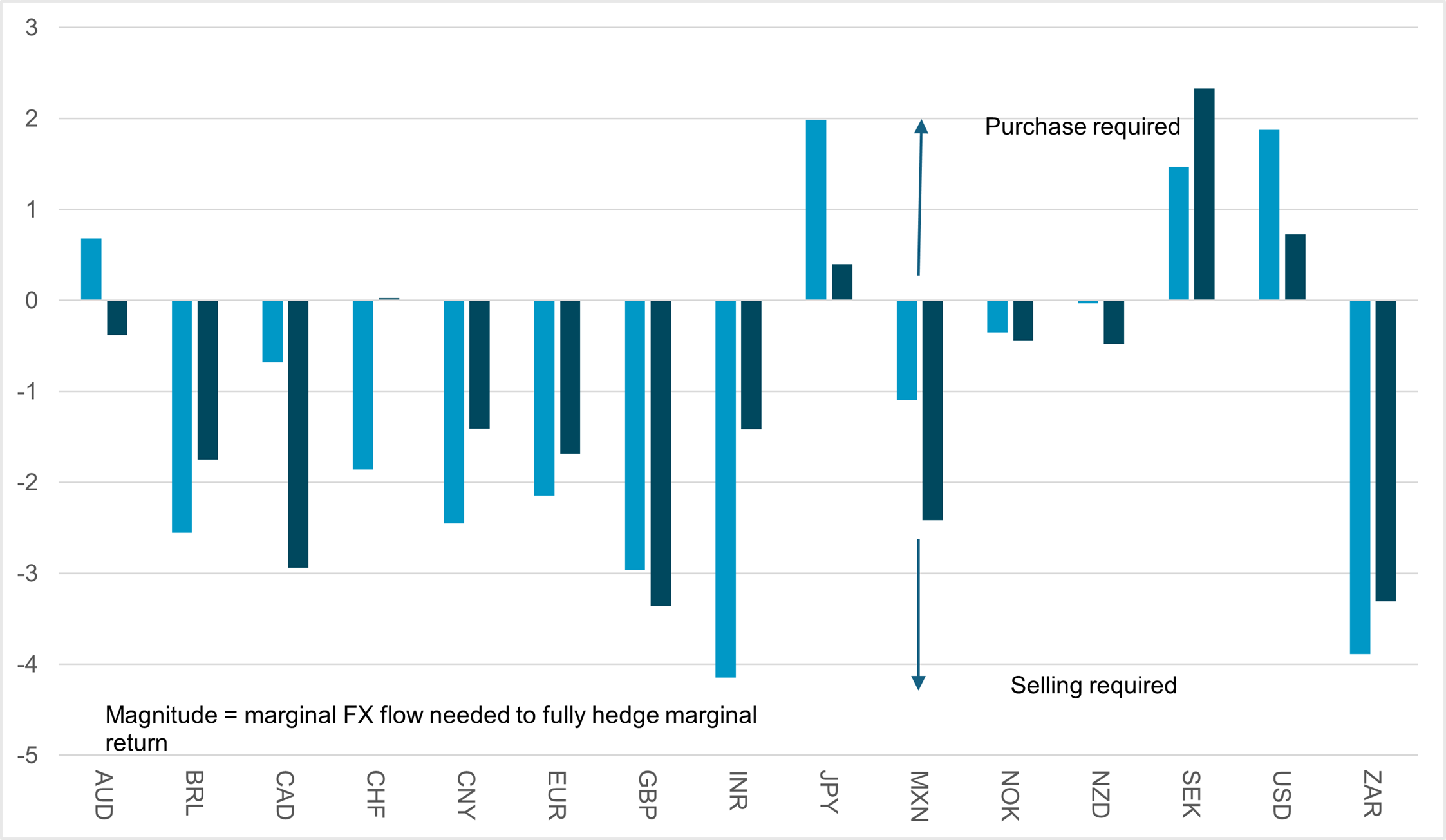

EXHIBIT #1: MONTH-END REBALANCING SUPPORTS LIGHT DOLLAR PURCHASES

Source: BNY

The main strategy heading into month end can be characterized as simply “the reversal of the reversal.” Sentiment improved markedly throughout the month due to détente on trade between the U.S. and multiple partners. Risks are not gone but we believe that sufficient hedging has now taken place through dollar sales accompanying recovery flows into U.S. assets. However, based on both aggregate and cross-border realized flow figures, we find that the dollar was still the worst performer (on a cross-border basis), indicating that the dollar was also being used to fund additional risk exposures elsewhere. Looking at the best-bought names on both an aggregate and a cross-border basis, GBP, EUR and CNY led the way. These could be considered “alternatives” to the dollar in a reserve management sense, but we believe that flows were more active in reflecting gains in underlying asset exposures. Based on equity rebalancing, GBP, CAD and ZAR face sales, as U.K., Canadian and South African equity markets have high levels of commodity and energy exposure. If concerns over global stagflation continue heading into quarter-end, these markets will be seen in a more positive light despite demand stress, as cheaper currency valuations will encourage additional cross-border flows. Fixed income-driven rebalancing is the core feature of the month, with liquid names such as the EUR, GBP and CNY complementing sales in INR and BRL. ZAR should face selling pressures as well given its bond market is modestly positive. Pressure on the CNY is expected based on the comprehensive asset inflows into the country in recent weeks alone, and we also stress that fundamentals do not support excessive CNY appreciation as risks to price pressures remain to the downside. The selling of these currencies with heavy weights in the USD’s trade-weighted index will help lift USD holdings, indicating a better-positioned dollar ahead of key events next month.

Risk sentiment surges back to positive with the U.S. federal court ruling against reciprocal tariffs providing relief in Asia. NVIDIA’s earnings also helped tech shares as the company beat expectations despite Chinese restrictions on chip sales. Although it was expected, the rate cut by the BoK also helped, with the focus now turning to the South Korean election on June 3. The reality of the ruling is more complicated than the reaction by markets. The U.S. has ten days to halt collection of tariffs and determine what to do with the funds it has already received. The U.S. could work around reciprocal tariffs and target sectors instead or consider other bilateral actions. In addition, the ruling will likely be appealed and slowly make its way to the Supreme Court. The uncertainty of trade deals vs. tariffs looks slightly different today, but that doesn’t change how the Trump administration sees the world or its policy. Rulings may change the timing of the tariff pause but not the rhetoric around global trade. Watching markets at month-end is also difficult because of rebalancing, as noted in our FX commentary today. USD buying should be expected, and dissecting the move up today on the back of tariff slowdowns may be a false signal. The key drivers beyond the rebalancing today will be wrapped around GDP revisions, Fedspeakers, jobless claims and home sales. The fundamental drivers for all markets despite rulings remain in the forward expectations for growth and inflation. The bond markets may be more important to consider given the break back over 30y 5% and given that the revenue expectations from tariffs make any “big, beautiful” tax bill in the Senate more difficult to pass. While many will find solace in equity markets globally, rates will require more effort to rally back to calmer ranges.

A U.S. court has ruled that Donald Trump’s “Liberation Day” tariff scheme is illegal, stating he exceeded his authority under emergency economic powers. The Court of International Trade declared the April 2 executive orders imposing global tariffs invalid, dealing a major blow to Trump’s trade agenda. The decision, following lawsuits from small businesses and U.S. states, excludes existing sectoral tariffs on steel and cars. The White House plans to appeal but faces mounting opposition from Congress and business groups. Financial markets rallied on the news. The ruling challenges Trump’s use of emergency powers to justify tariffs, which had disrupted supply chains and raised consumer costs. S&P Mini 1.533% to 5993.25, DXY +0.198% to 100.072, 10y UST +4.6bp to 4.523%.

Bank of Korea cut rates by 25bp to 2.5% to mitigate downward pressure on the economy. BoK lowered both GDP and CPI forecast with 2025 GDP below 1% at 0.8% and 2026 GDP at 1.6%. Headline CPI for 2025 is seen as unchanged at 1.9%, while core inflation is slightly higher, increasing from 1.8% to 1.9%. The BoK Board unanimously judged that a base rate cut was appropriate due to significantly weakening economic growth and stable inflation. While concerns about rising household debt and exchange rate volatility persist, the rate cut aims to alleviate downward economic pressure. The Board also acknowledged the potential need for larger future cuts, depending on incoming data, while emphasizing the importance of monitoring financial stability risks. KOSPI +1.891% to 2720.64, USDKRW +0.04% to 1375.75, 10y KTB -0.3bp to 2.702%.

Fitch Ratings said that Japan issuers appear resilient to super-long bond yield spike. A sharp rise in “super-long” Japanese government bond (JGB) yields would be unlikely to have a major impact on rated Japanese issuers’ credit profiles in the near term, says Fitch Ratings. The major Fitch-rated Japanese banks’ JGB holdings have short average maturity of around one to three years, limiting the effect of shifts in super-long yields. Risks may be higher among regional banks, which collectively have longer average JGB maturity. Japanese life insurers’ yen-denominated liabilities and bonds are both recognized at book value using amortized costs under Japanese GAAP, rather than being marked to market. Consequently, there is little direct impact from fluctuating JGB yields on their capitalization or earnings. Nikkei +1.884% to 38432.98, USDJPY +0.353% to 145.35, 10y JGB +1.4bp to 1.529%.

The U.S. is escalating its crackdown on Chinese students by revoking visas of those linked to the Chinese Communist Party or studying sensitive fields, according to Secretary of State Marco Rubio. This move, part of the Trump administration’s broader effort to tighten scrutiny of foreign students, follows a pause in U.S.-China tariff tensions and could strain relations further. The action affects thousands and includes halting student visa interviews globally. Critics argue the decision is discriminatory and harmful to U.S. universities, where Chinese students are a major source of revenue. The policy continues Trump first time efforts to limit China’s influence in U.S. academia and national security. CSI 300 +0.586% to 3858.7, USDCNY -0.08% to 7.1902, 10y CGB +0.7bp to 1.716%.

U.S. Q1 GDP (second estimate) consensus unchanged at -0.3% vs. first estimate focus on any personal consumption revisions and core PCE.

U.S. weekly jobless claims forecast higher at 230k vs. 227k last week, with continuing claims expected own 10k to 1.893mn.

U.S. April pending home sales are expected to drop -1.0% m/m after 6.1% gain in March.

Fedspeakers: Richmond Fed President Barkin participates in a fireside chat, Chicago Fed President Goolsbee participates at the bank’s 2025 Mackinac Policy Conference, Fed Governor Kugler gives opening remarks at 5th Annual Federal Reserve Board Macro-Finance Workshop, San Francisco Fed President Mary Daly speaks at a fireside chat at the Oakland Rotary Club.

South Africa Reserve Bank rate decision consensus for 25bp rate cut to 7.25%.

Mood: iFlow Mood has shifted to risk-on mood, with accelerated equities demand while sovereign bonds buying eases.

FX: CNY, KRW and PEN posted significant inflows. Overall strong FX demand with pockets of outflows, notably in USD and SEK.

FI: Australia and Eurozone government bonds were most sold along with cross-border selling pressure in U.S. Treasurys. Elsewhere, flows in LatAm and APAC were mixed with buying in China sovereign bonds and selling across LatAm region.

Equities: DM APAC equities were sold against buying in the rest, especially in EM EMEA, particularly in South Africa. China and Hong Kong continue to draw good demand, while Japan, Canada and Hungary equities were most sold.

“To know your ruling passion, examine your castles in the air.” – Richard Whately

“Rhetoric is the art of ruling the minds of men.” –- Plato

South Africa’s annual producer price inflation for final manufactured goods remained steady at 0.5% in April, with a monthly increase of 0.5%. The primary contributor was food, beverages and tobacco products, which rose 4.7% y/y. Intermediate manufactured goods rose 8.5% annually and 2.4% monthly, driven by basic and fabricated metals. Electricity and water saw the highest annual rise at 11.2%, mainly due to a 12.5% increase in electricity prices. Mining PPI rose 4.1% annually, supported by gold and metal ore prices. Agriculture, forestry and fishing recorded a 4.4% annual increase, led by a 4.7% rise in agricultural products. JSE TOP40 +0.399% to 86590.32, USDZAR +0.095% to 17.9472, 10y SAGB -0.3bp to 10.341%.

In the three months through March 2025, private new capital expenditure (capex) in Australia fell by 0.1% and was 0.5% lower y/y. Non-mining investment declined 0.9%, while mining rose 1.9%. Equipment and machinery capex dropped 1.3%, led by a 17.9% fall in information media & telecommunications. This followed a strong 19.8% rise in the three months through December. Spending on buildings and structures rose 0.9%, driven by mining projects in oil, gas, and metals. State-level declines were led by Victoria (-5.3%) and the Northern Territory (-13.2%), while South Australia (+11.1%) posted the largest rise. Businesses revised up expected capex by 2.2% for 2024–25 and 5.6% for 2025–26. ASX -0.101% to 4730.29, AUDUSD +0.156% to 0.6436, 10y ACGB +4bp to 4.372%

Japan May consumer confidence rebounded from 31.2 to 32.8 after five months of decline. The percentage of the group who expect "Go up" in May was 93.6%, an increase of 0.4% points from the previous month. Nikkei +1.884% to 38432.98, USDJPY +0.353% to 145.35, 10y JGB +1.4bp to 1.529%.

New Zealand ANZ May Activity Outlook and Business confidence collapsed to 34.8 (47.7) and 36.6 (49.3) respectively to the lowest levels since Q3 2024, but remain at an elevated level. Pricing and cost indicators eased with 1-year inflation expectation rose to 2.71% from 2.65%. Employment intentions dropped from 18.1 to 6.0. NZX 50 -0.655% to 12281.31, NZDUSD -0.135% to 0.5959, 10y NZGB +1.6bp to 4.635%.

Taiwan’s Central Bank released its 19th Financial Stability Report, covering developments from early 2024 to April 2025. Key highlights include stable domestic growth and easing inflation, though housing affordability remains a concern despite a cooling real estate market. U.S. tariff policy has heightened global uncertainty, potentially weakening Taiwan’s economic momentum and affecting corporate and household debt repayment. Taiwan’s financial system remains broadly stable, with strong bank profits and capital levels. Life insurers saw a significant rebound in profitability and improved capital adequacy, though they face elevated market risk due to large domestic and overseas investment exposures. In response to external shocks, the government introduced a NT$93bn industrial support package, while the central bank implemented rate hikes, FX interventions and liquidity measures to preserve financial stability. TAIEX -0.049% to 21347.3, USDTWD +0.067% to 29.917, 10y TGB -0.5bp to 1.57%.

Türkiye’s foreign trade deficit widened significantly in April. Exports rose by 7.8% y/y to $20.8bn, while imports increased by 12.7% to $32.9bn, resulting in a trade deficit of $12.1bn – a 22.3% annual increase. For the January-April period, exports grew 3.7% and imports 6.6%, pushing the deficit up 14.7% to $34.6bn. Excluding energy and non-monetary gold, exports and imports rose 11.1% and 13.5%, respectively. The manufacturing sector accounted for 94.4% of total exports, while intermediate goods made up 69.4% of imports. Germany remained the top export destination, and China was the leading import source. BI 100 +0.104% to 9187.2, USDTRY +0.034% to 39.1124, 10y TGB -2bp to 33.02%.

Hungary recorded an external trade surplus of EUR 1.4bn in April. Compared to March, seasonally adjusted exports rose by 3.4% and imports by 1.1%. Year on year, export volume fell by 2.3% and imports by 0.1%, with the trade balance declining by EUR 354mn. Machinery and transport equipment exports rose 0.5%, while manufactured goods exports dropped 7.5%. Fuel and energy exports surged 39%, helping offset declines in other categories. Trade with EU countries showed a surplus, while extra-EU trade showed a deficit. From January to April, exports rose 0.5% and imports 1.9%, with a trade surplus of EUR 5.4bn, down EUR 267mn from the previous year. Budapest SI -0.188% to 96671.03, EURHUF +0.139% to 404.37, 10y HGB 0bp to 6.98%.

Consumer and business confidence in Italy improved in May. The consumer confidence index increased from 92.7 to 96.5, driven by improved perceptions of the general economic situation, with the economic climate rising from 89.6 to 97.5. All sub-indices – personal, current, and future – also improved. Business confidence rose from 91.6 to 93.1, ending a three-month decline. Gains were seen in market services (from 91.4 to 94.5), retail trade (101.8 to 102.8) and manufacturing (85.8 to 86.5), while construction declined (103.6 to 102.2). Confidence in tourism services notably rebounded. Overall, the rise reflects stronger sentiment in market services and modest improvements in retail and manufacturing. FTSEMIB +0.236% to 40222.42, EURUSD -0.231% to 1.1266, 10y BTP +2.1bp to 3.556%.