Market Movers: Risk and Reward

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 6 minutes

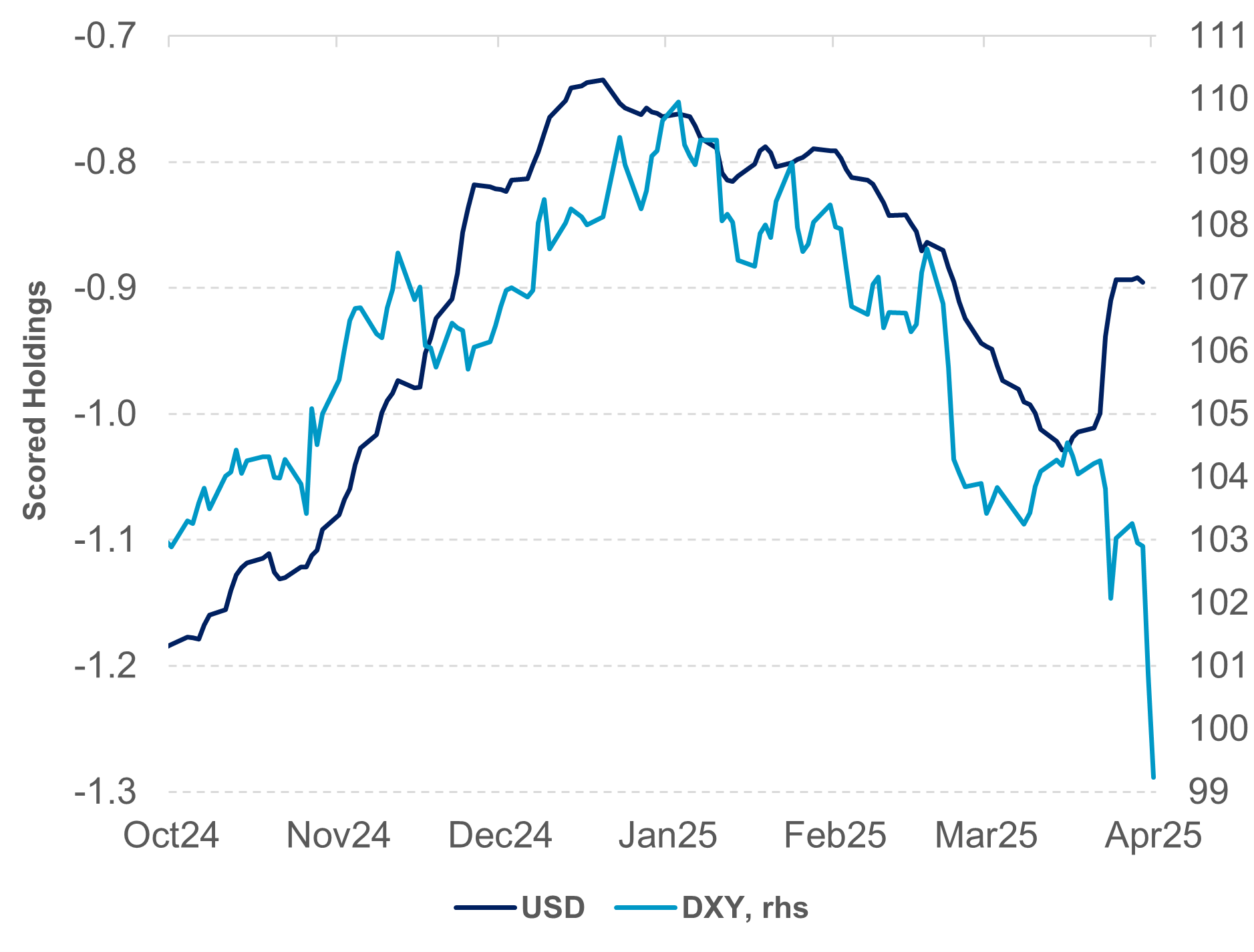

EXHIBIT #1: USD HOLDINGS AND THE USD INDEX

Source: BNY

The current selling of U.S. dollar has yet to unwind the U.S. safe haven hedging we saw in the middle of March onwards. iFlow data suggests there is more USD selling risk ahead.

Risk sentiment mixed as the shift in investor focus moves from equities to bonds and now turns to FX with the USD breaking a key support level back to July 2023 levels. The safe haven currencies are at decade highs with CHF leading while JPY is back to 6-month intervention highs. The bigger mover today is the EUR, which is up 0.1%, breaking 1.1300 back to February 2022 levels. The moves reflect doubts about the tariff policy as well as a push to diversify away from U.S. holdings. The U.S. exceptionalism trade continues to unwind. Overnight the focus was more on market moves than economics with South Korea KOSPI off nearly 1% in equities, Japan Nikkei off 4.3%, while Taiwan saw a reversal up 2%. China CSI 300 was -0.1% but Hong Kong HSI was up 0.56%. For Europe, the ongoing low CPI drive ECB rate cut expectations and growth. EU meetings today and talks with the U.S. look more even-footed and markets are seeing the EUR as a logical alternative to the USD. For the U.S. session, more data, with a keen focus on inflation expectations from the University of Michigan, sets the tone for rate markets. The main concern remains whether U.S. 10-year yields break and hold over 4.50% again as this seems to be the trigger for more Trump Administration reactions. The ability for U.S. markets to stabilize will require some matching of risk and reward and that appears to be dependent on policy shifts both from the President and the FOMC.

South Korea Ministry of Finance explicitly mentioned they are closely monitoring equity and Treasury bond markets as well as the usual FX market. Exports in South Korea advance 13.7% during first 10 days of April y/y, leaving a trade deficit of $1.09bn. Exports to China rebounded from -4.1% (full March) to +8.8% y/y in the first 10 days of April while exports to U.S. fell -0.6% y/y (March: 2.3% y/y). Chip exports were up 32% vs. 11.9% in March. While the headlines are all positive, the daily average exports at +0.3% y/y vs. 12.3% y/y for the first 10 days of March are a source of concern. KOSPI –0.5%, 10yr KTB flat at 2.70%, KRW +0.8% at 1445

Sharp risk reduction in Shanghai Composite and Taiwan equities. Shanghai Stock Exchange’s margin trading outstanding is cut by CNY 38bn this week, the most since March 2024, while Taiwan’s margin loan posted the largest reduction on record by TWD 76bn, more than double the magnitude seen in more recent Taiwan market volatility in August 2024. Total margin loan stood at TWD 222bn, the least since October 2023. The drop in speculative buying suggests ongoing intervention has kept the two equity markets more stable than the underlying sentiment for both China and Taiwan risk. SHCOMP up +0.5%, 10yr CGB flat at 1.66%, CNH off

–0.1% at 7.3287

UK February Monthly GDP rose by 0.5% in February 2025, with growth in all main sectors. Services output grew 0.3% m/m, production output up 1.5%, and construction output at 0.4% m/m. Looking into detail of production data, the largest positive contributions to manufacturing output in February 2025 came from computer, electronic and optical products (+9.8%), “basic pharmaceutical products” (+4.4%) and “transport equipment” (+1.8%). UK FTSE +0.5%, 10yr gilt 5bp higher at 4.69%

U.S. March PPI expected up 0.2% m/m, 3.3% y/y after 0% m/m, 3.2% y/y but with core expected -0.1% m/m, 3.4% y/y after 3.6% y/y – key input for PCE and after the CPI report important for FOMC views on inflation.

U.S. April preliminary University of Michigan consumer sentiment expected down to 54.5 from 57.0 with focus on inflation expectations and just how weak outlooks and current conditions are after “liberation day.”

Fed Speakers: St. Louis Federal Reserve Bank President Alberto Musalem speaks on the U.S. economy and monetary policy, New York Federal Reserve John Williams speaks on economic outlook and monetary policy.

Mood: No sign of easings with iFlow Mood moving deeper into the risk-off zone, with selling of equities against buying momentum in bonds.

FX: Safe haven demand seen in USD, JPY and CHF while selling pressure continues in GBP but at less magnitude in EUR and GBP. Elsewhere, notable flows were significant TRY outflows and continued inflows in CNY.

FI: Demand for Eurozone and China government debt stood out against broad selling pressure in the rest of the iFlow Universe. Notable government outflows seen in Chile, Canada, Poland, Turkey and Indonesia.

Equities: Equity risk reduction is widespread globally with accelerated unwind in Chinese equities. Within U.S. equity, real estate was the only sector with inflows while financial, energy, health care and communication services sectors were the most sold.

"Risk, then is not just part of life. It is life. The place between your comfort zone and your dream is where life takes place. It’s the high-anxiety zone, but it’s also where you discover who you are." - Nick Vujicic

“There’s no reward without work no victory without effort, no battle won without risk.” - Nora Roberts

Japan M3 money stocks plunged to 0.4% y/y, the lowest since late 2007.

New Zealand March PMI slips to 53.2 from 54.1 - as expected and as in expansion for the third straight month. The sub-index values were mostly in expansion during March. Production (54.2), the highest since December 2021, employment (54.7), the highest since July 2021, finished stocks (56.3), the highest since December 2021, while new orders (49.6) returned to slight contraction. NZX50 -1.5%, 10yr NZGB +11bp at 4.76%, NZD +1.5% 0.577

German March final CPI up 0.3% m/m, 2.2% y/y after 0.4% m/m, 2.3% y/y – unrevised as expected. The HICP rose 0.4% m/m, 2.3% y/y after 2.6% y/y – also unrevised. This moderation came amid a sharp slowdown in services inflation, which eased to 3.5% from 3.8% in February, along with a faster decline in energy costs, which fell by 2.8% compared to a 1.6% drop in the previous month, mainly weighed by lower prices for motor fuels, solid fuels and heating oil. However, food inflation increased to 3.0%, up from 2.4%. EuroStoxx +0.5%, 10yr Bund +4bp higher at 2.62%, EUR +2.3% higher at 1.133

Sweden March final CPI -0.7% m/m, +0.5% y/y after +0.6% m/m, +1.3% y/y – unrevised as expected – the lowest reading since December 2020 and the eighth consecutive month that inflation has remained below the Riksbank's 2% target. The CPIF -0.5% m/m, 2.3% y/y after 0.9% m/m, 2.9% y/y. The slowdown in prices was particularly evident in clothing and footwear (1.4% vs. 3.8% in February) and recreation and culture (0.6% vs. 2.2%). Additionally, costs dropped further for housing and utilities (-2.8% vs. -0.4%) and transport (-2.1% vs. -0.8%). On the other hand, food inflation accelerated to a sixteen-month high (5.4% vs. 3.9%), led by higher prices for coffee, chocolate, and dairy products. OMX –0.8%, 10yr SGB +3bp higher at 2.42%, SEK +1.5% at 9.804