Market Movers: Relative Value

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 10 minutes

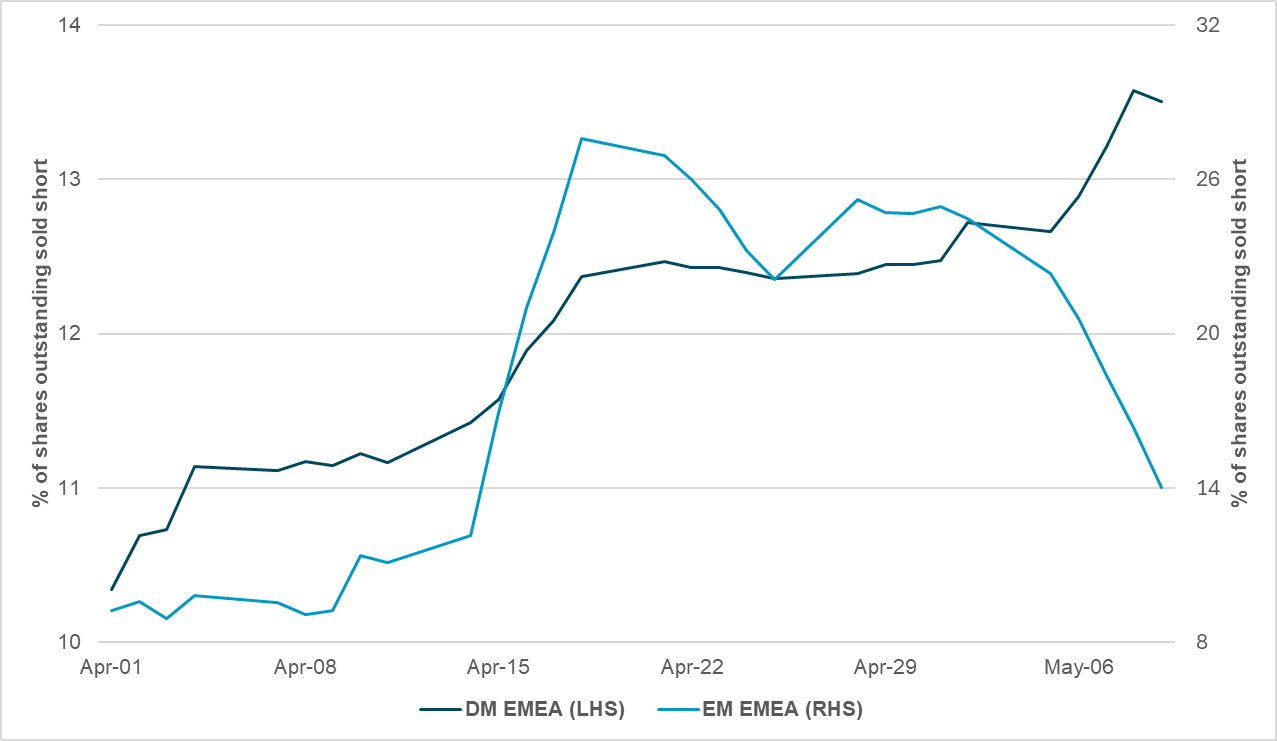

EXHIBIT #1: DM EMEA EQUITY SHORT UTILIZATION JUMPS

Source: BNY

Risk appetite has improved in the wake of the U.S.’ trade deals, but the interest is not uniform – especially where trade deals aren’t forthcoming. As highlighted in our Start of the Week, we are increasingly worried about European equity holdings as the reality of the outlook and earnings may dash expectations. The hiccup for German Chancellor Merz last week was a reminder of political difficulties for Germany, and there will also be growing uncertainty surrounding the broader outlook for the EU as well – with the final round of Romania’s presidential elections later this week likely to yield another outcome which could challenge defense narratives out of Brussels. Consequently, the bottom five performing equity markets last week in flow terms were all in non-Eurozone Europe, while Eurozone equity markets were also net sold on an aggregate basis. The strong holdings position established for DM EMEA equities due to the European re-investment theme has now become a risk factor, reflected in the rise in short utilization for DM EMEA equities. As valuations and holdings in EM EMEA are already quite depressed, by its own standards short utilization has fallen significantly. In contrast, DM EMEA short utilization has only been rising since early April, irrespective of broader changes in the risk environment. The two geographies enjoyed significant co-movement beforehand, which makes the recent split in performance notable. DM EMEA is clearly at risk of earnings disappointment. In absolute terms, utilization remains low but the rise of almost 40% over the course of the last few weeks underscores the shift in expectations for performance.

Risk sentiment mixed as investors return to the grinding work of finding relative value in a global market still filled with uncertainty. U.S. equity futures, U.S. bond yields and USD are all lower. Gold is higher but so is oil as markets rethink the balance of momentum factors against value. Global growth fears have eased but global inflation doubts are rising. The key event today is the release of U.S. CPI, which is widely expected to rise by 0.3% m/m after a surprise -0.1% m/m decline, with a focus on goods-related price increases from tariffs. Core inflation in the U.S. is expected to hold remain at 2.8% y/y as service costs hold steady. The overnight data could foreshadow trouble as the U.K. labor market weakens but wages remain high. In EM markets, the increase in the jobless rate in South Africa has added to growth concerns. Meanwhile, BoJ Governor Ueda is again talking about raising rates, making it clear that FX matters to policymakers. A large number of Fedspeakers will begin giving speeches tomorrow. While mostly graduation speeches, any guidance they can provide is important, as they may see more reasons to wait given the rebound in U.S. shares. There is a niggling fear that trade deals won’t fix the overall economic growth engines for the U.S., particularly with the USD holding up. We also got data from the German ZEW and Australian confidence surveys as global sentiment climbs on hopes for trade trade negotiations, but the timing and details of any deals remain uncertain – adding to the sense of caution in trading today. The broader strategy of buying the dip works when markets are short, not when they are long. The tactical work ahead is about finding relative value as investors look for new themes at the grinding start of summer trading, with the pressure on to find returns and put money to work.

The six biggest life insurance companies in Taiwan reported a total loss of NT$18.7 billion ($616 million) in April due to the surging Taiwan dollar, the worst performance in nearly 18 months. Only one insurer remained profitable, while the rest reported losses due to elevated hedging costs and abrupt currency moves triggered by unexpected U.S. tariff policy announcements. The surge in the TWD, driven by capital repatriation and weakening of the U.S. dollar, also forced a major drawdown in foreign exchange reserves. Across the six largest firms, over NT$380 billion was withdrawn from FX reserve accounts during the first four months of 2025. Despite the losses, insurers stressed that their overall capital adequacy, solvency and liquidity remain sound. Most are adjusting asset allocations and hedging strategies to manage ongoing volatility and external policy risks, particularly those stemming from U.S. trade developments. TAIEX 0.949% to 21330.14, USDTWD -0.464% to 30.446, 10y TGB -25.6bp to 1.547%.

Republicans in the House of Representatives have introduced their tax reform bill, intended to provide trillions of dollars in tax cuts in addition to targeted tax hikes. House Speaker Mike Johnson continues to eye Memorial Day (May 26) as the deadline for the bill’s passage. The bill would extend the 2017 tax cuts and add new deductions for tipped wages, overtime, Social Security benefits and loans for U.S.-made cars. It also raises the standard deduction and child tax credit and eases the cap on state and local tax (SALT) deductions. To offset its projected $4.9 trillion cost over a decade, it proposes deep cuts to Medicaid, food aid, and green energy programs, along with stricter work requirements. Internal GOP divisions, especially over the deficit impact, could delay passage beyond the target date. S&P Mini -0.401% to 5841.5, DXY -0.205% to 101.58, 10y UST -2.4bp to 4.447%.

As part of the executive order regrading reciprocal tariffs against China, the U.S. has lowered the de minimus tariff for low-value imports from China to 54% from 120%, while retaining a $100 flat fee. Previously this exemption allowed goods valued under $800 to enter the U.S. duty-free. Long-term prospects for such shipments remain in doubt as the U.S., U.K. and European Union have been actively looking at making similar adjustments. U.K. Chancellor Rachel Reeves in April launched a review of the country’s zero-tax regime for shipments below £135, and the EU is also actively pursuing reforms to its de minimis threshold for low-value imports (€150 or less) to align its regime with the U.S. CSI 300 +0.145% to 3896.26, USDCNY +0.069% to 7.2004, 10y CGB -2.1bp to 1.66%.

The ZEW Economic Sentiment Index for Germany rebounded sharply in May 2025, rising to +25.2 points (consensus: 11.3) – an increase of 39.2 points from April, reversing last month’s sharp decline. Despite this improvement in expectations, the current economic situation remains bleak, with the situation index dropping slightly to -82.0, the lowest among surveyed countries. Optimism was driven by the formation of a new government, easing of trade tensions and stabilizing inflation. Expectations improved across nearly all sectors, particularly banking, automotive, chemicals and construction, the latter supported by recent and expected ECB rate cuts. Domestic demand is also expected to pick up. For the Eurozone, expectations rose by 30.1 points to +11.6, while the current situation assessment improved modestly to -42.4 points. DAX -0.024% to 23560.92, EURUSD +0.181% to 1.1107, 10y Bund +2.7bp to 2.675%.

Based on the latest labor market report, in the three months to March 2025, wage growth in the U.K. remained resilient. Regular pay (excluding bonuses) rose by 5.6% year-on-year, while total pay (including bonuses) increased by 5.5%. When adjusted for inflation, real wage growth also remained positive. Using the Consumer Prices Index including owner-occupied housing costs (CPIH), real regular pay rose by 1.8%, and total pay by 1.7%. Based on the standard CPI measure, both grew by 2.6%. These figures indicate that earnings are continuing to outpace inflation, offering some relief to households facing persistent cost-of-living pressures. However, growth rates have eased slightly from the previous quarter, suggesting momentum may be moderating. Overall, we don’t believe these figures are sufficient for the BoE to entertain cuts until the August forecast round. FTSE 100 +0.046% to 8608.92, GBPUSD +0.266% to 1.3211, 10y gilt +2bp to 4.663%.

Despite firm U.K. wage growth, broader labor market conditions weakened. The unemployment rate rose to 4.5% in January–March 2025, up from 4.4% in the previous quarter and 4.3% a year earlier. The employment rate remained stable at 75.0% for those aged 16–64, while the economic inactivity rate declined slightly to 21.4%. Vacancies continued their downward trend, falling by 42,000 to 761,000 in the three months to April – marking the 34th consecutive quarterly drop. The claimant count increased to 1.726 million in April. Collectively, these data suggest a cooling labor market, even as wages continue to rise, possibly reflecting weakening demand for labor.

South Africa’s official unemployment rate rose to 32.9% in Q1, up from 31.9% in Q4 2024. The number of employed persons declined by 291,000 to 16.8 million, while the number of unemployed increased by 237,000 to 8.2 million. The total labor force shrank by 54,000. The number of discouraged jobseekers rose slightly by 7,000 (0.2%), and those not economically active for other reasons increased by 177,000 (1.4%), pushing the non-economically active population up to 16.7 million. The expanded unemployment rate, which includes discouraged jobseekers, increased to 43.1%, up by 1.2 percentage points from the previous quarter’s 41.9%. JSE TOP40 +0.066% to 84745.33, USDZAR -0.181% to 18.2969, 10y SAGB -2.2bp to 10.495%.

U.S. April CPI – headline CPI expected at 0.3% m/m, 2.4% y/y. Core CPI expected steady at 0.3% m/m, 2.8% y/y.

Mood: iFlow Mood continues to normalize, with buying in both equity and fixed income instruments.

FX: USD, SEK, JPY, AUD and TWD posted significant outflows versus strong demand in CAD and GBP. JPY and USD scored holdings ease sharply, while GBP and EUR holdings pick up strongly.

FI: Demand for Brazilian government bonds, U.S. Treasurys and Eurozone bonds stood out amid light selling pressure in most other government bonds.

Equities: Concentrated demand in APAC equities against selling in Americas. Flows in EMEA were mixed. Hungarian equities stood out with significant selling, against most demand seen Thailand.

“All animals are equal, but some animals are more equal than others.” – George Orwell, from Animal Farm

“Value is relative,” said the saint. “A man with his house on fire and a man dying of thirst each place a different value on a glass of water.” – Jonathan Maberry

U.K. April BRC sales like-to-like surged to 6.8% y/y, the strongest sales growth since January 2022 at 8.09%. The British Retail Consortium noted that the timing of Easter, which fell in April this year rather than March, contributed to an inflated April figure and a weaker March result. Food sales rose sharply by 8.2% compared to a 1.6% decline in the same month last year. Non-food sales also saw strong gains, up 6.1% versus a 6.0% drop in April 2024. The U.K. government announced a new initiative encouraging pension funds to allocate a greater share of their assets to private markets and domestic investments. A group of major pension providers has committed to directing at least 10% of default defined contribution funds to private market assets by 2030, with a significant portion targeted at U.K.-based projects, such as infrastructure, clean energy and technology. This move is expected to unlock up to £50 billion in long-term capital, with roughly half of that anticipated to support the U.K. economy directly. While participation is currently voluntary, the government has suggested it may consider legislation to enforce these investment targets if commitments fall short. The shift is part of a broader effort to boost growth and strengthen domestic capital markets. FTSE 100 +0.046% to 8608.92, GBPUSD +0.266% to 1.3211, 10y gilt +2bp to 4.663%.

Chinese President Xi Jinping pledged deeper ties with Latin America and the Caribbean (LAC), offering visa-free travel to five countries and a ¥66 billion ($9.2 billion) credit line. Speaking at the Fourth Ministerial Meeting of the China–Community of Latin American and Caribbean States (CELAC) Forum in Beijing, Xi framed China as a fairer, multilateral partner amid rising U.S. protectionism. While not naming the U.S., he criticized trade wars and hegemonism. Beijing is leveraging its Belt and Road investments, trade growth, and new deals – including $4.7 billion in Brazilian projects –to expand influence. Despite U.S. pressure, LAC nations are deepening ties with China due to limited alternatives. Xi promised more imports and Chinese investment, sidestepping criticism over industrial overcapacity, even as countries like Brazil and Mexico impose steel tariffs. CSI 300 +0.145% to 3896.26, USDCNY +0.069% to 7.2004, 10y CGB -2.1bp to 1.66%.

Australia May Westpac Consumer Confidence improved slightly to 92.1 from 90.1, supported by a rebound in financial market and a clear-cut federal election result. Consumers are a little less downbeat about spending and gained confidence in job prospects. The Westpac–Melbourne Institute Index of House Price Expectations rose 1.4% to 155.5, as 87% of consumers expect prices to be the same or higher in a year’s time. Elsewhere, Australia April NAB business condition dropped from 3 to 2, the lowest since August 2020. ASX +0.091% to 4672.99, AUDUSD +0.55% to 0.6407, 10y ACGB +6.9bp to 4.429%.

NAB Business confidence for Australia edged up 1 point to -1 but remained negative and below the long-run average. Forward orders softened again, and capital expenditures fell sharply to their lowest level since mid-2024. Capacity utilization also declined to 81.4%, reversing March’s strong gains. While labor cost growth held steady at 1.6%, purchase and retail price growth accelerated. Industry-wise, mining and transport/utilities saw the steepest declines in conditions, while Tasmania and Queensland recorded state-level improvements. Despite rising product prices, the decoupling of profitability and employment suggests further monitoring is needed.

Bank of Japan deputy Governor Uchida reiterated overnight that the BoJ will hike rates if its economic outlook is realized. However, he noted that rapid moves in FX markets have increased economic uncertainty, and the central bank would need to “carefully watch” the economy to see if forecasts materialize without any preconception. 30y JGB auction improved, with a 2bp tail versus 4.3bp but still above the sub-2bp tail for most of 2024. The bid/cover ratio, at 3.07, remains near the lower end of the range in 2024. Nikkei +1.432% to 38183.26, USDJPY +0.304% to 148.01, 10y JGB -1.1bp to 1.444%.

April Czech consumer prices declined by 0.1% month-on-month, mainly due to lower prices in alcoholic beverages and tobacco, as well as declines in food and fuel costs. Year-on-year inflation slowed sharply to 1.8%, the lowest since March 2018, reflecting base effects and continued drops in energy prices. Notable monthly price falls included sugar (-10.6%), eggs (-4.4%), wine (-5.1%) and fuel (-2.7%). However, services inflation persisted, with catering and accommodation rising, and household maintenance items increasing. On an annual basis, food price growth moderated across several categories, while housing-related costs, such as rents and maintenance, remained firm. Despite the slowdown, service prices rose 4.7% year-on-year. The harmonized index of consumer prices (HICP) increased 1.7%, down from 2.7% in March, showing broader disinflationary pressure. Prague SE -0.29% to 2161.98, EURCZK +0.121% to 24.949, 10y CZGB +5.3bp to 4.215%.