Market Movers: Politics

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 9 minutes

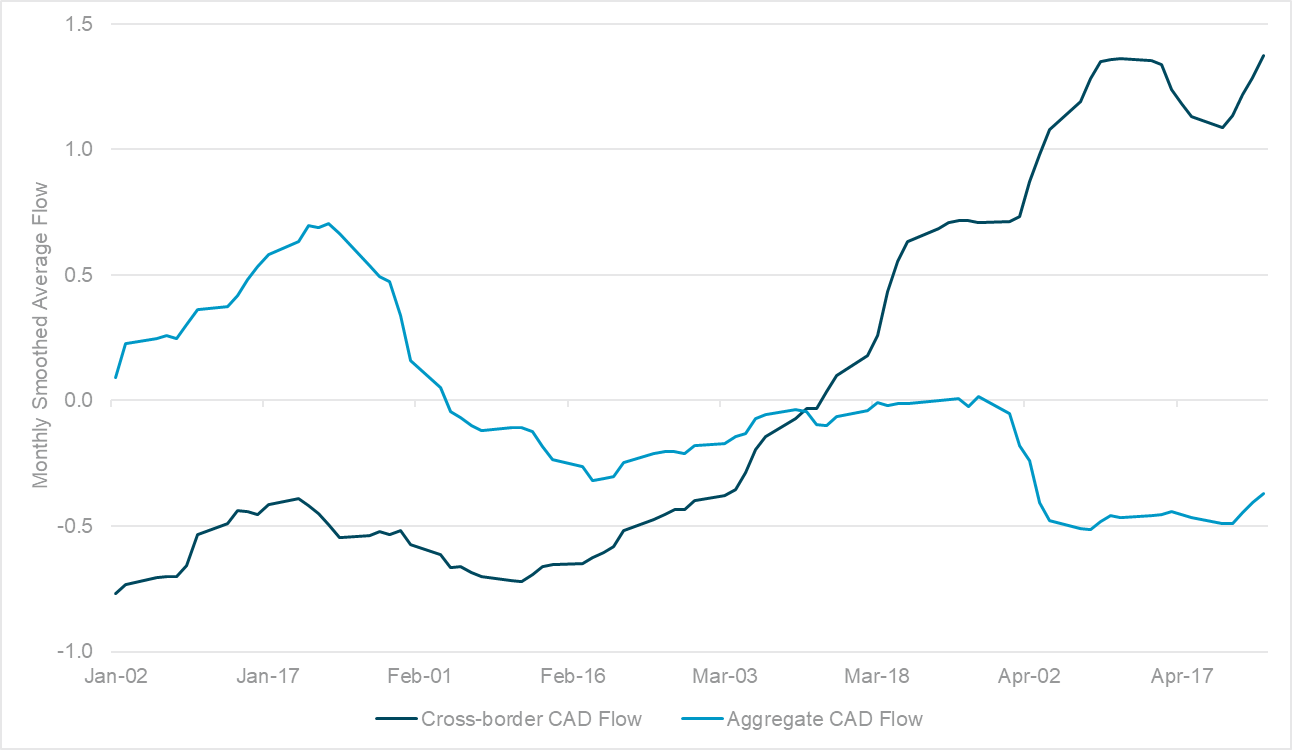

EXHIBIT #1: CAD RESILIENCE ARISING FROM CROSS-BORDER FLOW

Source: BNY

Our flow monitor points to cross-border investment interest in Canada changing as rapidly as the Liberal Party’s fortunes year to date. The first two months were a struggle as international investors believed Canada would be among the countries most affected by tariffs, and there was a sharp rise in hedging interest. Instead, the aggregate figure held up well, which shows domestic investors are happy to own CAD. However, the two client groups diverged sharply from March on as trade tensions began to extend globally. Canada tariff exemptions and an improvement in valuations saw cross-border investors return in earnest. The run-up to the election continued to see a strong period of cross-border inflows into CAD as well. This divergence between onshore and offshore interest is rare for CAD, but as the latter group drives marginal flow, the post-election relief should be strong enough to sustain CAD resilience.

Risk sentiment is positive, with hopes for further Trump’s tariff relief on autos and better earnings supporting equities. The USD is higher, but U.S. bonds are lower, with focus on the economic data ahead, including U.S. jobs from the consumer confidence and JOLTS surveys and the U.S. goods trade deficit for March. The overnight news revolved around politics with Canada’s Carney victory helping CAD, but geopolitical risks for India and Pakistan and ongoing hopes for a Russia-Ukraine deal beating out the flash higher CPI from Spain and the overall lower confidence in the Eurozone. The lack of bigger moves suggests volatility has been contained, but not returned to pre- “Liberation Day” levels. The key for the rest of the day is in the U.S. data and the delivery of tariff and tax relief from the Trump administration. Markets are set up for a long week, with month-end flows dominating the tape, but the risks of downside surprises look oddly less priced. The May Day holidays are likely to force many to rethink their positions. Rising worries about U.S. politics have seen the U.S. bond market return as the barometer of trouble, with tariff pain seen offset by tax cuts but dependent on a divided Congress.

U.S. Treasury Secretary Scott Bessent has set a July 4 deadline to pass a tax cut package. He made the announcement after meeting with congressional leaders from the Republican Party. Speaker Mike Johnson has also stated that the House aims to pass tax legislation by the end of May, which would renew tax cuts from President Trump’s first term while further cutting federal spending. S&P 500 +0.064% to 5528.75, DXY +0.243% to 99.251, 10y UST -2.7bp to 4.208%.

Pakistan’s Defense Minister Khawaja Muhammad Asif warned of “an immediate threat” to the country due to a rise in tensions with India. He also stated that China, Saudi Arabia and other Gulf states are working to prevent conflict from breaking out and “if something has to happen, it will happen in two or three days.” This will likely keep pressure on Indian assets, which are already facing pressure from rebalancing flows. SENSEX +0.055% to 80262.55, USDINR -0.219% to 85.22, 10y INGB -4.7bp to 6.349%.

Spanish April preliminary inflation surprised to the upside at 0.6%m/m, 2.2%y/y on a both a national and HICP basis. However, GDP was weaker than expected for the first quarter, expanding by 0.6%q/q – though this is still considered extremely strong by European standards. IBEX 35 +0.636% to 13487, EURUSD -0.21% to 1.1396, 10y Bono -2.6bp to 3.155%.

Spain announces almost 90% of power has been restored to the country after the entire Iberian Peninsula was affected by a major power outage yesterday. The Spanish Ministry of the Interior declared a state of emergency late on Monday. Authorities in Portugal also announced that power had been restored for all electricity users. National and regional leaders said there were no indications of a cyberattack “at this point.”

Eurozone April economic sentiment slips to 93.6 from 95.0 – weaker than 94.5 expected and worst since December – with higher inflation expectations, weaker selling prices, lower industrial sentiment and services. Among the Eurozone’s largest economies, sentiment deteriorated notably in the Netherlands (-2.5) and Italy (-1.8), while improving slightly in Germany (+0.5) and Spain (+0.4). Sentiment in France remained broadly stable.

The National Bank of Hungary is expected to keep its benchmark interest rate unchanged at 6.50% at today’s meeting – a dovish tilt is expected in statement.

U.S. March flash goods trade deficit expected $145.0bn from $147.9bn – this matters to Q1 GDP and to the set-up for the Q2 trade narrative following the implementation of tariffs.

U.S. February home prices – FHFA expected up 0.3% m/m after 0.2% m/m, while the Case-Shiller 20-City Index expected up 0.4% m/m, 4.7% y/y after 0.46% m/m, 4.6% y/y.

U.S. March JOLTS job openings expected down to 7.5mn from 7.568mn with rate 4.5% steady – focus will also be on quits rate and layoffs expected 1.816mn after 1.79mn.

U.S. April conference board consumer confidence expected down to 88 from 92.9 with focus on jobs hard to get and inflation outlooks.

Mood: iFlow Mood remains in “risk off” territory but attempting to recover as month-end sees light support for risk.

FX: APAC continues to perform well, with most currencies net bought – softer inflation in the region is helping support real rates and currencies. Month-end will bring risk to global commodity FX, but NOK and ZAR are holding up well due to supportive real rates and domestic developments. COP the weakest performer as fiscal risk picks up.

FI: Major markets are performing well as Germany and France see strong inflows; Brazil is also benefiting from real rates support and central bank commentary remains hawkish. Indonesia and Poland both see outflows, while Chinese government bond flows also continue decline after a strong period of flows initially in April.

Equities: Surprisingly robust flow in minor Latin American economies ahead of core central bank decisions. Colombia again looking exposed due to fiscal risk.

“… central bank policies are not the cause of low rates, but responses to them. We are actors in a play written by others.” – Mark J. Carney

“You want a friend in Washington? Get a dog.” – Harry S. Truman

U.K. April BRC Shop Price Index improved to -0.1% from -0.4% y/y, of which food prices at 2.6% y/y (March: 2.38%) and non-food prices up -1.45% y/y (March: -1.86%). Headline food price indices were flagged as one of the potential inflation pressure points by the Bank of England as taxation changes have led to a rise in labor costs, which employers appear to the passing on to underlying consumers. BoE Governor Bailey remains concerned that such adjustments will keep inflation expectations elevated. FTSE 100 +0.025% to 8417.34, GBPUSD -0.305% to 1.34, 10y gilt +3bp to 4.509%.

New Zealand March filled jobs rose 0.2% m/m, or -1.5% y/y. Looking into breakdown, primary industries jobs recovered the most at 0.62% y/y, but it accounts for only a small portion of the jobs market. Services industries, which account for 77% of jobs, remains in negative growth at -0.95% y/y. New Zealand unemployment rate stood at 5.1% as of December 2024 and likely to stabilize if filled jobs is a good indicator. NZX 50 -0.607% to 12025.45, NZDUSD -0.485% to 0.595, 10y NZGB +3.4bp to 4.476%

In a speech overnight on exchange rates and the Australian dollar, RBA Assistant Governor for Financial Markets Christopher Kent highlighted the increasing role of superannuation funds in Australia’s FX markets. Due to accumulation of foreign assets, “the rise in net equity assets of late has occurred while Australia has been running a current account deficit, creating an unusual situation.” ASX +0.104% to 4553.16, AUDUSD -0.295% to 0.6412, 10y ACGB +2.1bp to 4.191%.

South Korea March Retail Sales surged by 9.2%y/y, up from 4.4%y/y prior. However, the distribution of sales was mixed as department store sales fell by 2.1% y/y and discount store sales fell by 0.2% y/y. The Ministry of Trade, Industry and Energy said the increase is mainly attributable to strong demand for e-commerce deliveries in food and daily shopping sectors and other services. Sales from the online sector increased 19% on-year as revenue from the food sector rose 19.4% and revenue from the daily necessities sector expanded 7.5%. Sales from online services, such as food delivery and e-coupons, spiked 78.3%. KOSPI +0.65% to 2565.42, USDKRW +0.035% to 1435.95, 10y KTB +1.2bp to 2.59%.

Turkish unemployment in March fell slightly to 7.9% from 8.2%. Economic confidence, however, declined to 96.6 from 100.8 the previous month. Youth unemployment increased slightly to 15.1% but the adjusted labor force participation rate improved to 53.4%. BI 100 -0.398% to 9269.89, USDTRY +0.016% to 38.424, 10y TGB -14bp to 35.22%.

Hungarian PPI contracted further by 0.7% m/m in March, though the annualized growth rate remains elevated at 7.3% y/y. The bulk of the gains continues to come from external sources as non-domestic output prices were up 8.6% y/y, led by a 27.3% y/y gain in the energy industry. The figures could solidify a dovish bias from the National Bank of Hungary, but rate cuts may need to wait. Budapest SI +0.2% to 93170.73, EURHUF +0.045% to 404.18, 10y HGB -12bp to 6.81%.

Swedish data released overnight were mixed. On a working day adjusted (WDA) basis, retail sales strengthened to 3.6% y/y, while the GDP indicator also showed a good recovery for the economy in March, growing by 0.6%m/m (1.3% yy WDA basis). However, on a quarterly basis the Swedish economy was flat, with growth maintaining a soft 1.1% annualized growth rate. The trade balance fell to SEK 12.8bn vs. SEK 15.0bn the previous month. Swedish consumer confidence for April fell sharply to 81.6 from 89.8 the previous month. However, manufacturing confidence managed to recover to 99.6 from 96.7 (revised) in March. The Swedish National Institute of Economic Research warned that “significantly more firms than in March reported difficulties in predicting future business conditions,” and “the consumers’ confidence indicator has declined by over 16 points during the past three months, representing both a sharp and rapid downturn.” OMX +0.293% to 2435.16, EURSEK -0.234% to 10.9664, 10y Swedish GB -1.4bp to 2.367%.