Market Movers: Policymakers

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 10 minutes

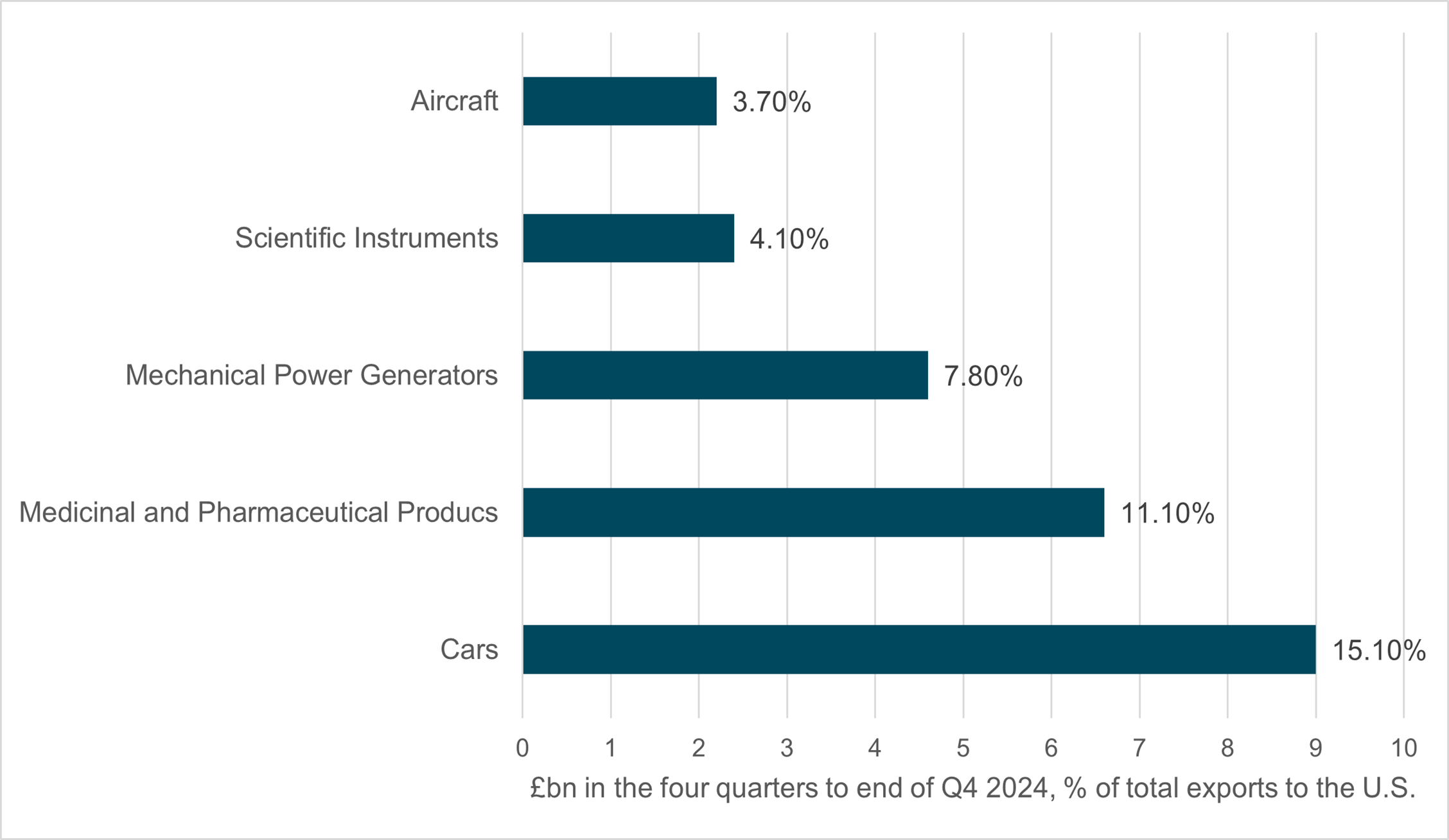

EXHIBIT #1: MAIN U.K. EXPORTS TO THE U.S.

Source: BNY, U.K. Government

News of a trade deal between the U.S. and U.K. is a welcome boost to the Bank of England ahead of today’s policy decision. While not as exposed compared to major goods exporters, the Monetary Policy Committee remains attuned to the associated risks. The nature of U.K. manufacturing exports to the U.S. means that the country is uniquely exposed to tariffs on high value-added manufacturing goods, and why a trade deal remains essential despite the flat goods balance between the two nations. Just over 40% of U.K. exports to the U.S. in 2024 are in five extremely high value-added categories. If there are general tariffs applied by industry group – especially pharmaceuticals – then the damage to U.K. growth will be material. Headline exports aside, the revenue loss through income and corporation tax would have a knock-on impact on government finances, which are already under heavy scrutiny by the market. The U.K. government said that “as of 2020, exports to United States supported around 974,200 jobs in the U.K.” – and these are jobs the country cannot afford to lose. Even with positive pass-through from a weaker pound, we expect the Monetary Policy Committee (MPC) to align with most assessments by the U.S.’ key partners that the demand loss would exert greater downside risk on prices and justify additional easing – provided other inflation barometers show looming disinflation.

The risk sentiment continues to be positive today led by trade talks and deal hopes along with rate cuts around the world from central bankers. The rally in U.S. shares yesterday extends on the back of deal hopes with the U.K. today. The balancing act for investors is in the timing of negotiations and deals against the rising signs of a slowdown in global trade. The focus on shipping continues as shown in Q1 earnings reports – Maersk cut their outlook for volumes from +4% in 2025 to -1% to 4% − and there is a risk premium on the uncertainty of when trading will return to normal. Furthermore, the confirmation of caution over future growth in the FOMC statement and Chair Powell’s press conference makes clear that rate cuts in the U.S. will lag but will follow hard economic data. Whether the Fed is late to easing matters less to markets today because the rest of the world is moving on with countermeasures to growth. The role of the USD as a counterweight to rising risks is clear, and while there are clear signs that the dollar is finding a bid from the contrast of the FOMC wait-and-see position against other countries, the medium-term trend is lower. The risk premium for growth will outweigh any carry offered by rates given the level of uncertainty. We don’t know the end rate of global tariffs and likely won’t even after the 90-day reciprocal pause. The rate decisions for the Fed still matter for June, but the waiting game highlights the lack of viable forward guidance. The cost of that is in the USD.

President Trump is expected to announce the framework of a trade agreement with the United Kingdom, marking the first such deal since his administration imposed sweeping tariffs last month. The agreement, expected to reduce tariffs on British exports like steel, aluminum and cars, follows intensive negotiations led by U.K. Prime Minister Keir Starmer. In exchange, the U.K. has offered concessions, including lowering its digital services tax on major U.S. tech firms. However, the deal is not expected to be comprehensive, with contentious issues like agricultural standards and tariffs on pharmaceuticals and films remaining unresolved. Starmer is set to make a statement later today, emphasizing the U.K.’s commitment to protecting national interests while strengthening economic ties with the U.S. FTSE 100 +0.124% to 8569.94, GBPUSD -0.158% to 1.3271, 10y gilt -0.6bp to 4.454%.

India and Pakistan appear to be moving towards de-escalation but local markets remain on edge. Trading on the Karachi Stock Exchange was halted after a 7.2% plunge in the benchmark KSE-30 Index, and Pakistan temporarily suspended operations at major airports, initially leading to concerns of a further escalation of the situation. However, Prime Minister Sharif indicated the response to India had been delivered, and Indian Minister for External Affairs Subrahmanyam Jaishankar also stressed that it was not India’s “intention to escalate the situation.” KSE-30 -7.148% to 31212.9, USDPKR (NDF) +0.088% to 284.75, 10y PGB +0.3bp to 12.576%.

BNM kept rates unchanged at 3% with a dovish tilt in a forward looking statement. While BNM reiterated that the MPC will ensure that the monetary policy stance remains conducive to sustainable economic growth amid price stability, BNM omitted a crucial sentence – “current policy stance remains supportive of the economy,” suggesting the intention of a policy shift in rates going forward. The next BNM policy meeting is on July 9. We do not see BNM preemptively delivering a rate cut. The odds of easing have risen, but we maintain our view that BNM will keep rates on hold in the near term. March inflation stood at 1.40% – the lowest level since January 2024. There is a case for easing, but we see no urgency to do so. MYR has strengthened this year but remains cheaply valued. KLCI -0.24% to 1546.18, USDMYR -0.814% to 4.2745, 10y MGB +0.6bp to 3.659%.

The Riksbank has kept rates unchanged at 2.25%. Despite challenges to the Swedish economy from external factors, the Executive Board judged that current conditions do not warrant further easing unless the inflation or growth outlooks shift materially. While inflation remains somewhat elevated, the Riksbank believes this is temporary and that risks now slightly favor lower inflation ahead – pointing to a dovish lean. Global uncertainty, especially surrounding U.S. trade policy, has worsened the growth outlook for both the U.S. and Europe, with potential indirect effects on Sweden. The Riksbank emphasized the need to wait for clearer data before adjusting policy again, noting the current stance is proportionate and balanced. The policy rate path was unchanged compared to the previous meeting. OMX +0.981% to 2455.501, EURSEK -0.008% to 10.9267, 10y Swedish GB -0.3bp to 2.331%.

Norges Bank kept the policy rate unchanged at 4.5% at their May decision, where it has remained since December 2023. While inflation has fallen significantly from its peak, it remains above the 2% target. The Committee warned that lowering rates too soon could reignite inflation, though an overly tight policy risks unnecessary economic restraint. Norway’s output is near potential, and unemployment has edged up from low levels. Global uncertainty – particularly rising trade barriers and a weaker krone – adds complexity to the rate outlook. The Committee anticipates a likely rate cut later in 2025 but emphasized that future decisions will depend on incoming data, with new forecasts due at the June meeting. OSE +0.006% to 1513.04, EURNOK -0.139% to 11.714, 10y NGB +3.2bp to 3.966%.

German exports for March rose by 1.1% month-on-month to €133.2bn, while imports declined by 1.4% to €112.1bn. This resulted in a trade surplus of €21.1bn, up from €18.0bn in February. Compared to March 2024, both exports and imports grew by 2.3%. Exports to EU countries increased by 3.1%, with a 3.8% rise to euro area members, while imports from the EU fell by 3.5%. Trade with non-EU countries was mixed: exports decreased by 1.1%, while imports increased 0.8%. Notably, exports to China rose 10.2%, and imports from China climbed 9.6%, making it Germany’s top trading partner. DAX +0.95% to 23335.45, EURUSD -0.124% to 1.1287, 10y Bund +2bp to 2.495%.

Bank of England policy decision – with inflation near the 2% target and domestic demand weakening, the BoE is likely to ease gradually to support growth while remaining watchful for signs of renewed price pressure in what Governor Bailey warned is an inflation “hump” due to price resets in the new fiscal year.

U.S. Q1 nonfarm productivity, unit labor cost – a drop of 0.8% q/q expected in productivity, but labor costs likely rebounded strongly by 5.1%.

U.S. weekly initial jobless claims – a drop to 230k expected after the previous week’s jump to 241k.

U.S. April New York Fed 1-year inflation expectations – elevated reading above 3.5% y/y expected, supportive of the Fed’s assessment yesterday.

Mood: iFlow Mood is out of significantly risk-off zone and has been drifting higher, driven by ongoing demand for sovereign bonds as well as equity buying flows.

FX: USD, ILS outflows vs. GBP, CAD, EUR inflows dominated the flows. ILS scored holdings dropped sharply to be the most underheld currency within iFlow universe.

FI: Australian and Chinese government bond outflows continue against strong demand for Brazilian sovereign bonds. U.S. Treasury buying momentum continues but in light terms.

Equities: Better buying dynamic in equities complex in G10 and APAC, with selling pressure in EMEA and LatAm countries. Within U.S. equities, the energy, industrials, consumer discretionary and consumer staples sectors were sold against buying in the rest.

“We’re always going to consider only the economic data, the outlook, the balance of risks, and that’s it.” – Jerome Powell, when asked about political pressure to cut rates, May 7, 2025

“What I learned is that policymakers have to force consideration of actions that may not have occurred to them at the time.” - Susan Rice

U.K. house prices rose by 0.3% month-on-month, bringing the average property value to £297,781, according to the latest Halifax House Price Index. Annual growth accelerated to 3.2%, up from 2.9% in March, marking the strongest rate this year. Over the past six months, prices have remained broadly stable, with a minimal net decrease of just £48. The market continues to show resilience, supported by falling mortgage rates (mostly below 4%) and rising earnings, which have improved affordability. Northern Ireland led regional growth, with prices up 8.1% year-on-year, followed by Wales (+4.7%) and Scotland (+4.6%). London saw the weakest growth (+1.3%), though it remains the U.K.’s most expensive region. Buyer activity has cooled since the early-year stamp duty rush but remains strong compared to recent years. FTSE 100 +0.124% to 8569.94, GBPUSD -0.158% to 1.3271, 10y gilt -0.6bp to 4.454%.

U.K. April RICS House Price Balance dropped for the fourth straight month at -2.6, the lowest since July 2024, pressured by higher borrowing costs and a cautious economic outlook. Most of the survey’s indicators have edged up at least somewhat from the lows hit toward the end of last year, while 12-month expectations continue to signal a more stable backdrop coming through further ahead.

South Korean FX reserves drop to the lowest in five years at $404.7bn as BoK smoothed FX market. The Bank of Korea said foreign exchange swap trading with the country's pension fund, meant to temporarily reduce dollar demand in the currency market, was one of the factors that contributed to the decline. KOSPI +0.221% to 2579.48, USDKRW -0.351% to 1397.05, 10y KTB +0.7bp to 2.602%.

Philippines Q1 GDP improved from upwardly revised 5.3% y/y in Q4 2024 to 5.4% y/y in Q1 2025. That said, growth momentum slowed on a quarterly basis to 1.2% from 1.5%. The main contributors of growth were wholesale and retail trade at 6.4% y/y, financial and insurance activities at 7.2% y/y and manufacturing at 4.1% y/y. Elsewhere Philippines March net bank lending eased slightly to 11.8% y/y after peaking in January 2025 at 12.8% y/y. PSEi -1.175% to 6389.49, USDPHP -0.378% to 55.618, 10y PHGB +2.7bp to 6.166%.

Malaysia March industrial production improved to 3.2% y/y from 1. 5% and March manufacturing sales eased to 3.7% from 4.7% y/y. Malaysia April foreign reserves nearly unchanged at $118.7bn. KLCI -0.24% to 1546.18, USDMYR -0.814% to 4.2745, 10y MGB +0.6bp to 3.659%.

Germany’s industrial production rose sharply by 3.0% m/m in March – the strongest gain since early 2022. Growth was led by the automotive sector (+8.1%), pharmaceuticals (+19.6%), and machinery and equipment manufacturing (+4.4%). Excluding energy and construction, industrial output increased by 3.6%. Within that, production of capital goods and consumer goods each rose by 4.9%, while intermediate goods rose 1.1%. Energy production declined by 1.8%, whereas construction output grew by 2.1%. Compared with March 2024, total industrial output was down slightly by 0.2%. However, production in Q1 2025 was up 1.4% over the previous quarter – the strongest quarterly growth since early 2022. DAX +0.95% to 23335.45, EURUSD -0.124% to 1.1287, 10y Bund +2bp to 2.495%.

Norwegian industrial production fell by 0.3% m/m, with the working day-adjusted figure falling by 3.2% y/y. Manufacturing was stagnant on the month. The impact of low oil prices on the extraction sector is clear as the sector was flat in March, and the index of production for the sector declined by 4.2% y/y. In manufacturing, production in food & beverages and basic materials also fell. OSE +0.006% to 1513.04, EURNOK -0.139% to 11.714, 10y NGB +3.2bp to 3.966%.

Hungary’s industrial production in March showed no year-on-year growth in raw terms, but working-day adjusted figures revealed a 5.4% decline compared to March 2024. This drop was partly due to two additional working days in the current year. On a month-on-month basis, industrial output rose slightly by 0.1%, based on seasonally and working-day adjusted data. Among major manufacturing branches, output increased in transport equipment, computers and electronics, and food, beverages and tobacco. However, production of electrical equipment fell, and most manufacturing subsectors recorded annual declines. Over the first quarter of 2025, total industrial production decreased by 4.4% year-on-year, reflecting persistent weakness across much of the sector despite modest monthly improvements. Budapest SI +0.101% to 92917.35, EURHUF -0.183% to 405.05, 10y HGB -2bp to 6.88%.