Market Movers: On Edge

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 10 minutes

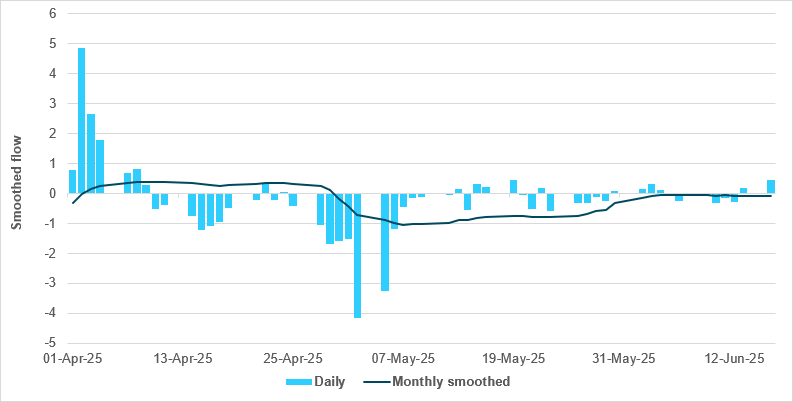

EXHIBIT #1: MATERIAL COMPRESSION IN USD FLOW RANGES AHEAD OF FOMC DECISION

Source: BNY

USD FX trading activity is remarkably light heading into the FOMC decision. Effectively, we have not seen a significant daily flow in the dollar for over a month. For both aggregate and cross-border components, the dollar is struggling to even break through a 0.5 flow score, let alone 1.0. It seems that any residual adjustment arising from “Liberation Day” ended toward the first week of May. There is a base effect in place given the large flow ranges in April; as these forward positions roll off in the near future, we should start to see USD flow magnitudes shift higher. On a directional basis, the past month has displayed a small bias toward selling, but there is little indication of aggressive moves away from the U.S. attributable to trade or fiscal risk. There has been very limited change in total and cross-border USD holdings over the past six weeks. At -1.10x the 1y average, cross-border clients are materially underheld on a relative basis, but the high-point was right before “Liberation Day” at -0.80. By this measure, investors have increased their hedges against USD by 40% from the prior equilibrium point, in a clear sign of concern about U.S. exceptionalism. We continue to believe the U.S. diversification theme itself is not being strongly actioned upon, and it was always going to be difficult to replace the dollar and UST as key reserve assets. However, factoring in additional risk premia through hedges on the currency is an efficient way to reflect any concerns, and the 10% increase relative to last year indicates only minor misgivings for now regarding the currency itself.

Risk sentiment is mixed to lower, as investors brace for more news about the U.S. role in Iran. Our mood index is flat, suggesting an uneasy balance. Markets are on edge, and the crowded consensus is to wait and see on monetary and geopolitical events ahead. Oil prices – a barometer for global unease – remain near 5m highs, while the global bond and stock markets are mixed, with modest volumes and price moves. USD has given back half of yesterday’s gains, with the focus on the Fed and its guidance. The Summary of Economic Projections (SEP), known as the dot plot, is expected to lose one cut, and that could be hawkish enough to push USD higher. However, rate cuts in Sweden and Indonesia have done some of the work. Conversely, sticky inflation in the U.K. makes tomorrow’s BoE rate decision trickier. U.S. Treasury Secretary Scott Bessent also told the New York Post that he will likely meet with China again in “about three weeks.” U.S. swap spreads have tightened further after Bloomberg added to the SLR stories, suggesting a significant shift is planned for banks holding U.S. Treasurys. Beyond geopolitical fears, the focus today ahead of the FOMC decision rests on the data: U.S. housing and U.S. jobs are the hard data to watch, highlighting the cost of a wait-and-see policy in times of great uncertainty. The key correlation for investors today isn’t in overnight interest rates but in oil and stocks, as tail risks force leverage lower, hurting EM markets, and oil keeps demand-destruction fears alive with more inflation risk.

Sweden’s Riksbank cut its policy rate by 25bp to 2.00%, citing weaker-than-expected domestic growth, high unemployment and falling inflation. Although rising real wages offer some support, the recovery remains sluggish and uncertain. Inflation has aligned with March forecasts and is projected to decline further due to soft demand. The rate path implies a possibility of another cut later this year. However, risks remain high due to geopolitical tensions – particularly in the Middle East – and ongoing trade policy uncertainty, which could dampen global and domestic growth. Future monetary policy decisions will depend on new data and their implications for inflation and the economic outlook. OMX -0.038% to 2460.46, EURSEK +0.467% to 11.0167, 10y Swedish GB -0.4bp to 2.35%.

Bank Indonesia cut its BI rate by 25bp to 5.50% in May 2025, citing low and controlled inflation within the 2.5±1% target, the need to support economic growth and efforts to maintain rupiah stability. The decision also reflects weaker-than-expected domestic growth (Q1: 4.87% y/y) and a slightly downgraded 2025 growth outlook to 4.6-5.4%. Although inflation remains manageable, global uncertainty – especially around U.S.-China tariffs –continues to weigh on exports and investor sentiment. The rate cut was part of a broader policy mix that includes liquidity easing, enhanced FX market intervention and macroprudential support to stimulate credit. Bank Indonesia emphasized continued alignment with its pro-market operations strategy to ensure effective transmission and reaffirmed its commitment to its inflation and stability mandates. JCI -0.773% to 7100.556, USDIDR +0.123% to 16300, 10y IDGB -0.2bp to 6.725%.

U.K. inflation slowed marginally in May 2025, with CPIH rising 4.0% y/y (down from 4.1% in April) and CPI at 3.4% y/y (down from 3.5%). Monthly increases were also smaller: 0.2% for both indices versus 0.4% (CPIH) and 0.3% (CPI) in May 2024. Transport made the largest downward contribution to the annual rates, partly offset by food and household goods. Core CPIH eased to 4.2% y/y (from 4.5%), driven by a slowdown in services inflation (5.3% from 5.8%), though goods inflation rose (2.0% from 1.7%). Similarly, core CPI fell to 3.5% (from 3.8%), with services inflation dropping to 4.7% (from 5.4%) and goods up to 2.0%. April inflation had been overstated due to a VED error, now corrected in May’s data. The decrease in services inflation corroborates the recent softer wage data. However, no major falls are seen, and the data should support the BoE in holding its rates steady tomorrow. FTSE 100 +0.098% to 8842.73, GBPUSD +0.187% to 1.3454, 10y gilt -1bp to 4.54%.

At the 2025 Lujiazui Forum, PBoC Governor Pan Gongsheng announced eight major financial opening initiatives, including developing free trade offshore bonds and promoting RMB futures trading. Key measures are: 1) establishing a transaction reporting database for the interbank market; 2) creating an international operations center for digital renminbi; 3) supporting the establishment of personal credit reporting agencies; and 4) launching a pilot for comprehensive offshore trade finance reform in Shanghai’s Lingang New Area, including innovative business rules. Also announced were: 5) the development of free trade offshore bonds; 6) optimization of and functional upgrades to the free trade account; 7) innovation in structural monetary policy tools, such as pilots for blockchain-based aviation trade refinancing, cross-border trade refinancing and expanded carbon reduction tools; and 8) working with the CSRC to study and promote RMB foreign exchange futures trading. CSI 300 +0.119% to 3874.97, USDCNY -0.009% to 7.1862, 10y CGB -5.6bp to 1.638%.

U.S. May housing starts forecast to come in -0.8% m/m at 1,359k (April: 1,361k); May building permits also expected to be near-unchanged at 1,425k (April 1,422k).

U.S. weekly jobless claims expected to be down 3k to 245k vs. 248k last week, with continuing claims expected down 14k to 1.941 million.

FOMC – The Federal Reserve is expected to keep the federal funds rate unchanged at its 17-18 June meeting, maintaining a cautious stance amid persistent inflation and external uncertainties.

Fed SEP (dot plot) – We expect the dots to indicate one less cut for 2025 than was previously projected. Uncertainty continues to keep the Fed from being prescriptive about policy, but more hawkish dots could upset the market.

COPOM – The Central Bank of Brazil is expected to keep the Selic rate at 14.75% at its 17-18 June meeting, following a 50bp hike in May that brought borrowing costs close to a two-decade high. With inflation still exceeding the target and economic activity showing signs of deceleration, the central bank is likely to hold rates steady while assessing the impact of previous tightening measures. There is a tail risk that hikes may continue.

Mood: iFlow Mood eases further into risk-neutral level, prompted by slowing equity buying combined with accelerated demand for core sovereign bonds.

FX: PLN saw the most significant outflows, against demand in NOK and ZAR. Elsewhere, APAC currencies were most sold, followed by EMEA, against buying in G10 and LatAm. Both USD and EUR were lightly sold.

FI: U.S. Treasurys, Eurozone and Japanese government bonds, and Hungarian sovereign bonds posted the most buying, against selling in Korean government bonds and U.K. gilts.

Equities: Asset allocation shift away from emerging markets to developed markets. Notable equities selling in Norway, South Africa and Malaysia, against broad demand in G10 equities including the majors such as the U.S., Europe, the U.K. and Japan.

“I want to stand as close to the edge as I can without going over. Out on the edge you see all kinds of things you can’t see from the center.” – Kurt Vonnegut

“If the experience of leadership is like being at the edge of an unfamiliar chasm, the act of leadership is building a bridge across that chasm.” – Kevin Cashman

South Africa’s annual consumer price inflation held steady at 2.8% in May 2025, unchanged from April. Monthly CPI rose by 0.2%. The main drivers of the annual rate were housing and utilities (4.5%, contributing 1.0 percentage points), food and non-alcoholic beverages (4.8%, contributing 0.9 percentage points) and alcoholic beverages and tobacco (4.3%, contributing 0.2 percentage points). Goods inflation edged up to 1.8% (from 1.7% in April), while services inflation eased to 3.6% (from 3.8%). JSE TOP40 -0.536% to 86680.48, USDZAR -0.07% to 18.0089, 10y SAGB -3.1bp to 10.08%.

U.K. private rental prices rose 7.0% y/y in May 2025, down from 7.4% in April, marking the fifth consecutive month of easing rental inflation. House price growth also slowed sharply, with average prices rising 3.5% y/y to £265,000 in April 2025, down from 7.0% in March. This was the first deceleration since December 2023. It was driven by a drop in prices between March and April, linked to Stamp Duty Land Tax (SDLT) changes in England and Northern Ireland that took effect on April 1, 2025 and increased tax on properties over £125,000 (other than for first-time buyers). The policy shift caused a surge in transactions and prices in March, followed by a sharp drop in April. FTSE 100 +0.098% to 8842.73, GBPUSD +0.187% to 1.3454, 10y gilt -1bp to 4.54%.

EU annual inflation fell to 2.2% in May 2025 (from 2.4% in April), while euro area inflation dropped to 1.9% (from 2.2%). The main contributor to euro area inflation was services (+1.47 percentage points), followed by food, alcohol & tobacco (+0.62 percentage points) and non-energy industrial goods (+0.16 percentage points). Energy made a negative contribution of -0.34 percentage points. Among member states, the lowest inflation rates were in Cyprus (0.4%), France (0.6%) and Ireland (1.4%), while the highest were in Romania (5.4%), Estonia (4.6%) and Hungary (4.5%). Annual inflation decreased in 14 countries, remained stable in one and rose in 12. Euro Stoxx 50 -0.134% to 5281.6, EURUSD +0.192% to 1.1502, BBG AGG Euro Government High Grade EUR -1.6bp to 2.781%.

The New Zealand Westpac McDermott Miller Consumer Confidence Index rose two points in June, taking it to a level of 91.2. That marks a fairly modest rise after the sharp fall we saw last quarter and leaves consumer confidence a fair bit below average levels (NB: A level below 100 indicates that there are more households that are pessimistic about the outlook than those that are optimistic). This continued softness in economic confidence comes against a backdrop of mixed economic conditions. While domestic economic growth is now turning higher, for the moment activity remains uneven across regions and industries. At the same time, a number of major geopolitical events continue to cast shadows over the outlook. NZX 50 -0.095% to 12627.32, NZDUSD +0.217% to 0.6027, 10y NZGB -0.3bp to 4.602%.

New Zealand’s seasonally adjusted current account deficit narrowed slightly to $5.5 billion in Q1 2025, down $53 million from Q4 2024. Goods exports rose during the quarter, but gains were partially offset by higher goods imports. The services balance worsened, with increased imports and decreased exports. Additionally, the income deficit widened as foreign investors earned more from their New Zealand holdings than New Zealand investors did from overseas assets. The annual current account deficit was $24.7bn (5.7% of GDP) in the year ended March 31, 2025.

Australia’s May Westpac Leading Index dropped for the third straight month at -0.06% m/m. The six-month annualized growth rate in the Westpac-Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, dropped to -0.08% in May from 0.19% in April. The growth pulse has shown a significant deterioration since February, with May marking the first below-trend read since September last year. The detail suggests what was mainly an external drag on momentum is becoming more domestically focused. That said, some of these drags are likely to be temporary. ASX +0.086% to 4799.49, AUDUSD +0.34% to 0.6497, 10y ACGB -0.6bp to 4.251%.

Japan May exports declined by 1.7% y/y, the first year-on-year contraction since September 2024 (-1.8% y/y), to ¥8.135tn, after a 2% y/y gain in April. Imports also saw accelerated declines, with a drop of 7.7% y/y to ¥8.773tn, the weakest rate since January 2024 (-9.6% y/y), leaving a wider trade deficit of ¥637.6bn vs. ¥-115.6bn in April. Looking into the details, semiconductors, transport equipment and chemicals exports were down the most at -8.8% y/y, -8.1% y/y and -5.6%, respectively. Exports to the EU surged by 4.9% y/y, from -5.2% y/y in April, while exports to China were down -8.8% y/y in value, and those to the U.S. -11%. Elsewhere, Japan April private sector core machine orders declined by -9.1% m/m, after a 13% gain in March. Year-on-year orders slowed from 8.4% to 6.6%. Nikkei +0.904% to 38885.15, USDJPY -0.159% to 145.06, 10y JGB -1bp to 1.455%.