Market Movers: No Hiding

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

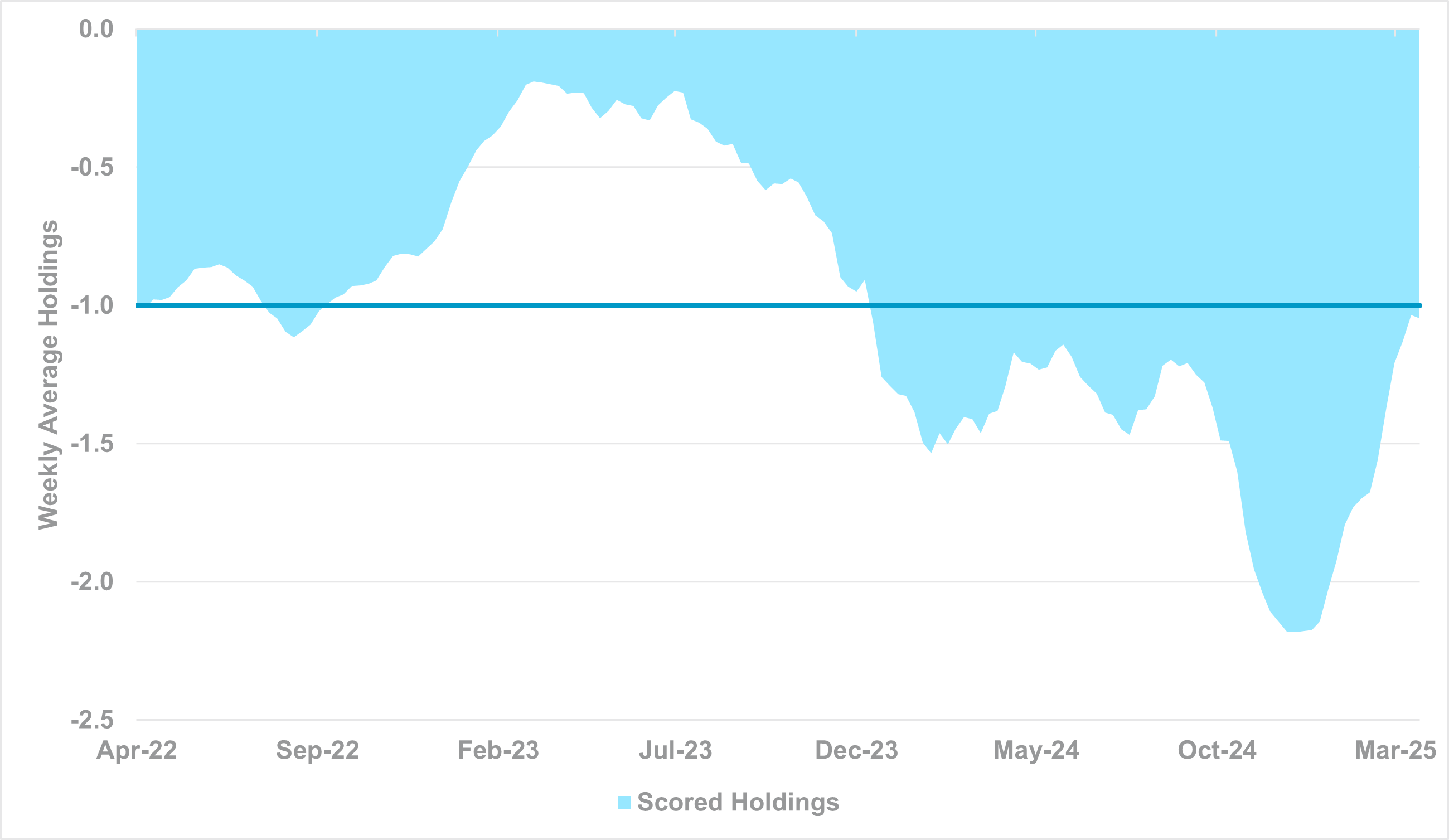

EXHIBIT #1: CROSS-BORDER HOLDINGS IN EUR RETURN TO THE ONE-YEAR AVERAGE

Source: BNY

At the end of 2024, political risk, growth weakness and expectations for sustained ECB easing pushed cross-border EUR holdings to the weakest level in nearly two decades. Our data showed overseas investors were excessively hedging their Eurozone assets. Through Q1, the unwinding of such hedges augmented EUR-positive factors, such as a less dovish ECB, European defense spending plans and more recent tariff-related changes to global asset allocation. The same data shows the EUR move now is excessive and represents a tightening in financial conditions which requires an offset by the ECB. Crucially, the same cross-border holdings have mean reverted to the average level over the past year. This will allow fundamental drivers like carry and growth to have a stronger role in determining price action for the EUR.

Risk in equities is mixed as trade talk and central bank decisions limit volatility. Still, there is no hiding from doubts in markets, with the clock ticking on tariff pauses. Outlooks for growth are lower as shown by BOJ Governor Kazuo Ueda’s testimony today. The discussions between U.S. and Japan aided sentiment in APAC as well as results from key semiconductor manufacturers. Meanwhile, Europe awaits the ECB decision ahead of the holiday weekend. There is evidence that Beijing wishes to keep lines of communication with the U.S. open, which has helped to steady equities. However, meaningful talks remain contingent on gestures from the Trump administration as well as consistency in the administration’s messaging. With dovish holds in place from the Bank of Canada, along with the Bank of Korea hold overnight and a concerned message from Federal Reserve Chair Jerome Powell – in which he said that tariffs drive uncertainty on policy, increasing the risk of higher inflation and lower growth – most investors want more forward guidance. The decision of the ECB, as the first G3 central bank to decide on rates post “liberation day,” matters. We expect ECB President Christine Lagarde’s message to be simple: the facts have changed so the ECB’s Governing Council will have to change their mind and rate cuts are the base case again. Front of mind is the re-tightening of financial conditions across the Eurozone, especially through euro strength and equity valuations, whose moves in Q1 contributed materially to the end of more forceful easing by the ECB. On the other hand, given trade negotiations and domestic responses to tariffs – especially fiscal – remain on hold, the Governing Council will likely limit available guidance. Even so, central banks would generally acknowledge that the uncertainty itself would lead to strong tightening in financial conditions, such as higher costs of hedging in options markets.

Germany PPI for March fell sharply by -0.7%m/m, which is the lowest figure since December 2023 and well below expectations of -0.1%m/m. The annualized number has also fallen back into negative territory at -0.2%y/y. According to the Federal Statistics Office, the biggest declines came in energy-related items (-2.8%m/m) such as heating oil (-7.4%m/m) and gas (-3.0%m/m). Consumer goods inflation rebounded slightly to 0.3%m/m, led by gains in non-durable goods. The data is the latest in a series of downside inflation prints, paving the way for a rate cut by the ECB today. DAX -0.18% to 21,272.15, 10y Bund +2.3bp to 2.529%, EURUSD -0.22% to 1.1374

Australia saw its economy gain 32,000 jobs in March after a -57,500 revision in February. Both full-time and part-time employment are higher at 15k and 17.2k. The March unemployment rate rose to 4.1% from 4.0%. The employment-to-population ratio held at 64.1% while the participation rate increased slightly to 66.8% from 66.7%. Overall, it was a good labor market report, raising the risk of RBA surprise at May meeting where for the market priced in a greater than 25bp rate cut. ASX200 -0.01% to 9270.01, 10yr ACGB 6bp lower at 4.28%, AUDUSD –0.4% at 0.634

Italian Prime Minister Georgia Meloni set to meet U.S. President Trump today in Washington D.C. Her relationship with the administration is seen as the strongest among Western European countries and her aim is to help jumpstart EU-U.S. trade talks. The European Commission has signaled it has confidence in Meloni, and a spokeswoman said, "any outreach to the U.S. [was] very welcome.” However, the spokeswoman added that Meloni's trip was being "closely coordinated" with the institutions and highlighted that handling trade policy was a job for the EU. FTSEMIB -0.34% to 35945.07, 10y BTP +2bp to 3.718%, EURUSD -0.22% to 1.1374

Chinese President Xi Jinping has completed his three-nation tour of ASEAN trade partners with a state visit to Cambodia. Xinhua reports President Xi will call for “joint opposition to hegemony, power politics, and camp confrontation, and seeks to maintain multilateral trading system and promote supply chain cooperation with Cambodia.” During his visit to Malaysia, Malaysian Prime Minister Anwar Ibrahim stated that ASEAN nations “will not support any unilateral trade tariffs”. CSI300 -0.02% to 3772.22, 10yr CGB +1.1bp to 1.6505%, USDCNY -0.07% to 7.2944

Thai Prime Minister Paetongtarn Shinawatra confirms a delegation led by Deputy Prime Minister Pichai Chunhavajira has an appointment to meet with U.S. officials at a ministerial level. The Thai delegation will meet with U.S. trade officials on April 23 to discuss potential relief from a planned 36% reciprocal tariff on its goods. Prime Minister Shinawatra has also discussed ASEAN’s strategy on U.S. tariffs with Malaysian Prime Minister Anwar. SET +0.19% to 1141.04, 10y Thai Government Bond +0.8bp to 1.996%, USDTHB +0.23% to 33.325

The European Central Bank expected to cut rates by 25bp and abandon the notion that policy had become “meaningfully less restrictive” as communicated in the March meeting. The market now expects the ECB to cut rates to well-below neutral. There is also a strong risk ECB President Christine Lagarde will push back against EUR strength.

U.S. March Housing Starts are expected to be down 5.4% to 1.42mn rate after +11.2% at 1.501mn in February. Building permits are expected to fall 0.6% m/m after a 1% decrease in February.

U.S. April Philadelphia Fed Business Outlook is expected to drop to 2.2 from 12.5 in March with focus on weakness risks after surprise outperformance of NY Empire State Fed Manufacturing Survey earlier this week. The 2Q growth outlook is important for investors/Fed.

U.S. weekly jobless claims expected to be up 2K to 225k with continuing claims up 20k to 1.87mn, the best indicator for the U.S. Federal Reserve’s action on rates ahead.

Federal Reserve Governor Michael Barr speaks at a fireside chat Federal Reserve Bank of New York conference on Cyber Risk with Q&A – unlikely to shift view of FOMC waiting on policy for more data.

U.S. Treasury sell 5Y $25bn TIPS at 11.30 am – as the U.S. Bond Market has early close at 2pm with futures shut at 1pm ET – liquidity and interest continue to matter to investors.

Mood: Risk aversion continues to dominate investors sentiment with iFlow Mood dipping below –0.2 for the first time since early March, driven by pick up in equities selling vs. buying in bonds.

FX: A visible pick up in G10 and APAC inflows while outflows bias remains for LatAm and EMEA region. AUD, CHF, NOK, NZD and TWD posted significant inflows with scored flow >1. TRY and SGD posted the most outflows

FI: The trend of cross border U.S. Treasurys selling against buying of Eurozone government bonds continues. Elsewhere, notable flows are large selling in U.K., Swedish and Turkish government bonds.

Equities: Selling pressure stood out in APAC, especially in China and Hong Kong compared with mixed flows across G10, LatAm and EMEA regions. Within U.S. equities, iFlow observed turnaround of flows to buying in Communication Services, Utilities, Information Technology and the Consumer Staples sector.

“Don't let an angry man wash dishes; don't let a hungry man guard rice” – Cambodian Proverb

"We have done our part. And it's now the case that governments - maybe I sound a little bit sharp - can no longer hide behind the European Central Bank." – Wim Duisenberg, ECB President 1998-2003

Bank of Korea (BoK) keeps its policy rate unchanged at 2.75% with a dovish tilt. The decision was not unanimous with one member calling for a rate cut. BoK highlighted that the downside risks to economic growth have intensified and uncertainties surrounding the economic outlook have significantly increased and it will maintain its rate cut stance to mitigate downside risks to economic growth and adjust timing and the pace of any further rate cuts. KOSPI +0.9% higher to 2407.41, 10yr +2bp higher at KTB 2.65%, USDKRW –0.3% at 1420

New Zealand Q1 CPI rose more than expected with 0.9% q/q, 2.5% y/y (Q424: 0.5% q/q, 2.2% y/y). Tradable CPI at 0.7% q/q, 0.3% y/y while non-tradable CPI at 1.1% q/q, 4.0% y/y. Near-term higher inflation trajectory is within expectations and unlikely to alter RBNZ easing path ahead. NZX50 +0.4% to 4473.96, 10yr NZGB 6bp lower at 4.53%, NZDUSD +0.1% at 0.591

Japan March Exports dropped to 3.9% y/y from 11.4% in February, while imports rise to 2% from -0.7%. March trade balance steady around JPY 544bn surplus. This is the second straight trade surplus month since July 2021. Exports value to China -4.8% while strong to HK (19.7% y/y), Taiwan (19.5% y/y) and South Korea (11.5% y/y), Exports to U.S. at 3.1% y/y. Transportation equipment, the largest export value category, grew at 4.2% y/y with cars at 6.7% y/y, machinery at 3.8% y/y, electrical machinery at 1.4% y/y, Manufactured goods exports down -0.1%, dragged by -8.2% y/y decline in iron and steel products. Nikkei +1.4%, 10yr JGB +5bp higher at 1.31%, JPY unchanged at 142.7

Singapore March Electronic Exports posted 11.9% y/y gains from 6.9% y/y in February. Non-oil domestic exports slowed to 5.4% from 7.6% y/y. Exports to Indonesia surged 63% y/y, while exports to U.S. dropped sharply to 5.7% from 21.5% in February 2025. Exports to China stayed depressed at -29.4% y/y. STI +1.4%, 10yr SIGB +2bp at 2.56%, SGD flat at 1.313

Chinese CNY accounts for 4.13% of Swift global payment in March from 4.33% in February. USD payment rises to 49.08% while payment via EUR and GBP payment eases to 21.93% and 6.64%. JPY and CAD payment picked up the most but are low in absolute terms at 3.87% and 2.82%. SHCOMP +0.1%, 10yr CGB flat at 1.65%, CNH unchanged at 7.304

Swiss exports (adjusted, real basis) increased by 3.2%m/m in March, while imports increased by 4.5%m/m. On a seasonally adjusted basis, the trade surplus widened to CHF5.3bn. Underscoring the risks to Switzerland from tariffs on pharmaceutical products, the Swiss Government also highlighted that in the first quarter of 2025, Chemicals and Pharmaceutical product exports hit CHF43.57bn, accounting for 58% of total exports over the same period. SMI +0.01% to 11599.32, Swiss Confederation 10y Bond +1.1bp to 0.468%, USDCHF +0.61% to 0.8183.