Market Movers: Never-ending

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

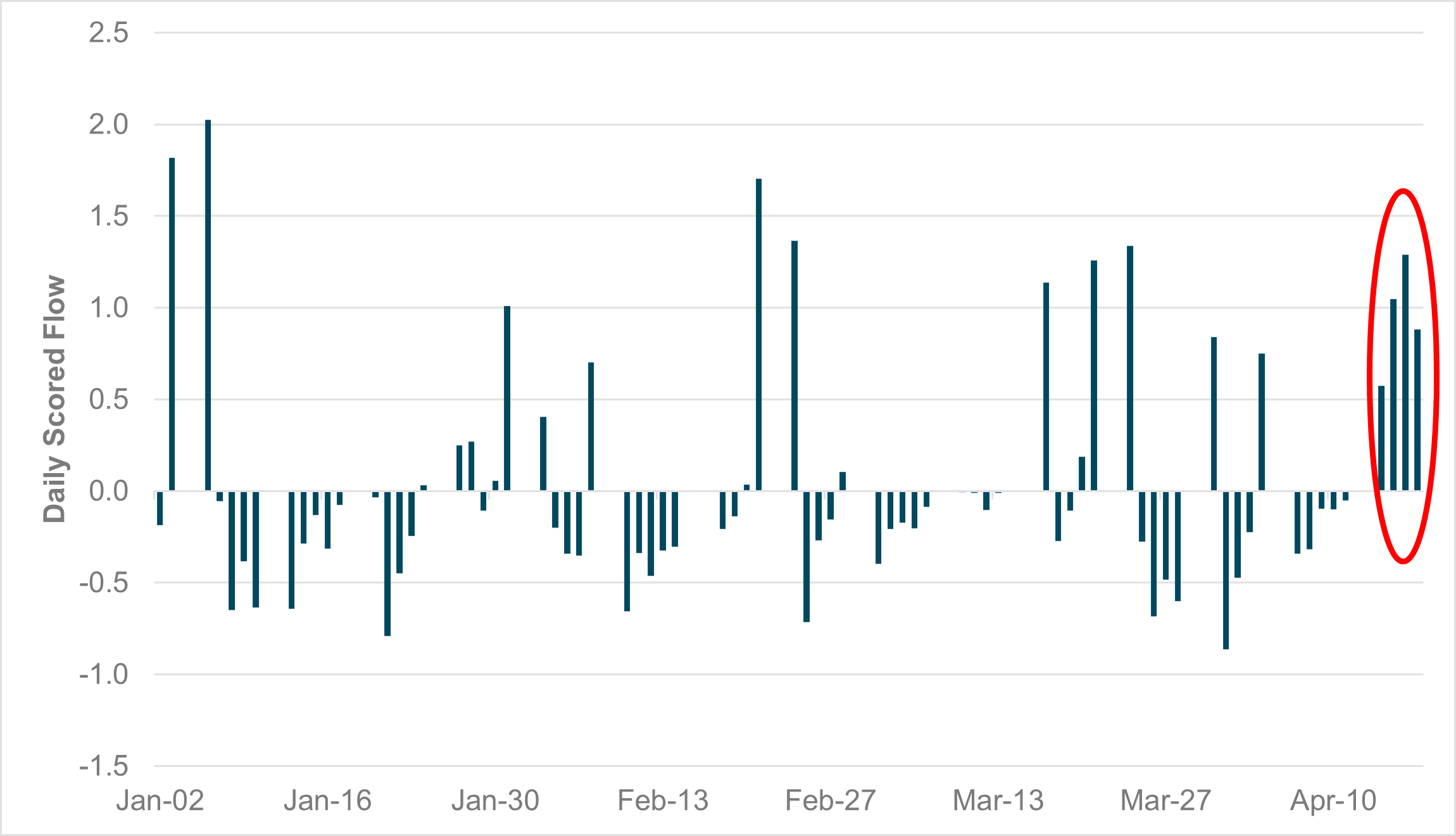

EXHIBIT #1: MATERIAL SURGE IN U.S. CASH FROM LAST WEEK ANOTHER SIGN OF RISK AVERSION

Source: BNY

iFlow data show last week’s aggregate flow in cash and short-term instruments (CAST) was the strongest year-to-date. Both domestic and international investors were active in driving up interest in cash. Selling of underlying assets was one factor as investors strengthened liquidity preference and continue to take advantage of elevated front-end yields. Cash demand was also high last week in core G5 markets, especially in the U.K. and Germany. This confirms that markets’ defensive preference remains strongly intact.

Risk mixed as Asian equity markets rally except Taiwan and Japan, and U.S. futures fall on the back of President Trump’s rebuke of Fed Chair Powell. The threat to Fed independence shows up most in the U.S. dollar, which is off over 1% today, with EUR at a 3-year high at over 1.1550. Markets remain in low volume and sketchy liquidity due to ongoing Easter holiday. The news flows overnight was filled with never-ending discussions of trade policy and responses to U.S. tariffs along with the actual data on trade from South Korea, underscoring a slowdown ahead. The death of Pope Francis and what this means for frontier and emerging markets could matter in the weeks ahead as well, with many investors looking for alternatives to G10 amid ongoing growth confusion. ECB’s hawkish talk added to the EUR gains. The JPY gains are also important and the focus there is on 140, with significant option interest, with ongoing tariff talks adding to volatility. On the day ahead, a lighter news agenda for the U.S. will leave investors focused on supply and rates, with yield curve steepening and an ongoing focus on both fiscal and monetary policy resulting in a never-ending search for the right risk premium. The risk barometer of choice remains the U.S. 10-year as it holds 4.20% and retests 4.40% – a break to either side would signal a larger view on U.S. recession risks and policy shifts.

The Holy See announced Pope Francis passed away at the age of 88 after 12 years of service – search for next pope will be unique as of the 137 cardinals eligible to vote, 109 were appointed by Francis from underrepresented places and diverse backgrounds, most have never met each other. Conclave to start in 15-20 days.

Vice President JD Vance starts a four-day visit to India. He will meet Indian Prime Minister Modi, according to the White House. Currently, India is set to face 26% tariffs on exports to the U.S. at the end of the 90-day pause in reciprocal tariffs. SENSEX +1.21% to 79504.87, 10y IGB -3bp to 6.341%, USDINR -0.35% to 85.0737.

China leaves 1y and 5y LPR rates unchanged at 3.1% and 3.60%, respectively, in line with expectations. Easing measure is likely via credit and liquidity expansion. CSI300 +0.33% to 3784.88, 10y CGB +1.6bp to 1.6632, USDCNY -0.17% to 7.2874.

South Korea first 20-day exports declined sharply by -5.2%. Exports to the U.S. and China fell -14.3% and -3.4% y/y, respectively, while shipments to the European Union rose 13.8% y/y.

U.S. March Leading Index expected to be down -0.5% after -0.3%, ending Q1 weaker – with the risk of it being worse than March 2024 – growth doubts rising.

Chicago Fed Goolsbee on CNBC – unlikely to add much to easing debate, may discuss Fed independence.

Mood: Investor sentiment worsened, as iFlow Mood dipped further to -0.26, with persistent equities outflows coupled with increasing demand for sovereign bonds.

FX: Good FX inflows day led by G10, except for U.S. dollar, which is the most sold, along with EUR and JPY. AUD, CHF, CZK, HKD, KRW and TWD posted significant inflows with >1 scored flows.

FI: Mixed and light flows. Notable flows were increasing demand for Australian government bonds, while the pace of selling of cross-border U.S. Treasury eased.

Equities: Selling pressure in APAC equities, especially in China. Elsewhere, flows in the region were mixed. Notable demand observed in European and New Zealand equities. In terms of U.S. equities, sectoral flows have been mixed, with buying in the energy, consumer staples, financial, communication services and utilities sectors.

“Life is a journey. When we stop, things don’t go right.” – Pope Francis

“Success is never ending; failure is never final.” – Robert H. Schuller

China leaves 1y and 5y LPR rates unchanged at 3.1% and 3.60%, respectively. The decisions are in line with expectations as the authorities continue to ensure monetary policy remains stimulative for the economy due to trade shocks. Note that several major joint-stock banks and small to medium-sized banks in China had lowered their deposit rates. Such measures were broadly anticipated, and investors continue to await a stronger fiscal impulse to support at-risk enterprises. CSI300 +0.33% to 3784.88, 10y CGB +1.6bp to 1.6632, USDCNY -0.17% to 7.2874.

Indonesia's trade surplus hit $4.33bn after previously reaching $3.10bn – more than the $2.64bn expected – exports unexpectedly grew by 3.16%y/y, marking the 12th consecutive month of expansion, though it was the softest pace since last June, as non-oil and gas export growth eased sharply to 2.56% from a 15.40% surge in February. The export figure easily beat expectations of a 3.4% decline, despite slowing sharply from a marginally revised 13.86% increase in the previous month. Imports rose 5.34% y/y, below forecasts of a 6.6% rise, following a 2.3% increase in February. Last year, Indonesia posted a $31.04 billion surplus, down from $36.89 billion in 2023. JCI off 0.3%, IND 10y +1.6% to 5.30%, IDR up 0.1% to 16,800.

South Korea's first 20-day exports declined sharply by -5.2%, after a positive export figure of +13.7% y/y for the first 10 days in April. Exports to the U.S. and China fell -14.3% and -3.4% y/y, respectively, while shipments to the European Union rose 13.8% y/y. Exports of semiconductors increased by 10.7% y/y, while shipments of automobiles were down 6.5% y/y. Imports decreased by 11.8% y/y. Daily average exports fell 5.2% y/y. South Korea and the U.S. will kick off trade negotiations this week. U.S. Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer will meet with South Korea’s Finance Minister Choi Sang-mok and Industry Minister Ahn Duk-geun in Washington at 8 a.m. local time Thursday. KOSPI +0.2% to 2488.42, 10y KTB -3.3bp to 2.599, USDJPY -0.52% to 1416.35.

March Tokyo condominium prices were up 37.5%y/y, +40%y/y on a per square meter basis. Unit supply has fallen by 9.8%y/y to 2,210 units. The Real Estate Economic Institute of Japan (JREI) announced that the average price per unit of condominium supplied in Tokyo increased to ¥104.85 million. Central Tokyo prices were up 19.7%y/y to ¥149.39 million. The average price for metropolitan Tokyo has surpassed ¥100 million for only the second time on record, and the price level is the second highest on record. Current trends underscore growing interest among private and institutional investors in Japan’s real estate market, especially while JPY valuations remain relatively attractive against global peers. TOPIX -1.18% to 2528.93, 10y JGB +0.2bp to 1.281, USDJPY -1.11% to 140.60.

ECB Governing Council member and Estonia Central Bank Governor Madis Muller cautioned against markets expecting more aggressive easing up ahead. He noted that the ECB should be “cautious [on] how tariffs affect inflation” and that “German public spending could also boost inflation.” Echoing the “no pre-commitment” assertion by ECB President Lagarde at last week’s post-decision press conference, Muller noted that presently “there’s no consensus on what the next decision should be.” EURUSD +1.49% to 1.1563.