Market Movers: Moments

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 10 minutes

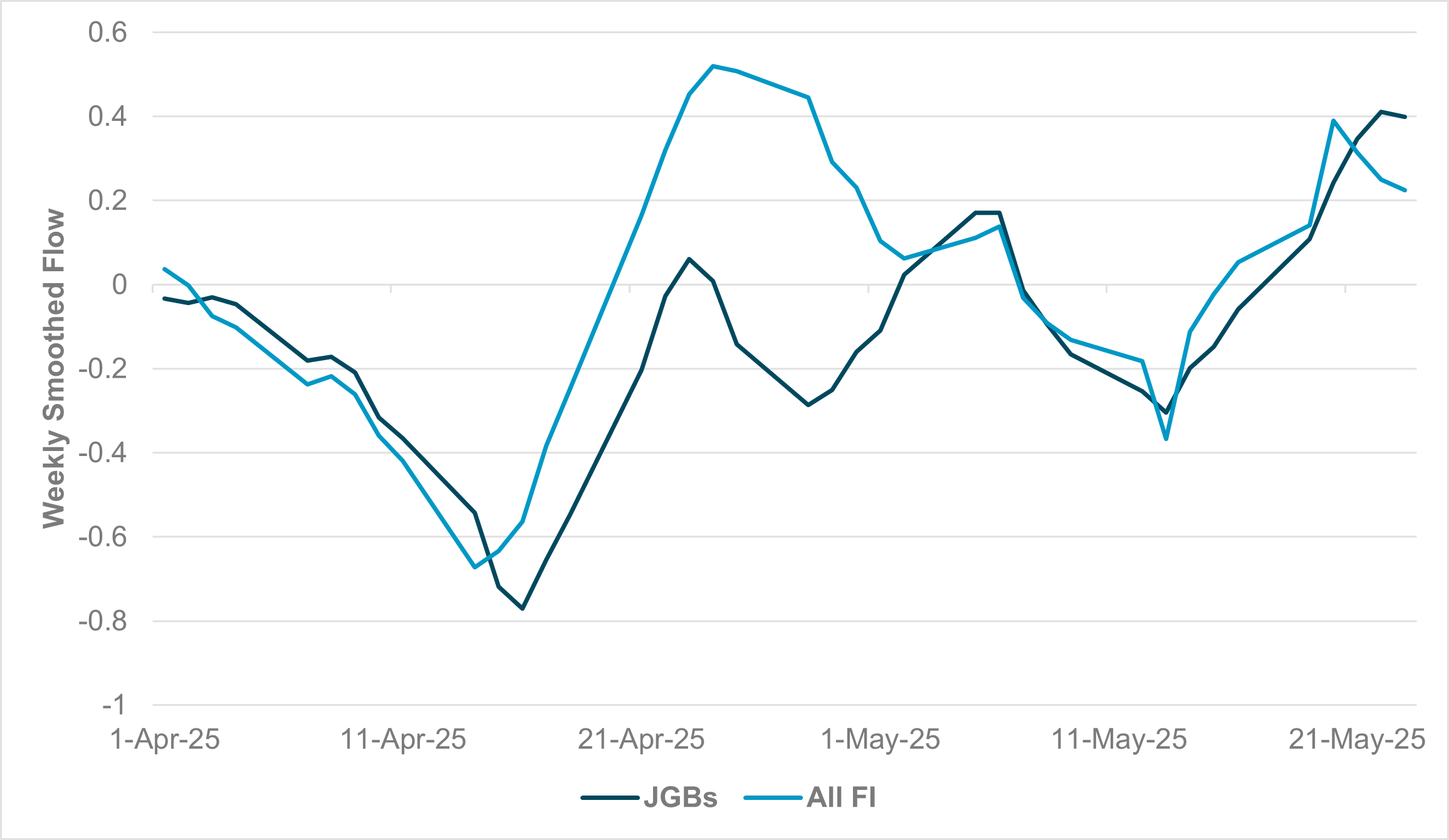

EXHIBIT #1: RISE IN CROSS-BORDER FLOW IN JGBS AND JAPANESE FIXED INCOME

Source: BNY

Global yields have begun to stabilize after several days of sharp moves in the long end of government bond curves. A common thread across economies like the U.S., the U.K. and Japan is stagflation, though the underlying drivers differ, and markets will assess each country’s financing capacity accordingly. Japan holds a strong net positive foreign asset position, and foreign ownership of its government bonds remains low. As a result, markets should have no doubts about Tokyo’s ability to manage yield curve stability. We see cross-border investors starting to see value in Japanese yields for the first time in decades. Beyond yield levels, the JPY itself remains at attractive levels to draw external capital. If Japan begins to draw down its net foreign asset position to meet domestic liabilities – particularly if new surpluses are not emerging due to trade shifts or are being retained locally due to better risk-reward in domestic markets – then Japanese fixed income, even with lower hedge ratios, offers a stronger risk-reward profile. iFlow data shows foreign interest in Japanese government bonds is at the highest level this quarter, and broader fixed income flows are also performing well. If Japanese fixed income has reached a new equilibrium, we expect sustained positive performance at current yield levels. Given the still modest share of foreign investors, we believe such inflows will be welcomed by the Bank of Japan and the Ministry of Finance.

Risk sentiment steadies after the long weekend in the U.S. and U.K., with tariffs, long-end yields and lower inflation driving equities higher. On Sunday, President Trump delayed his 50% tariffs on the EU until July 9. The EU, in turn, gave “fast-track” status to trade negotiations. This action led to a relief rally in shares on Monday, but an extension of equity buying today will depend on yields. The focus on long-end JGB yield reversals stands out, even with the BoJ’s Ueda still pushing for rate hikes and a stronger JPY. But the most important event driving markets in Europe this morning is the release of economic data as the French flash CPI dips, leading to speculation about a June rate cut and a “global euro moment.” The fear of stagflation in the U.S., U.K., Canada and even Japan continues to matter to investors and puts the focus on today’s economic data release in the U.S. The hard data has yet to catch up with the soft data, with durable goods orders a key test of this point today. There is an ongoing focus on jobs and retail spending, along with earnings and the Conference Board’s consumer confidence report. For many, any indication of the U.S. holding to a soft-landing rather than a bumpy one will be first reflected in the U.S. dollar, then U.S. bonds. The question for the week ahead is whether investors rebalance positions to favor the newfound hope of the moment – that the U.S. can avert a recession, trade deals can reduce tariffs and the U.S. tax plan can drive growth while easing debt burdens ahead.

ECB’s Lagarde suggests EUR could become a viable alternative to the U.S. dollar, providing benefits to the Eurozone. “This is a prime opportunity for Europe to take greater control of its own destiny. But this is not a privilege that will simply be given to us. We have to earn it.” Any enhanced role for the euro must coincide with greater military strength that can back up partnerships, Lagarde said. “This is because investors – and especially official investors – also seek geopolitical assurance in another form: they invest in the assets of regions that are reliable security partners and can honor alliances with hard power,” Lagarde said at a Hertie School lecture. EuroStoxx 50 +0.373% to 5415.44, EURUSD -0.317% to 1.1351, BBG AGG Euro Government High Grade EUR +1.5bp to 2.859%.

Japan MoF considers tweaking super long-end bond issuance. The MoF is reported to have sent a questionnaire to market participants regarding appropriate issuance amounts for JGBs. The MOF will make a decision after discussions with market participants around mid- to late-June, the sources said. The total planned size of JGB issuance for the current fiscal year that ends March 2026 will remain unchanged from ¥172.3tn ($1.21tn), they said. Nikkei +0.513% to 37724.11, USDJPY +0.728% to 143.89, 10y JGB -4.8bp to 1.47%.

Minneapolis Fed President Neel Kashkari emphasized the current challenge posed by tariff-driven inflation, which forces policymakers to choose between supporting economic activity and defending inflation expectations. He argued against “looking through” this inflation and supports holding rates steady to preserve credibility. Kashkari noted that previous shocks – such as the 2008 crisis and COVID-19 – highlight the risks of acting too slowly or relying on rigid rules like the Taylor rule, which can misguide policy in times of disruption. He stressed that in today’s uncertain environment informed judgment and flexibility are essential for effective monetary decision-making. S&P Mini 1.435% to 5900.5, DXY +0.431% to 99.36, 10y UST -4.4bp to 4.467%.

France’s preliminary Consumer Price Index (CPI) for May came in at 0.7% y/y, down from 0.8% in April, driven by slower service inflation and falling energy prices. Food prices are expected to increase slightly, while manufactured goods and tobacco remain stable. Month on month, CPI is set to decline by 0.1% after a 0.6% rise in April, with energy prices falling for the fourth straight month and against expectations for an expansion of 0.1% m/m. The Harmonized Index of Consumer Prices (HICP) is estimated to rise 0.6% annually and fall 0.2% over the month. CAC40 +0.154% to 7840.16, EURUSD -0.317% to 1.1351, 10y OAT -3.3bp to 3.204%.

China April industrial profit up 3.0% y/y, 1.4% ytd y/y from 2.6% y/y, 0.8% ytd y/y in March. Profit growth for high-tech manufacturing has accelerated at 9.0% ytd y/y (vs. March: 5.5% ytd y/y). The profits of semiconductor special equipment manufacturing, electronic circuit manufacturing and integrated circuit manufacturing increased by 105.1%, 43.1% and 42.2%, respectively. Profits for intelligent vehicle equipment manufacturing were up 177.4% ytd y/y, while intelligent unmanned aerial vehicle manufacturing was up 167.9% ytd y/y and wearable intelligent device manufacturing was at 80.9% ytd y/y. CSI 300 -0.537% to 3839.4, USDCNY +0.084% to 7.1924, 10y CGB +0.9bp to 1.701%.

National Bank of Hungary policy decision – no change from status quo at 6.5% expected.

U.S. April durable goods orders – consensus is a sharp -7.8% m/m decline vs. 7.5% m/m gain in March, while durable goods ex-transportation is projected to be at flat on the month. Capital goods ex-defense and air expected -0.1% m/m after +0.2% m/m.

U.S. March FHFA house prices – are expected at 0.1% m/m, unchanged vs. February.

U.S. March S&P CoreLogic Case-Schiller 20-city composite city home price index – consensus at 0.2% m/m, 4.5% y/y vs. 0.4% m/m, 4.5% y/y in February.

U.S. May Conference Board Consumer Confidence – is expected at 87 from 86 – with focus on jobs hard to get survey.

U.S. May Dallas Fed manufacturing activity – consensus sees an improvement from -35.8 to -26.1.

Fedspeakers: Richmond Fed President Barkin scheduled to be on Bloomberg TV, New York Fed Williams speaks late in moderated Tokyo session.

U.S. Treasury sells $69bn in 2y notes along with $76bn in 3m and $68bn in 6m bills.

Mood: iFlow Mood turned positive for the first time since early February, helped by increasing appetite for equities and dwindling demand for core sovereign bonds. Demand for equities is near the highs of Q3 2024.

FX: AUD and SEK remain the most sold currencies within iFlow Universe, with better demand in CZK, HKD and CNY. USD is marginally sold, while EUR and GBP posted inflows.

FI: Notable sovereign bond buying in Norway, Japan and the U.S. as well as Malaysia. Elsewhere, Chinese government bonds were bought against selling in Australia and the U.K.

Equities: DM APAC equities were lightly sold against buying in the rest for the region, especially in Peru, Poland and China. Within U.S. equities, communication services is the only sector with outflows while there are strong buying flows in the health care sector.

“We do not remember days, we remember moments.” – Cesar Pavese

“Do not dwell in the past, do not dream of the future, concentrate the mind on the present moment.” – Buddha

U.K. shop prices fell 0.1% y/y for the period May 1-7. 2025, unchanged from April and above the 3-month average of -0.2%. Non-food deflation widened to 1.5% (from 1.4%), also above the 3-month average of -1.6%. Food inflation rose to 2.8%, compared to 2.6% in April, and above the 3-month average of 2.6%. Fresh food inflation increased to 2.4% (up from 1.8%), while ambient food inflation eased to 3.3% (down from 3.7%), falling below the 3-month average of 3.6%. Retailers continue to navigate rising costs and shifting pricing dynamics. FTSE 100 +0.972% to 8802.74, GBPUSD -0.141% to 1.3545, 10y gilt -2.9bp to 4.652%.

The latest GFK survey for Germany notes that sentiment was mixed in May. The Consumer Climate Index is projected to rise moderately by 0.9 points to -19.9, its highest level since November 2024. Economic expectations increased by 5.9 points to 13.1 – marking a two-year high – while income expectations rose 6.1 points to 10.4, driven by recent wage settlements and easing inflation. However, the willingness to buy declined by 1.5 points to -6.4, and the savings indicator increased by 1.6 points to 10.0. Despite improved economic and income outlooks, consumer sentiment remains weak due to continued uncertainty over U.S. trade policy, market volatility and concerns about economic stagnation and rising unemployment. DAX +0.521% to 24152.74, EURUSD -0.317% to 1.1351, 10y Bund -3.8bp to 2.522%.

According to the Early Summer 2025 DIHK Economic Survey, business sentiment in Germany remains weak, with only 25% of companies reporting good conditions and another 25% describing their situation as poor. GDP is forecast to shrink by 0.3% in 2025. Business expectations, while slightly improved, remain negative, with 26% of firms expecting conditions to worsen and just 16% expecting an improvement. Key risks cited include economic policy (59%, near a record high), domestic demand (57%), and labor costs (56%). Export expectations declined due to U.S. tariff uncertainty, and investment plans remain subdued, with only 24% planning increases. Employment and financing conditions also remain strained.

Economic sentiment in the EU and euro area improved modestly in May after two months of decline. The Economic Sentiment Indicator (ESI) rose to 95.2 in the EU and 94.8 in the euro area, while the Employment Expectations Indicator (EEI) increased to 97.5 and 97.0, respectively. Despite gains, both indicators remain below their long-term average of 100. Consumer confidence also recovered slightly, rising by 1.4 percentage points in both regions. However, it remains well below average, at -14.5 in the EU and -15.2 in the euro area. EuroStoxx 50 +0.373% to 5415.44, EURUSD -0.317% to 1.1351, BBG AGG Euro Government High Grade EUR +1.5bp to 2.859%.

The latest South African composite leading business cycle indicator rose by 1.1% in March, supported by gains in five of seven components. Key positive drivers included growth in the real M1 money supply and a rise in residential building plan approvals. However, declines in new passenger vehicle sales and indicators from major trading partners offset some of the gains. Meanwhile, the composite coincident indicator fell by 0.5% in February, reflecting weaker wholesale, retail, and motor trade sales, lower industrial output, and reduced manufacturing capacity use. The composite lagging indicator also declined by 0.8% in the same month. JSE TOP40 +0.2% to 86293.71, USDZAR +0.108% to 17.8841, 10y SAGB -4.7bp to 10.433%.

Swiss foreign trade contracted sharply in April after two months of strong growth. Seasonally adjusted exports fell 9.2%, while imports dropped 15.6% − the steepest decline since April 2020. The chemical-pharmaceutical sector drove the downturn, with medical exports plunging 43.9%. Despite this, watch exports rose 16% to a record CHF 2.6 billion. The overall trade surplus hit a monthly record of CHF 6.3 billion due to weak imports. Exports to the U.S. dropped 36.1%, while shipments to Asia rose 4.4%, especially to China and Japan. Imports declined across most product groups and regions, with the sharpest falls in Slovenia, Italy and France. Imports of jewelry and precious items, however, rose 9.6%, providing one of the few bright spots in an otherwise weak month for inbound trade. SMI +0.277% to 12351.22, EURCHF +0.192% to 0.93655, 10y Swiss GB -3.4bp to 0.287%.

Sweden’s Economic Tendency Indicator edged down to 94.6 from 95.0 in May, reflecting continued subdued sentiment. Manufacturing confidence was steady at 100.1, aligning with the historical average, while construction rose to 100.7 – the first reading above average since December 2022. Trade sentiment was the strongest among sectors, increasing to 104.6, though price expectations eased. Service sector confidence declined to 95.9, driven by weaker demand expectations. Household confidence remained very low despite a slight uptick to 83.1, with pessimism persisting about the economy and durable goods purchases. Temporary survey questions revealed that 20% of manufacturers experienced slight output reductions due to tariff-related uncertainty, and over 40% anticipate minor future impacts. OMX +0.601% to 2525.947, EURSEK +0.175% to 10.8524, 10y Swedish GB -5.5bp to 2.353%.

Japan April PPI services eased to 3.1% from an upwardly revised 3.3% in March. Looking into the breakdown, the easing of PPI was primarily driven by transportation and postal activities at 2.9% y/y (March: 3.1%) and leasing and rental at 1.6% y/y (March: 2.5%). PSEi -0.083% to 6384.62, USDPHP +0.226% to 55.56, 10y PHGB -3.1bp to 6.235%.

South Korea May Consumer Confidence surged by 8 percentage points from 93.8 to 101.8, back to October 2024 levels prior to the “martial law” saga in December 2024. It is the largest monthly increment since October 2020. The 1-year inflation expectation dropped from 2.8% to 2.6%, the lowest since January 2022, while 3-year and 5-year inflation expectations are at 2.5%. KOSPI -0.272% to 2637.22, USDKRW +0.081% to 1371.5, 10y KTB +0.5bp to 2.77%, 30y KTB +0.5bp to 2.637%.

The Philippines government recorded a budget surplus of PHP 67.3 billion in April, a 57.5% y/y increase, driven by an 11.1% rise in Bureau of Internal Revenue (BIR) collections, particularly from corporate and value-added taxes. Total revenues reached PHP 522.1 billion, down 2.8% due to a 68.1% drop in non-tax revenues. Expenditures declined by 8.0% to PHP 454.8 billion, mainly from lower interest payments. Year to date, the government posted a PHP 411.5 billion deficit, up 79% from 2024, as spending grew 13.6%, outpacing the 3.4% rise in revenues. PSEi -0.083% to 6384.62, USDPHP +0.226% to 55.56, 10y PHGB -3.1bp to 6.235%.