Market Movers: Moderation

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

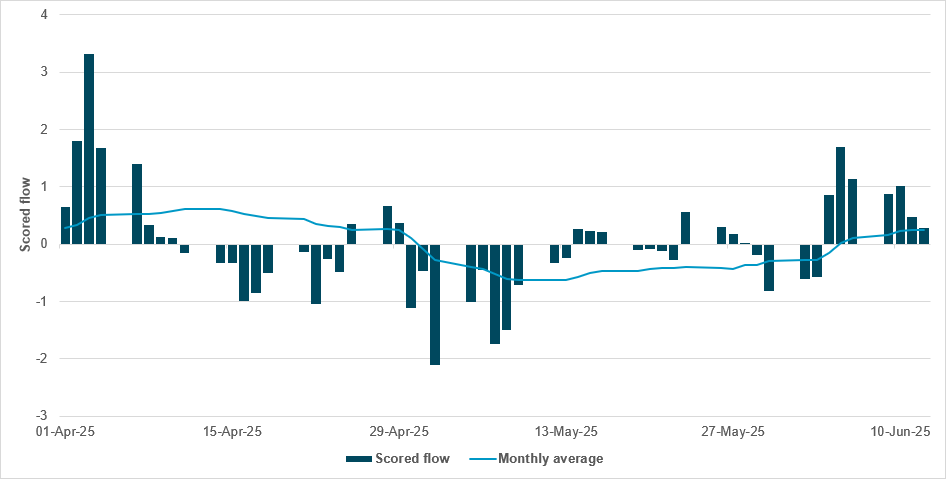

EXHIBIT #1: JPY STILL NET BOUGHT BUT MOMENTUM SOFTENING PRE-BOJ, POST IRAN

Source: BNY

JPY heads into the BoJ decision with some softening in momentum. Since the May meeting, flows have been mixed: significant sales initially due to a risk-on phase have now given way to purchases as various risk factors have come through. There is some difficulty in calibrating the currency’s impact on financial conditions vis-à-vis the moves in the JGB market, which is clearly playing a more important role in policy formation. Rather than interest rates and JPY strength, the market’s focus will be on any potential adjustment in JGB purchase operations; the direction points toward some reduction in the size of cuts to the purchase program. We would not consider this to be an “easing” step as such, given that the balance sheet is still undergoing contraction. Nevertheless, market functioning and volatility mitigation are important, especially with external factors such as geopolitics possibly generating additional stress. Japan’s exposure to oil prices remains quite acute, so there is no guarantee that risk aversion based on current factors will automatically result in JGB or even JPY purchases. Consequently, the slowdown in recent JPY purchases as risk appetite peaked may continue, but with the overall flow average quarter-to-date running at close to flat there is no broad need for mean reversion in either direction. JPY flows should consider both policy guidance and wider risk factors such as oil shocks.

Risk sentiment has reversed to slightly positive, led by hopes that the Iran-Israel conflict is nearing its end and tracking oil price reversals. Oil rose 3% at open in Asia, but is now down 0.5%. Whether this conflict escalates will be of central importance, and oil remains the main barometer. The focus on this conflict is shifting from all-consuming to one of many geopolitical events, with G7 meetings in Canada, ongoing trade deal talks in Washington and further talks between Trump and Putin on Ukraine all taking place. Moderating peace looks essential if today’s buying back of risk is to work. Investors are also wary of lessons past when it comes to oil price spikes driving more rebounds than risk aversion, as they see limitations for both Iran and Israel in sustaining a long war. The net result has been rallies in APAC and EMEA bourses, with USD lower and bond yields higher. The safe havens of JPY, CHF and gold are lower too and remain key barometers in measuring the level of market anxiety. Also overnight, the better China retail sales suggest that some of the government stimulus is working, albeit not for real estate. Trade talk progress with Japan ahead of the BoJ meeting tonight will also turn the spotlight onto the bond roll-off plans for its balance sheet. Markets will also be watching the FOMC and BoE for their guidance later in the week, all of which is a source of comfort, providing some modest stability to markets. However, the central questions for all investors remain how long the four-day conflict will last and whether it will escalate, as oil prices remain sharply higher (+13%) versus a week ago and well over their long-term 1y average of close to $66. Higher energy prices will hurt growth and drive inflation, making monetary policy decisions harder in the months ahead.

The 2025 G7 summit opens today in Canada’s Rocky Mountains, with leaders seeking to avoid the tensions that defined the 2018 meeting, when then-President Trump rejected the joint communiqué. This year, no joint statement is planned, reflecting the Trump administration’s preference for avoiding shared commitments that might conflict with its current priorities. The summit takes place amid unresolved global challenges, including wars in Ukraine and Gaza, rising tensions between Israel and Iran, and concerns over climate change, migration and artificial intelligence. President Trump is scheduled to hold bilateral meetings with Canadian Prime Minister Mark Carney, Mexican President Claudia Sheinbaum and Ukrainian President Volodymyr Zelenskyy. S&P Mini 0.56% to 6065.25, DXY -0.223% to 97.966, 10y UST +4.8bp to 4.446%.

In a speech in Frankfurt today, Bundesbank President Joachim Nagel expressed cautious optimism about Germany’s economic outlook, stating the country could become a success story if it tackles its structural challenges head-on. While recent indicators suggest the end of a prolonged period of stagnation, Nagel stressed that the path to recovery remains difficult, with trade tensions and geopolitical risks still weighing heavily. Despite euro area inflation returning to the 2% target, he warned there is no reason for monetary policy to ease, advocating continued vigilance and flexibility. Nagel concluded that increased public spending must be accompanied by structural reforms, such as expanding labor supply, cutting bureaucracy and improving investment conditions. This will lay the foundations for lasting growth. DAX +0.192% to 23561.46, EURUSD +0.243% to 1.1577, 10y Bund +4bp to 2.575%.

In May 2025, Italy’s national consumer price index (NIC) fell by 0.1% m/m and rose by 1.6% y/y, down from 1.9% in April. The slowdown was mainly due to lower inflation in regulated and unregulated energy, fresh food, recreational and personal services, and transport services. Processed food prices rose more sharply, and the fall in durable goods prices eased. Core inflation (excluding energy and fresh food) slowed to 1.9%. Goods inflation fell to 0.8% and services to 2.6%, narrowing the gap between the two. The harmonized index of consumer prices (HICP) also fell 0.1% m/m and rose 1.7% y/y, while the FOI index rose 1.4% y/y. Government data also showed that government debt had increased by almost €30bn to €3.635tn. FTSEMIB +0.503% to 39637.1, EURUSD +0.243% to 1.1577, 10y BTP +2.7bp to 3.511%.

China’s new-home prices fell 0.22% in May, marking the steepest monthly drop in seven months, while used home prices declined 0.5%, in the sharpest fall since September. The continued downturn suggests that the impact of last autumn’s stimulus measures is fading, as weaker housing demand persists amid falling incomes and corporate profits. Residential sales by value dropped 6.1% y/y in May, and real estate investment slumped 12% – the biggest fall since December. Expectations of further price declines remain widespread, further discouraging potential buyers. In response, Premier Li Qiang pledged renewed action to halt the sector’s decline during a recent State Council meeting. CSI 300 +0.249% to 3873.8, USDCNY -0.041% to 7.1803, 10y CGB -0.4bp to 1.698%.

China’s retail sales rose 6.4% y/y in May to ¥41.33tn, with retail excluding autos up 7.0%. From January to May, total retail sales reached ¥203.17tn, growing by 5.0%. Urban retail expanded by 6.5% in May, while rural sales rose 5.4%; both segments have recorded over 5% growth year-to-date. Goods retail grew by 6.5% and catering revenue rose 5.9% in May, with year-to-date figures at 5.1% and 5.0%, respectively. Among large retailers, convenience stores led with 8.5% growth, followed by specialty and supermarket sales. Online retail grew 8.5% to ¥6.04tn, with physical goods making up 24.5% of total retail; food sales surged 14.5%, while clothing and daily-use goods rose 1.2% and 6.1%, respectively.

U.S. June NY Fed Empire Manufacturing index expected to improve from -9.2 to -6.3.

U.S. Treasury sells $13bn in 20y bond reopening – testing duration appetite again – along with $76bn in 3m bills and $68bn in 6m.

Mood: iFlow Mood has eased sharply and dropped into risk-neutral zone (<0.1), driven by the rising geopolitical tension. Equity buying slowed, while demand for sovereign bonds increased.

FX: Mixed flows, with G10 inflows against EMEA outflows, with relatively muted flows in LatAm and APAC. NOK and JPY inflows stood out, against outflows in PLN.

FI: Good demand for U.S. Treasurys, Eurozone and Chinese government bonds continues. There is notable selling pressure in South Africa, followed by South Korean KTBs. G10 and APAC corporate bonds were sold across the region.

Equities: Notable selling in South Africa, Malaysia and Norway, against moderate buying in Peru. Light buying was recorded in the U.S., Japan and the U.K., against light selling in Europe. Within developed markets, materials, health care and information technology are the most favored sectors.

“Moderation is a virtue only in those who are thought to have an alternative.” – Henry Kissinger

“Temperance is moderation in the things that are good and total abstinence from the things that are foul.” – Frances E. Willard

Norway’s exports fell 5.4% m/m in May 2025 to NOK 138.2bn, down 7.4% y/y. Crude oil exports rose 3.9% on the month but remain 29% below May 2024 levels, while natural gas exports dropped 10.1% from April but increased by 5.5% y/y. Mainland exports fell 7.1% m/m, but were up 1.1% y/y. Imports edged up 0.6% from April to NOK 92.1bn, but fell 5.0% from a year earlier. The trade surplus narrowed to NOK 46.1bn, down 15.5% from April, while the mainland trade deficit widened to NOK 31.6bn. Year-to-date, exports rose by 7.6% and imports by 3.4%, with the total trade surplus at NOK 333.8bn. OSE +0.59% to 1636.97, EURNOK -0.086% to 11.4394, 10y NGB +5.2bp to 4.142%.

Türkiye’s current account posted a USD 7.86bn deficit in April 2025, or USD 1.94bn excluding gold and energy. Trade in goods recorded a USD 9.89bn deficit, while services posted a USD 3.90bn surplus, driven by net revenues from travel of USD 3.09bn and from transportation of USD 1.60bn. On a 12-month basis, the current account deficit stood at USD 15.8bn. On the financial front, April saw a USD 268mn net direct investment outflow, with residents’ external assets increasing by USD 676mn and non-resident inflows at USD 408mn. Portfolio investment posted a net outflow of USD 10.88bn, including large-scale sales of domestic debt securities. Official reserves shrank by USD 24.99bn. BI 100 -0.176% to 9295.51, USDTRY -0.001% to 39.4181, 10y TGB -8bp to 33.85%.

In April 2025, Türkiye’s trade sales volume index rose 9.6% y/y. Within this, wholesale and retail trade and repair of motor vehicles and motorcycles increased by 13.8%, wholesale trade was up 8.0%, and retail trade grew 11.5%. On a monthly basis, the overall trade sales volume fell 3.1% compared with March 2025. Wholesale and retail trade and repair of motor vehicles rose 0.2%, wholesale trade fell by 6.1% and retail trade rose by 2.8%. In other data, the government recorded a budget surplus of TRY 235.2bn in May.

In May 2025, Czech industrial producer prices fell for the fourth consecutive month, down 0.6% m/m and 0.8% y/y, mainly due to falls for energy and chemical products. Agricultural producer prices dropped 1.5% m/m but rose 15.7% y/y, with notable annual increases in fruit (+36.3%) and eggs (+43.6%), though pig prices fell. Construction work prices rose 0.4% m/m and 3.9% y/y, while service producer prices in the business sphere increased 0.2% m/m and 4.4% y/y. Gains were strongest in media and advertising services. Prices excluding energy and advertising services also showed continued annual growth. Prague SE +0.004% to 2147.93, EURCZK -0.113% to 24.794, 10y CZGB +1.4bp to 4.343%.

Switzerland’s Producer and Import Price Index fell by 0.5% m/m in May 2025, reaching 106.4 points (December 2020 = 100), with prices down 0.7% y/y. The decline was primarily driven by lower costs for mineral oil products, electricity for large consumers, metals, and petroleum and gas. Import prices also dropped for non-ferrous metals, rubber and plastic products, and energy commodities. Conversely, pharmaceutical and chemical products saw price increases on the domestic side, while computer prices rose among imports. The data reflect continued downward pressure on industrial input costs, particularly in energy and raw materials. SMI -0.37% to 12101.09, EURCHF +0.416% to 0.94083, 10y Swiss GB +3bp to 0.325%.

Switzerland’s Federal Government Expert Group revised its GDP growth forecasts for 2025 to 1.3% (from 1.4%) and for 2026 to 1.2% (from 1.6%), citing heightened global uncertainty and weaker momentum following a strong Q1 driven by services and pharmaceuticals. The outlook assumes no further escalation in U.S. trade tariffs, currently capped at 10%. Slowing global demand and high uncertainty are expected to dampen exports, industrial capacity and investment. Inflation is projected at just 0.1% in 2025 and 0.5% in 2026. Unemployment is expected to average 2.9% in 2025 and rise to 3.2% in 2026. Downside risks dominate, including financial market volatility, global debt and geopolitical instability.

U.K. June Rightmove House Price Index showed asking prices fell unexpectedly in June, with new sellers cutting prices by 0.3% (£1,277) to £378,240 – an unusual move for this time of year, driven by heightened competition among sellers. Regional disparities emerged, with price drops more pronounced in higher-priced southern regions and London due to steeper stamp duty and increased supply. In contrast, more affordable areas such as the North West, Wales, and Yorkshire and The Humber saw the fastest price growth. Despite this dip, prices remain 0.8% above last year’s levels. Buyer demand is 3% higher y/y, while listings are up 11%, making the market highly price-sensitive. Rightmove notes that homes attracting an inquiry on day one are 22% more likely to sell. FTSE 100 +0.215% to 8869.64, GBPUSD +0.082% to 1.3582, 10y gilt +2.5bp to 4.575%.

From January to May 2025, China’s fixed asset investment (excluding rural households) reached ¥191.95tn, up 3.7% y/y, with private investment flat. On a monthly basis, investment rose 0.05% in May. By sector, primary industry investment increased by 8.4% and secondary industry investment surged by 11.4%, while tertiary industry saw a 0.4% fall. Within the secondary sector, industrial investment rose by 11.6%, led by a 25.4% jump in utilities, 8.5% growth in manufacturing and a 5.8% rise in mining. Infrastructure investment within services rose 5.6%, notably in water transport (27.2%) and water management (26.6%). Regionally, investment grew fastest in the west (4.9%) and central areas (4.5%). Foreign-invested enterprises saw a 13.4% decline, while domestic and Hong Kong/Macau/Taiwan firms posted moderate growth. CSI 300 +0.249% to 3873.8, USDCNY -0.041% to 7.1803, 10y CGB -0.4bp to 1.698%.

China’s industrial output rose 5.8% y/y in May, with a m/m increase of 0.61%. Over January-May, output grew 6.3%. Mining rose by 5.7%, manufacturing by 6.2% and utilities by 2.2%. By ownership, output of state-owned firms rose 3.8%, private firms 5.9%, and foreign/Hong Kong/Macau/Taiwan-invested enterprises 3.9%. Among 41 major industries, 35 posted annual growth, with standout performances in auto manufacturing (+11.6%), electronics (+10.2%) and transport equipment (+14.6%). Steel and non-ferrous metal output rose 3.4% and 2.9%, respectively, against falls of 8.1% and 1.8% for cement and crude oil processing. New energy vehicle output surged 31.7%. The product sales rate was 95.9%, down 0.8 points y/y, while the export delivery value rose 0.6% to ¥1.27tn.

In May, China’s national urban surveyed unemployment rate was 5.0%, down 0.1 percentage points from the previous month. The rate was 5.0% for both local and migrant registered labor forces, with migrant agricultural hukou holders at 4.9%. The surveyed unemployment rate in 31 major cities also fell to 5.0%. From January to May, the national average urban surveyed unemployment rate stood at 5.2%. Nationwide, employees at enterprises worked an average of 48.5 hours per week.

Personal remittances to the Philippines rose to USD 2.97 billion in April 2025, a 4.1% increase from USD 2.86bn in April 2024. Cumulative remittances for January-April 2025 reached USD 12.37bn, up 3.0% y/y. Cash remittances sent via banks totaled USD 2.66bn in April, also growing 4.0% from the previous year. Year-to-date cash remittances rose 3.0% to USD 11.11bn. The increase was driven by higher inflows from the U.S., Saudi Arabia, Singapore and the United Arab Emirates, with the U.S. remaining the top source of cash remittances, followed by Singapore and Saudi Arabia. PSEi -0.579% to 6358.58, USDPHP +0.454% to 56.423, 10y PHGB +2.6bp to 6.31%.

New Zealand June Performance Services Index plunged further to 44.0, its lowest level since June 2024. For the sub-index results, the key results for activity/sales (40.1) and new orders/business (43.2) were also the lowest since June 2024. Employment (47.2) fell further into contraction, while deliveries (45.7) remained unchanged from the previous month. Many businesses noted reduced demand and falling revenues due to rising costs, economic uncertainty and low consumer confidence. Comments noted customers spending less, delaying decisions and responding cautiously to inflation, interest rates and broader market instability. NZX 50 +1.093% to 12690.13, NZDUSD +0.25% to 0.603, 10y NZGB +7.7bp to 4.623%.