Market Movers: Melting Up and Down

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 12 minutes

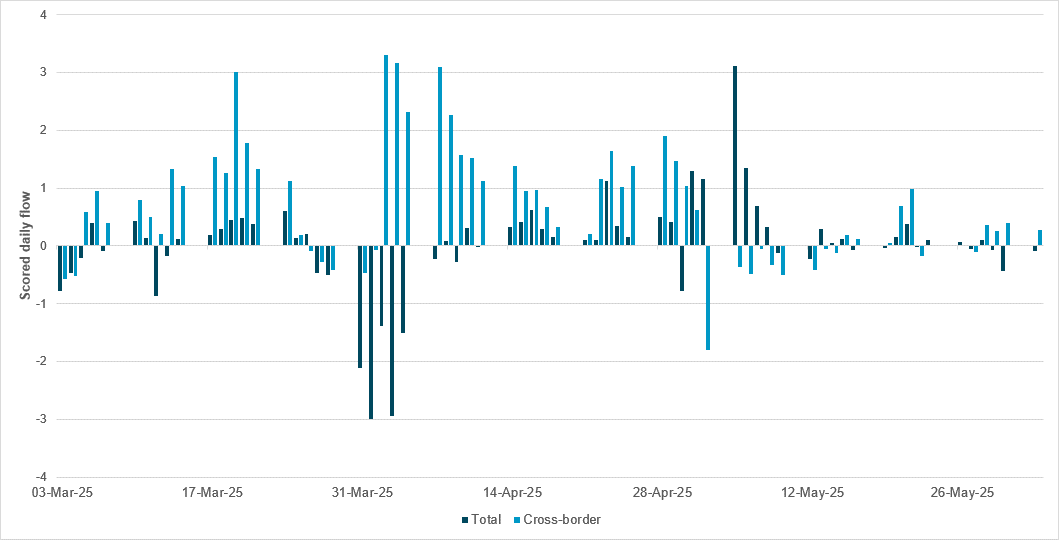

EXHIBIT #1: NEUTRAL CAD FLOWS AHEAD OF BOC DECISION

Source: BNY

CAD flows have been flat to negative over the past week, with four out of five days coming in below zero. The week before was similarly muted – generally net bought, but keeping to tight ranges. This marks a continued loss of momentum following the strong buying seen in late April and early May, when daily flow scores peaked above +3.0. The two-month average remains marginally positive at +0.01, propped up by that earlier demand surge. However, the recent stalling in flow points to a market that is now more hesitant to build exposure, possibly due to valuation constraints or BoC positioning caution ahead of this week’s policy decision. However, there is a chance of a cut, and, given the current level of flows, the prospect of a wider than expected rate gap versus the Fed could open up the currency to more significant selling in the near term. Aggregate CAD holdings remain elevated, holding above +1.0 for most of the past month, even as profitability has slipped from earlier highs. This indicates that positioning has remained sticky, with little evidence of de-risking despite a softer profitability buffer. By contrast, cross-border holdings remain steady at close to -1.0, while profitability has been consistently negative and recently weakened to -1.0. Lack of adjustment by cross-border investors indicates that an equilibrium has been reached in hedging levels and rate differentials will likely narrow for now.

Risk sentiment remains positive following another U.S. equity rally linked to better job openings. This is despite ongoing doubt over trade talks with China and the imposition of the new U.S. steel and aluminum tariffs. President Trump posted that it is “extremely hard to make a deal” with China’s President Xi. Today also brings the deadline for “best offer” letters for fast-track trade deals, ahead of the July 9 end to the reciprocal pause. As for the economic data, the PMI services report showed stalling growth in Japan and most of Europe. The more mediocre outlooks are balanced against ECB easing expectations and the German cabinet approving €46bn in corporate tax cuts today. The problems with trade uncertainty and growth remain, but the stock markets globally are bouncing and bonds are weaker with USD lower. The focus for U.S. markets remains on the hard data ahead, with ADP employment, services ISM and the Fed Beige Book all likely important to keeping the melt-up price action for risk intact. The bond markets may be the problem, given the Senate pushback on the “big, beautiful” tax bill. The risk of a surprise comes from the Bank of Canada: we expect rates to be kept nervously on hold, as new tariffs and a delayed supplemental budget from Prime Minister Carney cast further doubt on growth prospects. For investors, doubts about growth, rates supporting it, inflation that remains sticky and the value of the dollar continue to drive discussions, as they try to find safe returns in the run-up to the end of Q2.

Japan’s service sector lost momentum in May, as the country’s services PMI slipped to 51.0 from 52.4 in April, indicating only marginal growth. Softer increases in business activity and new orders led to a slowdown in job creation, now at its weakest pace since December 2023. Export demand rose, but at the slowest rate in five months. Input cost inflation eased from April’s 26-month high but remained historically elevated, prompting solid output price hikes. Despite the softer demand backdrop, business sentiment improved to a three-month high, supported by optimism around store openings, product launches and stronger demand. Nikkei +0.803% to 37747.45, USDJPY -0.056% to 143.89, 10y JGB +1.2bp to 1.506%.

Sweden’s services PMI rose to 50.8 in May from 48.7 in April, marking the first increase in three months but remaining well below the historical average of 55.6. Despite the slight rebound, growth remains sluggish, with weak business volumes and continued caution in hiring – the employment index stayed below 50 for a tenth consecutive month. All subindices improved, led by new orders and followed by employment, delivery times and business volume. The composite PMI held steady at 50.3, with services lagging behind a more expansive manufacturing sector. Input price pressures eased further, as the index for raw and intermediate goods fell to 51.4, the lowest level since October 2024. OMX +0.769% to 2506.834, EURSEK -0.119% to 10.931, 10y Swedish GB +2.3bp to 2.333%.

Germany’s services sector contracted sharply in May, with the HCOB Services PMI falling to 47.1 from 49.0 in April – its lowest level in 30 months. Weak demand, increased uncertainty and the steepest fall in new business since February 2024 weighed on activity. New business from abroad also dropped at the fastest rate since December. Despite this, employment rose marginally for a fifth straight month. Input and output price inflation eased slightly but remained above their long-term averages. The composite PMI fell to 48.5, reflecting declines in both services and manufacturing orders, with overall new business seeing its steepest drop this year. DAX +0.905% to 24309.65, EURUSD +0.229% to 1.1398, 10y Bund +0.7bp to 2.532%.

France’s service sector contracted for a ninth straight month in May, but at a slower pace, with the HCOB Services PMI rising to 48.9 from 47.3 in April. Demand remained weak, particularly domestically, prompting firms to cut prices at the fastest rate since February 2021. Employment also declined for the sixth month in a row, though only slightly. Cost inflation rose due to wages, but firms were largely unable to pass these costs on to customers. Business confidence fell to a five-year low, reflecting geopolitical concerns and domestic challenges. The composite PMI rose to 49.3, its highest level in 2025, yet still below 50. CAC40 +0.707% to 7818.72, EURUSD +0.229% to 1.1398, 10y OAT +0.9bp to 3.2%.

The U.K. service sector returned to modest growth in May, as the S&P Global Services PMI rose to 50.9 from 49.0 in April – its highest level in three months. The rebound was supported by improved client confidence, easing tariff concerns and competitive pricing. However, new business decreased again, and employment fell for the eighth consecutive month. Input costs remained high, driven by wages, though inflation eased slightly: output price inflation dropped to a seven-month low. Business optimism rose to its strongest level since October 2024. The composite PMI climbed to 50.3 from 48.5, marking a return to growth, though still near recent lows. FTSE 100 +0.142% to 8799.53, GBPUSD +0.178% to 1.3541, 10y gilt +3.1bp to 4.669%.

The Eurozone’s private sector continued to expand marginally in May, with the HCOB Composite PMI slipping to a three-month low of 50.2, from 50.4 in April. Growth was narrowly sustained by manufacturing, as services activity contracted slightly for the first time since November, as the services PMI dropped to 49.7 from 50.1. New business decreased again, especially export orders, while backlogs fell and employment rose only fractionally. Inflation eased, driven by falling manufacturing costs, though service sector price pressures remained high. Italy and Spain led regional growth, offsetting falls in Germany and continued weakness in France. Euro Stoxx 50 +0.718% to 5414.28, EURUSD +0.229% to 1.1398, BBG AGG Euro Government High Grade EUR -1.6bp to 2.781%.

U.S. May ADP employment change expected up 112k, from 62k – while usually not a driver, the data do move markets if wildly higher or lower than forecast.

U.S. May S&P final services expected 52.3 from 50.8 previously; this is usually comparable to ISM.

U.S. May ISM services expected to come in at 52 from 51.6 – combination of how services improve and mood matters to markets; recent upticks in growth, with a keen focus on prices and jobs.

Bank of Canada rate decision: no change expected at 2.75%, but this is a close call and the BoC press conference at 10.30 am is key.

Fedspeakers: Atlanta Fed Bostic and Fed Governor Cook moderate a roundtable at 8.30 am.

Fed May Beige Book expected to show some bounce-back from tariff pause, but inflation and jobs are still districts’ key focus.

Mood: Market sentiment remains solid despite renewed tariff uncertainties. IFlow Mood drifted slightly higher into risk-on territory. Demand for equities is strong, with moderating sovereign bonds inflows.

FX: Broad G10 FX outflows, especially for the Swiss franc, against APAC inflows, above all in KRW and CNY. LatAm and EMEA currency flows were mixed.

FI: A notable flow trend is rising buying of U.S. Treasurys and Singapore government bonds, against selling in Eurozone government bonds. Elsewhere, U.K. gilts and Japanese and Chinese government bonds posted light buying.

Equities: Selling flows in the Americas region, especially in the U.S. and Colombia, against buying in EMEA and APAC region. Polish equities were most bought, followed by Hong Kong and Hungary. Within U.S. equities, utilities posted the most demand, against selling in consumer discretionary, consumer staples and health care sectors.

“Most of our obstacles would melt away if, instead of cowering before them, we should make up our minds to walk boldly through them.” – Orison Swett Marden

“Yet, taught by time, my heart has learned to glow for other’s good and melt at other’s woe.” – Homer

Italy’s service sector recorded its fastest growth in nearly a year in May, with the HCOB Services PMI rising to 53.2 from 52.9 in April. The expansion was driven by resilient domestic demand, steady new business inflows and the strongest job creation since July 2024. Although export orders declined for the tenth straight month, firms showed improved optimism, with 32% expecting higher activity over the next year. However, sentiment remained below the historical average. Input costs rose due to energy and wage pressures, leading to the sharpest increase in service fees in over a year. Italy’s composite PMI also climbed to 52.5, marking a 13-month high, as manufacturing joined services in growth territory. FTSEMIB +0.193% to 40151.96, EURUSD +0.229% to 1.1398, 10y BTP +0.6bp to 3.501%.

Spain’s service sector posted its weakest expansion in 18 months in May, as the HCOB Services PMI fell to 51.3 from 53.4 in April. Growth was hindered by heightened uncertainty, particularly around tariffs, which hurt international demand – export orders declined for the first time since November. New work and business confidence also slipped to their lowest levels since late 2023. Nonetheless, firms added staff, though at the slowest pace in over a year, enabling modest backlog reductions. Input costs rose due to wages and supplier charges, yet inflation eased to its lowest level since November. Selling price increases also slowed, restrained by competitive pressures. IBEX 35 +0.14% to 14134, EURUSD +0.229% to 1.1398, 10y Bono +0.6bp to 3.116%.

Spain’s Industrial Production Index (IPI) for April 2025 rose by 0.6% y/y in the seasonally and calendar-adjusted series, despite a sharp -5.7% fall in the unadjusted series. Consumer goods led growth (+1.4%), while capital, intermediate goods and energy all posted 0.6% gains in the corrected series. The monthly change was -0.8% when adjusting for seasonal and calendar effects.

South Africa’s private sector returned to growth in May, with the S&P Global PMI rising to 50.8 from 50.0 in April. This was the highest reading since November 2024. Business activity surged at the fastest pace in four years, supported by stronger domestic demand and new project starts. New order growth accelerated to an eight-month high, though export orders declined slightly due to U.S. tariffs. Firms increased input purchases and inventories, while supply chains improved for a second month. Input cost inflation eased markedly, enabling some companies to reduce selling prices. However, employment fell amid rising backlogs and restrained hiring. JSE TOP40 +1.014% to 88065.85, USDZAR -0.48% to 17.7752, 10y SAGB -5bp to 10.077%.

Czechia’s consumer prices increased by 2.4% y/y in May 2025, with a monthly rise of 0.5%, according to the flash estimate from the Czech Statistical Office. The year-on-year growth was driven by price increases in both goods and services. Key components include energy (classified under goods, including automotive fuels), which contributed to the inflationary pressure. Prices in housing-related services, such as water supply, also rose, while other services showed moderate gains. Prague SE +0.032% to 2166.8, EURCZK -0.27% to 24.827, 10y CZGB +1.8bp to 4.182%.

Czechia’s average gross monthly nominal wage rose by 6.7% y/y in Q1 2025 to CZK 46,924, translating into a 3.9% real increase after adjusting for 2.7% inflation. The median wage reached CZK 38,385, with men earning CZK 41,677 and women CZK 35,226. Wage growth was strongest in real estate (12.4%), professional and technical activities (10.9%) and construction (10.3%). The weakest gains were in mining (3.1%) and energy supply (3.3%), though wages in both sectors remain above the average. The overall wage volume rose 7.1%, as employment grew slightly by 0.4%. Quarter-on-quarter, wages increased by 1.7% on a seasonally adjusted basis.

Australia Q1 GDP came in softer than expected at 0.2% q/q, 1.3% y/y, from 0.6% q/q and 1.3% y/y in Q4 2024. Public spending recorded the largest detraction from growth since Q3 2017. Extreme weather events reduced domestic final demand and exports. Weather impacts were particularly evident in mining, tourism and shipping. Government spending was flat, and household spending up 0.4%. Private investment rose 0.7% in Q1 2025, led by investment in dwellings, new buildings and new engineering construction, while public investment fell 2.0% q/q. Net exports detracted 0.1% from Q1 GDP. Elsewhere, the household saving to income ratio rose to 5.2% in Q1 2025 vs. 3.9% in Q4 2024. Gross disposable income rose by 2.4%, outpacing a 1.0% rise in nominal household spending. ASX +0.162% to 4773.85, AUDUSD +0.202% to 0.6475, 10y ACGB -0.9bp to 4.249%.

Australia May final services PMI came in at 50.6, a touch better than the flash estimate of 50.5, amid a weaker expansion of new business and falling export orders. Firms continued to raise staffing levels at a solid pace, which supported the clearing of outstanding work. Price pressures notably eased in the service sector in May. Output charge inflation fell to its lowest level in nearly four and a half years, as average input prices rose at a less pronounced pace.

South Korea's consumer price index (CPI) in May 2025 stood at 116.27 (2020=100), down 0.1% from April but up 1.9% y/y. Core inflation, excluding food and energy, rose 0.2% m/m and 2.0% y/y to 113.10. By category, prices for food and non-alcoholic beverages dropped sharply by 1.3% m/m, while transport fell 0.2%. In contrast, clothing, furnishings, recreation, education and restaurants all saw monthly increases of 0.2-0.3%. Annual inflation was led by restaurants and hotels (+3.3%), miscellaneous goods and services (+4.9%) and furnishings (+3.2%). Transport prices declined 1.3% y/y, marking the biggest drop among major categories. KOSPI +2.663% to 2770.84, USDKRW -0.896% to 1366.8, 10y KTB +2.3bp to 2.795%.

Hong Kong May PMI improves from 48.3 to 49.0, the fourth straight month in contraction. Companies registering only marginal drops in both output and new orders. Demand from abroad meanwhile decreased at a slower rate, while sales to mainland China were broadly stable. Firms recorded an increase in employment levels for the first time since January. On the price front, overall input costs rose at a modest pace that was the slowest in 2025 so far. Output prices were also raised, though the rate of charge inflation was only marginal. Hang Seng +0.602% to 23654.03, USDHKD +0.025% to 7.847, 10y HKGB -1.2bp to 1.417%.

Singapore May PMI came in at 51.5 from 52.8. Business conditions across Singapore further improved further in May, albeit at a reduced pace. Business activity growth moderated in tandem with a more modest uptick in new work. Pessimism resurfaced among businesses amid concerns over the outlook for growth and contributed to another fall in headcounts. Meanwhile, input cost inflation fell to a 45-month low, resulting in only a marginal rise in output charges in May. STI +0.066% to 3896.94, USDSGD -0.086% to 1.2886, 10y SGB -6.9bp to 2.358%.

Thailand May PMI was back into expansion zone at 51.2 after two months of contraction. Rising new business, supported by renewed growth in export orders, contributed to a solid rise in production. Thai manufacturers thereby raised their employment and inventory levels in May. Firms also remained strongly optimistic, even as the level of confidence eased since April. Turning to prices, charges rose for a second successive month in May to reflect higher raw material costs, though average input costs fell on the back of discounts from suppliers. SET -1.438% to 1132.66, USDTHB -0.418% to 32.693, 10y TGN -3bp to 1.782%.

India’s service sector maintained strong momentum in May, with the HSBC Services PMI at 58.8, nearly unchanged from April’s 58.7. The pace of expansion remained sharp, supported by robust domestic demand and a near-record surge in export orders – one of the strongest in the survey’s 19.5-year history. Employment rose at the fastest rate ever recorded, as firms expanded capacity to meet rising sales. Input cost and output charge inflation both intensified, driven by wages, materials and energy. Business confidence rebounded from a 23-month low, as firms expected growth from larger workforces, new clients and marketing. Composite PMI edged down slightly to 59.3. SENSEX +0.318% to 80994.17, USDINR +0.376% to 85.9137, 10y INGB +0.4bp to 6.258%.