Market Movers: Maypoles

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

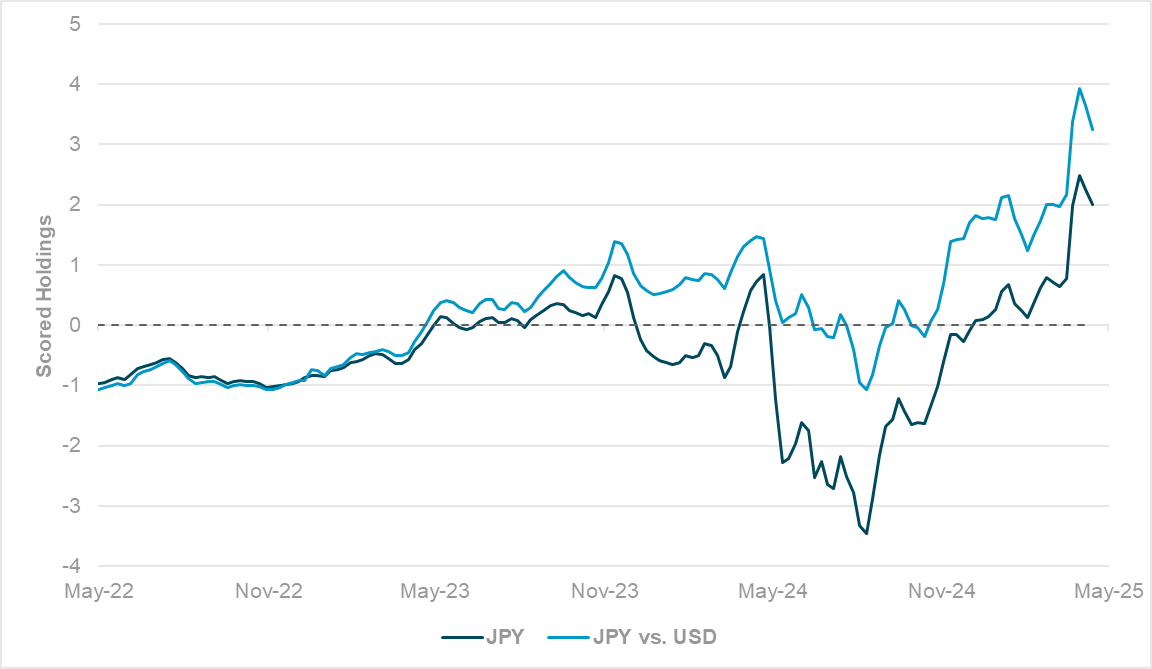

EXHIBIT #1: JPY LONGS HIT EXTREME LEVELS AHEAD OF BOJ MAY 1 DECISION

Source: BNY, iFlow

The JPY remains one of the best-held G10 currencies as risk-aversion through April generated surge flow back into the currency. Despite low yields, a strong cash preference for JPY and some concern that JPY valuations could add to the need for restrictive monetary policy led to the JPY gains. Meanwhile, symmetry remains in place between JPY vs. all FX and USD/JPY in holdings path and direction, but not in scale. Before the unwinding phase, USD/JPY underheld positions were almost twice the size of aggregate JPY vs. other FX overheld positions, which indicates that a significant carry position funded out of JPY was in place. It remains to be seen whether these JPY-funded carry trades have been fully unwound. If carry interest remains weak or the market is looking to further add to JPY longs on the crosses, there is a greater prospect of JPY moving back into balance vis-à-vis USDJPY. Although JPY strength is uncomfortable, convergence along the lines of 2022 and early 2023 would help with BoJ policy calibration, especially as much of Japan’s trade invoicing is still conducted in dollars.

Risk sentiment positive but much of Europe and some of APAC is on Labor Day holidays. The net effect has been low volume and low conviction trades. The rally back in risk started with the after-trading following Q1 earnings reports from Meta and Microsoft that beat expectations. In Asia, the most notable mover was Japan with the Nikkei up 1.13% as the BoJ sounded dovish and held rates, which translated into a weaker JPY and lower yields, with 10-year JGBs off 6bp. The BoJ’s path for rate hikes is linked to tariff talks and a deal. This is the focus for most markets and risk for the month of May from Europe to China. Global growth worries are high and the most read story overnight comes from former U.S. Treasury Secretary Yellen in the FT warning on tariffs. In the piece she says, “I’m not yet ready to say that I’m forecasting a recession, but certainly the odds have gone way up.” The counterpoint to this fear came from China state media suggesting a softening in their position. “But if the U.S. wishes to engage with China, there’s no harm in it for China at this stage,” an official CCTV account noted on social media. In another interview last night, President Trump noted his tariff policy was risky – it could cost the Republicans control of the House in 2026 – but he would not rush to make deals. For their part, the Senate with Vice President Vance breaking a tie, rejected a bill to reign in control over tariffs. The role of politics, tariffs and markets won’t let up because some traders are dancing around a maypole today. The focus will continue to be on hard economic data catching up to soft survey fears. The U.S. ISM manufacturing index and weekly jobless claims will be key. Local elections in the U.K. may also matter as polling everywhere highlights the correlation of easy policy to hard politics.

BoJ kept rates unchanged at 0.5% with unanimous vote. Its policy statement was relatively dovish, with risk to both economic activities and prices to the downside for fiscal 2025 and 2026. The Japanese central bank revised its growth forecast for fiscal 2025 and 2026 lower to 0.5% and 0.7% y/y, respectively, from its forecast of 1.1% and 1.0% in January 2025, before backing up slightly to 1% in fiscal 2027. Underlying inflation is likely to be sluggish. BoJ lowered headline inflation for fiscal 2025 and 2026 to 2.2% and 1.7%, respectively, while saying core inflation will stay steady at 2.3% y/y for fiscal 2025 before dropping below 2% to 1.8% for fiscal 2026. BoJ Governor Ueda noted that although the economy continues to recover, current uncertainty could cause the price trend improvement “to stall temporarily.” However, he warned that a “delay in price goal timing doesn’t mean delay in hikes,” underscoring that the base case for BoJ remains one of policy normalization rather than responding forcefully to tariffs. Nikkei +1.129% to 36452.3, USDJPY -0.784% to 144.2, 10y JGB -6.1bp to 1.256%.

In a sign of uncertainty creeping into the Japanese economy, the final April Japan PMI was confirmed at 48.7, indicating ongoing contraction in the economy. The report noted that this represented a decline in output for the eighth month in a row, with sharper falls in both total new work and new export orders. Business confidence is now at the lowest level since June 2020. However, the survey warned that “price indicators continued to signal historically strong increases in both input costs and output charges,” supporting the BoJ’s vigilance on price growth.

U.K. net lending secured on dwellings hit £13.0bn in March – the second highest figure on record. This was likely due to a flurry of housing transaction completions in March, ahead of the changes to the stamp duty in April, which would have pushed up the amount of tax paid on transactions. Mortgage approvals, in contrast, were weaker than expected at 64.3k (consensus: 64.5k), while other money supply indicators were in line with expectations. FTSE 100 -0.012% to 8493.85, GBPUSD +0.008% to 1.333, 10y gilt -2.1bp to 4.42%.

Australian international trade price index showed expansion in both export and import prices of 2.1% q/q and 3.2% q/q, respectively. However, export prices are now down 4.7% y/y, which points to ongoing weakness in the country’s terms of trade as commodity prices struggle. The Australian Statistics Bureau also reported that non-monetary gold prices increased by 12.4% q/q, highlighting “ongoing strength in demand for gold as a safe-haven asset and continued building of gold reserves by central banks. Also, expected easing of monetary policy globally increased the attractiveness of gold as a non-interest-bearing asset.” ASX +0.027% to 4595.28, AUDUSD -0.203% to 0.6389, 10y ACGB +2.4bp to 4.189%.

U.S. weekly initial jobless claims expected up 1k to 223k with continuing claims up 14k to 1.865mn – only a spike over 250k will move the market.

U.S. April Manufacturing ISM expected down to 47.9 from 49.0 – with a focus on prices and jobs. Prices paid expected 73 from 69.4 while jobs 44.6 from 44.7.

U.S. March construction spending expected up 0.2% m/m after 0.7% m/m. This is another indicator that Q1 GDP will be revised, which could be important for Q2 trading.

Canada April Manufacturing PMI expected 46 from 46.3 – how weak the manufacturing sector is from tariff fears matters to market pricing of BoC cuts ahead.

U.S. Q1 earnings – Apple reports after the close, adding to focus on big tech names.

Mood: iFlow Mood falls deeper into risk-off zone, driven primarily by very strong demand for sovereign bonds while flattening out of equities selling pressure. iFlow Mood was close to -0.30.

FX: Strong APAC inflows continue, especially in AUD, CNY and THB at the expense of USD outflows. EUR inflows picking up momentum with scored holding drifting higher. Notable selling of SGD into election weekend.

FI: Notable demand in Eurozone and Brazilian government bonds as well as U.S. Treasurys against selling flows in Australian, Chinese and Indonesian government bonds.

Equities: G10 biased on the sell side with demand in U.S. equities. Mixed and moderate flows in the rest of the region.

“Getting money is like digging with a needle; spending it is like water soaking into sand.” – Japanese proverb

“What’s not devoured by time’s devouring hand? Where’s Troy and where is the maypole in the strand?” – James Bramston

South Korea April exports grew 3.7% y/y to $58.2bn, while imports plunged to -2.7% y/y to $53.3bn, leaving a larger than expected trade surplus of $4884mn. Auto exports down -3.8% y/y while semiconductor exports rose 17.2% y/y. Exports to the U.S. down -6.8% y/y, driven by a fall in shipments of automobiles and machinery. Exports to the EU up 18.4% y/y, 3.9% y/y to China and 4.5% y/y to ASEAN countries. KOSPI -0.343% to 2556.61, USDKRW +0.699% to 1424.3, 10y KTB -4bp to 2.57%.

Japanese consumer confidence fell to 31.2 in April from 34.1 in March. Material declines were seen in confidence in overall livelihoods and employment. Willingness to purchase durable goods also dropped. The index is now at the lowest level since early 2023 with very little sign of a turnaround in momentum. Nikkei +1.129% to 36452.3, USDJPY -0.784% to 144.2, 10y JGB -6.1bp to 1.256%.

Final Australian Manufacturing PMI was confirmed at 51.7. S&P noted that “greater inflows of new work contributed to higher production. Purchasing activity and inventory levels also rose in tandem, while backlogs of work accumulated for the first time since November 2022.” That said, optimism slipped to the lowest level in six months, while the improvement in demand was restricted to the domestic sector amid another fall in export orders. ASX +0.027% to 4595.28, AUDUSD -0.203% to 0.6389, 10y ACGB +2.4bp to 4.189%.

Swiss retail sales increased by 2.2% y/y (real terms, working day adjusted), led by a strong recovery in non-food (ex-fuel) sales, indicating ongoing strength in core demand. While household demand remains strong, this is not translating into firmness in prices, especially in volatile components such as food and beverages, which grew by only 0.3% y/y on a nominal basis. SMI +0.417% to 12116.98, EURCHF +0.036% to 0.93567, 10y Swiss GB -8.3bp to 0.304%.

National Bank of Poland policymaker Kotecki said that a rate cut in May is a “foregone conclusion.” Annualized inflation for April surprised to the downside, which opens up policy space for a cut. On Wednesday, Polish Prime Minister Donald Tusk also called on the NBP to cut rates, in a sign that political intervention in monetary policy is evident across the global political spectrum. WIG -2.076% to 98722.91, EURPLN -0.205% to 4.287, 10y PGB -0.8bp to 5.214%.