Market Movers: Long-Term

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

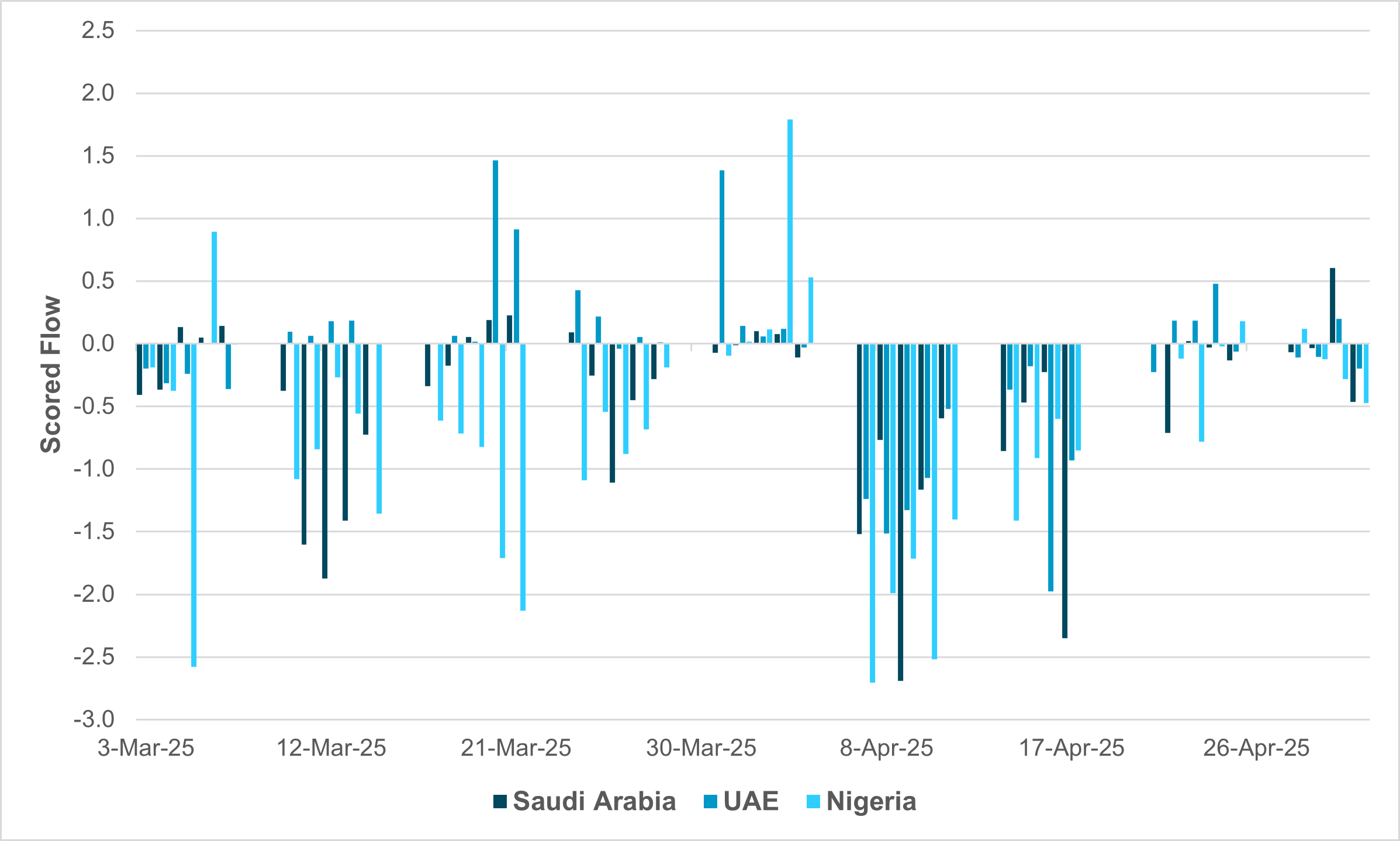

EXHIBIT #1: MENA OPEC SOVEREIGN BOND MARKETS DETERIORATE IN APRIL

Source: BNY, iFlow

OPEC’s decision to increase output will likely exert further downside pressure on oil prices. While Saudi Arabia and other key producers are pushing for a market share rather than a price strategy, we continue to express reservations about whether the financial accounts and fiscal positions of MENA oil producers can materially improve. The past two months have been extremely difficult for flows into frontier market sovereign debt. Even before the tariff announcements by the U.S. in April, our flow data show MENA oil producers such as Saudi Arabia, the UAE, and even Nigeria were facing outflows in sovereign bond markets. Dollar pegs and relatively high real yields have not helped their case, and recently, our flows have also shown negative sentiment towards Emerging- and Frontier-market sovereign bonds. Terms of trade remain a concern, and the abandonment of the price strategy will likely leave a material gap against fiscal targets. Further fiscal retrenchment across oil and broader commodity producers is necessary, though some relief might come in the form of some acceleration in Fed easing.

Risk sentiment is turning negative, but in light volume, with the May 5 holidays across the world, with Japan and the UK markets closed, leaving bond futures for the US waiting for the open. Investors faced three elections over the weekend – Australia, Singapore, and Romania – all important but are not obvious market movers. The more important stories were in oil as it fell nearly 3% at the open after OPEC+ continued to increase production, while volatility in FX markets also mattered with TWD again the focus as it rallies another 5% in 1M NDF. This rally was linked to capital inflows and highlights the ongoing importance of technology in driving global growth. Today is expected to be about how U.S. markets deal with more tariff plans – Hollywood being a new spin, but one that, like autos, is complicated with supply chains. The other focus is on the Service index ISM, where the markets expect more weakness and further signs that sentiment drives the economy. The FOMC meeting this week is widely expected to lead to a pushback on fast easing plans, with the market Friday repricing to three rather than four cuts for the rest of the year. There is a clear short-term and long-term clash for investors as the U.S. President pushes a long-term view on growth and accepts short-term pain to get there. Earnings also matter, as we have passed the midpoint and EPS beats are back, with earnings now closer to 12.5% up from 7% just 2 weeks ago. The bounce-back in shares last week has many arguing that April was the washout bottom for equity fear. Whether this holds this week will be key for such trend-chasers.

In the 2025 Australian federal election held on Saturday, Labor won an absolute majority with at least 85 seats in the 150-member House of Representatives — an increase from its previous majority. Opposition Leader Peter Dutton lost both the election and his seat of Dickson to Labor’s Ali France, marking a major political upset. The Liberal-National Coalition’s seat count fell to 39. Key issues driving the result included cost-of-living pressures, housing, and climate policy. Labor’s message of stability resonated with voters, while the Coalition’s campaign faced criticism for divisive rhetoric and unpopular fiscal proposals. ASX +1.087% to 4652.38, AUDUSD +0.637% to 0.6475, 10y ACGB +5bp to 4.27%

In Singapore’s general election on Saturday, the ruling People’s Action Party (PAP) won 87 out of 97 parliamentary seats, increasing its vote share to 65.6% from 61% in 2020. This was Prime Minister Lawrence Wong’s first electoral test since succeeding Lee Hsien Loong in 2024. Despite growing concerns over the cost of living, the PAP’s campaign focused on stability and economic resilience, resonating with voters amid global uncertainty. The Workers’ Party retained its 10 seats and secured two NCMP positions, bringing its total to 12. Voter turnout exceeded 94%, underscoring continued public support for the PAP’s leadership and its handling of national challenges. STI -0.016% to 3844.52, USDSGD +0.534% to 1.2927, 10y SGB +1.7bp to 2.496%

In Romania’s presidential election rerun held on Sunday, far-right nationalist George Simion emerged as the frontrunner, securing an estimated 30 to33% of the vote, according to exit polls. Simion, leader of the Alliance for the Union of Romanians (AUR), has run on a nationalist, Eurosceptic platform and opposes military aid to Ukraine. His candidacy was endorsed by Călin Georgescu, the pro-Russian candidate whose controversial win in the annulled 2024 election was invalidated by Romania’s Constitutional Court due to evidence of Russian interference. The Romanian Prime Minister Marcel Ciolacu, has offered his resignation in the wake of the result. The contest for second place remains tight between centrist candidates Crin Antonescu, supported by the ruling coalition, and Bucharest mayor Nicușor Dan, both polling around 21 to23%. The top two candidates will face off in a runoff on May 18. Simion’s lead raises concerns over Romania’s Western alignment, with observers warning of potential diplomatic and economic risks if he wins the presidency. BET -1.753% to 16838.98, EURRON unchanged at 4.978, 10y RGB +6.6bp to 7.536%

Swiss CPI surprised materially to the downside, coming in flat on an annualized basis and a monthly basis. Core inflation also fell to 0.6% m/m. Signs that domestic demand was starting to struggle, discretionary consumption components such as leisure goods, restaurants, and hotels all fell sharply in the month, underscoring the impact of the franc surge in April on prices. Domestic goods inflation contracted by 0.1% m/m while external goods, surprisingly, continued to expand despite more favourable FX translation. The figures further undershoot the Swiss National Bank’s conditional inflation forecast and all but guarantee a cut in June. SNB President Schlegel has also warned about the disproportionate impact of U.S. tariffs on the Swiss economy, highlighting further growth risks through the external channel. SMI +0.386% to 12301.07, EURCHF -0.039% to 0.9349, 10y Swiss GB -2.2bp to 0.335%

Taiwan’s Central Bank held an unscheduled press conference overnight amid sharp moves in the TWD. The currency strengthened by another 5% on an intraday basis on Monday, which was the most significant gain in over three decades. Meanwhile, regulators have also met with life insurers to discuss the impact of currency strength on their operations, given their exposures to U.S. bonds. The CBC acknowledged that the TWD rate has been excessively volatile of late. However, the central bank reiterated that the exchange rate issue did not come up in talks with the U.S., nor was there any requirement for the TWD to appreciate, committed to not manipulating the currency. TAIEX -1.225% to 20532.99, USDTWD +2.419% to 30.097, 10y TGB -1.8bp to 1.552%

Warren Buffett to step down as CEO of Berkshire – will leave at the end of the year and pass control to Vice Chairman Abel. Investors remain unclear how the $1.16 trillion conglomerate, which has 189 operating businesses, $264 billion of stocks and $348 billion of cash, will fare after Buffett leaves. Focus will be on the stock price reaction at the U.S. open. S&P500 futures -0.75%, USD index -0.25%to 99.77

U.S. April final services PMI expected 51.4 from 54.4 – with composite 51.2 from 53.5 – watched to see if it points in the same direction as ISM.

U.S. April ISM Services expected 50.3 from 50.8 – with focus on prices paid expected 61.4 from 60.9 and employment expected 46 from 46.2

Mood: iFlow Mood stayed in the risk-off zone on elevated demand for core sovereign bonds, supported by easing expectations, while equities selling pressure continues to ease. iFlow Mood at -0.29.

FX: USD posted the most outflows within the iFlow Universe, while broad inflows occurred globally. Notable inflows in AUD, GBP, and CNY. LatAm and G10 currencies aggregate the most over held, while APAC scored holdings had unwound previous underheld condition to near neutral.

FI: Mixed and moderate flows with demand seen in both U.S. Treasurys and Eurozone government bonds on easing expectation. Brazilian government posted the most inflows while Chinese government bonds were most sold.

Equities: US equities were bought lightly against selling pressure in the rest of G10. LatAm and EMEA were biased to selling except for Polish equities which posted strong demand. APAC equities flows were light with tentative buying flows in Chinese equities after a month of selling in April.

“Short-term thinking is the greatest enemy of good government.” – Anthony Albanese, Prime Minister of Australia

“You must have long term goals to keep you from being frustrated by short term failures.” – Charles C. Noble

The S&P Global Australia Composite PMI posted at 51 in April 2025, with the services PMI print also confirmed at 51 – the lowest figure since February but still the 15th straight month of expansion. Meanwhile, Melbourne April Institute Inflation surged from 2.8% to 3.3% y/y, the highest since April 2024 (3.7% y/y). This is the first April inflation reading and risk for the rebound of inflation, which has been broadly on a lower trajectory since the peak in early 2023. The cost of living was one of the core themes of the elections over the weekend. Despite the strong mandate achieved by the incumbent Labor Party, current realized price growth and expectations underscore the situation's urgency. It may continue to limit the RBA’s ability to cut rates more forcefully. ASX +1.087% to 4652.38, AUDUSD +0.637% to 0.6475, 10y ACGB +5bp to 4.27%

Singapore March retail sales dropped by 2.8% m/m but year-on-year, back to positive territory at +1.1% y/y from –3.5% y/y in February. Ex-auto retail sales were at 0.72% y/y. Looking into breakdown, food & alcohol, petrol, and apparel & footwear were down the most by –5.1% y/y, -8.2%, and 8.0% y/y, while spending on watches and jewelry surged 13.5% y/y. STI -0.016% to 3844.52, USDSGD +0.534% to 1.2927, 10y SGB +1.7bp to 2.496%

Turkish CPI was broadly in line with expectations at 3% m/m, translating into an annualized rate of just under 38% y/y. Although high on a nominal basis, this is the 11th straight decline for the annualized figure. The highest price hikes were seen in education with 79.2%, housing 74.07%, and health 41.99% on a yearly basis, according to TurkStat's data. Lowest rates were posted in clothing and footwear with 16.92%, communications 21.31%, and transport 22.76%. Inflation has struggled to break materially below 40% y/y, with recent volatility in the exchange rate complicating the process. However, the TCMB’s assertive hike last month will help to tighten financial conditions further and support real rates. BI 100 -0.538% to 9118.26, USDTRY -0.104% to 38.5929, 10y TGB +24bp to 34.56%

Indonesia Q1 GDP fell into a contraction at –0.98% q/q, with year-on-year at 4.87% y/y. Agriculture, Forestry, and Fishing experienced the highest growth at 10.52% y/y on the production side. Meanwhile, exports of goods and services experienced the highest growth at 6.78% on the expenditure side. The biggest drag is the –1.38% y/y drop in government spending, which aligns with the new administration's strategy. Bank Indonesia also commented overnight that it would “remain in the market to smooth out rupiah volatility”. JCI +0.718% to 6864.656, USDIDR 0% to 16435, 10y IDGB -0.5bp to 6.87%

Hungarian manufacturing PMI fell to 50.2 from a revised 51.4 in March, according to the Hungarian Association of Logistics, Purchasing and Inventory Management (HALPIM). Respondents noted slower growth compared to March following a moderate expansion in industry since June last year. The volume of new orders was unchanged, but production volume decreased. The employment index remains above 50, underscoring some tightness in the labor market, which had held back MNB from rate cuts. Budapest SI +1.422% to 93507.36, EURHUF +0.047% to 404.25, 10y HGB -1bp to 6.79%

Eurozone Sentix Investor Confidence came in at -8.1, better than expectations of -11.5 and a sharp improvement from -19.5 registered in April. The report noted that “the dust is settling…[and]…the data on the eurozone economy could be described as ‘a rollback after the rollback.” Investors are acknowledging the calm response to the U.S. tariffs so far. Both the current situation and expectations show signs of recovery. However, expectations for the U.S. had fallen to a 4-year low as tariffs were seen as an act of “self-harm”. DAX +0.468% to 23194.61, EURUSD +0.23% to 1.1323, 10y Bund -1.6bp to 2.517%