Market Movers: Linkages

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

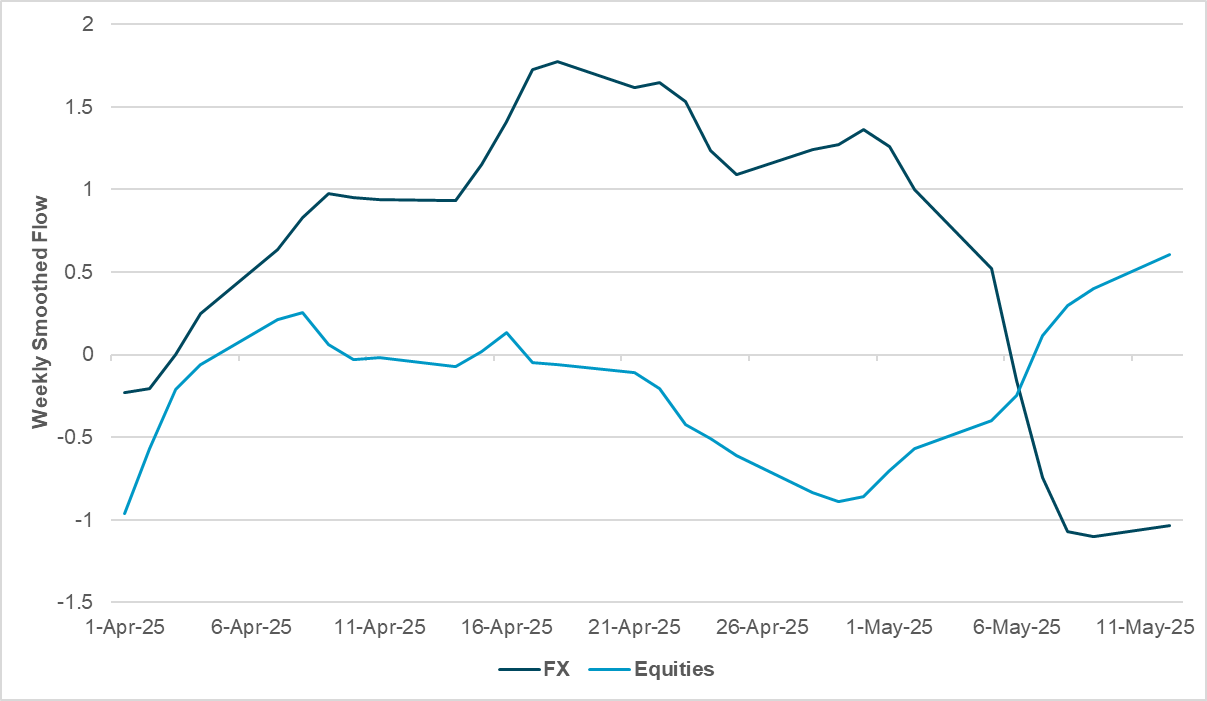

EXHIBIT #1: AUD FLOWS SHOW HEDGING OF CROSS-BORDER EQUITY INTEREST

Source: BNY

By aligning equity flows and FX flows in forwards and swaps since the beginning of April, we can see FX hedging is rising. Throughout much of April export-dominated countries faced heavy equity flows and FX hedges were unwound as a result. Now that equity sentiment has stabilized, the process is reversing. The flows largely reflect changes in equity positioning rather than any outright discretionary adjustments in currency exposures. Movements in TWD and HKD have been the most obvious examples, but we are seeing similar trends in Japan and even the U.S. among cross-border investors. Such behavior is not limited to goods exporters. AUD is an example, just as weekly smoothed flows in equities turned positive for the first time since early April, FX flow directionality has been the mirror image of equities. FX hedging of local assets should remain in place unless there is a major downward revision in U.S. rate expectations.

Risk sentiment mixed as APAC rallies, led by China, while EMEA sees profit-taking in equities. The focus on AI-led growth has helped push the MSCI emerging market index up 1.7% to a 7-month high. Easing U.S. restrictions on chips from President Trump’s Saudi visit help shift growth hopes. The issue for Europe is more straightforward as the Swedish Riksbank minutes highlight the concerns on lower activity linked to tariffs and uncertainty. The boisterous return of equities in the U.S. to flat on the year for the S&P 500 has brought even more animal spirits abroad, but European investors are already positioned for the rally while the rest of the world is catching up. The focus overnight was on the dollar as trade talks are linked to currency levels as much as U.S. reindustrialization. The nearly 2% gain of KRW from 1422 to 1390 against the USD overnight clearly matters to the region and to the overall storyline for risks as we head into the summer. Equity flows and hedging the USD are likely to continue to be linked. The role of shipping and further stockpiling of APAC exports to the U.S. will be a critical part of the data watching ahead. For the U.S. session, lack of hard economic data means more focus on the U.S. Congress and its tax bill along with a host of Fedspeakers. The lack of clarity over what matters next for investors is likely to limit some of the upside with a renewed focus on duration and risk premiums in U.S. assets. The role of the dollar in smoothing over the sharper volatility of both equities and bonds makes it the barometer of the day. We are back to the first quarter anomaly of the dollar being correlated to U.S. shares.

China USDCNY fixing fully normalized as countercyclical factor turn positive. CNH-CNY basis is close to zero and USDCNY spot is trading close to USDCNY fixings with minimal deviation. USDCNY fixings are now fully normalized and flexible to move in both directions as dictated by the market. News reports suggest that state banks were seen buying dollars to slow appreciation, though the PBoC is not pushing for active devaluation. We believe China is also seeing equity inflows, which has triggered some currency strength. Similar patterns are in place for the Hong Kong equity market, based on our data. Over the past week and a half, flow direction has fully reversed while intensity also matches: The HKD is now being net sold again – helped by the central bank – while equity interest is clearly recovering. Given the current sentiment in markets, such trends will likely continue and central banks in the region will need to push back against currency strength. CSI 300 +1.205% to 3943.21, USDCNY -0.053% to 7.2084, 10y CGB +1bp to 1.671%.

China’s total social financing stock reached ¥424.0 trillion, up 8.7% year-on-year in April. Increase in aggregate financing year to date came in at ¥16.34 trillion, behind expectations of ¥16.57, indicating ongoing weakness in credit impulse. Decomposition of financing stock indicate that RMB loans to the real economy stood at ¥262.27 trillion (+7.1% y/y), while foreign currency loans (RMB-equivalent) dropped 33.9% to ¥1.18 trillion. Entrusted and trust loans totaled ¥11.24 trillion (+0.5%) and ¥4.35 trillion (+5.6%), respectively. Corporate bond balances reached ¥32.8 trillion (+3.2%), and government bond balances surged to ¥85.93 trillion (+20.9%). Undiscounted bank acceptances fell 7.6% to ¥2.39 trillion. Equities issued by non-financial firms stood at ¥11.86 trillion (+2.9%). Structurally, RMB loans accounted for 61.9% of the total (down 0.9 ppt y/y), while government bonds rose to 20.3% of the total (up 2.1 ppt).

China’s Ministry of Commerce reiterated the country’s desire to intensify full-chain controls on strategic mineral exports to safeguard national security and development interests. In a statement released overnight, China stated that the initiative, launched on May 12, mandates strict oversight across the entire supply chain – from mining to export – to prevent illegal outflows. At a special meeting in Changsha, ten ministries and seven provinces were instructed to coordinate efforts. Authorities will improve information tracking, enforce daily supervision, and strictly punish violations. Local governments are required to map out all relevant businesses, ensure accurate registration and reporting, and raise compliance awareness. Departments will divide responsibilities, conduct regular inspections, and offer policy guidance to ensure no weak links. Beijing stated that the overarching goal is to build a robust regulatory framework that leaves no blind spots, ensuring strategic mineral controls are fully enforced and aligned with national interests.

The Riksbank released the minutes of their May 7 decision where rates were kept on hold at 2.25%. Governor Erik Thedéen supported the decision, highlighting that economic activity in Sweden and abroad is likely to weaken, potentially dampening inflation below the 2% target if the rate remains unchanged. While inflation remains elevated, it is expected to decline, barring prolonged supply chain disruptions. Thedéen stressed the difficulty in forecasting under such uncertainty, noting mixed signals: household sentiment has deteriorated while business optimism remains relatively stable. He welcomed the krona’s appreciation and recent wage agreements aligned with the inflation target, both of which help anchor price stability. However, he cautioned that trade conflicts could either reduce inflation through weaker demand or raise it via cost shocks. Thedéen concluded that while a rate cut is more likely than a hike, the Riksbank should maintain its current stance until clearer data emerges. OMX -0.255% to 2522.273, EURSEK +0.169% to 10.8588, 10y Swedish GB +0.7bp to 2.455%.

Germany’s inflation rate eased to 2.1% year-on-year in April 2025, down from 2.2% in March, as confirmed by the Federal Statistical Office’s final monthly figure. Energy prices had a strong dampening effect, falling 5.4% annually, driven by lower motor fuel and heating oil costs. In contrast, food prices rose 2.8%, with notable increases in fruit and vegetables. Core inflation, excluding food and energy, stood at 2.9%, highlighting persistent price pressures in other categories. Service prices rose 3.9% year-on-year, led by transport and healthcare. Goods inflation was modest at 0.5%, with declines in mobile phones and IT equipment offsetting other gains. Month-on-month, prices rose 0.4%, largely due to seasonal increases in air travel and holiday costs, while energy prices fell slightly. The harmonized index confirmed a 2.2% annual rise. DAX -0.215% to 23587.78, EURUSD +0.439% to 1.1234, 10y Bund -0.2bp to 2.678%.

Sweden’s final April CPI inflation rate fell to 0.3% y/y, down from 0.5% y/y in March. On a monthly basis, CPI rose by 0.1%. CPIF inflation remained at 2.3%, while CPIF-XE increased to 3.1% from 3.0%. Electricity prices fell 5.1% month-on-month and fuel dropped 3.0%. Interest expenses for owner-occupied and tenant-owned housing declined 21.8% and 25.1% year-on-year, respectively, subtracting 1.7 percentage points from CPI. Offsetting this were sharp price increases in coffee (+14.8% monthly, +42.2% annually), chocolate (+30.9% y/y), car rentals (+36.6% y/y), and international flights (+35.8% m/m). Food and non-alcoholic beverages rose 5.5% annually, and rental costs increased 5.5%, contributing 0.4 points. CPI inflation continues to be dampened by housing and energy costs. OMX -0.255% to 2522.273, EURSEK +0.169% to 10.8588, 10y Swedish GB +0.7bp to 2.455%.

Fedspeakers: Fed Governor Waller already spoke on central bank research with no new comments on the economy. Fed Governor Jefferson speaks on the economic outlook. San Francisco Fed Daly speaks in a fireside chat and Chicago Fed Goolsbee appears on NPR.

Mood: Sentiment recovery on trend with a further narrowing of iFlow Mood, supported by a pickup in equity buying magnitude along with elevated demand for sovereign bonds. iFlow Mood at -0.17.

FX: SEK, AUD, JPY, TWD and HKD posted the most outflows against good inflows in EUR and GBP. JPY scored holdings narrowed at a fast pace toward 1, while EUR scored holding broke above 1.0.

FI: Mixed and light flows globally. Notable flows were strong demand for Brazilian government bonds, followed by U.S. Treasurys.

Equities: Both EM And DM APAC were bought. DM EMEA were the most sold followed by Americas. For global equities, the health care sector was most sold, followed by the consumer discretionary and financial sectors against best demand in the real estate and consumer staple and energy sectors.

“The foundation of changing behavior is linking rewards to performance and making the linkages transparent.” – Larry Bossidy

“The increased global linkages promote economic growth in the world through two key mechanisms; the division of labor and the international spillovers of knowledge.” – Toshihiko Fukui

Hungary’s ruling Fidesz party proposed legislation to expand the central bank’s Monetary Council from 9 to eleven members, enhancing Prime Minister Viktor Orban’s influence over monetary policy ahead of the closely contested 2026 election. The bill, which also restricts the bank from engaging in non-core activities, follows a police probe into alleged misuse of public funds linked to a bank foundation under former governor Matolcsy. The central bank welcomed the reforms, which it had suggested, but did not comment on the council’s expansion. As deputy governors are appointed by Orban, the new structure ensures his sway over monetary policy for six more years. This comes as Hungary battles high inflation, prompting Orban to impose price controls and pressure banks and telecoms to lower service prices. Budapest SI +0.634% to 94729.7, EURHUF -0.067% to 404.25, 10y HGB 0bp to 6.92%.

Bank of England policymaker Catherine Mann said she voted to hold interest rates steady last week due to the U.K. labor market proving more resilient than previously expected. While there are signs of some cooling, Mann noted the adjustment is not sharp or linear. She also expressed concern about rising household inflation expectations and renewed goods price inflation. Despite potential downward pressure on import prices from diverted exports due to U.S. tariffs on China, Mann warned that U.K. retailers may use this as an opportunity to restore profit margins, keeping inflation elevated. She emphasized the need to see clear evidence of firms losing pricing power and moderating price-setting behavior before supporting rate cuts. FTSE 100 +0.101% to 8611.61, GBPUSD +0.309% to 1.3347, 10y gilt +0.5bp to 4.675%.

In a keynote speech overnight, BoE Deputy Governor for Financial Stability Sarah Breeden emphasized the need for a system-wide, macroprudential approach to supervising central counterparties (CCPs) to ensure they don’t amplify shocks during stress. She highlighted the margining “trilemma” – balancing coverage, cost and responsiveness – and warned that procyclical margin calls could destabilize markets if participants are unprepared. Breeden urged greater transparency, conservative assumptions around portfolio margining and better liquidity planning among market participants. She also called for reforms to improve resilience in core markets like gilt repo and noted the importance of the operational resilience CCPs, especially amid cyber and geopolitical risks. Coordination across institutions and jurisdictions is critical to maintaining systemic financial stability.

South Korea April Bank lending to household re-accelerates by KRW 4.8tn, the largest monthly gain since September 2024 (KRW 5.6tn) to KRW 1150tn or 4.2% y/y. This might be driven by the surging house prices in Seoul. Loans to corporates are up strongly to KRW 1338tn from KRW 1324tn. Elsewhere, South Koreas think tank Korea Development Institute cut its 2025 GDP forecast from 1.6% to 0.8%, citing weakness in the construction sector and trade conflicts. 2026 GDP is projected to grow by 1.6%. KDI sees 2025 and 2026 CPI at 1.7% and 1.8%, respectively. KOSPI +1.233% to 2640.57, USDKRW +1.147% to 1399.75, 10y KTB +3.3bp to 2.725%.

South Korea’s unemployment rate in April declined to 2.9% (2.7% on a seasonally adjusted), down 0.1 percentage points, with 854,000 people unemployed. The economically active population rose by 163,000 year-on-year to 29.74 million, with the labor force participation rate increasing slightly to 65.1%. Employment also improved, with 28.89 million people employed – up 194,000 from a year earlier – raising the employment-to-population ratio to 63.2%. Female participation and employment rates rose, while male labor force participation dipped marginally. Sector-wise, employment in manufacturing and construction fell, but the services, finance and public sectors added jobs. Daily workers and unpaid family workers declined, while regular employment rose. The economically inactive population edged up by 18,000 to 15.98 million.

Australia’s Wage Price Index (WPI) rose 0.9% on a seasonally adjusted basis in Q1, with annual growth of 3.4%. Public sector wages rose 1.0% quarterly and 3.6% annually, outpacing the private sector’s 0.9% and 3.3%. Health care and education drove growth, aided by new enterprise agreements and wage reforms in aged care and childcare. Only 21% of jobs saw wage changes this quarter, though public sector adjustments were significant. Western Australia led state growth at 1.0%, while New South Wales contributed most due to both private and public sector activity. However, NSW had the lowest annual growth (3.1%), while the ACT recorded the highest (3.9%). ASX +0.093% to 4675.69, AUDUSD +0.31% to 0.6491, 10y ACGB +5bp to 4.479%.

In the March quarter of 2025, new investment loan approvals in Australia fell by 3.7% to 47,218, with their total value down 0.3% to $32.4 billion. Owner-occupied new home loans also declined by 3.4% to 79,890, valued at $53.2 billion, and average loan sizes fell across both categories. Despite the declines, lending remained higher than a year earlier. The largest drops in investor loans were in Western Australia and South Australia. First home buyer loans for owner occupiers dropped 4.2% to 28,383, with notable falls in Queensland, South Australia and Victoria. However, refinancing between lenders rose 5.1% – the third consecutive quarterly increase – indicating continued borrower responsiveness to interest rate shifts. While the lending dip follows strong growth in 2024, figures still exceed pre-pandemic averages, suggesting resilience in the broader housing finance market.

New Zealand April total card spending is down -0.2% m/m, -1.1% y/y. Total retail spending was flat on the month or -0.6% y/y. Within retail spending, consumables (+0.5% m/m), hospitals (+0.2% m/m) and durables (+0.1% m/m) posting gains, and declines in motor vehicles (-2.9% m/m), apparel (-1.9% m/m) and fuel (-2.2% m/m). NZX 50 -0.058% to 12779.26, NZDUSD +0.371% to 0.596, 10y NZGB +2.2bp to 4.653%.

Japan April PPI eased to 4.0% from upwardly revised 4.3%, halting the seven-month uptrend and representing the first fall in the year-on-year print since August 2024. The export price index (contract currency basis) is down -0.3% m/m, -0.4% y/y, while the import price index (contract currency basis) is down -0.6% m/m, -2.6% y/y. This does not bode well for CPI evolution ahead. Nikkei -0.144% to 38128.13, USDJPY +0.718% to 146.43, 10y JGB +1.6bp to 1.46%.

India April wholesale price plunged from 2.05% to 0.85% y/y, the lowest since March 2024 (0.26% y/y). The decline was primarily driven by a fall in primary articles of -1.44% y/y and fuel, power and lighting prices of -2.18% y/y, against higher manufactured product prices at 2.62% y/y. SENSEX +0.017% to 81162.15, USDINR +0.022% to 85.3275, 10y INGB -2.7bp to 6.302%.