Market Movers: Lightning Rods

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 12 minutes

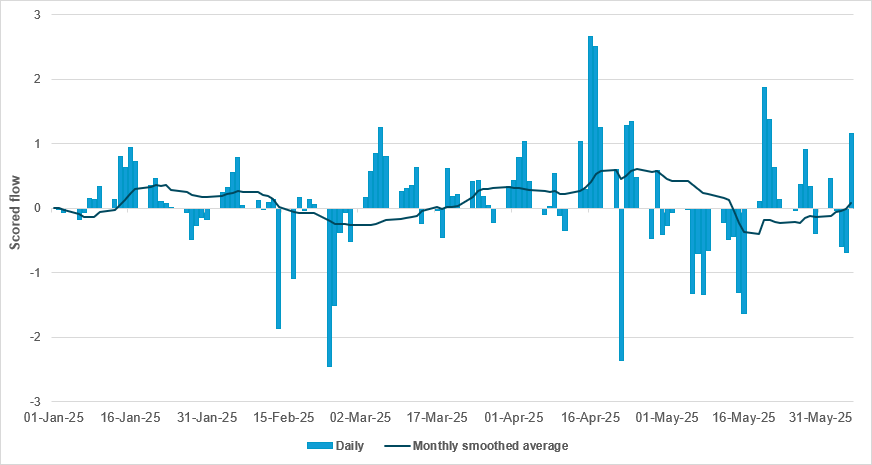

EXHIBIT #1: SURGE FLOW INTO HKD EXEMPLIFIES DEMAND FOR SAFE, PEGGED CURRENCIES

Source: BNY

We have of late been flagging the notable inflows into APAC asset markets and their impact on FX performance. Central banks in the region have been very forthright in highlighting the risks of inflows to currency arrangements, and the impact on currency board arrangements is particularly acute. HKD is under focus at present due to these pressures, and domestic funding rates have been plummeting even as the monetary authority intervenes to manage the impact on the board. Now the focus is widening to currencies with similar arrangements, both realized and potential. Most APAC savings-based economies have sufficient reserves to pin their exchange rates for an extended period, and inflows appear to be strengthening as the market continues to explore better-rated alternatives to the U.S. We find that momentum into APAC FX is not dropping, and now the liquidity preference is being felt in other cash markets, such as general cash and short-term instruments (CAST) and also local government T-bills. As such, the near-term pressure on funding costs is unlikely to ease. Our flows show that despite the ongoing fall in HKD rates, the past two weeks or so have generally seen further inflows into HKD. There are idiosyncratic factors in play, which are contributing to better liquidity, but good year-to-date flow average is a clear sign of improved preference for what usually is considered a funding currency. Furthermore, these inflows have been happening while the Fed is stepping back from further easing – a sign that USD rates are no longer driving marginal hedging/funding interest elsewhere and that portfolio exposures need to adjust accordingly.

Risk sentiment is mixed, with Chinese shares leading APAC lower as speculation on U.S./China trade talks dominates all markets. The lightning rod for fear starts with the dollar. KRW lost some ground on the NPS’s hedging stall. JPY gains yesterday added to worries about carry trade unwinding and risk aversion; however, these flipped overnight on government spending plans ahead of the election and BoJ Governor Ueda sounding a less hawkish note. EMEA saw the dollar bounce back, led by peripheral currencies. The U.K. jobs report drove GBP lower on increased rate cut expectations. Lower inflation in Norway and mixed Swedish data added to the USD bounce. The negative correlation link between dollar strength and equity weakness is in play today. Also in focus are talks between the U.S. and Iran, with oil breaking through the $65/barrel mark and the ongoing war in Ukraine, with Russia continuing large-scale air strikes on Kyiv. All the news overnight has left the markets nervously awaiting more details about talks, inflation and growth, and how the debt markets will deal with supply. The Canadian dollar bond issuance yesterday excluded U.S. banks for the first time since 2011. Brazil is planning a new panda bond to bolster China ties, after selling a dollar bond last week. Today, the focus in the U.S. will be on the Treasury sale of 3y notes as a foreshadowing of demand for 10y and 30y issues later this week. How the markets deal with debt clearly remains the second lightning rod for fears about markets. The final worry for the day is what happens in U.S. politics, with the L.A. riots continuing and the deployment of marines seen as a further escalation. The way in which that translates into markets will continue to unfold, with the Californian economy important for U.S. Q2 growth.

In the three months to April 2025, U.K. annual growth in average regular earnings (excluding bonuses) was 5.2%, while total earnings (including bonuses) rose 5.3%. In real terms, using the CPIH measure, regular pay increased by 1.4% and total pay by 1.5%. When adjusted using CPI, real regular pay rose by 2.1% and total pay by 2.3%. Regular earnings growth was 5.1% in the private sector and 5.6% in the public sector. The wholesaling, retailing, hotels and restaurants sector recorded the strongest regular pay growth, followed by the construction sector. The employment rate rose to 75.1%, while the unemployment rate increased to 4.6%. The economic inactivity rate fell to 21.3%. FTSE 100 +0.395% to 8867.13, GBPUSD -0.591% to 1.3471, 10y gilt -8bp to 4.552%.

U.S.-China trade and minerals talks in London are set to extend into a second day as both sides attempt to ease escalating tensions, particularly over rare earth exports. The Lancaster House discussions follow a temporary truce agreed in Geneva, which has run into difficulties due to the rare earths issue. President Trump has expressed optimism but offered no details, while officials are seeking concrete commitments, including easing export controls. The talks come amid economic strain in both countries, after China’s exports to the U.S. fell 34.5% in May and U.S. GDP contracted in Q1. CSI 300 -0.509% to 3865.47, USDCNY +0.14% to 7.1894, 10y CGB -0.2bp to 1.69%.

Japanese Prime Minister Shigeru Ishiba has announced that 50% growth in average pay and a ¥1 quadrillion ($6.9tn) economy will be the top campaign pledges for this summer’s upper house election. Achieving the wage goal requires annual increases of about 2.74%, slightly above recent trends. Ishiba is also aiming to reassure the public by ensuring wage growth exceeds inflation, which hit 3.5% in April, driven in part by a 98.4% surge in rice prices. To combat this, the government sold stockpiled rice directly to retailers at fixed prices. This move has proven popular, with Ishiba’s approval rating rising six points to 39% in the latest NHK poll. The ruling LDP is also considering a cash handout to counter inflation. Fiscal impulses will continue to support elevated price expectations in Japan. Nikkei +0.323% to 38211.51, USDJPY +0.083% to 144.69, 10y JGB +0.5bp to 1.473%.

South Korea’s National Pension Service is reported to have ended a five-month strategy of selling dollars in a bid to support the won. The halt was triggered when an internal threshold was reached after steady appreciation. The fund had begun reducing its dollar exposure in January when the won weakened to around 1,450 to the dollar, with potential sales estimated at $50bn. The U.S. Treasury recently kept South Korea on its currency monitoring list, urging limited intervention. In response, South Korea’s finance ministry pledged to maintain transparency and continue dialogue with the U.S. on exchange rate policy. KOSPI +0.563% to 2871.85, USDKRW +0.801% to 1365.75, 10y KTB -2.8bp to 2.862%.

U.S. May NFIB Small Business Optimism expected to improve from 95.8 to 96.0.

U.S. $58bn 3y auction with keen focus on foreign interest, previous bid/cover ratio at 2.56.

Mood: Risk-on mood continues, with ongoing strong demand for equities, while the pace of sovereign bond buying has dropped to early-April lows.

FX: Relatively light and mixed flows. Notable flows are strong MXN and PLN outflows vs. inflows into JPY, SGD and ILS.

FI: Mixed flows with better buying interest in LatAm and Chinese government bonds. Euro governments showed buying momentum after two weeks of outflow trends, while demand for U.S. Treasurys continues, but at a lighter pace. Elsewhere, Australia sovereign bonds were most sold.

Equities: South African equities were significantly sold against continued fiscal stimulus-motivated buying in South Korean equities. Overall, emerging market equities were bid while flows in developed markets were mixed. Within EM markets, the communication services sector was most sold, against good buying flows in energy, industrials and utilities.

“The best lightning rod for your protection is your own spine.” – Ralph Waldo Emerson

“Great innovators and original thinkers and artists attract the wrath of mediocrities as lightning rods draw the flashes.” – Theodor Reik

Switzerland’s consumer sentiment index rose modestly to -36.5 in May, from -38.0 in April. The outlook for personal finances improved slightly (from -35.6 to -30.3), and consumers were more positive about making major purchases (from -37.6 to -28.0). However, expectations for the broader economy deteriorated sharply, with the relevant subindex falling from -21.1 to -42.9. Assessments of past financial conditions also improved (from -57.7 to -44.8), though they remained weak. Overall, the mood among consumers remains subdued despite slight improvements in personal financial expectations. SMI -0.243% to 12336.15, EURCHF -0.154% to 0.93705, 10y Swiss GB -5bp to 0.316%.

Sweden’s private sector production rose by 2.3% m/m in April 2025 and by 3.4% y/y. Industrial production led the gains, rising by 3.4% m/m and 5.0% y/y. The strongest contributor was the chemicals and pharmaceuticals industry, up 17.5% m/m and 20.4% y/y. By contrast, paper and paper products fell 3.5% m/m and 7.5% y/y. The services sector expanded by 3.1% m/m and 3.4% y/y, driven by a 7.4% m/m rise for information and communication services. Meanwhile, real estate services fell 0.9% m/m but rose 1.6% y/y. Construction output dipped 0.4% m/m but was up 1.0% y/y. OMX +0.041% to 2513.889, EURSEK +0.042% to 10.9636, 10y Swedish GB -3.8bp to 2.33%.

Swedish household consumption rose by 0.5% m/m in April 2025 and increased 2.7% y/y at constant prices and on working-day adjusted terms. Over the latest three-month period, consumption was up 1.9% y/y. Most sectors saw annual growth, led by a 3.0% rise in retail trade (mainly food and beverages) and 4.6% for transport and motor vehicle-related spending. However, clothing and footwear fell by 1.1% y/y. Transport and motor vehicles posted the strongest m/m growth at 2.5%, while post and telecommunications saw the largest drop, down 3.2%.

Norway’s consumer price index (CPI) rose by 3.0% y/y in May 2025, while the CPI-ATE (excluding energy and tax changes) increased by 2.8%. On a monthly basis, the CPI rose 0.4% from April to May, and the CPI-ATE rose 0.2%. Key contributors to the y/y increase included food and non-alcoholic beverages, furnishings, recreation and restaurants. Meanwhile, transport and communications saw price declines over the same period. The electricity support scheme, which covers 90% of electricity costs above 75 øre/kWh for households and housing collectives, remains in effect. The electricity tax rate increased in April and is reflected in the CPI calculation through grid rental pricing. OSE +0.843% to 1597.97, EURNOK +0.251% to 11.5216, 10y NGB -2.8bp to 4.063%.

Swedish GDP increased by a seasonally adjusted 0.4% m/m in April, unchanged from the preliminary compilation of the GDP indicator. Calendar-adjusted GDP was up 1.2% y/y. Economists at Statistics Sweden noted higher household consumption and rising production in both goods and service-producing industries. Much like at the ECB, sustained data improvement will continue to undermine the case for more assertive easing, especially if forthcoming trade and tariff agreements with the U.S. reduce the prospect of large external shocks. OMX +0.041% to 2513.889, EURSEK +0.042% to 10.9636, 10y Swedish GB -3.8bp to 2.33%.

Czech consumer prices rose by 0.5% m/m in May, driven by increases in food, beverages and spa services. Year-on-year inflation accelerated to 2.4%, up from 1.8% in April, led by sharp rises in eggs (+44.3%), chocolate (+23.4%) and housing-related costs such as rents (+5.7%). Fuel prices fell, limiting further inflation. Goods prices increased by 0.9% and services by 4.9%. The 12-month average inflation rate held steady at 2.5%. The EU-harmonized index (HICP) showed Czech inflation at 2.3%, compared with 1.9% in the eurozone and 4.3% in Slovakia. Prague SE -0.209% to 2163.62, EURCZK -0.025% to 24.788, 10y CZGB -0.1bp to 4.324%.

Export price inflation in Norway slowed markedly in May, with prices received by industrial producers for goods sold abroad rising just 0.5% y/y, down from a 3.6% increase in April. This was driven by declines in key sectors such as basic metals and refined petroleum products. By contrast, prices for goods sold domestically rose 1.6% over the same period. It marks the first time since June 2024 that domestic manufacturing price growth outpaced exports. The basic metals industry saw a reversal from a 9% annual increase in April to a 0.6% decline in May. Meanwhile, imported food prices rose 9.5% y/y. Across the broader producer price index, falling oil and gas prices pulled the 12-month rate into negative territory at -0.1% in May, despite a 40.2% leap in electricity prices. These shifts reflect ongoing volatility in international markets and divergence across industrial sectors. OSE +0.843% to 1597.97, EURNOK +0.251% to 11.5216, 10y NGB -2.8bp to 4.063%.

Czech export prices fell by 0.6% m/m and 0.5% y/y in April, driven by falls for energy and tech goods. Import prices dropped 1.1% m/m and 0.8% y/y, mainly due to cheaper fuels and energy. Despite the Czech koruna’s appreciation against the U.S. dollar, only modest y/y declines were recorded after exchange rate adjustment. Key price increases were seen in wood products and food imports. Terms of trade improved to 100.6% m/m and 100.3% y/y, reflecting better relative export performance. This marks the first simultaneous annual fall in export and import prices since December 2023. Prague SE -0.209% to 2163.62, EURCZK -0.025% to 24.788, 10y CZGB -0.1bp to 4.324%.

The latest British Retail Consortium release showed U.K. retail sales rose 1% y/y in May 2025, the slowest growth this year, as non-food sales fell 1.1%, weighed down by weak demand for fashion and big-ticket items. Food sales rose 3.6%, supported by public holidays and sports events. In-store non-food sales declined 0.9%, while online non-food sales dropped 1.5%, with the online penetration rate unchanged at 35.9%. Retailers face mounting cost pressures, including £5bn from higher National Insurance contributions and wages, plus a further £2bn expected from upcoming packaging taxes. Despite brighter weather and rising travel demand, consumer sentiment remains cautious amid lingering financial uncertainty, limiting discretionary spending. FTSE 100 +0.395% to 8867.13, GBPUSD -0.591% to 1.3471, 10y gilt -8bp to 4.552%.

South Korea’s April current account eased to $5,702mn, from $9,145mn in March. This marked the 24th consecutive month in surplus, reports the Bank of Korea. The goods account recorded a strong $8.99bn surplus as exports rose 1.9% y/y to $58.57bn, while imports shrank 5.1% to $49.58bn. However, the services account posted a $2.83bn deficit, and the primary income account showed a $190mn deficit, reflecting outflows from dividends, interest and wages. Despite shrinking from March’s $9.14bn surplus, April’s figures highlight continued external strength driven by resilient exports and falling import costs. KOSPI +0.563% to 2871.85, USDKRW +0.801% to 1365.75, 10y KTB -2.8bp to 2.862%.

In May 2025, Japan’s money supply saw modest annual growth across key aggregates. M2 rose by 0.6% y/y, up from 0.5% in April, while M3 increased by 1.8%, recovering from a 4.1% decline the previous month. The narrower M1 measure, reflecting more liquid assets, grew just 0.2% y/y, improving from April’s flat reading. Broadly defined liquidity (L) expanded by 1.4% annually, continuing a slowing trend. Currency in circulation shrank by 0.4%, and quasi-money dipped by 2.4%. Certificates of deposit (CDs) fell 6.1% y/y. Overall, money supply growth remains subdued, reflecting weak credit demand and restrained economic momentum. Nikkei +0.323% to 38211.51, USDJPY +0.083% to 144.69, 10y JGB +0.5bp to 1.473%.

Japan May preliminary machine tool orders slowed to 3.4% y/y from 7.7% y/y. The gain was exclusively driven by overseas orders, which increased by 6.7% y/y; the year-to-date cumulative figure remains robust at +9.3% y/y. Domestic demand remains soft as orders fell by 5.2% y/y, with the year-to-date cumulative figure also slightly below year-earlier levels. Overall, export figures are still holding up for manufacturing despite the lack of a trade agreement with the U.S.

Australian June Westpac consumer confidence rose from 92.1 to 92.6 in “cautious pessimism” mode. Lower inflation and interest rate cuts are clear positives, but slow growth and trade disputes abroad are weighing on consumer sentiment. June saw a promising lift in buying intentions as the cost-of-living squeeze eased, but risk aversion has intensified despite positive expectations for house prices. Elsewhere, Australia May NAB business confidence improved from -1 to 2 while business conditions fell to 0.3, the lowest since August 2020 (-4.6). Overall, this survey highlights that business conditions remain weak amid ongoing profitability pressures and soft demand, with signs of a further weakening in labor demand. The fall in the latter does not bode well for Australian GDP. ASX +0.372% to 4813.82, AUDUSD -0.277% to 0.6498, 10y ACGB -1.9bp to 4.249%.