Market Movers: Holding

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

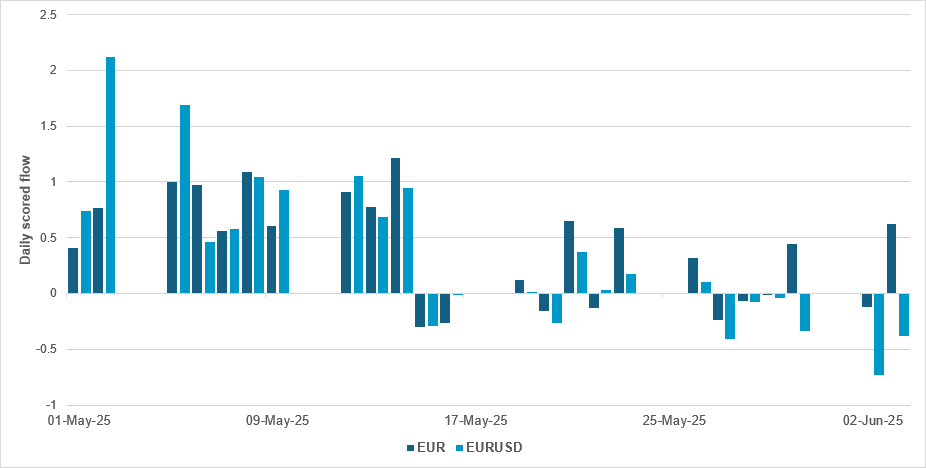

EXHIBIT #1: EUR BIDS CONTINUE AHEAD OF ECB MEETING, BUT MOSTLY ON CROSS-PURCHASES

Source: BNY

EUR is heading into the ECB decision on a relatively robust note. Over the past seven sessions, flows have held in a tight range. However, the inflow days are clearly far larger than the outflow days, increasing overall EUR holdings. Meanwhile, spot flows are broadly negative; this reflects some caution on further asset exposures, especially for Eurozone equity holdings, with levels for sovereign debt remaining robust. What is striking about current EUR flow is that it is not being driven by EURUSD and EURGBP buying. Flows in these pairs have been very light over the past week. Our flows show a 0.6 net inflow for overall EUR, despite -0.4 in outflows in EURUSD and -0.2 in EURGBP on Tuesday, in addition to flat EUR flows despite even stronger pair selling on Monday. This indicates that EUR is being strongly bought on other crosses. We suspect most of these flows are on G10 crosses, but it is another sign that markets are now much more attuned to EUR valuations, and EURUSD is no longer the best vehicle to express a positive view. Aggregate EUR holdings remain slightly above the one-year rolling average, and cross-border holdings (hedges, which are underheld EUR) are at a similar magnitude. Overall, holdings and profitability should not be material drivers for the currency for now. Underlying asset flows this week have been soft, as outflows are taking place in both equities and fixed income. We remain concerned that holdings are somewhat stretched and momentum across Eurozone assets could struggle heading into quarter-end.

Risk sentiment is positive but lacking in momentum. The ongoing tech push in China and political relief rally in South Korea led APAC, while in EMEA better Swedish and German economic data bolstered EMEA equities. Investors are awaiting the ECB decision, with expectations of further easing supporting equity uptrends. Bond markets are commanding significant attention as investors scrutinize yield curves across the U.S., Japan, South Korea and Australia, where deficit concerns have impeded duration buying. Alternatives to U.S. bonds gained, with Bunds and BTPs in Europe leading, while USD awaits more clarity. U.S. markets face important releases including trade figures and jobless claims, though Fed speakers approaching their blackout period may exert greater influence – particularly after yesterday’s weaker ISM and ADP data reinforced expectations of a September rate cut. The key focus on labor markets will be tested today and tomorrow. The increasing positive correlation between bonds and equities suggests investors are still seeking equilibrium rather than expressing clear convictions on growth and inflation. Market direction will likely be determined by USD movements in response to Fed commentary versus ECB President Lagarde’s forthcoming assessment of the global economy.

Germany’s factory orders rose 0.6% m/m in April 2025 and 4.8% y/y. Excluding large-scale orders, the monthly increase was 0.3%. The growth was primarily driven by a 21.5% surge in computer, electronics and optical equipment orders, alongside gains in other transport equipment (+7.1%) and metal products (+4.4%). However, machinery (-4.2%), electrical equipment (-9.2%) and pharmaceuticals (-14.1%) declined. Investment goods orders rose 4.1%, while intermediate and consumer goods fell 3.4% and 5.9%, respectively. Domestic orders climbed 2.2%, while foreign orders dipped 0.3% due to weaker non-Eurozone demand. Meanwhile, real industrial turnover dropped 1.5% from March. DAX +0.417% to 24192.17, EURUSD +0.467% to 1.1425, 10y Bund -0.3bp to 2.522%.

Sweden’s flash consumer price index (CPI) inflation rate for May 2025 was 0.2% y/y, down from 0.3% in April, with no change on a monthly basis. The CPIF (CPI with fixed interest rate) held steady at 2.3% y/y, with a 0.1% monthly increase. However, CPIF-XE (excluding energy) fell to 2.5% from 3.1% in April, with a 0.2% monthly rise. These preliminary figures, released ahead of the official June 13 publication, suggest moderating inflation trends, particularly when energy prices are excluded, reports Statistics Sweden. OMX +0.795% to 2507.495, EURSEK +0.007% to 10.9447, 10y Swedish GB +1.7bp to 2.327%.

Switzerland’s unemployment rate held steady at 2.8% in May 2025, while the seasonally adjusted rate edged up to 2.9%. The number of registered unemployed people fell by 2,157 to 127,944 (-1.7%). Youth unemployment fell 4.4% from the previous month but was 19.1% higher y/y. The number of job seekers dropped to 205,855 (-1.5%), although the seasonally adjusted total rose to 210,652. Vacancies reported to regional job centers (RAV) decreased by 6.7% to 38,142. In March, 2,248 people exhausted their unemployment benefits (-12.5%), and 10,007 employees were affected by short-time working (-30.5%). SMI +0.67% to 12321.6, EURCHF -0.021% to 0.9367, 10y Swiss GB 0bp to 0.242%.

Eurozone construction activity contracted more sharply in May, with the HCOB Construction PMI falling to 45.6 from 46.0 in April. Activity and new orders declined at faster rates, particularly in Germany and France, while Italy saw marginal growth. Housing remained the weakest segment, followed by commercial and civil engineering. Job cuts intensified, especially in Germany, though Italy posted modest job growth. Input cost inflation rose to a 17-month high, led by Italy, while subcontractor rates increased at the fastest pace in a year. Despite the downturn, business confidence turned positive for the first time since early 2022, driven by improving sentiment in Germany and Italy. Euro Stoxx 50 +0.454% to 5400.12, EURUSD +0.467% to 1.1425, BBG AGG Euro Government High Grade EUR -1.6bp to 2.781%.

According to the Bank of England’s Decision Maker Panel (DMP) survey – a survey of Chief Financial Officers from small, medium and large U.K. businesses – firms reported steady own-price growth of 3.5% in the three months to May, with expected year-ahead own-price inflation at 3.7%, down 0.2 percentage points from April. CPI inflation expectations were unchanged at 3.2% for one year ahead and 2.8% for three years ahead. Wage growth eased to 4.7%, with expected growth falling to 3.7%. Over 70% of firms saw no material impact from recent U.S. trade policy changes. Overall uncertainty fell, with 56% of firms reporting high or very high uncertainty. FTSE 100 +0.258% to 8809.69, GBPUSD +0.333% to 1.3562, 10y gilt -2.3bp to 4.615%.

Japan total nominal cash earnings rose 2.3% y/y, with base salaries up 2.2% y/y from 1.4% y/y in March. Regular pay increased by 2.2%, and special payments were up 4.1%. General workers earned ¥388,583 on average (+2.6%), while part-time workers earned ¥111,291 (+2.2%), with hourly wages rising 3.6%. However, real wages adjusted for inflation fell 1.8% using core CPI and 1.3% using headline CPI, reflecting rising consumer prices (4.1% and 3.6%, respectively). Wage growth based on a common sample of firms showed a 2.6% increase for both full-time and part-time workers. Nikkei +0.803% to 37747.45, USDJPY -0.535% to 143.2, 10y JGB +1.2bp to 1.506%.

China Caixin May PMI services growth May at 51.1 (April 50.7) on domestic demand uptick. Stronger domestic demand lifted new business and employment, though export orders declined for the first time in 2025. Firms faced rising input costs, driven by higher purchase prices and wages, but continued to cut selling prices for the fourth consecutive month due to competitive pressures. Optimism about future activity improved modestly. However, the Caixin Composite PMI dropped to 49.6, the first contraction since December 2022, as manufacturing output weakened, dragging down overall business activity. CSI 300 +0.434% to 3868.74, USDCNY -0.083% to 7.1824, 10y CGB -0.3bp to 1.704%.

ECB rate decision with forecast call for 25bp deposit facility rate cut to 2.0%.

U.S. April trade balance expected to improve to $-66.5bn deficit, from $-140.5bn in March.

U.S. Q1 final non-farm productivity and unit labor cost expected to be similar to flash at -0.8% q/q and 5.7% q/q.

U.S. weekly jobless claims forecast to drop 5k to 235k with continuing claims off 9k to 1.910mn.

Canada April international merchandise trade deficit is expected to widen to $-1.5bn, from $-0.51bn in March 2025.

Fedspeakers: Fed Governor Adriana Kugler speaks on the economic outlook and monetary policy at the Economic Club of New York; Philadelphia Fed President Patrick Harker gives remarks on the economic outlook at an event at the Philadelphia Fed; Kansas City Fed President Jeff Schmid speaks on banking policy at an event hosted by the Kansas City Fed.

Mood: Broad equities performance has seen continued strong demand for equities, while the lower core sovereign bond yield has not attracted a pick-up in bond buying, but seen a further easing in demand. iFlow Mood shifted higher into risk-on territory at 0.13.

FX: Flows in G10 were biased toward selling, with notable outflows in AUD, CHF and NOK. Flows in EMEA were light, but there were good inflows in CLP and PEN. APAC FX were mixed, with KRW and TWD recording the most inflows and outflows within the iFlow Universe.

FI: Selling of Eurozone government bonds continued, against continued demand for U.S. Treasurys and lighter buying in U.K. gilts and Japanese JGBs. Elsewhere, good buying was seen in Chinese and Singapore government bonds.

Equities: U.S., Colombian and Czech equities were most sold, against the best buying flows in Poland. Elsewhere, G10 and LatAm equities were biased toward selling, while flows in the EMEA and APAC regions were mixed.

“Life is not a matter of holding good cards, but of playing a poor hand well.” – Robert Louis Stevenson

“Courage is fear holding on a minute longer.” – George S. Patton

Italy’s retail sales rose in April 2025, with a 0.7% monthly increase in value and a 0.5% volume growth. Food sales led the gains, up 1.3% in value and 0.9% in volume, while non-food sales rose marginally. On a quarterly basis, sales edged up 0.1% in value but fell 0.4% in volume. Year-on-year, retail sales jumped 3.7% in value and 1.9% in volume, driven entirely by strong food sales (+8.6% in value, +5.4% in volume), likely due to the timing of Easter. Non-food sales declined y/y. Sales rose for large retailers (+6.8%) and small stores (+0.9%), but dropped slightly for non-store (-0.1%) and online (-0.7%) channels. FTSEMIB -0.037% to 40059.59, EURUSD +0.467% to 1.1425, 10y BTP -0.5bp to 3.49%.

UK construction activity declined in May 2025, though at the slowest pace in four months, with the PMI rising to 47.9 from April’s 46.6. Residential construction saw the steepest drop (45.1), while commercial work nearly stabilized (49.5). New orders fell modestly, and companies continued to cut jobs, in the sharpest decrease in employment since August 2020. Purchasing activity dropped for the sixth straight month, easing supply pressures and improving delivery times. Input costs rose further, though at a slower pace. Despite weak demand and squeezed margins, business optimism improved, with hopes tied to easing interest rates and future infrastructure projects. FTSE 100 +0.258% to 8809.69, GBPUSD +0.333% to 1.3562, 10y gilt -2.3bp to 4.615%.

New Zealand Q1 seasonally adjusted total building volume was flat q/q compared with Q4 2024. Residential rose 2.6% q/q, while non-residential fell -3.9% q/q. The total building value was $7.6 bn, down -10% vs. Q1 2024, with residential construction prices rising 0.6% q/q and non-residential prices 0.2% q/q. NZX 50 +1.359% to 12494.71, NZDUSD +0.517% to 0.6029, 10y NZGB -6bp to 4.543%.

Japan portfolio update as of 30 May 2025. Japanese investors net sold foreign bonds at ¥-118bn after three weeks of buying. Japanese investors’ sales of foreign equities accelerated. Last week’s selling of ¥-11,44bn was the second-largest weekly total of the year. Foreign investors net bought ¥1,165bn of JGBs for the first time in five weeks. Demand for JGBs was still at a record YTD pace of ¥10,715bn. Foreign investors posted nine straight weeks of buying in Japanese equities, at ¥336bn vs. ¥306bn the previous week, bringing the year-to-date total to a positive ¥978bn. Meanwhile, a 30y JGB auction was poorly received, with a larger tail at 3.4bp against a 2bp tail at the May auction; however, short covering outweighed this negative, with the JGB yield lower on the day. Nikkei +0.803% to 37747.45, USDJPY -0.535% to 143.2, 10y JGB +1.2bp to 1.506%.

Australia April exports declined -2.4% m/m from a downwardly revised 7.2% m/m, while imports grew by 1.1% m/m from -2.4% m/m in March. On the year, export and import growth is 4.0% y/y and 5.6% y/y respectively, leaving a smaller trade surplus of $5,413mn (exports: $44,075mn; imports: $38,661mn), from $6,892mn in March. Looking into the breakdown, exports to U.S. cooled substantially at 23.2% y/y (March: 189.4% y/y), while exports to China turned positive for the first time since December 2023, at 2.0% y/y, and the figures for South Korea and India were -8.3% y/y and -18% y/y, respectively. Elsewhere, Australia April household spending held steady at 3.7% y/y, from an upwardly revised 3.8% in March. ASX +0.272% to 4779.11, AUDUSD +0.573% to 0.6499, 10y ACGB -0.9bp to 4.249%.

South Korea Q1 final GDP stood unchanged, at -0.2% q/q. Year-on-year GDP was revised up to 0% (vs flash -0.1%). On the production side, manufacturing came in at -0.6% q/q (Q4: +0.1% q/q), mainly due to decreases in chemicals & chemical products and machinery & equipment. Construction came in at -0.4% q/q (Q4: -4.4%), led by a decrease in building construction. Services decreased by -0.2% q/q (Q4: +0.3% q/q), as transportation & storage and real estate decreased while finance & insurance and information & communication increased. On the expenditure side, private consumption was down -0.1% q/q (Q4: 0.2%), government consumption was flat (Q4: 0.4%), construction investment fell -3.1% q/q (Q4: -4.1%), and investment in intellectual property products grew 1.5% q/q (Q4: 0.9%). The gross saving ratio (gross saving/gross national disposable income) stood at 34.9% vs. 35.4% in Q4 2024, as final consumption expenditure (+0.7%) grew faster than gross national disposable income (+0.1%). KOSPI +2.663% to 2770.84, USDKRW -0.954% to 1366, 10y KTB +9.7bp to 2.892%.

Bank of Korea warned of the risk of South Korea falling into long-term stagnation without precise macroprudential management and swift structural reforms. The BoK cited that South Korea’s private debt ratio stood at 207.4% of GDP as of 2023, approaching the peak level of Japan’s bubble era (214.2% in 1994). There are also significant concerns about resource allocation distortion, as funds are excessively concentrated in the real estate sector, which has lower productivity than manufacturing.

Philippines May CPI eased from 1.4% to 1.3% y/y and marked a fourth successive m/m decline at -0.1% (April: -0.4% m/m). Core inflation was unchanged at 2.2%. Looking into the breakdown, transport -2.4% y/y (April: -2.1% y/y) was the main drag, followed by housing, water & electricity at 2.3% y/y (2.9% y/y). Rice inflation fell further to -12.8% y/y from -10.9% in April. Overall, food inflation is at the lower end of the range at 0.7%, with food & non-alcoholic beverages +0.9% y/y, while alcoholic beverage and tobacco prices were up 3.8% y/y (April 3.7%).

Singapore April retail sales posted a 0.3% m/m gain after a -2.7% drop in March. On the year, retail sales growth unexpectedly fell to 0.3% from an upwardly revised 1.3%, while retail sales ex-auto grew 0.8% y/y (March 0.9% y/y). Online sales growth remained strong at 12.6% vs. 13.3% previously. Within the retail trade sector, the computer & telecommunications equipment industry recorded y/y sales growth of 14.8%. Sales of watches & jewelry increased 12.9%, due to higher sales of jewelry, while sales of recreational goods rose 4.9%. In contrast, petrol service stations and retailers of apparel & footwear recorded y/y declines in sales of -10.6% and -10.3%, respectively.

Taiwan’s consumer price index (CPI) fell 0.27% m/m in May 2025, driven by sharp declines in fuel (-5.25%), vegetables (-3.72%) and garments (-1.55%). Core CPI dropped 0.08%. Year-on-year, CPI rose 1.55%, led by surges in fruit (+18.56%), meat (+4.80%) and dining out (+3.50%), while vegetables and eggs decreased sharply. Core CPI increased by 1.61%. The producer price index (PPI) plunged 4.63% versus April and 4.30% y/y due to steep drops in petroleum, chemicals, metals and electronics prices. However, farm product and utility prices partially offset these losses. The import price index slipped 2.60% y/y, while the export price index dropped 0.69%.