Market Movers: High Alert

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 12 minutes

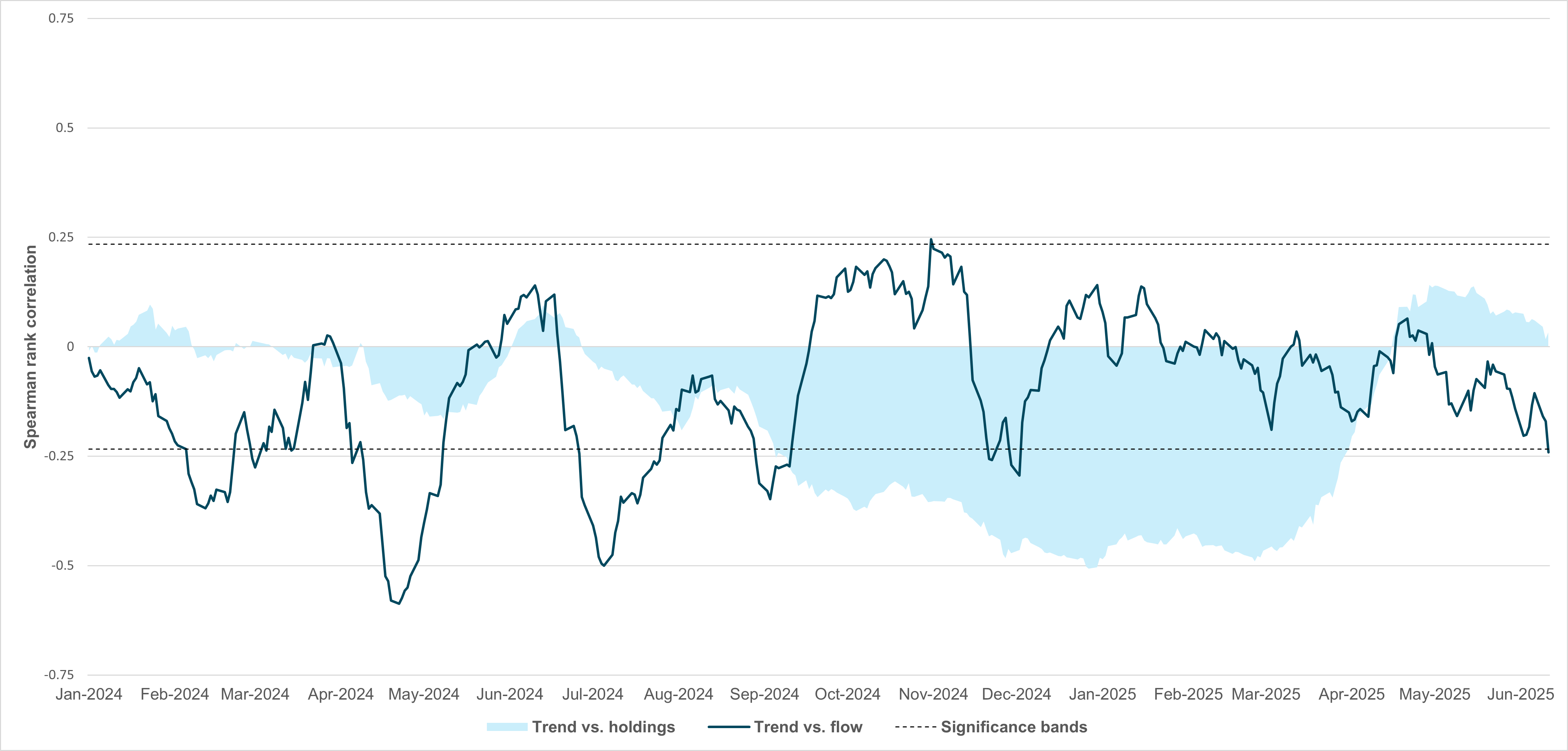

EXHIBIT #1: IFLOW TREND REACHES NEGATIVE STATISTICAL SIGNIFICANCE

Source: BNY

For the first time this year, iFlow Trend has registered statistical significance in either direction. Ongoing surprises like oil moves today help explain why trends are failing. Unsurprisingly, flows are now negatively aligned with currencies’ spot momentum against the dollar. This means that currencies which have seen good recent performance are poorly ranked in flows, and vice-versa. Given that most of the flows we track are cross-border in nature and that flows reflect hedging interest, reconciling the moves in certain currencies points to strong inflows into underlying assets. This moves spot rates, but the need to hedge means significant sales in the opposite direction. This is particularly the case for low-yielders, supported by the rankings anchored by both flow and momentum. We note that it has become increasingly difficult for iFlow Trend to move into positive statistical significance. Even last year, there were prolonged periods of negative significance, with the opposite direction touched only briefly. Positive flow and trend momentum tend to get crowded very quickly, which means the timeframe we track in iFlow Trend is probably not long enough to generate significance. Furthermore, we can see that through much of the latter stages of last year, even holdings’ significance turned negative. Given the dollar’s resilience at the time, we believe it reflected currencies that were softening against the dollar due to asset outflows (or rotation into the U.S.), which led to poor spot momentum. However, hedges were moving in the opposite direction, making flow alignment similarly negative. Such relationships are likely to remain in place if the dollar’s movements and U.S. asset allocation remain the dominant themes, though geopolitically driven risk aversion will likely have a bearing on upcoming shifts.

Risk sentiment is negative with stocks lower, oil higher and the U.S. dollar stronger after the Israeli air attacks on Iran, under the name “Operation Rising Lion.” EMEA markets have partially recovered from their lowest ebbs, while APAC was mixed given the timing of events. The focus now shifts to the U.S. markets and any risks of the conflict escalating over the next few days. The role of oil prices and their effect on global inflation matter. Investors are on high alert as they wait to see if oil prices move even higher, with those costs on top of tariffs seen as a block for manufacturing and global growth. Bond markets are not helping in Europe either, with ECB nearing the end of its cycle but the data continuing to flash weakness. The problem for the trading day ahead comes from the clash between CPI/PPI being tame enough to spark hopes of Fed easing and position unwinding that may be forced. The case for rate cuts in the U.S. is fighting against oil shocks and tariff uncertainty. Trump’s warning of more auto tariffs adds to the risk-off mood today. Trading today will be defensive and will likely make the current trend reversal more difficult into the FOMC, BoJ and BoE meetings next week. The potential for market stability to work with central bankers in controlling financial conditions is in doubt, as the high alert today following Israel’s actions adds to fragmentation worries. Consider the pressure on the Fed and the role of swap lines for the dollar as the USD rallies today, with the ability to fund in dollars and cover supply chain financing all showing up in the squeeze for money. The clearest case in point is perhaps Chinese carmakers and their own liquidity, as the FT reports today. The full extent of events from overnight is going to take weeks to unravel, and time is one thing that money can’t buy.

Israel has launched a sweeping aerial assault on Iran, striking key nuclear facilities including the Natanz enrichment site and military targets, killing senior commanders Major General Hossein Salami and Mohammad Bagheri. Explosions rocked Tehran early Friday, with smoke rising from the Revolutionary Guards’ headquarters. Prime Minister Netanyahu confirmed dozens of strikes targeting Iran’s nuclear and missile programs. Iran reportedly launched 100 drones in response, though it did not confirm retaliation. Oil prices spiked 12.5% before settling 8% higher. The U.S. denied involvement but reiterated warnings against Iranian retaliation. Tensions surged ahead of U.S.-Iran nuclear talks, with Iran threatening retribution and U.S. bases in the region on alert. TA-35 -1.561% to 2694.04, EURILS +1.094% to 3.5956, 10y IGB +7.1bp to 4.57%.

Germany’s inflation rate held steady at 2.1% in May 2025, unchanged from April, as lower energy prices continued to offset food and services inflation. Energy prices fell 4.6% y/y, driven by drops in fuel (-6.8%) and heating oil (-9.5%), though the decrease was smaller than April’s -5.4%. Food prices rose 2.8%, with notable increases for fruit (+7.4%) and confectionery (+6.6%), despite sharp falls in sugar (-27.5%) and olive oil (-17.2%). Core inflation (excluding food and energy) remained elevated at 2.8%, reflecting persistent pressures from services (+3.4%), especially public transport (+11.4%) and health care. On the month, overall prices edged up just 0.1%, with cheaper flights (-16.8%) and vegetables (-6.2%) cushioning small increases elsewhere. DAX -1.382% to 23442.89, EURUSD -0.432% to 1.1534, 10y Bund +0.3bp to 2.481%.

Poland’s consumer prices rose 4.0% y/y in May 2025, with services up 6.0% and goods up 3.3%. On a monthly basis, prices fell 0.2% (services -0.4%; goods -0.1%). Annual inflation was slightly below the 4.1% flash estimate. The strongest upward contributions came from housing (+8.3%), food (+5.4%), restaurants/hotels (+5.9%) and alcohol/tobacco (+6.3%). Transport prices fell 7.2%, subtracting 0.82 percentage points from the overall index. Month-on-month, the largest downward pressures were from transport (-2.4%) and recreation (-1.8%), while food and hospitality posted modest increases. The consumer price index has been above the Monetary Policy Council’s 2.5% ±1 pp target band since July 2024. WIG -1.031% to 99854.91, EURPLN +0.129% to 4.2724, 10y PGB +2.9bp to 5.55%.

The Bank of England’s May 2025 Inflation Attitudes Survey, conducted online by Ipsos, showed a slight easing in inflation expectations. Respondents estimated current inflation at 4.7% (down from 4.9% in February), with 12m and 5y expectations stable at 3.2% and 3.6%, respectively. A majority (67%) believed rising prices would weaken the economy. Satisfaction with the Bank’s inflation control rose, with net satisfaction at +6% (up from +1%). Only 12% supported higher interest rates for the economy, while 37% preferred lower rates. Personally, 30% favored rate cuts. Expectations of rising interest rates dipped to 33%, and fewer respondents reported recent rate increases. Methodological notes caution against comparing online surveys post-May 2020 with earlier face-to-face results. FTSE 100 -0.503% to 8840.23, GBPUSD -0.434% to 1.3554, 10y gilt +2.8bp to 4.505%.

U.S. June flash University of Michigan Consumer Sentiment is projected to rise to 53.6 (May: 52.2), while the 1y inflation expectation is seen easing to 6.4% from 6.6%; 5-10y inflation expectation is projected to be unchanged at 4.1%.

Canada April manufacturing sales are expected to drop for the third straight month, at -2.0% m/m from -1.4% m/m in March, while April wholesale sales ex-petroleum are projected to fall -0.9% m/m after a 0.2% m/m gain in March.

Mood: iFlow Mood remains in risk-on mode, but with a subtle reversal. Equities demand is easing slightly at a multi-year high, but there is a marginal pick-up in sovereign bond buying.

FX: Significant inflows in JPY; outflows in PLN. G10 currencies posted the most inflows, against outflows in APAC, EMEA and neutral in LatAm. Elsewhere, AUD and NOK flows shifted into inflows, CZK flows reversed to outflows, and selling momentum in KRW picked up.

FI: Notable buying in U.S. Treasurys, and Eurozone, Peruvian and Chinese government bonds, against selling in South Korean and South Africa sovereign bonds.

Equities: Selling bias in G10, EMEA and LatAm along with reduced inflows in the EM APAC complex. South African equities posted the most outflow within the iFlow universe.

“Be on the alert to recognize your prime at whatever time of your life it may occur.” – Muriel Spark

“One thorn of experience is worth a whole wilderness of warning.” – James Russell Lowell

The euro area recorded a goods trade surplus of €9.9bn in April 2025, down from €13.6bn a year earlier and sharply lower than March’s €37.3bn. Exports fell 1.4% y/y to €243.0bn, while imports edged up 0.1% to €233.1bn. The chemicals sector’s surplus halved m/m, and the “Machineries & Vehicles” surplus fell €4.0 bn y/y. From January-April, the euro area posted a €71bn surplus (vs. €68.6bn in 2024). The EU’s April surplus also narrowed to €7.4bn (April 2024: €12.8bn; March: €35.5bn). Extra-EU exports dropped 1.9% y/y; imports rose 0.5%. The cumulative EU surplus for January-April was €58.9bn (vs. €63.7bn). Seasonally adjusted April data showed steep m/m declines in both exports and surpluses for the euro area and EU. Euro Stoxx 50 -1.304% to 5290.9, EURUSD -0.432% to 1.1534, BBG AGG Euro Government High Grade EUR -1.6bp to 2.781%.

Germany’s wholesale prices rose by 0.4% y/y in May 2025, slowing from April’s 0.8% and March’s 1.3%. On a monthly basis, prices declined by 0.3%. The annual increase was driven primarily by food, beverage and tobacco prices, which climbed 4.3%, with particularly sharp gains in coffee, tea, cocoa and spices (+38.4%), confectionery and baked goods (+17.1%) and dairy and oils (+8.9%). Prices of non-ferrous ores and metals surged 19.5% y/y. However, falls in wholesale prices for solid fuels and petroleum products (-8.5%), IT equipment (-6.0%) and ferrous metals (-4.8%) partially offset the overall rise. This suggests inflationary pressures remain mixed across categories. DAX -1.382% to 23442.89, EURUSD -0.432% to 1.1534, 10y Bund +0.3bp to 2.481%.

New Zealand May Business PMI back in contraction at 47.5, down from 53.3 in April after four consecutive months of expansion. Four of the five main sub-index values were in decline, with new orders (45.3) contracting most sharply in May. Following healthy expansion from February-April, the employment indicator (45.7) decreased by 8.9 percentage points to reach its lowest level of activity since July 2024. Elsewhere, production came in at 48.7, deliveries at 49.2 and finished stocks at 51.3. The return to contraction also saw the proportion of negative comments from respondents increase to 64.5%, compared with 58% in April and 57.5% in March. Comments indicate that manufacturers are reporting a clear return to decline, driven by falling demand, weak orders and low business confidence. Rising costs, economic uncertainty and reduced consumer spending are compounding pressures, while forward orders and investment remain stalled. NZX 50 -0.761% to 12552.87, NZDUSD -0.907% to 0.6015, 10y NZGB -2.4bp to 4.546%.

As of end-May, China’s broad money supply (M2) rose 7.9% y/y to ¥325.78 trillion, while currency in circulation (M0) grew 12.1%. In the first five months of the year, RMB loans increased by ¥10.68tn, with household loans rising by ¥572.4bn and corporate loans by ¥9.8tn. Foreign-currency loans decreased by 16.3% y/y. RMB deposits rose 8.1% y/y, with ¥14.73tn added over the five-month period, largely driven by household deposits. In the interbank market, daily average turnover rose 14.9% y/y in May, while weighted average interest rates for repo and interbank lending fell to 1.56% and 1.55%, respectively. Cross-border RMB settlement under the current account reached ¥1.31tn in May, mainly from trade in goods (¥0.99tn). Direct investment settlement totaled ¥0.61tn, including ¥0.41tn in foreign direct investment. Overall, the data reflect steady credit expansion, falling interbank rates and continued growth in cross-border RMB use. CSI 300 -0.72% to 3864.18, USDCNY +0.116% to 7.181, 10y CGB -0.3bp to 1.7%.

Japan’s industrial output fell 1.1% m/m in April 2025, with shipments down 0.8% and inventories declining 0.9%, reflecting broad downward revisions across categories. Despite this, the manufacturing capacity utilization index rose 1.3% to 102.9, up 2.4% y/y, supported by strong performance in electronic machinery (+6.0%) and devices (+5.8%). The production capacity index fell 0.4% to 95.9, a 2.1% annual drop, highlighting ongoing structural constraints. Sector-wise, electronics (-3.7%), steel (-1.9%) and chemicals (-0.4%) weakened, while general-purpose and industrial machinery posted marginal gains. The mixed data point to cautious production strategies amid uncertainty, even as utilization levels continue to recover. Nikkei -0.888% to 37834.25, USDJPY +0.321% to 143.94, 10y JGB -4.1bp to 1.411%.

Japan’s tertiary industry activity index rose 0.3% m/m in April 2025 to 104.1, marking the first increase in two months. This was driven by gains for finance and insurance (+3.3%) and information and communications (+2.1%), particularly internet-related services. However, transport and postal services (-3.4%) and real estate (-0.9%) declined. Services for individuals rose 0.3% to 105.6, while business-oriented services increased 0.5% to 102.9. Notably, non-manufacturing-oriented business services rose 1.5%, offsetting a 1.9% drop for manufacturing-linked services. Within personal services, non-discretionary components rose 0.2%, but discretionary services fell 0.5%. The Ministry of Economy, Trade and Industry classified the overall trend as “stalling,” reflecting ongoing uncertainty despite modest improvement.