Market Movers: Growth Politics

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 9 minutes

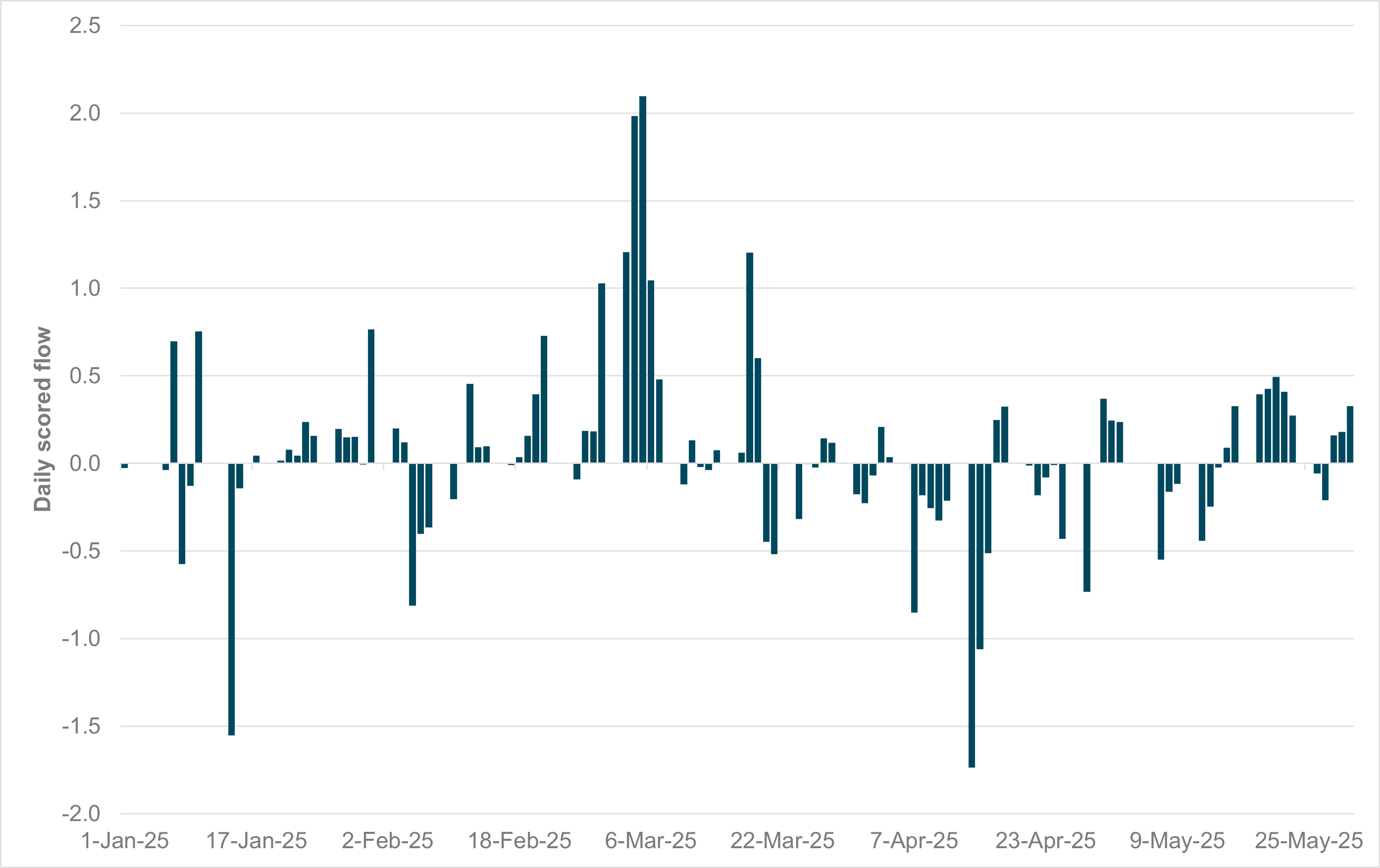

EXHIBIT #1: CROSS-BORDER FLOWS INTO JGBS, YEAR-TO-DATE

Source: BNY

Japan’s draft annual fiscal policy plan released overnight called for increased domestic ownership of government bonds to curb rising long-term yields and restore market confidence. While specifics are lacking, the plan stresses stable bond issuance and fiscal consolidation. The government has delayed its primary budget surplus target to fiscal 2025 or 2026, reflecting pressure from growing debt and market volatility. The Bank of Japan’s ongoing reduction of bond purchases, now down by ¥400bn per quarter, has weakened demand, with recent bond sales showing poor investor interest. The BoJ, which still holds over half of Japan’s government debt, will announce its post-April 2026 plans at its June policy meeting. Given the historically high levels of Japanese ownership of JGBs (86.5% as of 2023 according to the Japanese Ministry of Finance’s 2024 Debt Management Report), the role of foreign investors has generally been limited, though we acknowledge there could be a stronger impact on FX markets based on hedging flows. However, given the rise in long-dated Japanese bond yields and JPY’s historically cheap valuations, the clear attraction and demand are amplifying with a shift away from dollar-denominated assets toward economies with higher levels of savings. Our flow data show that there have been periods of good interest in JGBs year-to-date, including during the recent round of curve steepening, and these investors will be long-term in nature, able to help anchor stability in the market.

Risk sentiment has reversed on weaker economic growth surveys and politics. The collapse of the Dutch government coalition, along with South Korea’s election today and yesterday’s surprise result from Poland, plus the weaker PMI from China and Australia’s ongoing current account deficit, have all led the OECD to downgrade its forecast. Inflation data have also been important today, with a lower-than-expected Eurozone flash CPI and falls in Swiss and Turkish inflation. Bonds are bid on expectations of weaker equities and lower growth, with hopes of more easing from central bankers. Whether this extends into U.S. open trading rests on the U.S. Jolts report; job openings have for months suggested stable rather than robust demand for labor. Many will also be waiting for the factory orders release, as hard data weakness triggers more expectations of Fed action. The lower bond yields in Japan and Europe played a part in the moves pre-market, but the extent to which capital goods orders are confirmed by the economic data will reset growth views for U.S. Q2 GDP. Many are expecting more action from G7 leaders on debt in two weeks, as the U.S. Senate continues to debate and likely change the “big, beautiful tax bill.” U.K. gilts today rallied after a 30y sale, with Chancellor Reeves starting a multi-year spending review next week. The IMF and others are pushing for lower public spending. Politics and government spending are a source of worry for part of the day, while the data will confirm the cost. There appears to be less room for the optimists. What is different on the day is that this leaves the U.S. dollar holding above the three-year lows touched yesterday following weaker ISM data. Whether this continues or not matters, as the Fed and others look to thread the needle on inflation and growth.

Overnight, BoJ Governor Kazuo Ueda discussed the economic outlook amid heightened global trade tensions, particularly U.S. tariff hikes. He identified four key transmission channels affecting Japan: weakened export competitiveness, dampened business and consumer sentiment, a global demand slowdown and financial market volatility. Despite these headwinds, Ueda expects Japan’s economy to remain resilient, supported by strong corporate earnings and tight labor conditions. He highlighted wage growth as a crucial factor in sustaining the inflation path toward the 2% target, noting that labor shortages – especially in non-manufacturing sectors – are driving firms to raise wages. However, he cautioned that weaker corporate profits caused by trade shocks could suppress wage-setting behavior. Inflation is projected to stay near 2%, supported by this wage-price dynamic. Ueda reiterated a cautious policy stance, with further rate hikes contingent on confidence in stable inflation. He also confirmed a mid-year review of the BoJ’s bond tapering plan, balancing predictability against flexibility. Nikkei -0.064% to 37446.81, USDJPY +0.007% to 142.72, 10y JGB -1.9bp to 1.494%.

The Bank of Japan will likely decide to stop reducing its government bond purchases in a plan for the next fiscal year. Since last summer, the BoJ has cut purchases by ¥400bn each quarter, but concerns over rising yields may prompt a pause when the board meets on June 17. Sakurai cited the risks of long-term commitments in an uncertain economic climate; he expects policy rates to remain at 0.5% until year-end. Market participants are divided on the pace of tapering, and elevated yields have already pushed up debt servicing costs to a quarter of Japan’s budget.

China Caixin PMI manufacturing unexpectedly fell into the contraction zone at 48.3, the weakest level since September 2022. Manufacturing output and new orders declined, with export orders dropping at the fastest pace since July 2023. Employment shrank, purchasing activity was reduced and inventories rose slightly due to weak demand and shipment delays. Input and output prices fell, reflecting lower energy and material costs and intensified competition. Despite this downturn, business sentiment improved, supported by hopes of better trade conditions and a rebound in export markets. CSI 300 +0.307% to 3852.01, USDCNY -0.123% to 7.1901, 10y CGB -0.2bp to 1.704%.

The Dutch government has collapsed after the Freedom Party – which won the 2023 legislative elections – withdrew its support due to the coalition’s inability to agree on proposals to curb migration. This will likely trigger a new legislative election, and on current polling the Freedom Party will continue to perform strongly. Even so, any new government, even one led by Wilders, will likely prove unwieldy and take many months to formalize given the nature of the Netherlands’ political system, where multi-party coalitions are the norm. We see no impact on Dutch sovereign debt, which continues to benefit from strong demand for AAA-rated paper. AEX -0.417% to 914.53, EURUSD -0.289% to 1.1408, 10y NGB -2.1bp to 2.716%.

Eurozone May flash CPI slows to 0% m/m, 1.9% y/y – below the expected 2% y/y and down from 2.2% in April. The core CPI fell to 2.3% y/y from 2.7% y/y. The cost of food rose to 3.3% y/y from 3.0%, while services fell back to 3.2% y/y from 4.0% and goods were stable at 0.6%. Energy fell 3.6%, as in April. As expected, unemployment fell to 6.2%, matching December’s record low. Youth unemployment fell to 14.4% from 14.8%, to reach a four-month low. The data is seen as adding to rate cut expectations for this week, with service inflation a key focus. Euro Stoxx 50 -0.39%, EURUSD -0.289% to 1.1408, 10y EU -3.1bp to 2.896%.

Switzerland’s consumer price index (CPI) rose by 0.1% month-on-month in May, reaching 107.6 points (Dec 2020 = 100), while annual inflation turned negative at -0.1%. Key drivers behind the monthly increase included higher housing rents, overseas package travel and some fruit and vegetable prices, though these were offset by declines in airfares, heating oil and hotel-related services. Core inflation rose 0.1% m/m, coming in at +0.5% y/y. Domestic goods prices increased by 0.2%, while import prices remained flat but were down 2.4% y/y. The harmonized index of consumer prices (HICP) fell by 0.2% versus both the prior month and year. The figures support the case for further SNB easing, and negative rates cannot be ruled out. SMI +0.113% to 12211.96, EURCHF -0.133% to 0.93356, 10y Swiss GB -2.2bp to 0.252%.

South Africa Q1 GDP up 0.1% q/q, 0.8% y/y – better than the expected -0.1% q/q, 0.7% y/y. Growth did, however, slow from 0.4% q/q in Q4 (revised down from 0.6%). Growth in Q1 was led by transport and farming, while manufacturing contracted. The news will help support the new government coalition, after the Treasury cut its GDP projection from 1.9% to 1.4% y/y in response to U.S. trade policy. FTSE/JSE -0.4%, USDZAR +0.05% to 17.8495, 10y SAGB -5.6bp to 10.121%.

U.S. April factory orders expected to drop -3.2% m/m after 3.4% m/m in March, ex-transport consensus at 0.2% m/m vs. -0.4% previously. This is key for U.S. growth/hard data.

U.S. April final durable goods orders forecast unchanged from flash at -6.3% m/m.

U.S. April JOLTS job openings expected to come in lower, at 7,100k (March: 7,192k), with quits and the layoff rate also in focus in Friday’s unemployment report.

Fed Speakers: Chicago Fed Austan Goolsbee participates in Q&A at the Corridor Business Journal Mid-Year Economic Review; Fed Governor Lisa Cook discusses the economic outlook and monetary policy at an event hosted by the Council on Foreign Relations; Dallas Fed President Lorie Logan gives opening remarks at Fed Listens event.

Mood: iFlow Mood continues to be in risk-on mode. Equities demand remains elevated, as sovereign bill demand stabilizes.

FX: G10 currencies were sold, against buying in the rest of the region, above all in APAC. KRW, CNY and PEN posted the most inflows.

FI: U.S. Treasurys and U.K. gilts were bought, against continued cross-border selling in Eurozone government bonds. There were mixed and light flows in EMEA and LatAm, and better buying in APAC sovereign bonds.

Equities: Mixed flows with good-sized buying in EM EMEA, against selling in Americas. Flows in APAC were muted. U.S. and Colombian equities were most sold, against significant buying in Polish equities.

“Globalization presumes sustained economic growth. Otherwise, the process loses its economic benefits and political support.” – Paul Samuelson

“Preventing conflicts is the work of politics; establishing peace is the work of education.” – Dr. Maria Montessori

Turkey’s May consumer price index (CPI) rose by 1.53% m/m and 35.41% y/y. Housing costs surged 67.43% annually, food and non-alcoholic beverages rose 32.87%, and transport increased 24.59%, contributing a combined 21.66 percentage points to annual inflation. Monthly, housing rose 2.99% and transport 2.66%, while food prices fell 0.71%. Of 143 expenditure headings, 111 increased, 28 decreased and four were unchanged. The core CPI (excluding food, energy, alcohol, tobacco, and gold) rose 2.25% m/m and 34.81% y/y. Inflation on a 12-month moving average reached 45.80%, highlighting persistent price pressures across major categories.

New Zealand Q1 terms of trade eased to 1.9% q/q vs 3.2% in Q4 2024 as import prices rise 5.1% vs 7.1% q/q for export prices. Export price gains were led by dairy prices, which were up 10% q/q. The higher import and export prices were also driven by NZD weakness, with the NZD trade-weighted index falling 5.3% q/q in Q1 2025.

RBNZ announces changes to liquidity facilities, effective June 17, 2025. Key changes include: 1) The Standing Repo Facility (SRF) will be discontinued. 2) Weekly Reserve Bank bill auctions will be discontinued. 3) Pricing on the Bond Lending Facility (BLF) will revert to OCR -50bp (from OCR -25bp). There is no change to the availability of the BLF. This pricing change affirms the role of the BLF as a backstop facility to support liquidity in the secondary market for New Zealand government bonds. 4) Pricing on the Overnight Reverse Repurchase Facility (ORRF) will revert to OCR +50bp (from OCR +25bp). There is no change to the availability of the ORRF. This pricing change affirms the role of the ORRF as a backstop facility for sourcing cash liquidity in return for eligible collateral.

Australia Q1 BoP current account balance came in worse than expected at a deficit of AUD -14.7bn, from a downwardly revised AUD -16.3bn in Q4 2024. Imports of goods and services were up 2.2% q/q, while exports of goods and services climbed 1.9% q/q, led by exports of non-monetary gold. The $4.8bn rise in non-monetary gold exports was the highest on record. It was led by $11bn of non-monetary gold exports to the U.S., which was larger than the total combined value of non-monetary gold exports to the U.S. over the past four years. The capital and financial account surplus was $6,234mn, a decrease of $12,984mn on the Q4 2024 surplus. The net international investment liability position was $672,578mn in Q1 2025. Elsewhere, Australia’s national minimum wage will be increased by 3.5%, effective from July 1.

Based on the minutes of the May meeting, the RBA Board debated whether to cut rates amid global uncertainty. Some members favored holding the rate unchanged, citing tight labor markets, expected rises in headline inflation and limited domestic impact from global trade tensions. Others supported a cut, pointing to easing underlying inflation, weak consumption and increased downside risks from tariffs and policy unpredictability. A 50bp cut was discussed but rejected due to uncertainty and the absence of severe domestic effects. Ultimately, members agreed on a cautious 25bp reduction to 3.85%, balancing inflation progress with global risks while maintaining flexibility for future action.

Malaysia May PMI improved slightly from 48.6 to 48.8 with moderation in both production and new orders, although at slower rates. Weak domestic and external demand, uncertainty over U.S. trade policy and rising input costs – driven by tariffs and currency depreciation – contributed to muted activity. Input cost inflation hit a six-month high, ending a four-month streak of falling output prices. Employment stabilized after seven months of decline, but business sentiment weakened to its lowest level since June 2021 amid concerns about global trade and labor shortages.