Market Movers: Growing Pains

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 15 minutes

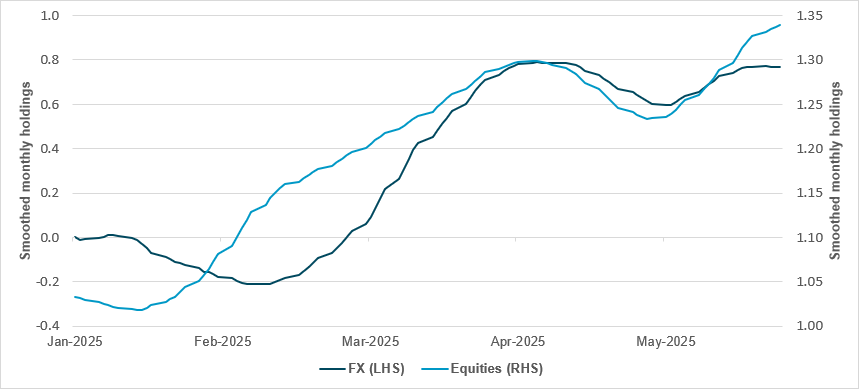

EXHIBIT #1: PLN AND POLISH EQUITY HOLDINGS

Source: BNY

The result of the final round of the Polish presidential election presents challenges for both local and regional assets. Pre-election polls pointed to a very close race, and much like the final round of the Romanian presidential election, the vote was viewed as highly binary, prompting significant hedging activity beforehand. For instance, RON experienced heavy outflows after Romania’s first-round vote, followed by strong recovery flows in response to the second round, though selling pressure returned near month-end. Similarly, the results of the first round of the Polish presidential elections marked a turning point in flow dynamics, with strong buying between mid-April and early May giving way to notable outflows, though less extreme than for RON. A key difference is that PLN has maintained more consistent interest over the past three months, with only volatility around “Liberation Day” prompting significant hedging. The market will now take time to assess the outcome’s implications, and PLN flows could be volatile in the short term. Over the medium term, however, overall momentum remains flat, and CEE asset performance will likely hinge more on monetary policy. This week’s NBP decision will be pivotal in setting the tone for the remainder of the year. We do not expect the current policy backdrop to support a renewed easing cycle in Poland, which should help anchor favorable positioning in the region.

Risk sentiment is off amid trade worries and weaker global PMI manufacturing reports. Copper futures are higher, breaking the traditional signal for their correlation to equities and reflecting Trump’s new 50% tariffs on steel and aluminum from Friday to support the Nippon Steel deal. Oil prices jumped 3% as OPEC kept its output increase steady rather than ramping it up further. The higher commodity prices are less about demand and more about supply expectations, with OPEC and Trump tariffs driving inflation. This is the key to the day ahead, as, speaking over the weekend, Fed Governor Waller it made clear 10% tariffs would allow the Fed to cut rates later this year. Attention will be on whether Fed Chair Powell repeats this message in his speech today. The underlying demand for new goods and the noise around front-loading them onto tariffs remains a data-watching story that investors and officials will continue to use for risk monitoring. The day ahead for the U.S. will revolve around that mix of growth and inflation fears from the PMI and ISM reports. Overnight was no different, as the PMI reports show a world in modest contraction with weaker exports. The USD is lower, but so are bonds, and that pain should be watched along with equities and the data.

Karol Nawrocki, a nationalist historian backed by the Law and Justice (PiS) party, narrowly won Poland’s 2025 presidential election with 50.89% of the vote, defeating liberal Warsaw Mayor Rafał Trzaskowski, who secured 49.11%. Nawrocki, a political newcomer known for his conservative views and leadership of the Institute of National Remembrance, campaigned on a “Poland first” platform. His victory is expected to challenge Prime Minister Donald Tusk’s pro-European Union agenda, as the president holds veto power over legislation. The election saw a record turnout of 71.31%, reflecting deep national divisions. Given the current extent of positive positioning in Polish assets, we expect a high risk of hedging flows in the near-term. WIG -0.909% to 100554.1, EURPLN +0.116% to 4.2559, 10y PGB +12.9bp to 5.486%.

Eurozone manufacturing showed further signs of recovery in May 2025, with output rising for the third consecutive month and the PMI increasing to 49.4, a 33-month high. Production growth was broad-based across major economies, and confidence among manufacturers reached its highest level since February 2022. While new orders and exports remained just below stabilization, declines in employment, purchasing and inventories slowed. Input costs fell at the fastest pace in 14 months, leading to renewed price discounting. Greece and Spain led the PMI rankings, while Germany remained the weakest. The outlook was buoyed by lower energy prices, easing financial conditions and expectations of ECB rate cuts. iFlow is showing general resilience in EUR flow/holdings, and we would be reluctant to chase the currency higher even with a “hawkish cut” this week. Euro Stoxx 50 -0.365% to 5346.98, EURUSD +0.67% to 1.1423, BBG AGG Euro Government High Grade EUR +1.5bp to 2.859%.

Germany’s manufacturing PMI edged down slightly to 48.3 in May 2025, from 48.4. While this is still below the 50.0 threshold, output rose for the third consecutive month, supported by stronger export orders, particularly to Europe and the U.S. Domestic demand remained weak, and total new orders dipped. Employment continued to fall, though at a slower pace, and purchasing activity neared stabilization. Input costs dropped sharply, allowing firms to cut output prices amid intense competition. Business sentiment improved to its highest level since February 2022, reflecting optimism around lower energy prices, expected ECB rate cuts and government stimulus plans. DAX -0.291% to 23927.59, EURUSD +0.67% to 1.1423, 10y Bund +5.8bp to 2.558%.

France’s manufacturing sector showed further signs of recovery in May 2025, with output rising for a second consecutive month and the PMI climbing to 49.8 from 48.7 in April, just below the 50.0 no-change threshold. Demand remained subdued, but new orders fell only slightly, nearing stabilization. Firms responded by increasing their discounting, leading to the sharpest price cuts since November. Employment rose for the first time in two years, and business confidence hit a 39-month high, driven by expectations of stronger sales and new product launches. Input price inflation eased, helping to support margins, while backlogs increased modestly for the first time since early 2023. CAC40 -0.387% to 7721.89, EURUSD +0.67% to 1.1423, 10y OAT +6.5bp to 3.225%.

Italy’s manufacturing PMI held steady at 49.2 in May 2025, just below the 50.0 no-change mark, signaling continued mild contraction. Output rose slightly, ending a 13-month decline, supported by a marginal rebound in exports. This marked the first export growth in over two years. However, new orders declined for the 14th consecutive month, with weakness in autos and electronics. Input costs fell at the fastest rate in over a year due to lower raw material prices, while selling prices were unchanged. Employment and purchasing activity continued to decline, albeit modestly. Business sentiment improved, reaching a three-month high on hopes of better demand, lower interest rates and easing inflation. FTSEMIB +0.149% to 40147.33, EURUSD +0.67% to 1.1423, 10y BTP +6.9bp to 3.549%.

U.K. manufacturing remained under pressure in May 2025, with the PMI rising slightly to 46.4 from 45.4. This is still firmly below the 50.0 threshold, indicating ongoing contraction. Output and new orders declined for the seventh and eighth consecutive months, respectively, driven by weak domestic and export demand, cost pressures and low customer confidence. Employment and purchasing were reduced, especially among small manufacturers. However, there were some incipient signs of the downturn easing, as falls in output and new orders slowed. Input cost inflation eased to a five-month low, though concerns over tariffs, labor costs and supply chain delays persisted. Business confidence rose modestly but remained historically subdued. We remain cautious on GBP valuations at current levels, but the BoE is unlikely to turn more dovish due to stubborn inflation. FTSE 100 +0.125% to 8783.38, GBPUSD +0.639% to 1.3545, 10y gilt +5.2bp to 4.699%.

China May PMI improved to 49.5, up 0.5 points, signaling improved conditions but still below the 50-point threshold. Large enterprises showed expansion (50.7), while medium (47.5) and small firms (49.3) remained in contraction. Production and new orders rose, but employment and inventories stayed weak. The non-manufacturing business activity index stood at 50.3, slightly lower than in April, with services holding steady and construction softening. New orders and prices improved slightly, while employment remained stable. The composite PMI output index rose to 50.4, indicating continued expansion in overall business activity across sectors. Confidence among non-manufacturing firms remained optimistic. We continue to see firm fixed income flows into Chinese government bonds, complemented by general FX interest. CSI 300 -0.479% to 3840.23, USDCNY +0.181% to 7.1989, 10y CGB -1.2bp to 1.706%.

South Korea May exports declined by -1.3% y/y (April: 3.7%), while imports fell more than expected to -5.3% y/y (April -2.7%), resulting a trade surplus of $6,938mn (April: $4,881mn). Exports to the U.S. and China dropped more than -8% y/y. Semiconductor exports rose to 21.2% y/y to $13.8bn, while auto shipments were down -4.4% to $6.2bn. iFlow is showing strong recovery flows into KRW, as markets look ahead to the presidential elections. KOSPI +0.048% to 2698.97, USDKRW -0.594% to 1374.4, 10y KTB +1.2bp to 2.772%.

U.S. May ISM is forecast to improve slightly to 49.5 (April: 48.7) with ISM Prices Paid expected to ease to 68.7 (April: 69.8).

U.S. April construction spending is forecast to rise by 0.2% m/m (March: -0.5% m/m).

Fedspeakers: Fed Powell gives opening remarks at the Board of Governors International Finance (IF) 75th Anniversary Conference. Fed Logan and Fed Goolsbee in moderated Q&A.

Mood: iFlow Mood remains in risk-on mood with a further pick-up in equity demand and moderate sovereign bond demand.

FX: Significant inflows in CNY, KRW and PEN and moderate flows in the rest of the iFlow universe. USD posted moderate outflows, against light inflows in EUR, GBP and JPY.

FI: Notable buying in U.S. Treasurys, U.K. gilts, and Singapore and Chinese government bonds vs. Australia and Eurozone government bond selling. LatAm and EMEA sovereign bonds were lightly sold.

Equities: Good demand in APAC, EMEA and LatAm against light selling in developed markets, especially Japan.

“Take chances, make mistakes. That’s how you grow. Pain nourishes your courage. You have to fail in order to practice being brave.” – Mary Tyler Moore

“Pain is part of progress. Anything that grows experiences some pain. If we avoid all pain, we are avoiding all growth.” – Craig Groeschel

Norway’s DNB manufacturing PMI rose to 51.2 in May 2025, recovering from April’s sharp drop and slightly exceeding Q1’s average. The rebound was largely driven by a seven-point increase in the production index to 53.4 and a marked recovery in new orders, which rose to 48.2 (from 38.5). However, the employment index edged down to 52.3. Supplier delivery times shortened slightly, while inventory levels of purchased goods fell to 49.2, suggesting stronger demand. Input price inflation accelerated, with the index climbing to 60.5. Overall, the data reflect a moderate improvement in industrial activity, although caution is advised due to the small sample size. OSE +0.115% to 1563.4, EURNOK -0.323% to 11.5495, 10y NGB +6.6bp to 4.071%.

Spain’s manufacturing sector returned to growth in May 2025, with the PMI rising to 50.5 from 48.1, the first expansion since January. Output rebounded and employment increased modestly, supported by improved sentiment and easing global tariff uncertainty. New orders continued to fall, but at a much slower rate, while export demand showed a tentative recovery. Input prices dropped for the first time since early 2024, driven by lower plastics and petroleum costs, prompting firms to cut output prices amid competition. Inventories of pre-production goods rose despite reduced purchasing. Business confidence reached a three-month high as firms anticipated a more stable economic outlook. IBEX 35 +0.164% to 14175, EURUSD +0.67% to 1.1423, 10y Bono +6.1bp to 3.153%.

Sweden’s manufacturing PMI fell slightly to 53.6 in May 2025 from 54.2 in April, remaining in growth territory for the tenth consecutive month. The decline was mainly due to a drop in new orders, which hit a five-month low and pulled down the headline index by 1.2 points. Production, employment and delivery times contributed positively. Input price pressures eased, with the subindex for supplier prices falling below 50 for the first time since October 2024. This reflected lower global commodity prices and a stronger krona. Analysts note that trade tensions and the uncertain future of U.S. tariffs could pose risks to the ongoing industrial recovery. OMX -0.174% to 2491.686, EURSEK -0.262% to 10.8569, 10y Swedish GB +1.6bp to 2.346%.

In May 2025, Swiss manufacturing sentiment fell sharply, with the PMI plunging to 42.1 from 45.8.This is well below the 50-point growth threshold, reflecting mounting concerns over U.S. trade policy. Key components such as production and order books dropped significantly, reaching their lowest levels since 2024 and 2023, respectively. Employment hit a five-year low, and purchasing volumes also decreased further. In contrast, the services sector improved, with the PMI rising to 56.3 – its highest since early 2025 – supported by stronger business activity and order books. However, service sector employment dipped below 50, and firms voiced concerns over narrowing price margins caused by easing input cost pressures. SMI -0.143% to 12209.55, EURCHF +0.141% to 0.93456, 10y Swiss GB +2.7bp to 0.296%.

Switzerland’s GDP grew by 0.8% in Q1 2025, up from 0.6% in Q4 2024, supported by broad-based services growth and strong domestic demand. The chemical and pharmaceutical sector surged by 7.5%, driving manufacturing up 2.1% and boosting goods exports by 5.0%, particularly to the U.S. In contrast, the energy sector fell by 9.4% due to low hydroelectric output. Services exports rose 1.4%, with solid growth in trade (+2.1%), health (+1.1%) and finance (+0.5%). Private consumption rose 0.2%, led by health and housing. Construction expanded by 1.1%, and government spending increased by 0.4%. Imports jumped 6.1%, reflecting stronger domestic activity.

In April 2025, Switzerland’s nominal retail sales rose by 0.3% year-on-year, while real sales (adjusted for inflation and calendar effects) increased by 1.3%. In contrast, service sector revenues declined slightly by 0.1% y/y in March 2025 after adjusting for working day effects.

U.K. house prices rose 0.5% month-on-month in May 2025, lifting the annual growth rate slightly to 3.5%, from 3.4% in April. The average house price reached £273,427. Rural properties continue to outperform urban ones, with a 23% rise over five years compared with 18% in cities. Market activity remains resilient, supported by strong labor markets, low unemployment and stable borrowing conditions. First-time buyer demand remains high, and older age groups are increasingly moving to rural areas, while younger buyers tend to shift toward cities. Input from the latest housing survey suggests optimism, though demand continues to be influenced by cost and demographic trends. FTSE 100 +0.125% to 8783.38, GBPUSD +0.639% to 1.3545, 10y gilt +5.2bp to 4.699%.

In April 2025, U.K. net mortgage borrowing turned negative at -£0.8bn, down sharply from £13.0bn in March. Mortgage approvals declined for a fourth month, while remortgaging rose. Consumer credit borrowing increased to £1.6bn, led by higher credit card use. Household deposits grew £3.0bn, with record ISA contributions. Businesses borrowed £1.2bn net, mostly from large firms, though SMEs saw flat activity. PNFCs repaid £2.4bn in finance. Business deposits fell £7.0bn. The effective rate on new loans to businesses rose, while input rates on household deposits increased slightly. Overall money supply (M4ex) and lending (M4Lex) both declined m/m.

Czechia’s manufacturing sector weakened in May 2025, with the PMI falling to 48.0 from 48.9 in April, indicating the steepest decline in three months. Output and new orders both fell, driven by economic uncertainty and weak demand, especially in the automotive sector. Export orders declined for a 39th straight month. Firms cut employment and purchasing activity, despite rising backlogs and modest growth in post-production inventories due to shipment delays. Input price inflation accelerated amid material shortages, prompting firms to raise selling prices, though increases were modest. Business confidence improved, reaching its highest level since February 2022, as firms anticipated stronger demand and product development ahead. Prague SE -0.007% to 2148.47, EURCZK -0.073% to 24.913, 10y CZGB +2.2bp to 4.181%.

Poland’s GDP grew by 3.2% y/y and 0.7% q/q in Q1 2025, supported mainly by strong domestic demand. Household consumption rose 2.5% y/y, and gross fixed capital formation increased 6.3%. The largest positive contributions came from consumption and investment, while net exports subtracted 1.1 percentage points from growth. Gross value added rose 2.2% y/y, led by transportation (+4.1%) and public services (+3.8%), though industry and financial services declined. On a quarterly basis, construction output rose 1.7%, but industry fell 1.7%. Input inventories declined, while investment and consumer spending showed resilience, reflecting a broad-based domestic recovery. WIG -0.909% to 100554.1, EURPLN +0.116% to 4.2559, 10y PGB +12.9bp to 5.486%.

Poland’s manufacturing sector saw a marked deterioration in May 2025, with the PMI falling to 47.1 from 50.2 – the sharpest monthly drop since June 2022. New orders declined at the fastest rate in six months, particularly in the automotive, energy and construction sectors. Output fell for the first time in four months, prompting cuts to employment and input purchases. Input inventories decreased at their steepest pace since January. Despite easing inflationary pressures, manufacturers lowered output prices for the first time in four months. Business confidence weakened further, with the outlook for future output hitting a 2025 low amid ongoing demand uncertainty.

Turkey’s manufacturing sector continued to contract in May 2025, with sector PMI falling to 47.2 from 47.3. This marked the 14th consecutive month below the 50 threshold. Muted demand led to further declines in output, new orders, employment and purchasing activity. Output fell at the sharpest pace since October 2024, and new orders decreased for the 23rd straight month. Input cost inflation remained elevated, mainly due to currency weakness, though the rate eased from April’s peak. Output price inflation also softened, reflecting firms’ limited pricing power. While inflationary pressure eased slightly, sentiment remained cautious amid ongoing demand weakness. BI 100 -0.354% to 8987.68, USDTRY -0.019% to 39.1909, 10y TGB +18bp to 33.7%.

South Korea May PMI was up from 47.5 to 47.7. Both output and new orders contracted more sharply, with the latter falling at the fastest rate since June 2020. At the same time, firms noted a reduction in exports, purchases and outstanding business, as reports of challenging domestic economic conditions and evolving global trade policies weighed on demand. Positively, firms took on additional staff for the first time in seven months, as manufacturers cited optimism regarding the year ahead. KOSPI +0.048% to 2698.97, USDKRW -0.594% to 1374.4, 10y KTB +1.2bp to 2.772%.

Japan May final PMI came in at 49.4, better than the 49.0 flash. The downturn in new orders eased significantly on the month, while production levels were down only modestly. Nevertheless, firms continued to trim their purchasing activity and reduced their inventories of both pre- and post-production items. Inflationary pressures meanwhile eased, with rates of input cost and output charge inflation slowing to 14-month and 47-month lows, respectively. Nikkei -1.302% to 37470.67, USDJPY -0.806% to 142.86, 10y JGB +1.2bp to 1.513%.

Indonesia May PMI improved slightly from 46.7 to 47.4. Output and new orders continued to fall, with the latter seeing an accelerated reduction from April. Positively, manufacturers signaled a renewed uplift in employment levels amid confidence that growth will resume over the coming months. Anecdotal evidence also suggested that some companies offered discounts as part of attempts to drive sales, as indicated by only a fractional rise in charged prices. This was despite a steeper rise in input costs. JCI -1.779% to 7048.138, USDIDR -0.258% to 16248, 10y IDGB +2.8bp to 6.866%.

Indonesia May headline CPI eased to 1.60% y/y from 1.95% and core CPI from 2.5% to 2.4% y/y. Elsewhere, Indonesia April exports improved slightly to 5.76% y/y from 3.15%, but imports surged 21.84% y/y, leaving a smaller-than-expected trade balance of $150mn vs. $4,327mn in March.

In May 2025, the Philippines manufacturing PMI dropped to 50.1 from 53.0, signaling a broad stagnation in the sector. Output contracted, new order growth slowed, and export demand declined at the fastest pace since November 2024. Employment fell for the first time in four months, marking the strongest job shedding in nearly a year. Inventory levels shrank, and input buying eased. Despite modest inflation pressures, sentiment remained weak due to global trade tensions, with business confidence at its third-lowest level on record. PSEi +0.176% to 6352.66, USDPHP -0.121% to 55.705, 10y PHGB -0.9bp to 6.258%.

India May final PMI eased to 57.6 (flash 58.3). May data indicated another robust improvement in business conditions across India’s manufacturing industry. Although rates of increase in new orders and output retreated to three-month lows, they remained well above their respective long-run averages. Cost inflation climbed to a six-month high, and selling prices were raised to one of the greatest extents seen in more than a decade. SENSEX -0.179% to 81305.4, USDINR -0.3% to 85.325, 10y INGB -0.2bp to 6.286%.

Taiwan May PMI improved to 47.8 to 48.6. Output, new orders and new export sales all declined for the second straight month. Panel members indicated that weaker demand conditions and increased client hesitancy to commit to new work amid U.S. tariffs had dampened sales. As a result, manufacturers cut their purchasing activity and employment levels again in May. At the same time, efforts to help drive sales led firms to cut their selling prices again, which was supported by a fresh decline in input costs. Meanwhile, Taiwan’s Central Bank (CBC) warned exporters against currency speculation. It urged local trading companies to only buy or sell U.S. dollars based on actual needs and not to follow speculative market predictions. TAIEX -1.614% to 21002.71, USDTWD +0.188% to 29.973, 10y TGB -1.1bp to 1.555%.