Market Movers: Green

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

• U.S. President Trump warns exemptions on smartphones, semiconductors will be temporary, while Commerce Secretary Lutnick sees separate electronic levies coming soon.

• China President Xi arrives in Hanoi, notes China and Vietnam “should strengthen cooperation in production and supply chains,” and warns there are “no winners from trade war.”

• Negotiators from the U.S. and Iran held “constructive” nuclear talks and are set for more meetings, while France, U.K., and Germany are vigilant that any deal must meet their security concerns.

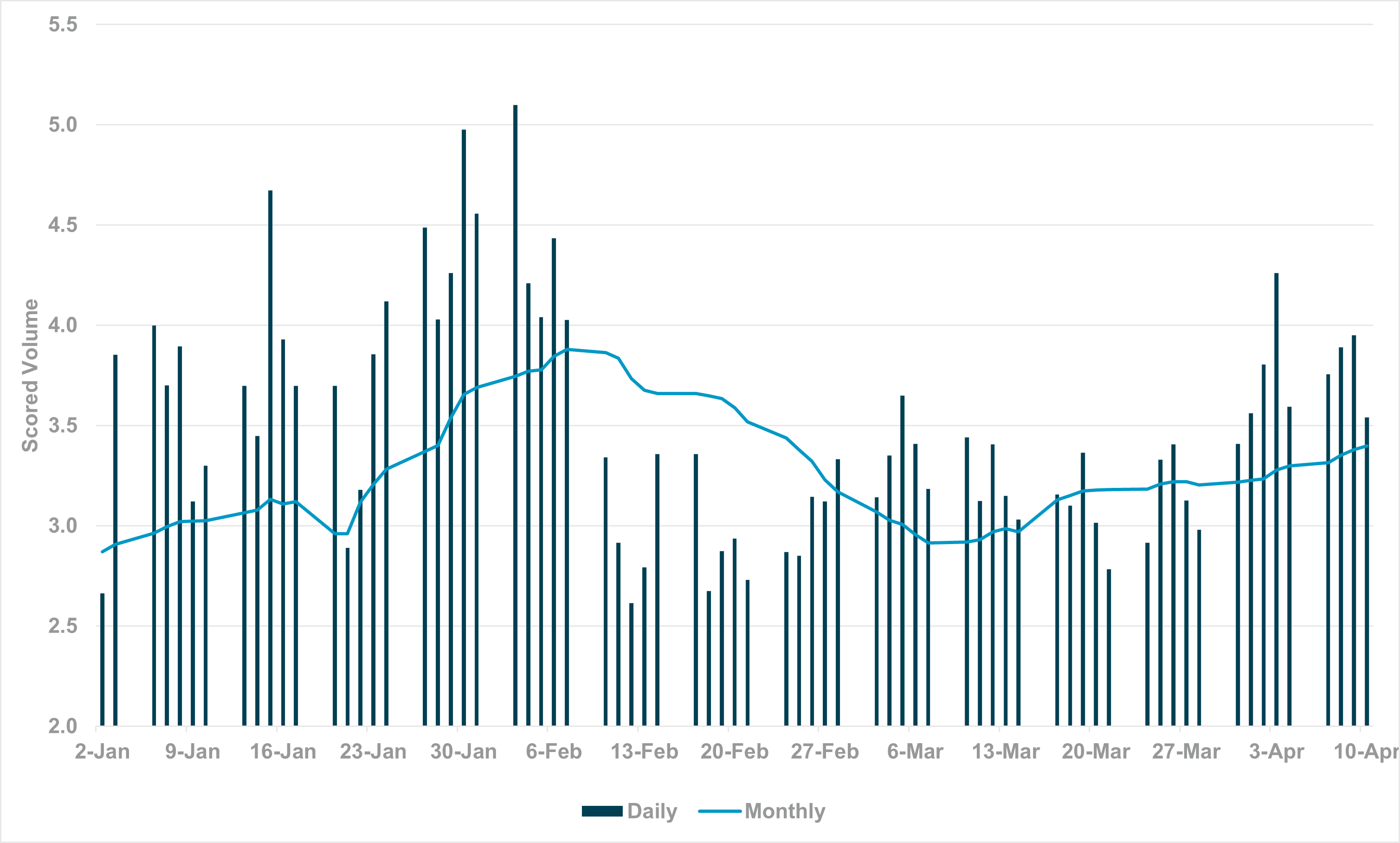

EXHIBIT #1: SURGE IN VOLUMES LAST WEEK IN U.S. TREASURYS

Source: BNY

The spike in U.S. bond volumes in our data has not yet reached January highs and suggests there is room for more moves ahead given ongoing uncertainty on policy.

Risk sentiment shifts to relief with the bounce back in shares in Asia extending to Europe. Some of the shift started with President Trump’s tariff exemptions on consumer electronics including smartphones, computers and semiconductors, which drove up technology shares globally. The ongoing surge in China exports and credit also played a role in the rally as it highlights the ongoing pre-tariff building of inventories as well as weaker consumer demand there. The CNY fixed is weaker again, leaving both China and U.S. currencies weaker. Surveys from the WSJ and the FT over the weekend highlighted the hit to confidence globally and put the focus on hard economic data to prove out the current weaker outlooks. The outlook for a recession in the U.S. rose from 22% in January to 45% in April. The other issue for investors globally is links to the USD. The role of the dollar as a safe haven remains under threat because of confusion over policy. The talk of pushing out the 20-year auction last week matters this week as all eyes remain on 10-year yields with 4.5% seen as a key pivot point. Some analysts do not expect any new action from Treasury Secretary Bessant unless 5.0% is retested. The new correlation between volume and yields looks more important than much else with volatility everywhere still elevated despite today’s modest green across the screens.

China March exports surged 12.4% y/y or 5.8% y/y. Exports to U.S. and European Union rebounded sharply to 8.8% y/y (Feb: -11.4%) and 9.9% y/y (Feb: -12.6%), respectively and exports to ASEAN were near all-time highs at $59bn in March, accounting for 19% of the total exports. The trade data is likely to embolden China’s push back on U.S. tariffs, with the view that exemptions are another step-back, adding to risk of extended tensions. – CSI up 0.23%, CGB 10Y up 0.2bps to 1.65%, CNH off 0.2% to 7.3055

Monetary Authority of Singapore (MAS) reduced the slope (rate of appreciation) of the SGD NEER policy band while keeping the width of the band at the level at which it is centered. MAS lowered its 2025 GDP and inflation forecasts. GDP at 0-2.0% (Jan25:1.0-3.0%), core CPI at 0.5-1.5% y/y (Jan25: 1.0%-2.0%) and headline CPI at 0.5%-1.5% (Jan25: 1.5-2.5%). The easing of policy is expected but likely not enough if trade issues extend for quarter – STI up 1.15%, SIGB 10Y off 6.3bps to 2.576%, SGD up 0.1% to 1.3140

Japan isn’t planning to use its U.S. Treasury holdings as a tool to counter U.S. tariffs in talks scheduled between the two governments on April 17. February final industrial production rose 2.3% m/m, 0.1% y/y – weaker than flash – but bouncing from January levels on machinery and electronics. The hope for a trade deal with U.S. is a key driver for BOJ and JPY with stronger FX and more rate normalization part of talks. Nikkei up 1.18%, JGB 10Y yields up 4bps to 1.325%, JPY up 0.3% to 142.95

Swiss Producers prices fell by 0.1%y/y, but there was a gain of 0.1m/m. Food products in particular were more expensive. Petroleum products, in contrast, were cheaper. The data would not reflect the recent surge in the franc as markets are now expecting a 50% chance of SNB moving back to negative rates at their September meeting. Swiss domestic sight deposits increased by CHF5bn to CHF438.37b in the week of April 11 from CHF433.37b in the week of April 4, according to the SNB. This is the biggest change since the second week of March. While high, this is not even the highest number in the last six weeks (w/c March 7th was CHF6.5bn). During extreme moves in August / September 2011, sight deposits increased by close to CHF100bn in barely three weeks. Swiss Mkt up 1.6%, Swiss 10-year yields up 0.6bps to 0.36%, CHF off 0.25% to .8170

Argentina dismantles capital controls, puts ARS trading into wider trading bands – The Argentina Peso will now be allowed to float freely between 1,000-1,400 shifting from a tightly controlled 1% crawling peg. The question is how much ARS weakens today after closing 1,074/dollar on Friday, with the blue market at 1,355/dollar. The country sealed a $20bn deal with IMF on Friday along with other loans from international lenders.

US New York Fed 1-year consumer inflation expectations forecast to rise to 3.15% from 3.13%. Given the spike up in the preliminary University of Michigan survey last week, this data matters

Fed Speakers: Federal Reserve Governor Christoper Waller speaks on economic outlook, Federal Reserve Bank of Philadelphia President Patrick Harker speaks on the role of Fed, Federal Reserve Bank of Atlanta President Rapheal Bostic to speak in a fireside chat. Watching for signals on what triggers FOMC easing or bond buying.

Mood: Heightened risk aversion mode with iFlow dropped deeper in the risk-off territory at –0.17, driven by the increase selling of equities against buying in government bills.

FX: Heavy selling pressure for MXN and CAD last week subsided while outflows continue for EUR and GBP. JPY is overheld and JPY’s scored holdings in USDJPY pair is at historical extreme levels. USD, AUD, CHF and CNY are bought.

FI: Broad selling pressure in government bonds globally except for demand in China, Australia and Europe. Cross border investors selling of U.S. Treasury continues.

Equities: DM America and EM APAC equities were sold the most. Energy, Health Care and Financials sectors were significantly sold.

“Green is the fresh emblem of well founded hopes. In blue the spirit can wander, but in green it can rest.” – Mary Webb

“It’s not easy being green.” – Kermit The Frog

Monetary Authority of Singapore (MAS) reduced the slope (rate of appreciation) of the SGD NEER policy band while keeping the width of the band and the level at which it is centered. MAS noted that Singapore’s output gap will turn negative. Imported and domestic cost pressures will remain low and MAS core inflation is forecast to stay well below 2%. The risks to inflation are tilted towards the downside. MAS lowered its 2025 GDP and inflation forecasts with 0-2.0% GDP (Jan25: 1.0-3.0%)and core CPI at 0.5-1.5% y/y (Jan25: 1.0%-2.0%) and headline CPI at 0.5%-1.5% (Jan25: 1.5-2.5%).

New Zealand March Performance Service Index at 49.1 from 49.0. Looking into breakdown, Activity/Sales (47.4) fell a further 1.7 points, although New Orders/Business (50.8) recovered to record its highest value since February 2024 and Employment (50.2) recorded its highest value since November 2023, ending 15 months of consecutive contraction. Businesses outlined reduced activity driven by economic uncertainty, high interest rates, inflation and weak consumer and client confidence. Added pressures included global tariffs, rising costs and seasonal or weather-related downturns. NSX50 +0.7%, 10yr NZGB down 3bp to 4.73%, NZD +1% at 0.5883

China March aggregate financing gained further at 8.4% y/y from 7.8% lows in October 2024 and March total loans by financial institutions (new yuan loans) edged higher at 7.4% y/y after 16 months of decline. M2 is unchanged at 7.0% y/y. Aggregate financing came at CNY 15180bn ytd, or CNY 5888bn increment for March, or 8.4% y/y. Total local currency bank loans account for CNY 3828bn while the government and local government bond issuance continues to be strong at CNY 1490bn vs CNY 1690bn in February 2025. As for financial institution lending, domestic loans to household surged by CNY 985bn after a decline of CNY 389bn in February 2025, of which medium-to-long-term loans to households, an indicator of mortgage conditions, surged to CNY 505bn (Feb25: CNY -115bn). This was the greatest monthly gain since January 2024 (CNY 634bn).

China March Exports grew strongly at 12.4% y/y against consensus of 4.3% y/y but imports declined at -4.3% y/y driven by lowering of commodities prices. In year-to-date cumulative terms, exports at 5.8% ytd y/y while imports at -7.0% ytd y/y. In terms of export destination, exports to U.S. surged to 8.8% y/y or 4.5% ytd y/y, and to European Union at 9.9% or 3.7% ytd y/y. Exports to ASEAN up 11.9% y/y or 8.1% ytd y/y. Indeed, the export to ASEAN is near record levels at $59bn in March compared with $59.7bn exports in December 2024. Exports to Vietnam at 19.6% y/y or 16.5% ytd y/y.