Market Movers: Goats

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

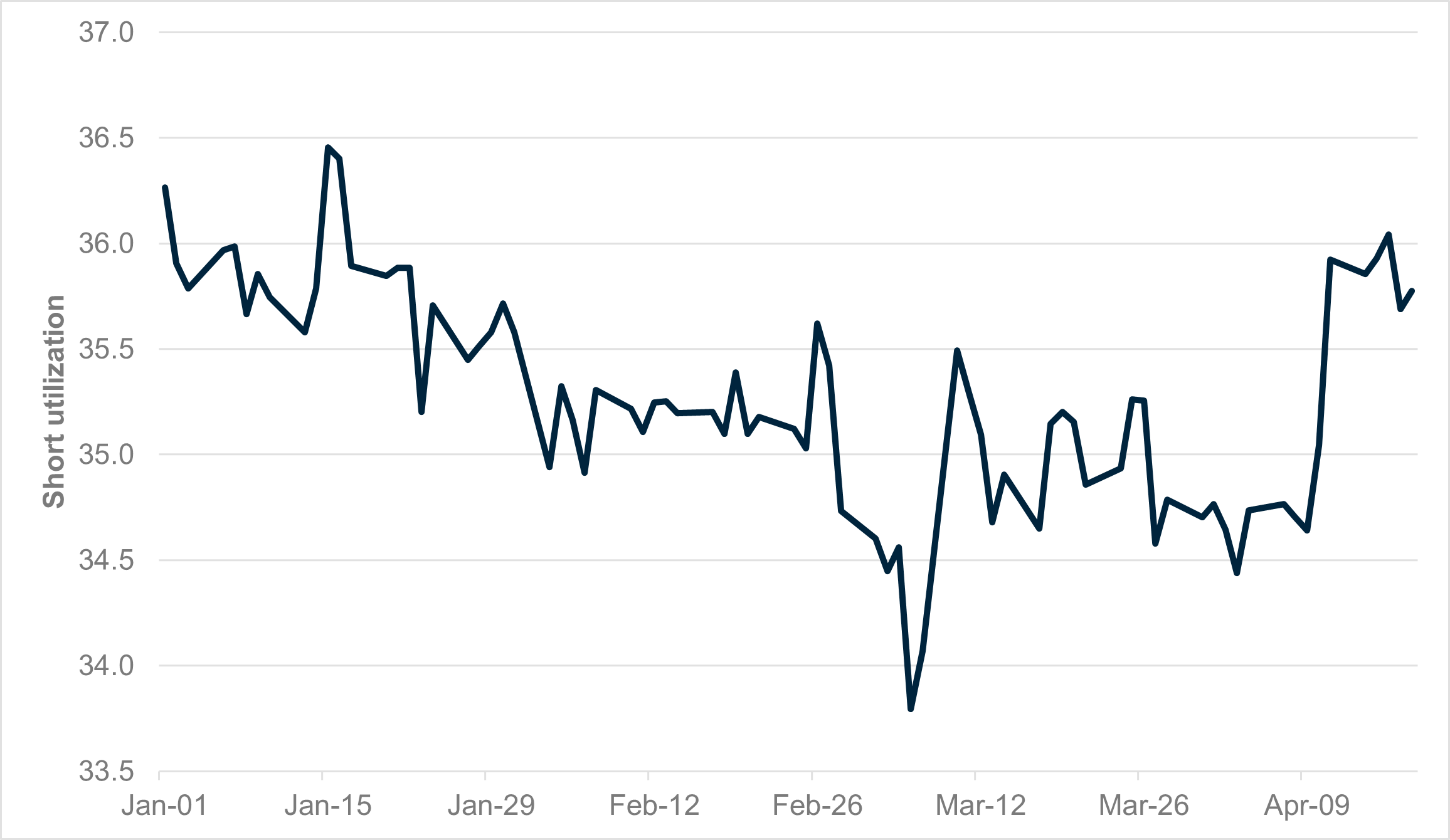

EXHIBIT #1: SHORT UTILIZATION IN U.S. TREASURY SECURITIES JUMPS OVER THE PAST WEEK

Source: BNY

In today’s Short Thoughts, we highlighted that both futures data and our own short interest data in iFlow indicate limited unwinding in the cash-futures basis trade. Any sharp unwinding would be manifested in a decline in short exposures. Within iFlow, we can also track exposures through short utilization, which measures the fraction of bonds in the BNY lending program that have been sold short, expressed as a percentage. The level of short utilization had a tight range between 34.5% and 35.5% throughout March and early April. However, last week there was a significant jump in short utilization, as it reached 36% for the first time since President Trump was inaugurated. While we would not rule out renewed interest in the basis trade, there is also the risk of monetary policy independence concerns starting to show up in Treasury term premia. Further, this is not how bonds should behave in a risk-off environment or during a rise in Fed easing expectations. Meanwhile, fears of ongoing weakness in foreign demand would only compound such concerns. Fears over bear steepening due to a variety of factors will likely sustain elevated levels of short utilization in the U.S. Treasury market. The ongoing shift in U.S. safe-haven status linked to trade has put the focus back on Europe, with EUR gains matching German Bund gains – a correlation shift from carry to safety.

Risk sentiment mixed as the mood music out of Asia regarding fast trade deals with the U.S. fades. Fed Chair Powell’s risk of firing by President Trump takes a back seat as growth worries return and as the scapegoat rhetoric suffices to bring some calm across markets. The longer trade talks take, the more risk to global growth gets priced into equities. Some of the delay is based on how countries view their relationship with China, with the prime ministers of both Japan and Vietnam sending clear signals to Beijing regarding their desires to balance their U.S. and China relationships. Thailand, meanwhile, also expressed concerns over a delay in trade talks, but Prime Minister Shinawatra also said that Bangkok will “approach talks with the mindset that we’ll give them something if they’re also willing to give us something.” This is in line with Japanese Prime Minister Ishiba’s comments yesterday, warning that Japan “won’t just keep conceding” in U.S. tariff talks, while a high-level Japanese delegation led by Tetsuo Saito, the junior coalition leader of Kometo, will deliver a letter from Prime Minister Ishiba to Chinese leader Xi Jinping highlighting a desire to maintain good trade relations with China as well. The APAC region’s relationship to U.S. trade and growth matters across all markets, as China is already pulling back from U.S. investments. The day ahead will keep the focus on how the nascent stability in U.S. equities plays against the 2-year note sale and USD. Carry trades remain fragile and the data on U.S. growth mixed, with central bank speakers saying it could hurt further hopes of a “Tuesday turnaround” in mood.

New Zealand sees trade surplus rise to NZD 970mn, led by a jump in exports, to NZD 7.59bn. China remains the top export destination for New Zealand, with exports rising by NZD $371mn (23%) on the month, driven by milk powder, butter and cheese. NZX50 -2.33% to 11836.70, 10y NZGB +3.5bp to 4.54, NZDUSD -1.3% to 0.6008.

The Thai cabinet has approved Somchai Sujjapongse as the new chair of the board of the Bank of Thailand. Meanwhile, talks between the U.S. and Thailand over a 36% tariff have been postponed after Washington asked Thailand to address certain “issues” related to trade. SET +0.28% to 1137.94, 10y TGB +1.8bp to 1.862%, USDTHB +0.2342% to 33.1650.

Swedish unemployment fell to 8.1% in March on an adjusted basis according to Statistics Sweden. This was well below expectations of a decline to 8.7% (from 8.9% in February) and is the lowest level in more than a year. The agency noted that while the labor market was “subdued,” there were “positive signs.” OMX30 -0.2% to 2350.85, 10y SGB -4bp to 2.293%, EURSEK +0.37% to 11.01.

Danish consumer confidence fell to -17.0 in April from -15.5 in March – the lowest level in over two years, according to Statistics Denmark. One-year forward expectations for the Danish economy have collapsed to the lowest levels since early 2021 to -31.7. OMX20 -5.04% to 1542.93, 10y DGB -4.4bp to 2.381%, EURDKK -0.0058% to 7.4660.

Swiss sight deposits on the week were up by CHF1.4bn on an aggregate basis to CHF448.3bn. Money supply was up by 2.8%y/y. The sigh deposit figures do not point to any sign of large-scale intervention, despite the recent surge in franc valuations. SMI -1.19% to 11521.70, 10y Swiss +3.1bp to 0.36%, EURCHF +0.053% to 0.9319.

U.S. April Richmond Fed Manufacturing Index expected -7 after -4 but given the weakness in other Fed reports downside surprises matter. Services revenues will be watched as well, expected -6 from -4.

U.S. Treasury sells $69bn in 2y notes along with $70bn in 6-week bills. First coupon auction of the week will be watched for demand, with 10y and 30y tomorrow and Thursday expected to matter more, but curve set-up key with this sale.

Fed Speakers will be the focus for easing bias and support for Powell/independence. Fed Governor Jefferson, Philadelphia Fed Harker both speak at Economic Mobility Summit; while Minneapolis Fed Kashkari moderates a discussion in D.C.; Richmond Fed Barkin holds a fireside chat in Virginia, and Fed Governor Kugler speaks on monetary policy transmission at the University of Minnesota.

ECB Speakers – President Lagarde on CNBC, ECB’s Guindos speaks in Madrid, ECB’s Knot speaks at IMF – all matter in context of EUR gains, tariff effects on economy, easing path.

Mood: Little sign of stabilization, with iFlow Mood drifting further into risk-off territory lead by equities outflows and the most demand for sovereign bonds since December 2024.

FX: Better FX inflows at the expense of rising USD outflow momentum as well as EUR and JPY outflows. AUD, CNH, NZD, CZK, HKD and TWD posted the most inflows. Note the significant surge in NOK scored holdings.

FI: Mixed flows with demand in Australia, U.S. Treasurys and Eurozone government bonds. U.K. gilt, Japanese and Chinese government bonds were sold.

Equities: APAC posted the most selling pressure, led by China, with light buying in LatAm. Flows in G10 and EMEA were mixed. Within U.S. equities, energy, the consumer staples and communication services sectors were the most bought vs. selling in materials, industrials and consumer discretionary.

“Ideas are easy. It’s the execution of ideas that really separates the sheep from the goats.” – Sue Grafton

“When a goat likes a book, the whole book is gone, and the meaning has to go find an author again.” – William Stafford

Bank of England MPC member Meghan Greene maintains caution over price trends in the U.K. She notes that although the falling dollar and tariffs would be disinflationary for the U.K., it is too early to say “where the dust settles” on currencies. Although markets are currently pricing in a full cut by the BoE at the May meeting, she warned that wage growth was still “pretty high” and there was “no sign of shakeout” in the U.K. labor market yet. She remains concerned about the rise in inflation expectations in the U.K. and the fact that services prices point to “inflation persistence” in the country. Her comments do not preclude a cut at the upcoming meeting, but given the supply pressures in the country, we expect the BoE to emulate the ECB in not committing to a sustained easing cycle. FTSE 100 +0.23% to 8294.7, 10y gilt +3.3bp to 4.6%, GBPUSD -0.4% to 1.3373.

South Korea March PPI eased from 1.5% to 1.3% y/y, the first month-on-month decline since October 2023. Lowering of PPI is likely to lead to similar trend in CPI. PPI agricultural dropped the most, falling by -3.0% y/y, while the PPI for electric power rose the most, at 4.6% y/y. PPI for manufacturing products at 1.0% y/y. KOSPI -0.1%, 10y KTB up 1bp to 2.62, KRW down -0.1% at 1422.

Taiwan March export orders were $53bn, up 12.5% y/y, down from an unusually high 31.1% y/y gain in February worth $49.5bn, while the Taiwan March unemployment rate ticked up slightly from 3.35% y/y to 3.36%. TWSE -1.6%, TWD down -0.1% at 32.498.

Turkey April consumer confidence drops to 83.9 from 85.9 – falling from 2-year highs with increased pessimism regarding current financial conditions (69.1 vs. 70.9) and household expectations for the next 12 months (84.3 vs. 84.7). Sentiment also weakened about the general economic outlook for the year ahead (82.8 vs. 84.6), while confidence in spending on durable goods over the next 12 months turned negative (99.3 vs. 103.2). BIST 100 up 0.45%, TRY off 0.15% to 38.261.