Market Movers: Glitter

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

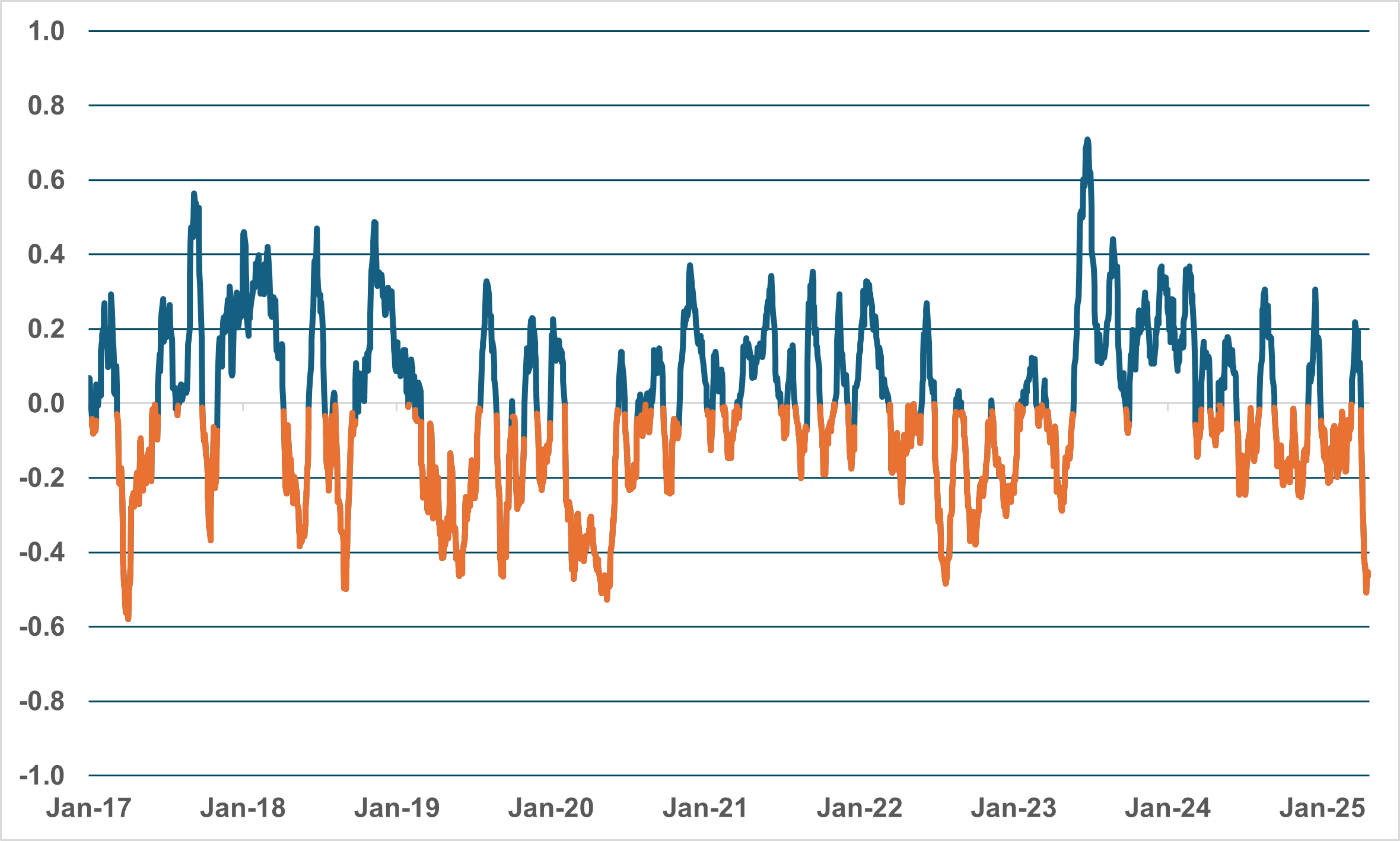

EXHIBIT #1: IFLOW CARRY BEGINS TO REBOUND FROM MULTI-YEAR LOWS

Source: BNY

Our iFlow Carry has been deeply into statistically significant and negative territory, reflecting the broader risk-off sentiment globally. The indicator was negative but inconsistent for much of 2025. It was not until April 2, 2025, before risk-off became far more severe, that the indicator suddenly moved into strong alignment with traditional carry-off views. Funders in APAC and Europe generally performed well (such as CHF and THB), while high yielders struggled (TRY, BRL and MXN). Our index was at the most negative and statistically significant level since 2017. However, this week, similar to what we are seeing in iFlow Mood, there are nascent signs of a rebound. EM high yielders may be the key barometer for watching risk ahead.

Risk sentiment has bounced back higher with three key drivers:

1) Better earnings led by Alphabet after U.S. close

2) China granting some tariff exemptions on 125% tariffs

3) Better hard economic data, with U.K. sales an example

The consequences of higher equities are a stronger USD, but not higher U.S. yields. That is the key point to watch. Japan 10y yields are higher again after their CPI surged, putting the BOJ into a tough place as economic slowing from tariff uncertainty has delivered stagflation risks. The other headlines of note pushing against risk are in India, where Apple now plans to make its U.S. iPhones, and where a water conflict with Pakistan has led to geopolitical concerns. The traditional geopolitical barometer of oil is lower this week with hopes high for an Iran nuclear deal albeit tempered by doubts about Ukraine/Russia talks. The IMF Spring Meetings end Saturday and the FOMC black-out period starts – both matter to the mood swings for the week ahead and how today plays out, given the rush of “hope” seen across markets to stabilize after a historic sell-off globally. Today, the focus will remain on stocks with S&P500 5450 a key resistance, along with more earnings and more hopes for better news, with focus on University of Michigan consumer sentiment. There is one correlation that glitters in the lightness of the moment: gold to equities. The markets will be watching for where the USD alternative finds support today and going forward.

Tensions between India and Pakistan continue to rise. Troops from Pakistan and India exchanged fire overnight across the line of control in disputed Kashmir, officials said, after the UN urged the nuclear-armed rivals to show “maximum restraint” after a deadly shooting in the region. Yesterday Pakistan closed its airspace to India’s airlines, said it would suspend a 1972 peace treaty with its larger neighbour, and warned that any diversion of shared river waters would be “considered an act of war.”

China’s Politburo held its customary meeting to analyze the current economic situation and economic work, noting that external shocks are intensifying. The meeting emphasized the need to strengthen bottom-line thinking and fully prepare contingency plans. Notably, it introduced a new expression: coordinating domestic economic work with international economic and trade struggles. The meeting emphasized stabilizing employment, enterprises, markets and expectations, seeking to counter external uncertainties with the certainty of domestic development. These statements reflect policy shifts since the U.S. implemented its reciprocal tariffs in April.

Japan April CPI surged from 2.9% to 3.5% y/y while core ex-fresh food and energy increased to 3.1% from 2.2% y/y. Fresh food inflation eased to 4.1% y/y from 13.2% y/y, but food inflation stayed elevated at 6.0% with rice inflation at a record 93.8% y/y. NIKKEI +1.9% to 35705.74, 10y JGB +2.8bp to 1.333%, USDJPY +0.554% to 143.41.

U.K. retail sales surprised strongly to the upside, with April rebounding +0.5% m/m, +3.3%y /y for ex-auto and fuels. The Office for National Statistics cited good weather as the general reason behind the surprise: "within non-food stores, clothing stores were the subsector with the strongest growth with retailers mentioning good weather boosting sales. Non-store retailing sales volumes were up on the month, with similar commentary received about the weather, specifically mentioning boosts to clothing and DIY goods." FTSE 100 +0.14% to 8418.87, 10y gilt -1.0bp to 4.492%, GBPUSD -0.3519% to 1.3294.

U.S. April final University of Michigan Consumer Sentiment expected 50.5 from 50.8 with current conditions at 56 from 56.5 and expectations at 46.3 from 47.2. Bigger focus will be on one-year inflation with flash at 6.8% and 5–10 year inflation expectation flash 4.4% steady – both are seen as risk to FOMC outlook.

Canada February final retail sales expected -0.4% m/m after -0.6% m/m, with ex-autos -0.4% m/m after +0.2% m/m – the March flash expected up 0.1% m/m. All this will add to the focus on BOC and the tariff slowdown set-up vs. their pre-emptive easing.

Mood: Risk normalization continues with reduced equities selling flows against ongoing demand for sovereign bonds. iFlow Mood likely to drift into neutral zone in coming days.

FX: CEEMEA and APAC FX were bought while mixed flows in LatAm and G10. USD, EUR and JPY were sold against significant demand in AUD.

FI: Continued selling pressure in Australian and Chinese government bonds while cross border investors show buying interest in both U.S. Treasurys, and Eurozone government bonds. Note the dissipating Indian government bonds inflows after achieving 10% benchmark weight at the end of March.

Equities: Both EM and DM APAC were sold against buying in EM and DM EMEA. Within U.S. equity, information technology is the only sector with outflows against the turnaround of flows in the rest, most in energy, real estate and financials sectors.

“People are like stained glass windows. They sparkle and shine when the sun is out, but when the darkness sets in, their true beauty is revealed only if there is a light from within.” – Elisabeth Kubler-Ross

“Enthusiasm is the yeast that makes your hopes shine to the stars. Enthusiasm is the sparkle in your eyes, the swing in your gait. The grip of your hand, the irresistible surge of will and energy to execute your ideas.” – Henry Ford

China’s Ministry of Commerce announced that it had concluded a two-day National Conference on Responding to Trade Frictions. The meeting emphasized that China is currently facing a phase of intensified trade frictions. In light of the difficulties and challenges, it is essential to strengthen confidence, remain composed and adopt strategic approaches—seizing opportunities in times of crisis and opening new paths amid shifting dynamics. It called for raising political awareness, adhering to a systematic mindset, enhancing bottom-line and extreme-case thinking and focusing on preventing and defusing trade risks. The commentary suggests that Beijing is prepared to change policy and prepared for worst-case scenarios. CSI300 +0.07% to 3786.99, 10y CGB +0.4bp to 1.656%, USDCNY -0.039% to 7.2858.

UK April GfK Consumer Confidence dropped more than expected from -19 to -23, the lowest since November 2023. The future indicator on personal finances slipped badly, dropping four points to -3. There are good reasons for this downturn. Consumers have not only been grappling with multiple April cost increases in the form of utilities, council tax, stamp duty and road tax, but they are also hearing dire warnings of renewed high inflation on the back of the Trump Tariffs.

Japan March nationwide departmental sales registered a 2.8% y/y decline, with Tokyo dropping by 4.2% y/y. The biggest declines were registered in clothing (-3.6% y/y) and accessories (-8.9% y/y), while food also declined by 2% y/y. Household goods, in contrast, jumped by 7% y/y.

Singapore March industrial production expanded by 5.8% y/y, far lower than the expected level of 8.1% y/y. Excluding biomedical manufacturing, output increased 4.9%. On a three-month moving average basis, manufacturing output increased 4.0% in March 2025 compared to a year ago. On a seasonally adjusted month-on-month basis, manufacturing output decreased 3.6% in March 2025. Excluding biomedical manufacturing, output increased 0.8%. Pharmaceuticals output expanded by 44.1% y/y, offset by a fall in petrochemicals to -7.9% y/y. General manufacturing also fell by 13% y/y. STI -0.1% to 3828.15, 10y SIGB -3.4bp to 2.477%. USDSGD +0.197% to 1.3139.

Singapore Q1 private home prices final reading at 0.8% q/q, better than flash estimate of 0.6% q/q but slowed from 2.3% q/q in Q4 2024. Singapore Q1 private home prices final reading at 0.8% q/q, a touch better than flash estimate of 0.6% q/q but slowed from 2.3% q/q in Q4 2024. Singapore real estate sector is cooling down at 3.3% y/y, the slowest y/y gains since 2.2% y/y in Q4 2020, but still at elevated record high levels in absolute terms.

French business confidence was unchanged for April at 96, while manufacturing confidence strengthened to 99, compared to expectations for a drop to 96. However, the production outlook fell to -16. INSEE highlighted that “the balance relating to the expected change in investments for 2025 is significantly lower than that on the estimated change in investments for 2024 in most of the sub-sectors, with the exception of the manufacture of machinery and equipment goods.” CAC 40 +0.63% to 7549.99, 10y OAT +1.2bp to 3.176%, EURUSD -0.337% to 1.1351.

Hungarian unemployment fell to 4.3% from 4.5%. In another sign of robustness in the labor market, there was a decline of 36,800 in the level of inactive population for the first quarter of the year. Sandor Czomba, the state secretary for employment policy, said the number of employed was "outstanding," while the jobless rate remained under the European Union average. The number of registered jobseekers is at a low not seen since the change of system, he added. BSE +1.49% to 92505.75, 10y HGB +4.9bp to 6.893%, EURHUF +0.21% to 406.99.