Market Movers: Follow the Money

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 10 minutes

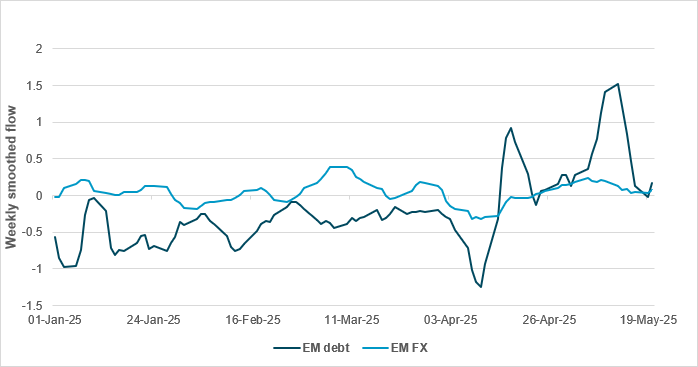

EXHIBIT #1: EM DEBT SURGE NOT ACCOMPANIED BY SIGNIFICANT HEDGING

Source: BNY

We have been monitoring capital flows into emerging markets, with a particular focus on their impact on hedging dynamics. Equity inflows have been especially notable in the Asia-Pacific region, while opposing foreign exchange flows in certain markets suggest that these inflows are being actively hedged. Several central banks have attributed recent currency volatility and their subsequent interventions to these equity-driven flows, which they view as contributing to excessive appreciation pressures. Outside of APAC, fixed income markets are also attracting strong inflows, particularly since late April; they may potentially be surpassing equities in driving EM demand. However, no clear hedging misalignment is evident. We observe that there has been a surge in sovereign bond inflows across emerging markets over the past four weeks. During the same period, overall FX flows have also turned modestly positive. On an aggregate basis, total EMFX flows, measured using weekly smoothed data, have reached their second-highest level of this year. The alignment between fixed income and FX flow trends suggests a growing interest in total return strategies. This indicates that, beyond capturing duration, investors are also actively seeking FX exposure, either across the full portfolio or through foreign exchange carry. Importantly, these developments appear to be occurring independently of U.S. market dynamics, lending support to the idea that broader diversification into emerging markets is underway. This is particularly notable given the historically low base in EM duration exposure.

Risk sentiment remains weak after the U.S. 20y bond sale disappointed investors, driving yields higher. The link between higher rates and lower growth and lower equity values continued overnight. A lack of dollar buying in response to higher rates added to concerns about U.S. fragility. However, as the U.S. market faces more economic releases – home sales, jobless claims, flash PMI and more Fedspeakers – there is a sense that buying the dip will return if the hard data continues to hold up against softer sentiment. The overnight session also made it clear that there are fewer alternatives to the dollar, given the weak Eurozone PMI and ongoing turmoil over debt in Japan, along with an IMF warning about French budgets. The odds that the U.S. will muddle through with a tax bill rose overnight, as another committee pushed the bill forward. In addition, the pushback from the U.S. administration on tariffs, which are driving up inflation, continues to be countered by ongoing talks. The pressure on market sentiment remains linked more to bond yields rising than to the dollar falling, leaving equities to look for other factors and to follow the money. Chasing momentum has worked in May. If the U.S. data today don’t block further evidence of a bounce-back in 2Q growth, then higher yields and a weaker dollar are likely to help rather than hurt a rebound in risk-taking.

Germany’s leading Ifo index came in at 88.9 in May, stronger than the expected 88.0. The confidence index also surprised to the upside, albeit marginally, at 87.5. The report suggests that trading stability in May has contributed to an improvement in the Germany economic outlook. At the same time, and despite some teething issues, the new government is poised to push forward a domestic investment agenda, which has been driving the wave of European corporate re-rating. Nonetheless, the index has been caught in an 85-90 range throughout the past 18 months, and structural issues cannot be ignored: several sectors face competition and tariff risk, with automotive and pharmaceuticals particularly affected. DAX -0.784% to 23933.19, EURUSD -0.053% to 1.1325, 10y Bund +1.4bp to 2.66%.

May flash composite PMI for Germany fell to 48.6 from 50.1 in April, marking the first decline this year. The downturn was led by services, where activity dropped to a 30-month low of 47.2, despite continued – though slower – growth in manufacturing output (51.5). New export orders, particularly from the U.S. and Europe, supported manufacturing, but overall new business declined. Employment slipped slightly, with job losses in manufacturing offsetting minor gains in services. Inflationary pressures eased, with output charge inflation at a seven-month low. Business confidence improved, especially among manufacturers, driven by expectations of fiscal stimulus and trade deals. Service sector sentiment remained subdued.

France’s private sector remained in contraction in May 2025, with the flash composite PMI at 48.0, marking the ninth consecutive month below the 50.0 threshold. Services were once again the main drag, offsetting stronger manufacturing output, which hit a 37-month high. New orders declined across both sectors, with service providers reporting the sharper drop. Businesses engaged in widespread discounting, leading to the steepest fall in output prices since January 2021, despite rising input costs. Employment fell for the sixth month in succession, and backlogs of work continued to decrease. Business confidence slumped to its lowest level since April 2020, driven by weak demand, economic uncertainty and geopolitical concerns, with firms turning pessimistic about future activity. CAC40 -0.786% to 7848.32, EURUSD -0.053% to 1.1325, 10y OAT +2.6bp to 3.337%.

Eurozone flash PMI shows private sector activity contracted in May 2025, with the composite PMI falling to 49.5 from 50.4 in April. This marked the first decline in five months and a six-month low. The decrease was driven by a sharper fall in service activity, with the services PMI sliding to 48.9 from 50.1 – the weakest reading in 16 months. Meanwhile, manufacturing showed relative resilience: the manufacturing PMI rose to a 33-month high of 49.4 (from 49.0), while the manufacturing output index held steady at 51.5. Employment was flat overall, with job losses in manufacturing offset by modest gains in services. Input and output price inflation eased, though service input costs rose while manufacturing prices fell. Business confidence dipped to its lowest level since October 2023, reflecting subdued demand and weak sentiment in the service sector, despite a notable improvement in manufacturing optimism. Euro Stoxx 50 -0.82% to 5409.71, EURUSD -0.053% to 1.1325, BBG AGG Euro Government High Grade EUR +1.5bp to 2.859%.

Japan May manufacturing PMI improved slightly but remained in the contraction zone at 49.0, while services PMI eased from 52.4 to 50.8. Looking into the details, demand conditions looked more fragile, with new business across both the manufacturing and service sectors falling for the first time in nearly a year, and foreign demand declining for the second straight month. Cost pressures remained elevated in May, but with some tentative signs that input price inflation is cooling, as the latest data show the slowest rise in operating expenses in over a year. This translated into a softer uptick in selling prices. Lastly, business confidence across Japan’s private sector was the second-lowest recorded since the initial wave of the COVID-19 pandemic, with uncertainty around the future trade environment and foreign demand clouding the outlook and dampening output projections for the year ahead. Elsewhere, Japan March private sector core machine orders rose sharply at 13.0% m/m, 8.4% y/y. Nikkei -0.839% to 36985.87, USDJPY -0.432% to 143.06, 10y JGB +4.6bp to 1.573%.

UK public sector net borrowing in April reached £20.2 billion, £1.0bn higher than in April 2024 and the fourth-highest April figure since records began in 1993. The rise was driven by increased spending on public services, welfare and pensions, partially offset by higher national insurance contributions. For the financial year ending March 2025, borrowing totaled £148.3bn, exceeding the Office for Budget Responsibility’s forecast by £11.0bn. Public sector net debt excluding public sector banks stood at 95.5% of GDP, a level last seen in the early 1960s. Despite strong tax receipts, inflation-linked spending pressures and policy commitments such as the pension triple lock continue to drive fiscal strain, underscoring ongoing challenges for fiscal consolidation and long-term debt sustainability. FTSE 100 -0.587% to 8734.9, GBPUSD +0.068% to 1.3429, 10y gilt +1.8bp to 4.775%.

Australia May PMI manufacturing was unchanged at 51.7, while PMI services dropped to 50.5 from 51, their lowest since November 2024. Within manufacturing, new order growth eased despite a renewed rise in exports. The main positive from the May release was a sustained and solid pace of job creation. There were signs of inflationary pressures softening in May, with both input cost and output prices increasing at slower rates than in April. ASX -0.567% to 4736.14, AUDUSD +0.327% to 0.6457, 10y ACGB +0.7bp to 4.457%.

U.S. weekly jobless claims expected to be near-unchanged at 230k vs. 229k last week.

U.S. May flash PMI for manufacturing is expected to dip into contraction (consensus 49.8) after four months of expansion, while services PMI is forecast to drift higher, to 51.0 (April: 50.8).

U.S. April existing home sales forecast to rise 2% m/m to 4.10 million from 4.02 million.

Fedspeakers: Richmond Fed Barkin in fireside chat in Virginia, while NY Fed Williams gives keynote address at a Fed event in NYC.

U.S. Treasury sells $18bn in 10y TIPS: this would not normally be an event, but given the tail to yesterday’s 20y sale, any Treasury sale is in focus, particularly of inflation-linked paper.

Mood: iFlow Mood has shifted into risk-neutral zone for the first time since early April. Equities buying momentum continue to be strong, along with robust demand for sovereign bonds.

FX: AUD and SEK recorded the most outflows, while TRY posted the most inflows, followed by CNY. In aggregate terms, EMEA were bought, against selling in G10, APAC and LatAm.

FI: Broad and moderate demand for sovereign bonds in G10, APAC and EMEA, compared with better selling in LatAm. Within G10, U.S. Treasurys were bought, but there was large selling in corporate bonds, against selling in Eurozone government bonds and U.K. gilts.

Equities: Swedish equities were sold the most, against better buying in Taiwanese, Polish and Chilean equities. Within U.S. equities, communication services and industrials were the only two sectors that posted outflows, against inflows in the rest, above all in the financial, materials and information technology sectors.

“Forget what they told you. You want the truth, follow the money” – Roxanne Bland

“Chase the vision, not the money. The money will end up following you.” – Tony Hsieh

India’s April flash composite PMI rose to 61.2 from 59.7 in April – the fastest expansion since April 2024. This was driven by a sharp upturn in services. The services PMI hit 61.2, marking a 14-month high, while the manufacturing PMI edged up slightly to 58.3 from 58.2, indicating continued strength. However, the manufacturing output index dipped to 61.4 from 61.9, reflecting the slowest production growth in three months. Despite this, both sectors benefited from strong domestic and export demand, with overall new orders rising at the fastest pace in a year. Employment growth hit a fresh series high, as firms expanded hiring to meet demand. Input cost inflation reached a five-month high, with the sharpest output price increase in manufacturing in over 11 years. Business confidence rebounded, led by service providers, as firms expected sustained demand to support output in the coming year. SENSEX -1.073% to 80720.71, USDINR +0.355% to 85.9463, 10y INGB +0.5bp to 6.25%.

Singapore Q1 final GDP came better than expected at -0.6% q/q, 3.9% y/y, vs. flash of -0.8% q/q, 3.8% y/y or 0.5% q/q, 5.0% y/y in Q4 2024. Singapore is maintaining a 2025 GDP forecast of 0%-2.0% but is warning against the possibility of a technical recession. The breakdown shows the following falls: manufacturing -5.8% q/q, 4.0% y/y (Q4: 0% q/q, 7.4% y/y); construction -1.4% q/q, +5.5% y/y (Q4: 0.3% q/q, 4.4% y/y); wholesale trade -0.4% q/q, 4.2% y/y (Q4: 0.9% q/q, 6.7% y/y); and information and communication -3.4% q/q, 4.4% y/y (Q4: 2.4% q/q, 4.2% y/y). Meanwhile retail trade (1.8% q/q, 0.1% y/y; Q4: -1.2% q/q, -1.0% y/y) and real estate (4.2% q/q, 7.1% y/y; Q4: 1.1% q/q, 3.5% y/y) grew on the quarter. See chart for y/y breakdown. Elsewhere, the MAS commented that the policy stance remains appropriate for now, a slight hawkish comment. Note that “appropriate” was used between April 2023 and July 2024, the meetings where the MAS maintained a status quo policy. The word “appropriate” was dropped in October before it initiated easing measures in January 2025 and April 2025. The unusual comment from the MAS could hint at a status quo stance ahead of July’s MAS meeting. STI -0.139% to 3877.14, USDSGD +0.047% to 1.2895, 10y SGB +1bp to 2.517%.

Malaysia April CPI unchanged at 1.4%, core CPI ticked up to 2.0%, its highest since November 2023. The upward trajectory in core inflation means the BNM will likely stay on hold for longer, despite a recent dovish tilt. KLCI -0.963% to 1529.92, USDMYR -0.298% to 4.2583, 10y MGB -0.6bp to 3.588%.

Japan international transactions in securities update, as of May 16, 2025. Foreign bond buying by Japanese investors accelerated to ¥2,825bn vs. ¥1,929bn, as the 10y UST yield rose. Demand for foreign equities came to a halt after eight weeks of buying, net sold small ¥-226bn. Foreigner investors net sold small JGBs for the third consecutive week (¥-241bn vs. ¥-141bn the week prior), as the JGB yield moved past 1.50%, while foreign investors net bought Japanese equities for the seventh straight week, at ¥715bn, bringing year-to-date net flows back into positive territory at ¥333bn. Nikkei -0.839% to 36985.87, USDJPY -0.432% to 143.06, 10y JGB +4.6bp to 1.573%.

New Zealand budget deficit is expected to widen to -2.6% of GDP in 2026 from -2.3% in 2025, before progressively improving to -1.7% of GDP, -0.6% of GDP and a balanced budget in 2027, 2028 and 2029, respectively. S&P Global Ratings commented after the release of budget that New Zealand’s elevated twin deficits – referring to its fiscal and current account balances – are weaknesses that could weigh on the credit rating. NZX 50 -0.322% to 12662.25, NZDUSD -0.051% to 0.5936, 10y NZGB +0.1bp to 4.679%.