Market Movers: De-escalation?

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

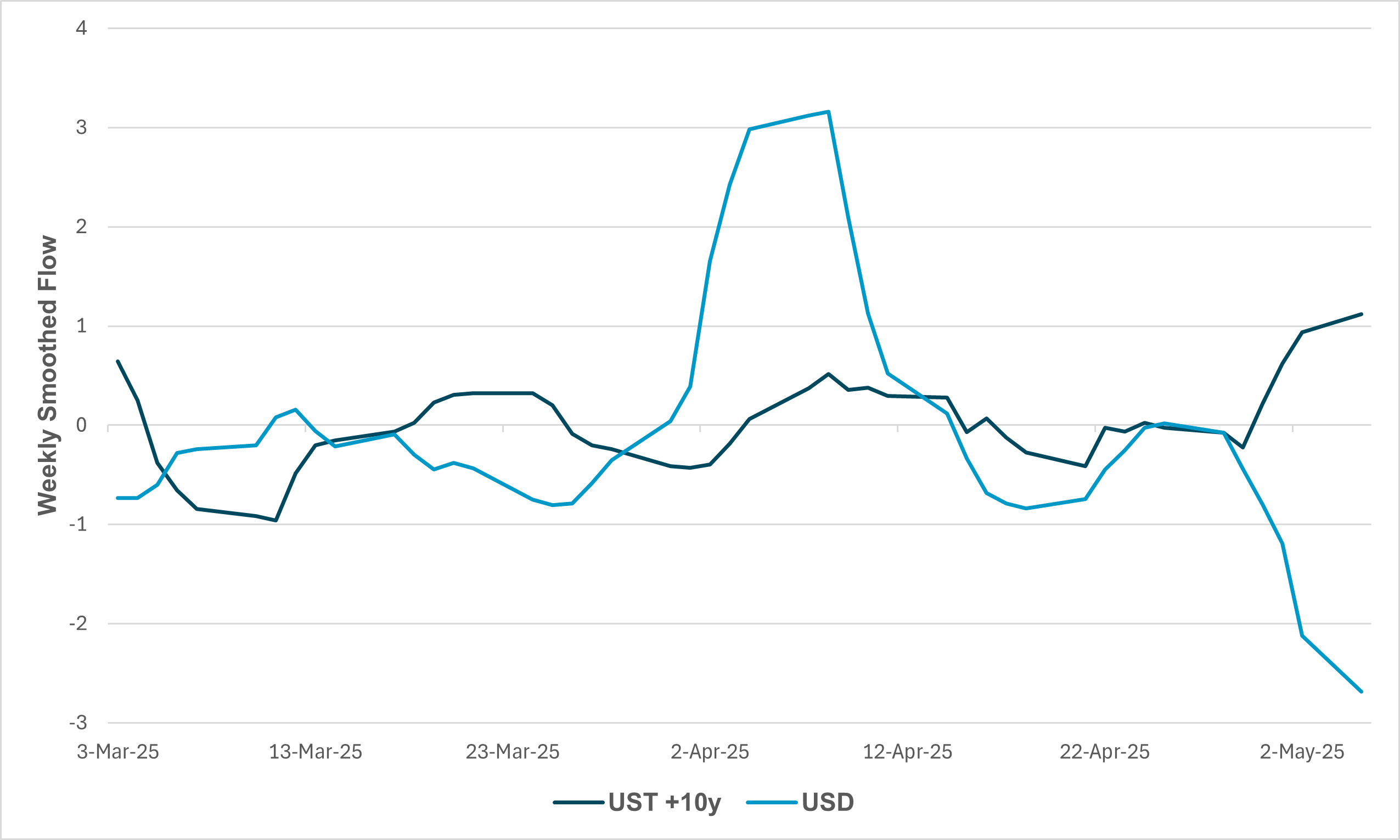

EXHIBIT #1: SIGNS OF RISE IN HEDGING OF U.S. TREASURY PURCHASES

Source: BNY, iFlow

Markets continue to monitor changes in hedging interest by APAC investors of U.S. fixed income assets after recent moves in TWD and heavy intervention in the HKD. Traditionally, asset managers in these economies have been content to capture yield exposures in the U.S. but there appears to have been a behavioral change since April. The chart above details weekly smoothed flow by cross-border investors in Treasurys and the dollar. During “liberation day,” there was surge flow in the dollar but given the client base, this may reflect some removal of USD hedges after liquidation of U.S. assets (particularly Treasurys with maturities below 10 years). Over the past week, we have seen surge flow return in US Treasurys buying duration over 10 years, accompanied by a sharp rise in USD selling. This appears to be a marked rise in hedging interest in the dollar − the reason could be as simple as expectations that the Fed will be more dovish than current expectations and rate differentials make it more efficient to run higher hedge ratios. Watching this price action after any Fed guidance which surprises to the hawkish side, there is a stronger case for a broader dollar decline as valuations and broader asset allocation reflect new realities.

Risk sentiment is negative as India launched strikes against targets in Pakistan and Pakistan-administered Kashmir. Islamabad has pledged a “befitting” response, but both sides appear willing to de-escalate. The episode marks the most significant clash between the two nuclear-armed neighbors since 2019, but so far, markets are showing resilience as expectations of a limited armed exchange have been building since late April. Meanwhile, trade de-escalation will be on the agenda in Switzerland as China and the U.S. have finally agreed to high-level talks this weekend. Both sides are managing expectations for any swift deal, but markets will be hopeful that sustainable relief for the world’s most crucial trade relationship can help generate economic certainty for the global economy. On the other hand, today, China’s domestic monetary and liquidity stimulus aimed at stabilizing growth is a tacit recognition that much damage has already been done. There is some disappointment over the ongoing lack of a fiscal follow-through; however, the measures add to the view that growth across Asia will stabilize. This supports the nascent money flows into the region, and central banks must manage FX movements accordingly. The current trade tariff uncertainty hasn’t changed much from where the Fed feared several weeks ago as it gears up for today’s decision, though we don’t expect any meaningful changes as data in the U.S. still do not support prospects for a cut. Nonetheless, policy divergence globally looks set to widen more than the 10bp from China today, as an unchanged Fed looks set to be sandwiched by deep cuts in Hungary and Poland of up to 50bp, while Brazil is expected to hike rates by the same amount − We will be watching if the actions or inactions today matter to markets and calm current volatility.

The U.S. and China will officially commence trade talks in Switzerland later this week. Chinese Vice-Premier He Lifeng will lead the Chinese delegation, while U.S. Treasury Secretary Scott Bessent and U.S. Trade Representative Jamieson Greer will lead U.S. efforts. This represents the most senior officials on the matter for both sides, which will likely raise market expectations for substantive results. However, Bessent noted that the initial contact will “center on de-escalation,” while Beijing’s statement from the Ministry of Commerce did not give any indication that headline tariff rates would come down immediately and repeated calls for the U.S. to “show sincerity” and “conduct talks on the basis of mutual respect, equal consultation and mutual benefit.” China’s Ministry of Foreign Affairs stated the meeting came at the U.S.’ request. CSI 300 +0.606% to 3831.63, USDCNY -0.102% to 7.2264, 10y CGB +1.3bp to 1.64%.

The People’s Bank of China announced cuts to multiple policy rates overnight. The required reserve ratio was cut by 50bp (different rates apply to different categories of banks), designed to release CNY 1tn in long-term liquidity. Meanwhile there was a 10bp rate cut in 7-day reverse repo rate from 1.5% to 1.4%, which should see LPR to be lowered by similar amount. The central bank also announced a 25bp interest rate reduction of structural monetary policy tools. Including re-lending to support agriculture and small enterprises, both from the current 1.75% to 1.5%; The Collateral Supplementary Loan (PSL) interest rate was cut from 2.25% to 2%.

In first comments made after Pakistan’s National Security Committee meeting overnight, Prime Minister Shehbaz Sharif called India’s strikes “an act of war…and a strong response is indeed being given.” Pakistan announced that it had shot down several Indian fighter jets in retaliation. However, Defense Minister Asif stated that Pakistan is also ready “to wrap up this tension” if India de-escalates. SENSEX -0.106% to 80555.86, USDINR -0.353% to 84.7363, 10y INGB -1.1bp to 6.34%.

U.K. construction activity declined for the fourth consecutive month in April, though at the slowest rate since January, with the construction PMI rising slightly to 46.6. Residential building showed relative resilience, while commercial construction dropped at its fastest pace since May 2020 due to heightened economic uncertainty. Civil engineering remained the weakest segment. New orders and purchasing activity both fell sharply, with job cuts continuing, albeit at a slower pace. Input cost inflation remained high, especially for materials like concrete and insulation, driven partly by rising payroll costs. Despite subdued demand, business confidence improved modestly, led by optimism in the residential sector. FTSE 100 -0.318% to 8570.04, GBPUSD -0.105% to 1.3355, 10y gilt -0.1bp to 4.513%.

Friederich Merz will travel to France and Poland today on his first foreign trip. He was sworn in as chancellor yesterday after a hastily scheduled second vote on his appointment passed the Bundestag yesterday afternoon. His failure to secure the appointment at the first attempt came as a major surprise to markets, leading to suggestions that some members of his coalition partners – the SPD – had reservations about the agreement. The vote also led to the main opposition AfD party to call for immediate new elections as Merz’ mandate was called into question. The unprecedented second vote was swiftly scheduled as parliamentarians looked to avoid a drawn-out process which would delay much needed reforms in Germany and Europe, especially as the final result was never in doubt as a simple majority would have sufficed later on. DAX +0.117% to 23276.89, EURUSD -0.009% to 1.1369, 10y Bund +0.4bp to 2.544%.

The papal conclave is set to begin today with the first the first vote expected at 6 p.m. Vatican time. 133 cardinal electors from 70 countries gathered to select the 267th pope following Pope Francis’s death on April 21. This conclave is notably the most geographically diverse, reflecting the Church’s global reach. The cardinals, many appointed by Francis, are divided between those favoring the continuation of his progressive reforms and others advocating a return to traditional values. Leading candidates include Italian Cardinal Pietro Parolin and Filipino Cardinal Luis Antonio Tagle, among others. The election process, steeped in tradition and secrecy, requires a two-thirds majority.

In their first official meeting, Canadian Prime Minister Mark Carney stated that Canada would “never” be for sale. However, he also noted that the meeting was “wide-ranging” and “constructive.” Trade tensions were prominent, with Trump maintaining tariffs on Canadian goods and hinting at renegotiating the USMCA. Carney emphasized Canada’s sovereignty and the need for a respectful bilateral relationship. Despite the disagreements, both leaders expressed a willingness to continue discussions, with plans to meet again at the upcoming G7 Summit in Canada. TSX +0.085% to 24974.72, USDCAD -0.058% to 1.3786, 10y CGB -4.4bp to 3.144%.

Czech National Bank decision: A 25bp cut is the base case as inflation continues to surprise to the downside, pushing the repo rate to 3.50%. More dovish members could push for a deeper move given downside risks to growth in Germany and Europe.

National Bank of Poland decision: The NBP is expected to cut its benchmark interest rate by 25-50bp to 5.50% or 5.25%, as MPC members have floated both positions. A cut was also demanded by Polish Prime Minster Tusk, which may draw unfavorable parallels with central bank independence issues elsewhere.

FOMC decision and post-decision press conference: The meeting will offer few fireworks. No rate move is expected, and without a Summary of Economic Projections the only additional information we’ll receive beyond the meeting’s prepared statement will be Chair Powell’s press conference.

Brazil Central Bank decision: COPOM is expected to raise the Selic rate by 50bp to 14.75%. The central bank has emphasized a data-dependent approach, but recent inflation surprises have shifted market consensus toward further tightening to regain credibility.

Mood: iFlow Mood stabilized and drifted slightly higher. Mood is shifting with signs of buying flows in equities complex and continued demand for sovereign bonds.

FX: Strong variation of G10 flow with USD and JPY outflows vs. CAD, GBP, EUR inflows. APAC and LatAm posted light inflows with outflows biased for EMEA currencies.

FI: Selling in Australian and Chinese government bonds continues against buying in U.S. Treasurys. Brazilian government bonds posted the most buying within iFlow universe.

Equities: Good EM APAC buying momentum against light selling in the of the region. Polish equities are the most favorable while Canadian equities are the least preferred.

“Peace is not absence of conflict; it is the ability to handle conflict by peaceful means.” – Ronald Reagan

“A gentle approach defeats the hard. Soft overcomes the strong.” – Lao Tzu

New Zealand released its Financial Stability Report. Five key highlights were: 1) trade tensions have increased financial stability risks, driven by tariffs, 2) weak New Zealand economy remains challenging, 3) lower interest rates have eased servicing costs but rising unemployment and businesses weak demand is a concern, 4) banks are well placed to support economy through any disruptions, and 5) stress tests continue to highlight increased resilience in the financial sector. NZX 50 +0.61% to 12496.89, NZDUSD -0.117% to 0.6001, 10y NZGB -5.3bp to 4.513%.

The People’s Bank of China also announced other targeted rate-based measures to support households and consumption. There was a 500bp cut (to 0%) in the required reserve ratio for automotive finance companies and financial leasing companies. The interest rate on personal housing provident fund loans will be reduced by 0.25%, effective May 8, the interest rate on the first home with a term of more than five years will be reduced from 2.85% to 2.6%, and the interest rate of other maturities will be adjusted simultaneously. China also launched or expanded multiple liquidity facilities to support the real economy. Beijing has increased the re-lending quota for scientific and technological innovation by CNY 300bn, from the current CNY 500bn to CNY 800bn; it will set up a CNY 500bn re-loan for service consumption and pensions, and guide commercial banks to increase credit support for service consumption and pensions; increase the amount of re-lending to support agriculture and small enterprises by CNY 300bn. To support assets and markets, China will provide low-cost re-lending funds to purchase science and technology innovation bonds, and cooperate with local governments and market-oriented credit enhancement institutions to share the risk of partial default losses of bonds through diversified credit enhancement measures such as joint guarantees. Finally, to support markets, authorities have decided to combine the CNY 500bn of Securities, Funds and Insurance Companies Swap Facility (SFISF) and the CNY 300bn quota of stock repurchase and re-lending, with a total quota of CNY 800bn. CSI 300 +0.606% to 3831.63, USDCNY -0.102% to 7.2264, 10y CGB +1.3bp to 1.64%.

Taiwan’s Consumer Price Index (CPI) in April rose 0.27% from March, mainly due to seasonal increases in garment prices and entertainment services during the Tomb-Sweeping holiday, though falling fruit and fuel prices partially offset gains. Core CPI rose 0.56%. Year-on-year, CPI increased 2.03%, driven by higher food prices, especially fruit (+25.26%) and dining out (+3.48%), while prices for eggs, fuel and communication fell. Core CPI rose 1.66% annually. The Producer Price Index (PPI) decreased 0.96% month-on-month but rose 0.93% year-on-year. Import and export prices in USD terms declined both monthly and annually, reflecting broader trade-related cost trends. TAIEX 0.116% to 20546.49, USDTWD -0.106% to 30.285, 10y TGB -1.5bp to 1.525%.

Philippines labor market remained stable in March. The unemployment rate stood at 3.9%, consistent with the previous year, indicating steady job availability. The employment rate was 96.1%, unchanged from the same period in 2024. However, underemployment rose to 12.3%, up from 11.2% in March 2024, suggesting that more employed individuals are seeking additional work or longer hours. The labor force participation rate was 65.2%, slightly higher than the 64.8% recorded a year earlier, reflecting increased engagement in the labor market. These figures suggest a resilient employment landscape, though the uptick in underemployment points to ongoing challenges in job quality and adequacy. PSEi +0.728% to 6465.45, USDPHP +0.374% to 55.408, 10y PHGB +4.7bp to 6.24%.

Germany’s manufacturing sector experienced a notable rebound in March, with new orders increasing by 3.6% month-on-month, seasonally and calendar adjusted, according to provisional data from the Federal Statistical Office (Destatis). Excluding large-scale orders, the rise was 3.2%. Year-on-year, orders were up 3.8%. Significant contributions came from the pharmaceutical industry (+17.3%), electrical equipment (+14.5%), and other transport equipment (+13.0%). Capital goods orders grew by 3.7%, while intermediate and consumer goods saw increases of 2.5% and 8.7%, respectively. Foreign demand rose by 4.7%, with euro area orders up 8.0% and non-euro area by 2.8%; domestic orders increased by 2.0%. Additionally, manufacturing turnover rose by 2.2% compared to February 2025. DAX +0.117% to 23276.89, EURUSD -0.009% to 1.1369, 10y Bund +0.4bp to 2.544%.

Germany’s construction sector downturn eased in April, with the HCOB construction PMI rising to a 26-month high of 45.1, up from 40.3 in March. Though still below the neutral 50.0 mark, this reflects a slower decline in activity, particularly in commercial and civil engineering segments. Housing remained the weakest area but recorded its softest fall in over a year. New orders dropped at a much slower rate, marking one of the largest month-on-month improvements in the survey’s history, though high prices and customer uncertainty persisted. Employment declined slightly, reversing March’s near-stability, while purchasing and subcontractor usage continued to contract at a milder pace. Input costs rose modestly to a 14-month high. Despite a slight dip in sentiment, business confidence remains relatively firm and is at a 38-month high.

France’s Q1 2025 private payroll employment remained stable, recording a marginal increase of 9,400 jobs (0.0%) compared to the previous quarter, which had seen a decline of 68,000 jobs (-0.3%). Despite this stabilization, employment levels were still 0.3% lower than in Q1 2024, equating to a reduction of 69,900 jobs year-on-year. These data suggest a tentative halt to the downward trend in private sector employment, although overall job numbers have yet to return to the figures observed a year earlier. CAC40 -0.443% to 7662.83, EURUSD -0.009% to 1.1369, 10y OAT +0.5bp to 3.264%.

Italy’s retail trade contracted in March. Seasonally adjusted data showed a 0.5% monthly decline in both value and volume. Compared to March 2024, retail sales value dropped 2.8%, with a steeper 4.2% fall in volume. All distribution channels experienced annual declines, including large-scale (-2.6%), small-scale (-3.1%), non-store (-4.7%), and online (-1.3%) retail. The non-food segment showed mixed results: while most categories declined, cosmetics (+1.8%) and pharmaceuticals (+0.6%) posted modest growth. Overall, the first quarter of 2025 registered a 0.2% decline in retail value and 0.5% in volume, indicating persistent weakness in consumer demand and broad sectoral slowdown. FTSEMIB +0.244% to 38654.5, EURUSD -0.009% to 1.1369, 10y BTP -0.3bp to 3.624%.

Sweden’s preliminary inflation data for April showed a continued easing in headline CPI, with the annual rate falling to 0.3% from 0.5% in March, and a modest monthly rise of 0.1%. The CPIF (Consumer Price Index with Fixed Interest Rate), which excludes direct interest rate effects and is closely watched by the Riksbank, remained unchanged at 2.3% year-on-year, with a 0.2% monthly increase. Meanwhile, CPIF-XE (excluding energy) rose to 3.1% from 3.0%, reflecting persistent underlying price pressures. These figures suggest a mixed inflation picture − headline rates moderating while core inflation remains elevated. Full CPI details for April will be released on May 14. OMX +0.089% to 2431.088, EURSEK -0.189% to 10.9026, 10y Swedish GB -1.3bp to 2.382%.

Eurozone and EU retail sales for March both fell by 0.1% month-on-month, following slight gains or stability in February. The euro area saw declines in food, drinks, tobacco and non-food products, though automotive fuel rose 0.4%. The EU posted similar trends, with food sales down 0.4% and fuel up 0.4%. Among member states, Slovenia, Estonia and Slovakia had the sharpest monthly declines, while Malta, Belgium and Croatia saw notable increases. Compared to March 2024, retail trade rose 1.5% in the euro area and 1.4% in the EU. Annual growth was strongest in Luxembourg, Bulgaria and Cyprus, with Slovakia, Poland and Italy reporting the steepest declines. Overall, the data reflect uneven consumer demand across the bloc. EuroStoxx 50 -0.174% to 5254.23, EURUSD -0.07% to 1.1362, BBG AGG Euro Government High Grade EUR 0bp to 2.813%.

Czech industrial production in March rose by 1.4% year-on-year and 0.4% month-on-month in real terms, reflecting a moderate rebound in output. Key contributors to this growth included the manufacture of motor vehicles, computers and electronic equipment. However, some sectors, such as metallurgy and pharmaceutical production, reported year-on-year declines. Total new industrial orders increased by 0.9% compared to March 2024, with domestic orders growing by 1.2% and foreign orders by 0.7%. Despite the overall positive trend, output remains uneven across industries, and growth rates are more modest compared to past recoveries. These figures suggest cautious optimism for the Czech manufacturing sector but reflect the economy before tariff announcements. Prague SE +1.103% to 2085.3, EURCZK +0.128% to 24.928, 10y CZGB +0.8bp to 4.103%.

The Czech trade balance of goods recorded a surplus of CZK 32.5bn in March, down CZK 8.0bn year-on-year. The decline was driven by reduced surpluses in fabricated metal products and electrical equipment, and a deeper deficit in electronics. However, stronger motor vehicle exports and reduced energy import deficits partially offset the drop. Trade with EU countries improved by CZK 5.8bn, while the non-EU deficit widened by CZK 12.3bn. Exports rose 6.0% and imports 8.8% year-on-year. Lithium-ion batteries were a key driver. Seasonally adjusted monthly trade declined slightly, while Q1 surplus rose to CZK 86.4bn.