Market Movers: Contrasts

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

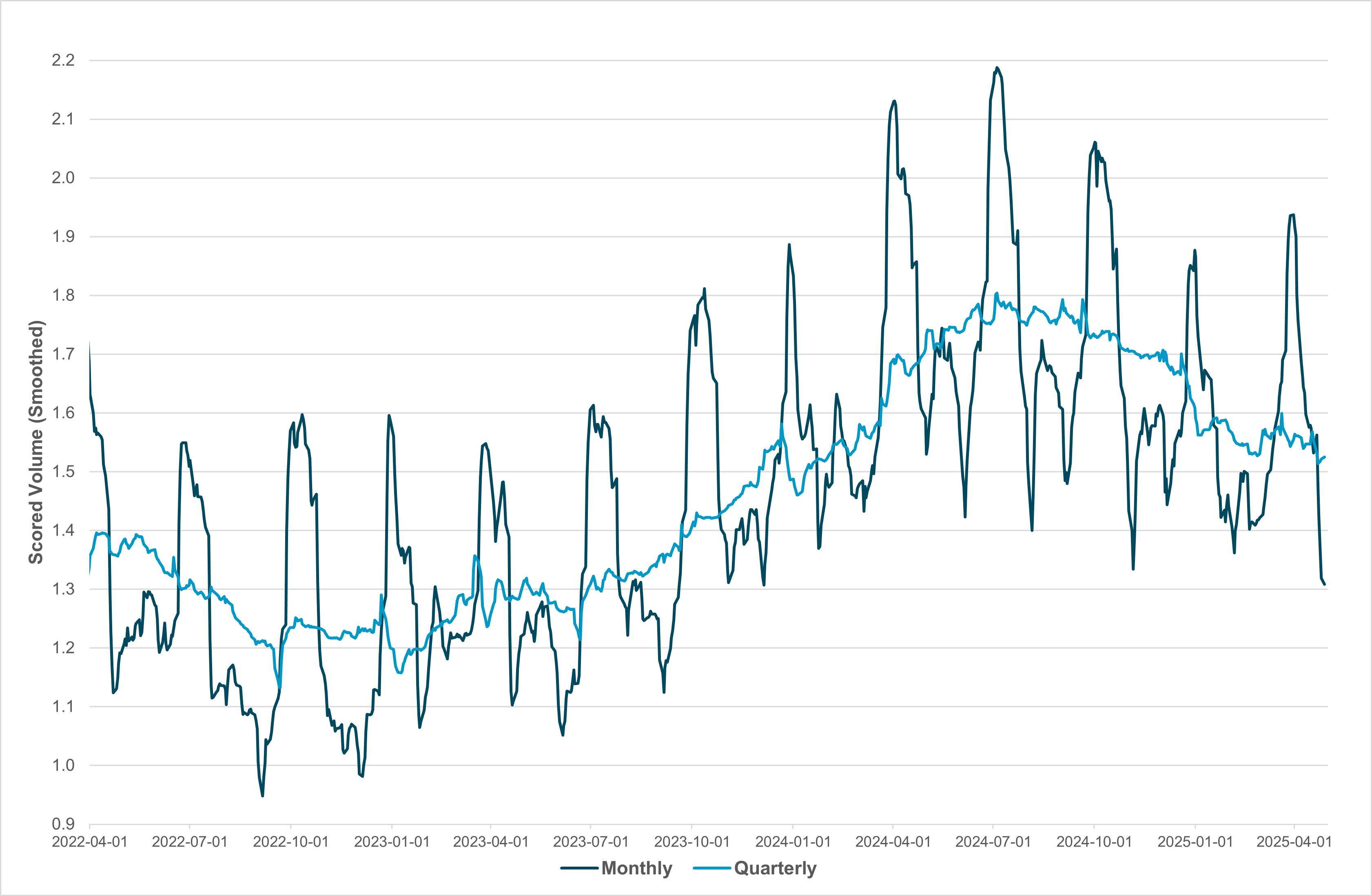

EXHIBIT #1: USD VOLUMES (AS A PROXY FOR MARKET FX VOLUMES), MONTHLY AND QUARTERLY SMOOTHED

Source: BNY

Looking at general dollar volumes as a proxy for FX price action, it is important to note that the most volatile periods this year were not the most “active” for markets. Volume spikes for our flows in March as the Q1 IMM flow surge reversed three straight quarters of volume declines. However, even with that spike, the trend decline has continued since the high point seen in Q3 2024. Markets are trading on event risk but nothing else changes. The Q1 tariffs on Canada and Mexico were a precursor for what could happen globally later, so asset managers were more active in their FX allocations in Q1. There were further adjustments triggered by geopolitics as Europe and NATO partners had to fundamentally reassess their own security arrangements, driving the surprise shift in Germany’s fiscal stance. However, the lack of a reversal in volumes in April points to a key general feature for our real money clients: they can afford to wait and ride things out. The current trend for FX is to hold tight as the U.S.’ trade policy remains highly volatile.

Risk sentiment mixed again as stronger Q1 growth in the Eurozone helps offset concerns about tariff pain in Q2. Overnight, China’s PMI missed expectations, leaving stocks there weaker ahead of the May Day holidays. The mood for month-end is one of wait and see, with economic data back in the driver’s seat as U.S. GDP is expected to contrast sharply with Europe. The risk of a U.S. recession continues to drive, with a 1% rate easing mostly priced in for the Fed this year. But that isn’t enough for the U.S. President, who is pushing back on polling and urging greater tariff acceptance. The host of data on the overnight leaves many investors less confident about global growth being positive and lower inflation, with the German data on inflation seen as key as well as U.S. core PCE. For equities, we are in the heart of Q1 earnings reports, and the risk of misses by the big tech remains in play. Markets are ready for bad news, with the skew of risks to the downside, leaving any comfort from better-than-expected reports a potential stabilizer. For many, the barometer for contrasts will be the EUR today, as U.S. growth and hopes compete with European stability.

Eurozone Q1 GDP up 0.4% q/q, 1.2% y/y after 0.2% q/q – better than the 0.2% q/q expected. The pickup was supported by stronger domestic demand, driven by easing inflation, lower borrowing costs, renewed optimism following Germany’s agreement to loosen fiscal constraints, and expectations of increased defense spending in the coming months. These developments helped offset persistent concerns over volatile U.S. tariff policies. However, economic momentum may soften in the months ahead, as the implementation of new U.S. duties begins to weigh on EU exports, while heightened uncertainty dampens investment and household consumption. Among major economies, Germany expanded by 0.2%, while Spain and Italy outperformed with growth rates of 0.6% and 0.3%, respectively. In contrast, France and the Netherlands recorded more modest growth, both at just 0.1%. EuroStoxx 50 up 0.1%, EUR off 0.1% to 1.1375.

The Bank of Thailand delivered a back-to-back rate cut of 25bp to 1.75%, as expected. The central bank has walked backed from its February statement, which warned that cuts did not represent “an easing cycle.” The move was considered necessary due to the larger-than-expected tariffs imposed on Thailand, in addition to risks from domestic and regional growth weakness. We see this as a more decisive dovish step and expect further easing ahead but most likely in H2 2025, with a pause at the June meeting. Other points of note during the press conference include slower-than-expected Chinese tourism, possibly driven by idiosyncratic factors earlier in the year. Slowing tourism would also been seen as negative for the THB. In other data, Thai exports surged by 17.7% y/y in March, generating a trade balance of $3.4bn. However, imports also increased and the overall trade balance, at $2.3bn, was slightly lower than expected. SET +1.002% to 1182.85, USDTHB -0.006% to 33.405, 10y TGN -0.3bp to 1.892%.

China April PMI Manufacturing fell back into contraction after two months of expansion. PMI manufacturing at 49.0 is the lowest since December 2023. The three key subcomponents were all lower. New orders back into contraction at 49.2 after two months of expansion while imports and new export orders plunged to 43.4, the lowest since April 2022 (42.9) and 44.7, the lowest since December 2022 (44.2). PMI non-manufacturing slowed from 50.8 to 50.4. Construction business activities sentiment dropped sharply from 53.4 to 51.9 while Services business activities continue to hover just above the 50 neutral zone at 50.1. The Caixin Manufacturing PMI also slowed to 50.4 from 51.2 – the seventh month of growth and beating expectations for contraction – with both input and output prices lower. Sentiment was weak, third worst since April 2012. Ability of China to wait out U.S. on tariffs talks not clear headed into the 5-day holiday period ahead. CSI 300 -0.119% to 3770.57, USDCNY +0.136% to 7.2615, 10y CGB -0.4bp to 1.628%.

French provisional inflation for April came in stronger than expected at 0.8% y/y. Consensus was for a 0.7% y/y reading. Statistics agency INSEE noted that “the increasing fall in energy prices should be partly offset by the rebound in food prices. Prices of services and manufactured products should follow the same trend as last month.” Meanwhile, March producer prices fell again (-1.1%m/m after -0.2%m/m in February). Producer prices continued to fall for products sold on the French market (-0.6%m/m after -0.4%m/m) and they fell back sharply for those intended for foreign markets (-2.6%m/m after +0.4%m/m in February). CAC40 +0.263% to 7575.72, EURUSD -0.141% to 1.1371, 10y OAT -3.2bp to 3.186%.

The KOF Institute says “outlook for the Swiss economy darkens” in the latest update of its economic barometer. The KOF Leading Indicator dropped sharply to 97.1 from a revised 103.2 in March. The KOF Institute notes that “in particular, the indicator bundle for manufacturing experiences a strong setback. Similarly, the indicator bundles for other services and hospitality are under downward pressure. Solely the level of the indicator bundle for financial and insurance services remains nearly unaltered.” SMI +0.333% to 12106.85, EURCHF -0.099% to 0.93903, 10y Swiss GB -3.5bp to 0.352%.

German April CPI – headline HICP expected to come in lower at 2.1% y/y, with a 0.4% m/m gain. However, the monthly figure was in line with or surprised to the upside for all key five state figures released overnight.

U.S. April ADP employment expected down to 115k from 155k – always a driver for expectations for the more important Friday NFP.

U.S. Q1 flash GDP expected -0.2% annualized q/q after +2.4% y/y, with focus on personal consumption expected 1.2% down from 4.0% while the price index core expected up 3.1% from 2.6% y/y. The key focus is on trade drag against inventories for 2Q outlooks.

U.S. March personal incomes expected up 0.4% after 0.8% while spending seen up 0.6% m/m after 0.4% m/m. March core PCE seen up 0.1% m/m, 2.6% y/y after 2.8% y/y. The key is real incomes for consumers.

U.S. March pending home sales expected up 1% m/m, -5.7% y/y after +2.0% m/m, -7.2% y/y. The role of rates on home sales still key focus.

Mood: Sentiment continues to trend lower as sentiment in equities remains highly variable amid lack of tariff progress.

FX: APAC performs strongly with AUD, CNY, JPY and THB leading flows. USD shifts back into funding status as month-end risk-positive flows undermine the greenback.

FI: APAC outflows continue as expectations for easing continue to rise in the region. Japan and China face sales, indicating yield sensitivity remains strong, especially for the most liquid markets.

Equities: Limited inflows across markets, but the U.S. and China find some support heading into month-end, most likely related to rebalancing.

“An appeal to fear never finds an echo in German hearts.” – Otto von Bismarck

“The greater the contrast, the greater the potential. Great energy only comes from a correspondingly great tension of opposites.” – Carl Jung

U.K. April Lloyds Business Barometer dropped sharply from 49 to 39 while price expectation rose to new highs at 68. The current economic optimism level fell to 28, the lowest in three months and the net monthly change of -13 for the index is the biggest over the last six months, underscoring the impact of the rise in global economic uncertainty. The U.K.’s Nationwide House Price index dropped by 0.6% m/m in April, the biggest decline since August 2023. The report noted that this was to be expected as a soft market follows “the pattern typically observed following the end of a stamp duty holiday. the biggest decline since August 2023. The report’s publishers noted that this was to be expected as a soft market follows “the pattern typically observed following the end of a stamp duty holiday.” However, the report noted that prospects for house prices remain favorable despite wider global uncertainties, as this is being helped by real wage growth and expected rate cuts from the Bank of England. FTSE 100 -0.035% to 8460.54, GBPUSD -0.246% to 1.3376, 10y gilt -4bp to 4.44%.

French GDP expanded by 0.1% q/q, reversing the decline from Q4 2024, but growth composition was not robust, with expansion driven by inventories, whereas domestic demand was relatively poor. The drag from net trade was also very large and underscores the challenges for the export sector in Europe up ahead. Despite the mixed results, French Finance Minister Lombard said the country was not planning on new taxes and France is on track to meet the 2025 growth forecast. CAC40 +0.263% to 7575.72, EURUSD -0.141% to 1.1371, 10y OAT -3.2bp to 3.186%.

French consumer spending registered a sharp contraction in March of -1.0% m/m, well below expectations of a small rebound of 0.1%. The annualized figure dropped to -1.5% y/y, the lowest level since October 2023. The sharp drop in energy prices contributed to the headline number, but there were declines in every single headline component, especially durable goods, which fell by 1.9% y/y, led by a 3.0% y/y decline in automobile sales.

Italian inflation was in line with expectations at 0.2% m/m, 2.0% y/y. HICP softened to 0.5% m/m (consensus: 0.6% m/m) and the annualized rate was unchanged at 2.1%. GDP for Q1 was stronger than expected at 0.3%. Istat – the statistical agency – indicated that domestic demand supported the recovery. FTSEMIB -0.498% to 37685.97, EURUSD -0.079% to 1.1378, 10y BTP -3.4bp to 3.573%.

South Korea March industrial production posted strong 2.9% m/m gain after 1.4% m/m in February but slightly lower in year-on-year term at 5.3% vs. 7.1% in February 2025. Construction sector remains the main drag at -2.7% m/m, -14.7% y/y. Elsewhere, March Cyclical Leading Index posted a second monthly gain at 0.2% m/m vs. 0.1% in February 2025. In year-on-year terms, cyclical leading y/y turned higher in March at 0.1% after a long downtrend since Q2 2024. A tentatively positive sign of stabilization of growth ahead after Q1 GDP contraction at -0.2% q/q, -0.1% y/y. KOSPI -0.343% to 2556.61, USDKRW +0.918% to 1421.2, 10y KTB +2bp to 2.61%.

Japan's March industrial production dropped -1.1% m/m, -0.3% y/y. Looking into the breakdown, motor vehicles, electrical machinery, and information and communication electronics equipment industries production declined, with increases seen in production machinery and transport equipment (excluding motor vehicles). Japan March retail sales dropped on the month at -1.2% m/m (February: 0.4% m/m) but improved in year-on-year terms at 3.1% y/y from 1.3%, mainly due to lower motor vehicles sales (-4.8% m/m) and fuel costs (-3.0% m/m). Nikkei +0.573% to 36045.38, USDJPY -0.357% to 142.84, 10y JGB -0.2bp to 1.317%.

Japan March housing starts surged by 39.1% y/y, well above expectations of 1%, surpassing 1mn units on an annualized basis. This was the strongest print since the end of the global financial crisis in 2009. There are evidently seasonality factors involved but the pick-up in activity suggests that the overall domestic housing investment picture in the country is volatile, but trend improvement is becoming evident over the past 12 months after consistent contraction 2023. The gains were particularly strong in starts for rental-designated housing.

Japan’s February Leading Index dipped to 107.9 from 108.2 in January, largely due to a decline in the lagging index from 111.3 to 110.8. Policymakers could be particularly concerned about the decline in new job offers, which fell by 4.1 points, by far the biggest decline over the past six months. However, machinery orders registered healthy growth of 2.8 points, which suggests the impact of tariffs has been muted so far.

New Zealand April ANZ Business Confidence plunged from 57.5 to 49.3, while activity outlook eases from 48.6 to 47.7. More positively, past own activity (the best GDP indicator in the survey) jumped 10 points from 1 to 11, while past employment jumped 8 points, from -6 to 2. Cost expectations rose to highest since September 2023. Note that NZD has been dislocated from ANZ business confidence since Q4 2024. NZX 50 -1.016% to 11903.31, NZDUSD -0.135% to 0.5923, 10y NZGB -3.2bp to 4.444%.

Australia March headline CPI and trimmed mean CPI stood unchanged at 2.4% y/y and 2.7% y/y, respectively. On the quarter, Q1 CPI stood at 0.9% q/q, 2.4% y/y vs. 0.2% q/q, 2.4% y/y in Q2 2024, while trimmed mean CPI eased from 3.3% y/y to 2.9% y/y. Looking into the breakdown, transportation dropped the most, to -1.9% y/y against higher, recreation, at 2.7% y/y, and food prices, at 3.3% y/y, while the housing component was unchanged at 1.8% y/y. Market adjusted front-end RBA pricing with strong CPI releases, but still pricing in a cut in May. ASX +0.006% to 4577.38, AUDUSD +0.11% to 0.6391, 10y ACGB -2.5bp to 4.165%.

Australia March private sector credit steady at 6.5% y/y but further rise in aggregate housing credit at 5.7%. Housing market remains hot in Australia with housing investor credit growth at 5.71% y/y surpassing housing owner occupied at 5.7% y/y.

Philippines March exports rose 5.9% at $6590mn and imports up 11.9% to $10720mn, leaving a trade deficit of $4128mn. Exports to the U.S., China and Japan grew at 12.8% y/y, 14.5% and 17.0% y/y, respectively, while exports to China declined by -9.8% y/y. PSEi +1.644% to 6354.99, USDPHP +0.528% to 55.86, 10y PHGB -1.9bp to 6.184%.

Polish Preliminary CPI for April was in line with expectations at 0.4% m/m, but the annualized print fell to 4.2% (consensus: 4.3%). This could open the way for easing at the next NBP meeting as several MPC members had stated that a downside surprise in inflation was necessary for rate cuts. Headline inflation came in at 0.8%m/m while fuel prices dropped by 1.7% m/m, after a 2%m/m drop in March. WIG -0.758% to 100051.9, EURPLN -0.257% to 4.2781, 10y PGB -0.4bp to 5.218%.

The Central Bank of Chile held policy rates unchanged at 5%, in line with expectations. Policymakers warned that “changes in global trade policy have deteriorated the prospects of global growth,” but there was some degree of confidence on domestic inflation. While the central bank warned that price growth “will remain at high levels in the immediate future, its recent evolution and that of its main determinant” reaffirmed the prospects of decline in inflation to the 3% target over the next 12 months. CSM Select +0.909% to 8059.4, USDCLP -0.308% to 946.75, 10y CGB +2bp to 5.72%.