Market Movers: Cloudy

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

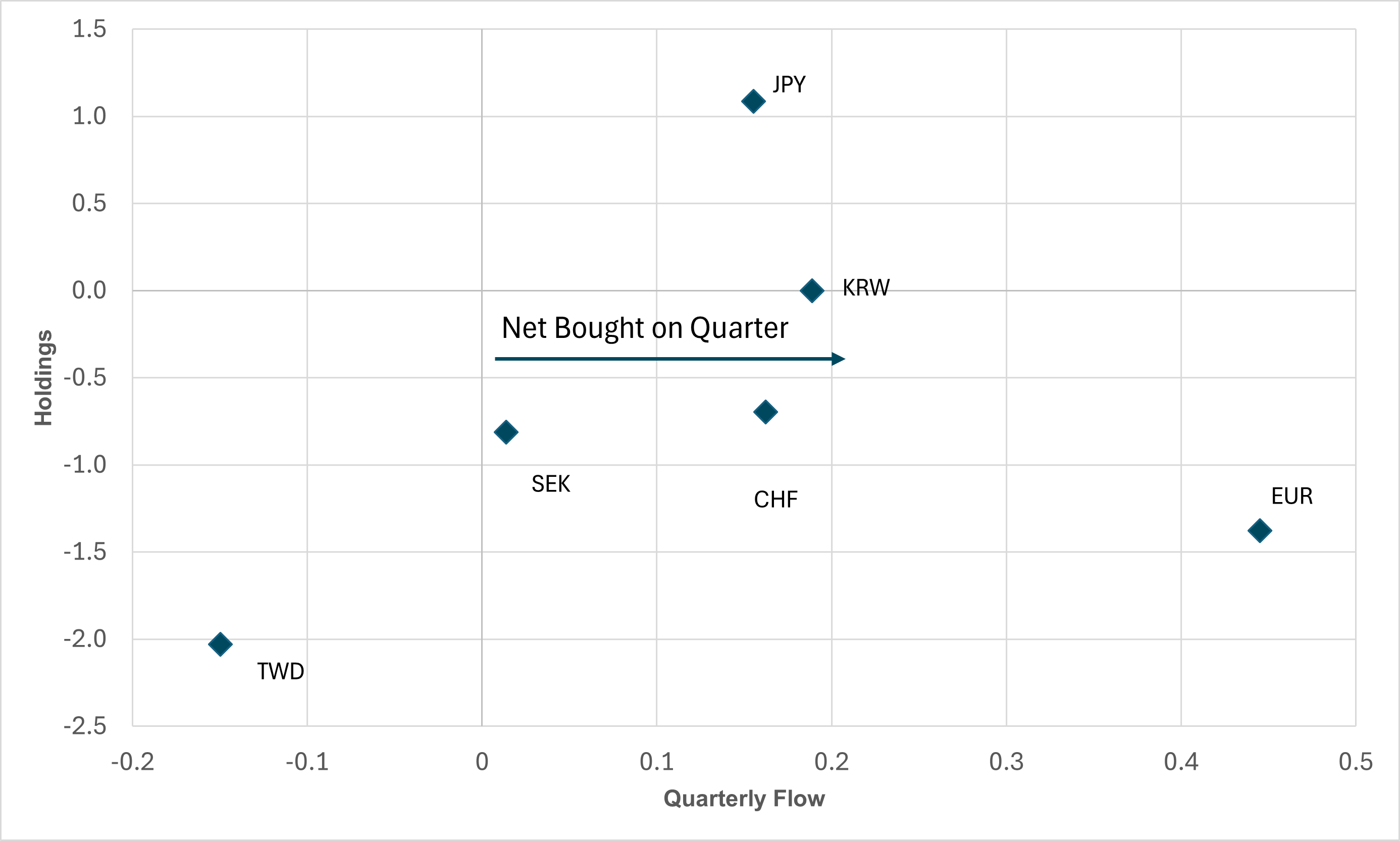

EXHIBIT #1: LOW-YIELDING GOODS EXPORTERS REDUCED CROSS-BORDER UNDERHELD POSITIONS OVER PAST QUARTER

Source: BNY, iFlow

Over the past few trading sessions, TWD has been the center of attention. The severe moves in the currency triggered monitoring of other APAC nations. In April, the market looked at a similar scenario for the SNB after extreme moves. Overall, it has been a very good period of flow for “funders,” given our iFlow Carry index recently moved to multi-year lows. High yielders are still struggling, and considering the moves in TWD, it is now worth asking whether funders can improve further, with mean reversion in risk appetite towards a positive carry environment, the next logical move. Over the past month, only CHF, SEK, and TWD have been net bought. Furthermore, only TWD is still well below the -1.0-equivalent level of flows over the past year, so its outsized moves are understandable. On the other hand, the JPY has set a template for moving back into over-held form from a strongly under-held position. Expect divergent carry outcomes ahead.

Risk sentiment is mixed as markets grapple with political risks again. APAC rallied on hopes of trade deals, slightly better China holiday spending offsetting clear PMI weakness and stronger FX across the region – all of which added to easing expectations. The CNY trades at 7.2105 after five days off, back to November 2024 lows for the dollar. EMEA retreats amid continued political uncertainty in Germany, casting doubt on faster fiscal spending, while the Romanian vote yesterday further clouds EU solutions for banking, labor, and defense. With weaker economic data on services PMIs, there are fears that rate cuts won't be sufficient to fix what ails Europe. The focus in the U.S. session will likely come from the Trump-Carney meeting on trade tariffs, where there is little expectation for a fast deal. Ahead of the meeting, we get the U.S. trade deficit for March, which was key to the negative GDP in Q1. How this mixes with the markets will be interesting. One standout factor is why the current rounds of FX intervention in Asia haven’t led to more U.S. bond buying. The dollar weakness trend is extending, and the move suggests other factors could extend in equities even as the rally up in equities stalled for the U.S. yesterday. Correlations and volatility remain uneven for any trading model, making it clear that the damage done in April hangs over May despite the bounce-back in risk. Behind the mood is the nagging fear that bad news for the economy won’t be met by any shift from the Trump administration on policy or from the Fed on easing. Further, good news has been insufficient to offset growth and inflation fears. Markets remain cloudy and reflect a dampening of risk appetites everywhere.

In a proposal aimed at expediting negotiations on a bilateral trade deal expected by fall this year, India has proposed zero tariffs on steel, auto components, and pharmaceuticals up to a certain quantity of imports in its trade negotiations with the U.S. on a reciprocal basis. Beyond this threshold, imported industrial goods would attract the regular level of duties, according to sources familiar with the current discussions. The offer was made by Indian trade officials visiting Washington late last month to expedite negotiations on a bilateral trade deal expected by fall this year, the people said. SENSEX -0.277% to 80572.74, USDINR -0.185% to 84.4037, 10y INGB +2.2bp to 6.347%.

Taiwan’s Central Bank announced that foreign exchange reserves rose to $582.83bn in April from $578.02bn in March. It also confirmed it had intervened in the market to buy dollars during the month. Investment gains, the central bank’s intervention, and exchange rate changes against the dollar are among factors affecting April forex reserves. The central bank also estimated that as of the end of April, external holdings of stocks and bonds amounted to US$721.9bn on a marked-to-market —equivalent to 124% of reserves. Given the recent moves, these figures have probably changed materially. Meanwhile, Taiwan’s financial regulator also highlighted that no insurers have asked for official support to cope with the FX swings, and major insurers have good solvency ratios. TAIEX -0.051% to 20522.59, USDTWD -0.4% to 30.218, 10y TGB -2bp to 1.53%.

Speaking at a digital currency event in Zurich, Swiss National Bank (SNB) Chairman Martin Schlegel emphasized the sharp appreciation of the Swiss franc, stating it has “really strengthened a lot.” Schlegel warned that the appreciation could impact inflation and exports. Further, he reiterated that the central bank stands ready to act in the foreign exchange market if necessary, and did not rule out zero or negative rates. Saying that “no one likes” negative rates, the SNB will act if necessary. His remarks suggest a heightened willingness to intervene, reflecting a shift in tone amid persistent market speculation. SMI +0.141% to 12250.28, EURCHF -0.356% to 0.93365, 10y Swiss GB +0.4bp to 0.354%.

China’s Caixin Services PMI fell to 50.7 in April from 51.9 in March, marking a seven-month low and missing expectations for a broadly unchanged print of 51.8. The slowdown reflects weakening domestic demand and rising pressure from the U.S. tariffs. New business growth slowed sharply, employment declined again, and business confidence fell to one of its lowest levels on record. Despite rising input costs, firms cut prices for a third straight month. The broader Composite PMI, which includes both manufacturing and services, also eased to 51.1 from 51.8. This points to only modest private sector growth as global trade uncertainty weighs on efforts to boost consumption growth amid economic rebalancing. CSI 300 +1.007% to 3808.54, USDCNY +0.8% to 7.2137, 10y CGB -0.2bp to 1.626%

In the final April PMIs release, Eurozone economic growth slowed, with the Composite PMI easing to 50.4 and the Services PMI down to 50.1—both indicating marginal expansion. Services nearly stagnated, while manufacturing output rose at its fastest pace in over two years. Demand remained weak, with new orders falling for the 11th straight month. Employment grew modestly, but only in services, as manufacturing jobs declined. Input cost and output price inflation eased, though they remained elevated. Business confidence dropped to an 18-month low. Among major economies, France contracted, while Ireland led growth, followed by Spain, Italy, and Germany with minimal expansion. EuroStoxx 50 +0.004% to 5283.28, EURUSD +0.203% to 1.1338, BBG AGG Euro Government High Grade EUR unchanged at 2.814%.

U.S. President Trump meets Canadian PM Carney to discuss trade at 11.45 am at the White House – expectations are low for a deal given the complication of USMCA already covering most of the trade

U.S. March final trade deficit expected to be $137.2bn after $122.7bn, with focus on services given the Hollywood tariff risks ahead. The market expects record trade drag.

U.S. Treasury sells $42bn in 10Y notes – focus will remain on foreign direct buying

Canada April Ivey PMI expected 50.2 from 51.3, with a focus on manufacturing risks and further contraction due to tariffs.

Brazil April services PMI was expected to be 52.2 from 52.6, with an ongoing slowdown linked to higher rates expected with focus on prices and orders.

Mood: iFlow Mood stabilizes but remains in risk-off zone, with continued demand for sovereign bonds, while near neutral equities flows.

FX: Active G10 with large USD outflows against significant AUD, GBP inflows, as well as EUR. USD scored holding drifted further into the under-held zone while further reduction of the over-held condition in JPY.

FI: Mixed demand globally, with demand seen in U.S. Treasurys and Brazilian government bonds, while selling pressure continues in Chinese and Australian bonds

Equities: G10 and LatAm equities were broadly sold, most in Sweden and Mexican equities. APAC and EMEA equities flows were mixed, with notable buying flows in Polish equities.

“A grey day provides the best light.” – Leonardo da Vinci

“When it’s foggy in the pulpit, it’s cloudy in the pew.” – Cavett Robert

Australian household spending fell 0.3% in March 2025 (seasonally adjusted), reversing February’s rise and marking the first monthly decline in six months. The drop was partly due to ex-tropical cyclone Alfred, which disrupted activity—especially in Queensland, where spending fell 1.3%. Nationally, transport and health spending declined by 3.9% and 3.3%, respectively, while Queensland food spending rose 2.9% due to stockpiling. Household spending volumes were flat for Q1, suggesting no GDP contribution. Annual growth slowed to 3.5%, highlighting persistent consumer caution amid cost-of-living pressures. Australian building approvals fell sharply in March, with total dwelling approvals down 8.8% to 15,220 units (seasonally adjusted). A 15.1% drop led the decline in approvals for apartments and townhouses (private sector dwellings excluding houses). In comparison, private house approvals fell by 4.5% to 8,804 units. The total value of residential buildings dropped 7.6% to $8.98 billion. In contrast, non-residential building approvals surged 46.0% to $6.61 billion, reflecting strength in commercial and infrastructure development. The data highlight continued weakness in new housing supply amid cost pressures and high interest rates, despite strong population growth and demand – the dominant topic in recent elections. ASX +0.394% to 4670.71, AUDUSD -0.093% to 0.6462, 10y ACGB +6.3bp to 4.333%.

Philippines April CPI was softer than expected , falling by 0.4% m/m and pushing the annualized figure to 1.4%y/y – the lowest since 2019. Food prices only increased by 0.9% y/y, while transport costs fell further to -2.1% y/y, undoubtedly helped by falling fuel costs, which continue to exert downward pressure on global inflation prints. However, in a sign that domestic demand remains robust, prices for household consumption continue to grow at a healthy clip, led by education, which increased by 4.2% y/y. PSEi +0.929% to 6418.69, USDPHP +0.279% to 55.615, 10y PHGB -0.5bp to 6.194%.

Singapore April PMI rose from 52.7 to 52.8 with new orders expanding at the fastest pace in six months, while future output index fell to a 26-month low. In terms of prices, the average charges fell for the first time since early 2021, reflecting the softer increase in cost. However, S&P warned that “That said, anecdotal evidence pointed to further signs of front-loading of goods orders ahead of tariffs while business sentiment and pricing powers were clearly affected by concerns over the outlook for trade and global growth.” STI +0.156% to 3859.09, USDSGD -0.217% to 1.2921, 10y SGB -1.2bp to 2.485%.

Thailand’s CPI fell 0.22% year-on-year in April 2025, the first negative reading in over a year, driven by lower energy prices and increased food supply. Core inflation rose 0.98%, indicating stable underlying price trends. The data came below expectations and remains outside the Bank of Thailand’s 1–3% target range. The central bank recently cut interest rates to 1.75% and lowered its 2025 GDP growth forecast to 2.0% amid global trade concerns. The Commerce Ministry stressed that the drop doesn’t signal deflation, and plans to revise its inflation forecast range downward. The figures support continued monetary easing to aid economic recovery. SET -0.208% to 1196.49, USDTHB +0.802% to 32.8, 10y TGN +2.1bp to 1.898%.

Swiss Secretariat for Economic Affairs (SECO) data indicate Swiss unemployment fell to 2.8% in April, down from 2.9% in March. Despite concerns over the sharp appreciation of the franc and potential hit to external demand in goods and services, the labor market remains tight. SECO highlighted that there was a 3.9% decline in vacancies on the month and a 1.6% decline compared to the same month last year. The level of individuals on unemployment benefits fell by 21.8% on a quarterly basis. SMI +0.141% to 12250.28, EURCHF -0.356% to 0.93365, 10y Swiss GB +0.4bp to 0.354%.

Sweden’s services PMI fell to 48.4 from 49.3 for April, its second straight month below the 50 threshold, indicating contraction. Employment, business volume, and new orders all declined, with the jobs subindex marking its ninth month under 50. The composite PMI dipped to 50.0, as industrial growth was offset by services weakness. Input price pressures eased for the third straight month. Sluggish demand, low construction activity, and global trade tensions continue to weigh on the sector, mirroring similar slowdowns in the eurozone, U.S., and U.K. Eurozone PPI. OMX -0.776% to 2445.628, EURSEK -0.112% to 10.9458, 10y Swedish GB +0.5bp to 2.392%.

Spain’s registered unemployment fell by 67,420 individuals in April, bringing the total to 2,512,583—the lowest April figure since 2008. This represents a year-on-year decrease of 153,782 unemployed persons. Youth unemployment (under 25) saw the most significant drop, decreasing by 20,095 individuals. Unemployment declined across all sectors, notably in services (down 42,067) and construction (down 4,902). All autonomous communities reported reductions. Female unemployment decreased by 34,422, and male unemployment by 32,998. The number of unemployed foreign nationals fell by 12,987. These figures indicate continued labor market recovery, supported by active employment policies and economic growth. IBEX 35 +0.41% to 13575, EURUSD +0.203% to 1.1338, 10y Bono +3.3bp to 3.201%.

Spain’s services sector continued to grow, but at a slower pace in April, with the Services PMI falling to 53.4 from March’s 54.7—its lowest since November 2024. Growth in activity and new orders weakened amid concerns over tariffs and a more challenging business climate. Foreign demand rose only slightly. Despite this, rising workloads supported continued—though softening—employment growth. Input costs remained high due to wage pressures and supplier price increases, often tied to tariffs, prompting firms to raise their prices. Business confidence dropped to its lowest since November, as uncertainty around U.S. trade policy tempered optimism about future activity.

Germany’s services sector fell into contraction, with the Final Services PMI dropping to 49.0 from 50.9—the lowest in 14 months—amid weaker demand and tariff-related uncertainty. New business declined for the eighth straight month, though at a slower pace. Business sentiment hit a seven-month low, with optimism barely outpacing pessimism. Despite this, employment rose at the fastest pace in nearly a year. Input costs accelerated, due to rising wages, but output price inflation slowed as competition limited pricing power. The composite PMI slipped to 50.1, as services weakness offset stronger manufacturing output. DAX -0.11% to 23318.79, EURUSD +0.203% to 1.1338, 10y Bund +3.1bp to 2.548%.

Italy’s services sector grew at a faster pace in April, with the Services PMI rising to 52.9 from 52.0 in March. Stronger activity and new business volumes, driven by demand and new project wins, supported continued—though marginal—employment growth. Input and output cost inflation eased to 2025 lows but remained historically high. Despite the upturn, business sentiment dropped to its weakest in four and a half years, amid concerns over economic conditions and tariffs. International sales declined for the ninth month. The composite PMI also improved to 52.1, reflecting stronger services growth and near-stabilization in manufacturing. FTSEMIB +0.279% to 38582.9, EURUSD +0.203% to 1.1338, 10y BTP +3.2bp to 3.635%.

France’s services sector continued to decline in April, with the Services PMI falling to 47.3 in the final print from 47.9 in March—marking the eighth consecutive month of contraction. Business activity and new orders both declined at faster rates, reflecting weak domestic demand. Employment fell moderately as firms faced shrinking workloads and hiring challenges. Input cost inflation eased to a six-month low, and prices charged were nearly stable, with competitive pressure limiting increases. Despite a slight rise in business sentiment, confidence remained well below the historical average due to global uncertainty. Manufacturing grew modestly, but services drove the overall composite PMI down to 47.8. CAC40 -0.036% to 7725.11, EURUSD +0.203% to 1.1338, 10y OAT +3.5bp to 3.271%.

Insee data show France’s manufacturing output in March rose by 0.6%, following a 1.3% increase in February, marking the second consecutive month of growth. Overall industrial production grew by 0.2% in March, after a 1.0% rise in the previous month. Growth was primarily driven by strong performance in the manufacture of transport equipment, which increased by 2.1%, and machinery and equipment goods, which rose by 1.5%. However, the energy sector experienced a 1.2% decline, limiting the broader gains. Compared to March 2024, manufacturing output increased by 1.8%, while total industrial production increased by 1.2%. These year-on-year improvements suggest that the French industrial sector is recovering, supported by strengthening demand and improvements in supply chain conditions. Nevertheless, the decline in energy output highlights persistent structural and external challenges that continue to weigh on certain parts of the industrial economy. CAC40 -0.036% to 7725.11, EURUSD +0.203% to 1.1338, 10y OAT +3.5bp to 3.271%.

April 2025 South African whole economy PMI signaled a turning point, with business conditions stabilizing at a neutral 50.0 after a prolonged contraction. Modest gains in output, new orders, and employment suggest early recovery momentum, especially in services and retail. Supplier delivery times improved for the first time since mid-2023, easing operational pressures. However, currency depreciation sharply drove input costs, particularly in imported goods, lifting overall inflation. While purchasing activity picked up, business confidence weakened due to political uncertainty and global trade tensions, despite 40% of firms still expecting growth over the coming year. JSE TOP40 +0.21% to 84721.7, USDZAR +0.115% to 18.2493, 10y SAGB +1.1bp to 10.631%.

Czech inflation registered a surprise monthly drop in April of -0.1% m/m, pushing the annualized rate to 1.8% y/y – the first time in seven years inflation has fallen below 2.0%. The drop was led by headline items such as food and energy, but goods prices declined by 0.3% m/m. Overall energy prices are now down 6.3% y/y. In contrast, services inflation remains high at 4.7%, pointing to some degree of ongoing labor market tightness, which could prove challenging for the Czech National Bank to navigate as cuts are sought in the region. Prague SE +0.757% to 2072.46, EURCZK -0.176% to 24.963, 10y CZGB -0.3bp to 4.094%.

U.K. services sector saw its first contraction in 17 months, with the Services PMI falling to 49.0 from 52.5 in March, as confirmed in the final April release. The downturn was driven by a sharp drop in new orders—particularly export sales, which declined at the fastest rate since February 2021—amid rising global uncertainty and U.S. tariff concerns. Employment continued to fall, with firms citing weak demand and rising payroll costs linked to National Living Wage increases. Input cost inflation surged to a 26-month high, prompting the most substantial rise in prices charged in nearly two years. Business confidence slumped to a 2.5-year low. FTSE 100 +0.375% to 8628.57, GBPUSD +0.196% to 1.3322, 10y Gilt +5.8bp to 4.566%.