Market Movers: Ceasefires

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 12 minutes

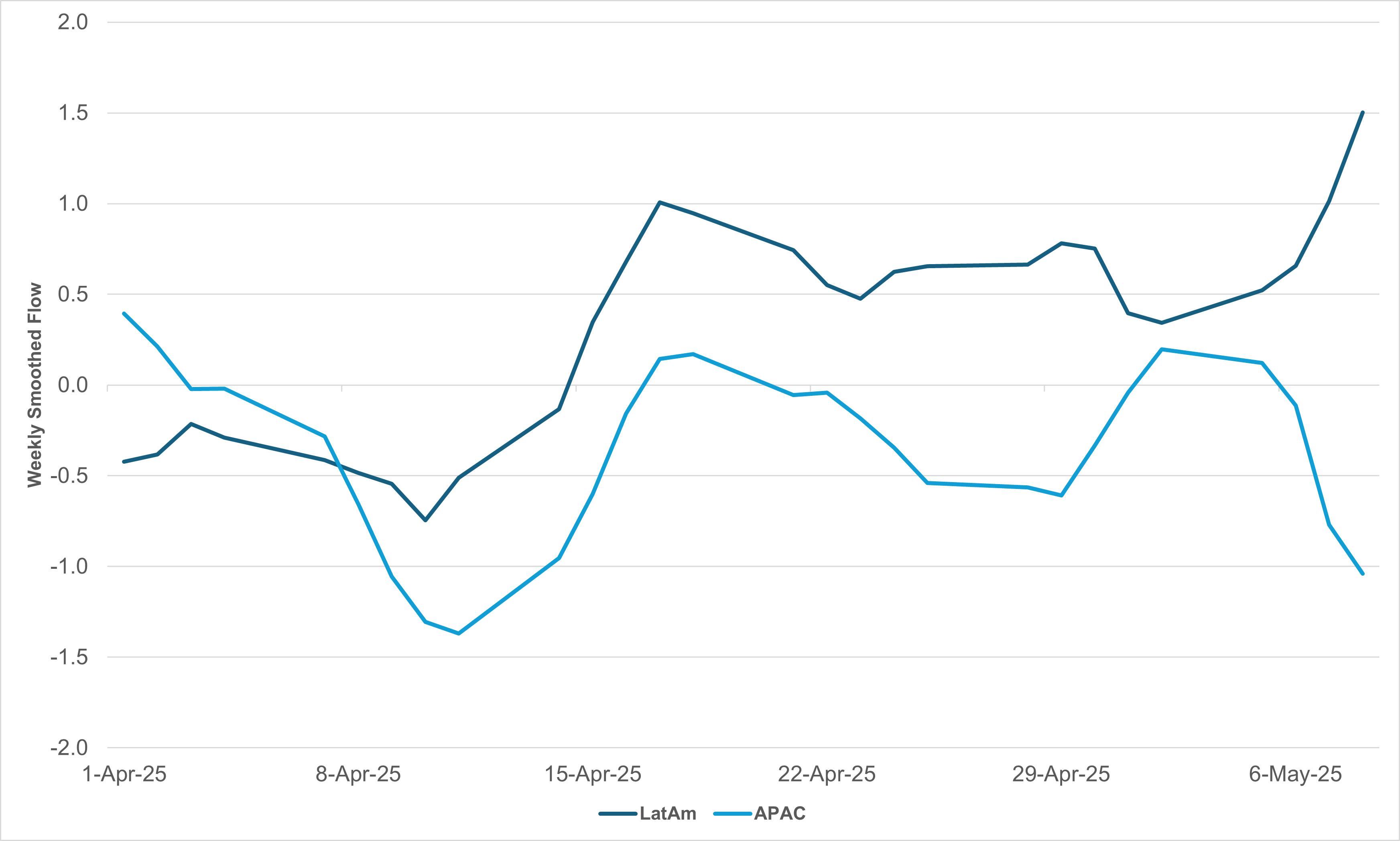

EXHIBIT #1: LATAM BONDS START TO OUTPERFORM APAC AS CARRY UNWIND ENDS

Source: BNY, U.K. Government

Several weeks ago, we highlighted that the unwind in carry trades appeared to be approaching extreme levels. Our iFlow Carry indicator showed statistically significant negative readings — historically a signal that positioning is stretched and a reversal may be near. We continue to express reservations over the ability of front-end yields to anchor currencies in the current environment, even if carry trades recover. Rate cuts are the preference for EM central banks, but only under the condition that dollar strength will be limited. However, after the tumult of April, the dollar is finding some footing so the risk is asymmetric against EM FX and hedge ratios will likely stay high. In the medium-term, we continue to expect more duration demand globally. Stagflation is an issue in developed markets, but we do not see a similar spillover into EM markets, as fiscal and labor supply dynamics are very different, comparatively. While there is no uniform flow into EM duration at present, we can see that there is very limited selling in LatAm, whereas the strong inflow into Brazil last week points to affirmation of policy credibility as monetary tightening offset the prospect of fiscal dominance. Mexico is also positive, notwithstanding ongoing trade risks with The Bank of Mexico (Banxico) decisions key this week. In contrast, APAC markets are pricing in different trade and balance of payments dynamics and the central banks are trying to delay such repricing. Coupled with low nominal rates, risk-reward is low for APAC duration, and this is now being reflected in flow divergence.

Risk sentiment flips to green with global trade and peace hopes leading equities and the U.S dollar. The reaction in bonds stands out with higher yields reflecting less recession fears and monetary policy cuts ahead. The move up in hopes for global growth leads to higher oil prices up 3% and gold down 3%. Markets are back to seeing 2025 upside risks, with the balancing act in rates. The 3% gains in U.S. stock market futures and 1% gain in the USD brings a 10bp jump in 2y U.S. yields and a 5.5bp move up in 10y with all eyes on 4.50% again. Of course, there is a time limit to the return of animal spirits across markets, as the U.S./China tariff talks have a 90-day pause, and ceasefires are different than peace deals. The ongoing path toward deals reduces tail risks but doesn’t eliminate them. Further, the balancing of inflation and growth will nag investors as policymakers continue to be hampered by uncertainty over what the terminal tariff rate really will be along, with how the final demand for U.S. consumers plays out. Overnight, CPI continued to be key with China low core inflation highlighting the need for fiscal change there. The day ahead brings little more than official comments on trade talks, more bravado on peace steps and less economic data. The U.S. budget deficit will be the only release and most expect ongoing trouble with April expected to show a 23% y/y increase, even with the better income tax take-in. Also in focus will be the amount of tariff revenue, $8.75bn in March, expected to be double that in April. The ability for U.S. exceptionalism to fit back into the narrative will require a cap in U.S. rates, with tame inflation, a lower dollar for better trade and further progress on international deals.

The United States and China reached a preliminary trade agreement in Geneva, aiming to de-escalate their ongoing tariff conflict. The accord includes a 90-day reduction in tariffs, with U.S. duties on Chinese goods decreasing from 145% to 30%, and China’s tariffs on U.S. imports dropping from 125% to 10%. Additionally, both nations agreed to establish a bilateral consultation mechanism to facilitate ongoing dialogue and address trade-related issues. U.S. Treasury Secretary Scott Bessent stated that there was also a possibility of purchasing agreements, and the U.S. had identified five or six “supply chain vulnerabilities” in place. U.S. Trade Representative Jamieson Greer noted that the toughest part of talks was repair of communications.” The agreement only covers reciprocal tariffs rather than sector-specific tariffs. CSI 300 +1.156% to 3890.61, USDCNY +0.325% to 7.2148, 10y CGB +4.3bp to 1.678%.

In its own statement, China’s Ministry of Commerce highlighted the latest Geneva trade talks with the U.S. as a constructive and meaningful turning point in stabilizing bilateral economic ties. Officials described the talks as “an important step toward resolving differences through equal dialogue,” and the joint statement emphasized a shared commitment to “mutual openness, continuous communication, cooperation, and mutual respect.” While acknowledging mutual tariff reductions, China underscored that its earlier countermeasures were “firm and legitimate responses” to Washington’s unilateral escalation. Beijing strongly condemned U.S. tariffs as actions that “severely disrupted the international economic and trade order” and reiterated that the latest agreement “creates conditions for further narrowing differences and deepening cooperation.” The newly-established consultation mechanism is seen as a platform for maintaining close communication and resolving trade concerns. China hopes the U.S. will now “thoroughly correct the erroneous practice of unilateral tariff hikes” and continue working toward a stable, sustainable economic relationship that benefits both countries and the global economy.

China headline CPI stayed in negative territory for the third straight month at -0.1% y/y with core CPI unchanged at +0.5% y/y. On the month, headline and core CPI were positive at +0.1% m/m and +0.2% m/m respectively. The biggest downside contributors are the drop of traffic and communication component at -0.3% m/m, -3.9% y/y and the easing of pork prices at -5% y/y. On aggregate, consumable inflation improved slightly to -0.3% from -0.9% y/y in February 2025, but remains in negative territory while services inflation registered 0.3% y/y. Overall, disinflation pressure continues in China, reflecting sluggish demand, which was also seen in the negative import growth. China April imports at -0.2% y/y or -5.2% ytd y/y.

U.S. President Donald Trump announced plans to sign an executive order introducing a “Most Favored Nation” policy to reduce U.S. drug prices. The proposal would cap drug prices at levels paid by the lowest-paying developed countries, potentially cutting costs up to 80%. Trump criticized pharmaceutical firms for inflated U.S. prices, blaming lobbying influence and global price disparities. The order revives a similar initiative from his first term, which was blocked by courts and later rescinded under the Biden administration. While specific details remain unclear —particularly regarding Medicare and Medicaid — the announcement triggered a drop in pharmaceutical stocks amid investor concerns. Trump framed the move as a necessary correction to ensure American consumers are no longer overcharged for essential medications compared to international peers. S&P Mini 2.549% to 5822.75, DXY +1.382% to 101.725, 10y UST +5.7bp to 4.435%.

U.S. Federal Reserve Board Governor Adriana Kugler speaks on the Economic Outlook at the National Association for Business Economics.

Bank of England’s Catherine Mann speaks on the Economic Outlook — she’s a crucial swing voter on the Monetary Policy Committee, though has recently been at odds with Governor Bailey in policy direction.

Mood: Sentiment is shifting with further normalization in iFlow Mood, led by the turnaround of equities flow along with ongoing demand for sovereign bonds.

FX: Large outflows in USD, JPY, AUD, SEK, ILS and TWD against strong inflows in CAD, GBP and EUR. Holdings of JPY and KRW dropped sharply but remain overheld while USD and ILS fell deeper into underheld territory.

FI: Brazilian government bonds stood out with strong buying flows, followed by U.S. Treasurys, against broad selling pressures in the rest, mostly, Chinese government bonds.

Equities: APAC region posted the buying against selling in Americas. EMEA equities flows were mixed with selling in DM vs. buying in EM. Globally, consumer discretionary is the only sector with outflows while consumer staples and real estate sectors posted the most inflows.

“Peace does not rest in charters and covenants alone. It lies in the hearts and minds of people.” – John F. Kennedy

“When envoys are sent with compliments in their mouths, it is a sign that the enemy wishes for a truce.” – Sun Tzu

The April 2025 U.K. Report on Jobs from S&P Global, KPMG and the Recruitment & Employment Confederation (REC) signalled a further weakening in the labor market. Permanent staff appointments declined for the 20th consecutive month, while temporary billings also fell slightly. Recruiters cited reduced client demand, budget pressures, and ongoing economic uncertainty. Overall job vacancies dropped, though the rate of decline was mild. Candidate availability improved sharply, driven by increased redundancies and fewer job openings. Pay pressures eased, with starting salary and temp wage growth slowing to their weakest pace since early 2021. Regionally, London saw the steepest decline in permanent hires, while the Midlands posted slight gains. REC’s Neil Carberry noted firms remain cautious, delaying hiring decisions until conditions improve. The data points to a subdued employment landscape, with employers prioritizing flexibility and short-term needs amid an uncertain economic outlook. FTSE 100 -0.093% to 8546.87, GBPUSD -0.962% to 1.3178, 10y Gilt +5.6bp to 4.623%.

Japan March current account balance eases from JPY 4060.7bn to JPY 3678.1bn. Elsewhere, Japan April Bank lending continues its downtrend. Lending including Trusts eased from 2.8% to 2.4% y/y and Lending excluding Trusts dropped from 3.0% to 2.6% y/y, both at the lowest since September 2022. Total Japan deposits and CDs amount outstanding slowed to 0.8% y/y, the least since mid-2007. Nikkei +0.376% to 37644.26, USDJPY -1.738% to 147.94, 10y JGB +8.6bp to 1.455%.

Japan’s Economy Watchers Survey for April 2025 showed a decline in sentiment. The seasonally adjusted Current Conditions Diffusion Index (DI) fell by 2.5 points to 42.6, reflecting weaker economic perceptions. Household-related DI declined due to a drop in housing activity, despite gains in food and beverage consumption. Corporate sentiment also worsened, particularly in non-manufacturing sectors, and employment-related DI slipped further. The Outlook DI dropped similarly by 2.5 points to 42.7, with all components — household, corporate, and employment — registering declines. On an unadjusted basis, the Current DI fell 3.2 points to 44.6 and the Outlook DI to 43.4. The report concluded that while some optimism persists due to expected wage hikes, overall recovery momentum is weakening amid rising prices and growing concern over the impact of U.S. trade policies. Nikkei +0.376% to 37644.26, USDJPY -1.738% to 147.94, 10y JGB +8.6bp to 1.455%.

South Korea first 10 days of May trade collapsed with exports down -23.8% y/y and imports down -15.9% y/y, resulting in a trade deficit of $1.7bn. The daily average exports fell -1% y/y vs. +0.3% y/y for the first 10 days in April. The sharp deterioration is partly due to reduced working days in 2025 (4 days vs. 6 working days in 2024). Chip exports rose 14% y/y. Exports fell for both China, -20.1% y/y, and U.S. -30.4% y/y. KOSPI +1.166% to 2607.33, USDKRW -1.615% to 1421.05, 10y KTB +4.7bp to 2.672%.

Turkey’s total turnover index (2021=100) for March across industry, construction, trade, and services rose by 33.4% year-on-year. Sector-specific annual growth was led by trade at 37.8%, followed by services at 35.9%, construction at 26.3%, and industry at 25.1%. On a monthly basis, the overall turnover index increased by 4.2%. Trade and industry saw notable monthly gains of 5.8% and 5.5% respectively, while services rose modestly by 0.5%. However, construction turnover declined by 4.6% compared to February. The data reflects strong year-on-year momentum in economic activity, especially in trade and services, despite some volatility in the construction sector on a month-to-month basis. The continued growth in turnover signals ongoing recovery and expansion across most sectors of the Turkish economy. BI 100 +2.942% to 9666.81, USDTRY -0.007% to 38.7619, 10y TGB -43bp to 34.3%.

Turkey’s trade sales volume index (2021=100) for March rose by 10.8% year-on-year, with wholesale and retail trade and repair of motor vehicles and motorcycles up 12.8%, wholesale trade up 11.1%, and retail trade up 9.2%. To better reflect household consumption demand, TurkStat has begun publishing retail trade sales excluding watches and jewellery, acknowledging that such items are often stores of value rather than consumption goods. On a monthly basis, total trade sales volume increased by 5.0%. Within that, wholesale trade rose sharply by 8.1%, and motor vehicles and motorcycles by 3.6%, while retail trade sales volume fell by 1.4%. The data suggests solid annual growth in trade activity, especially in wholesale segments, while retail performance showed a modest monthly pullback.

In a speech overnight, Bank of England Deputy Governor Clare Lombardelli stressed her focus remains on wages, which she sees as the key driver of underlying inflation, particularly through their impact on domestic services prices. Although inflation pressures are easing and justified a 25bp rate cut, she noted wage growth — at 5.9% — is still too high to be consistent with the 2% target. She highlighted that wage deceleration is gradual, and forward-looking indicators suggest further easing, but greater progress is needed. Lombardelli also introduced the Bank of England’s growing use of economic scenarios to manage uncertainty and improve policy robustness. Two key scenarios were examined: one featuring weaker demand from global trade tensions and another with persistent inflation due to sluggish productivity and heightened sensitivity to price shocks. These frameworks, she explained, are central to ongoing reforms and help assess how resilient current policy is under different outcomes. Policy remains restrictive at 4.25%. FTSE 100 -0.093% to 8546.87, GBPUSD -0.962% to 1.3178, 10y Gilt +5.6bp to 4.623%.