Market Movers: Causality

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

• China open to trade talks, wants U.S. respect and point person for any deal, while Q1 GDP in China rose 5.4% y/y and March economic data beat expectations.

• Semiconductor-linked stocks have fallen sharply due to U.S. export restrictions and drops in orders. Nvidia warns on $5.5bn charge, while ASML warns companies are unable “to quantify the impact from recent tariff announcements.”

• BOJ Governor Ueda warns U.S. tariffs have brought economy to “bad scenario”, may force policy response – May 1 meeting likely to see forecasts cut on growth.

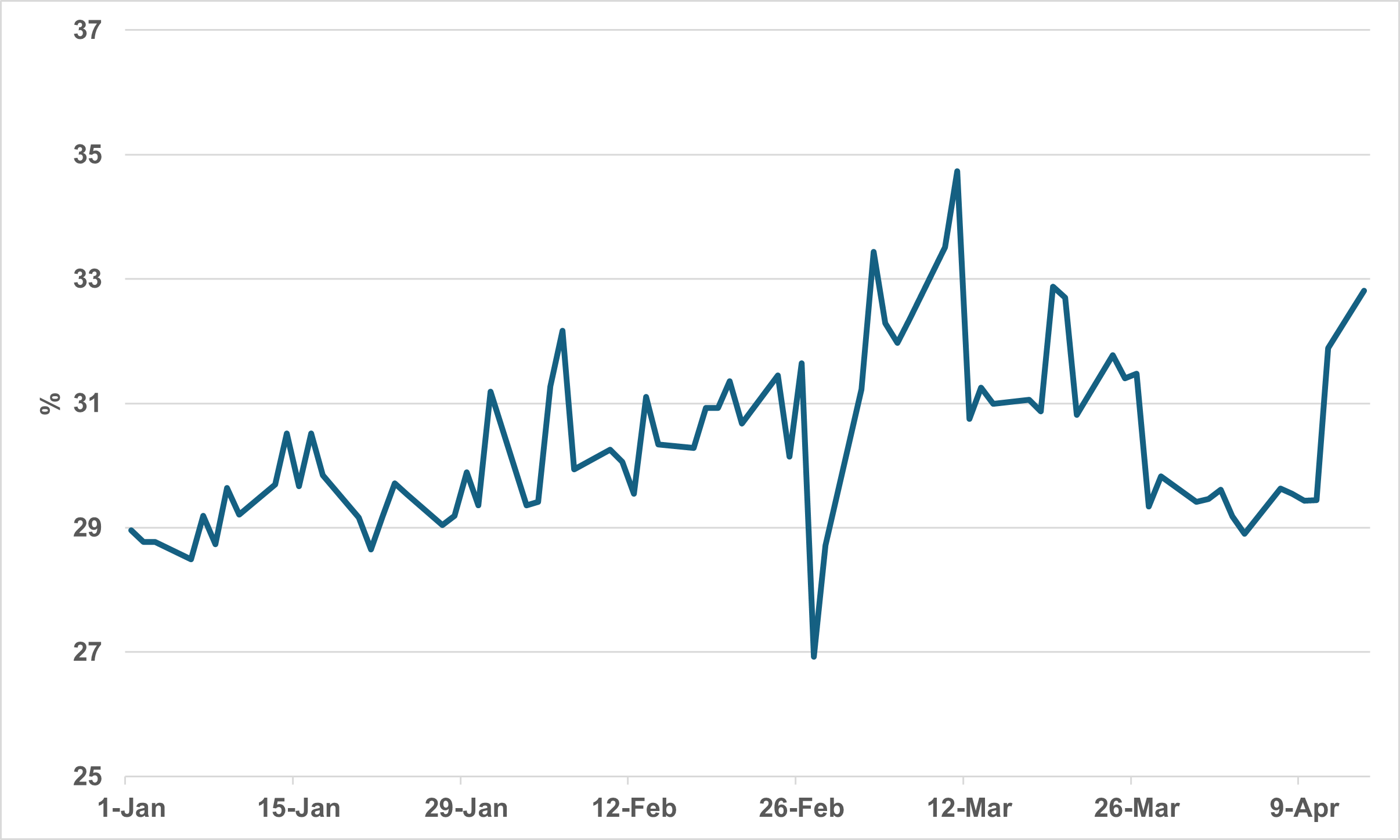

EXHIBIT #1: SHARP RISE IN SHORT UTILIZATION FOR CANADIAN GOVERNMENT BONDS

Source: BNY

Canadian government bonds don’t show any abnormal flow patterns. The only change is the range in flows from cross-border investors narrowing significantly. This suggests any rotation away from U.S. Treasurys into bond markets is not taking place in size. Vigilance remains necessary in Canada as the last few days show a material pick-up in short utilization, which runs counter to the “lack of selling” narrative. Canada’s debt position is not in doubt - even with the election uncertainty of next week and today’s Bank of Canada rate decision - so policy aspects could be in play here. Tactical positioning ahead of the BoC is the most likely source for the move, but market participants expecting a dovish decision, the level of short utilization provides good entry levels to capture some flattening.

Risk sentiment sours on back of semiconductor headlines and as good news on China growth prolongs expectations for the U.S. trade war. The cause and effect of policy shifts is the main driver for optimism in buying-the-dip in either bonds or stocks. The hope for an off-ramp on tariffs also pivots on the success for Japan trade talks ahead. The safe haven demand for USD alternatives has complications as BOJ and SNB comments suggest, and other bond markets have size limits – with our data showing ongoing doubts about global growth. Markets are still in low volume, high volatility mode but the worst fears of a break down in function have passed, but with today a key test of such with FOMC Chair Powell and the U.S. 20-year bond sale viewed as crucial to Fed easing direction and foreign appetite for U.S. assets. The duration demand and shape of the U.S. curve looks more important for investor moods than usual with the 2/10Y stuck around 50bp and the 2/30Y near 100bp – the longer end should be attractive but for the uncertainty on both fiscal and monetary policy. The U.S. term premium is still far from the December highs and the expectations for further Federal Reserve easing for May are back to 20%, with futures markets pricing in a target of 3.5% at the end of 2025. How the Bank of Canada deals with policy and guidance today will matter to the U.S. markets while the uncertainty over trade is global. After last week, there is also a sense of fatigue where relief in range trading rather than new inflection points across asset prices helps. The ongoing focus on U.S. growth over inflation matters to the overall mood along with U.S. retail sales, industrial production data, and the housing market, but policy reactions matter even more.

Headline UK inflation for March dropped to 2.6%y/y, slightly below expectations of 2.7%y/y. Services inflation also slowed to 4.7%y/y vs. 4.8% expected. There were clear signs of a consumer slowdown as discretionary items such as recreation and culture and restaurants and hotels all contributed to weaker price growth. Markets are currently pricing in around 100bp over the next four quarters, beginning in May. However, April figures will prove difficult to navigate due to broad-based price gains for the new fiscal year – Governor Bailey had already warned of a ‘hump’ for the month. UK CPI surprises to the downside, coming in at 2.6%y/y, 0.3% m/m. The results strengthens the case for the Bank of England to accelerate easing. The market is pricing in a 90% chance of a 25bp cut in May.

China Q1 GDP growth beats expectations. China Q1 GDP grew 5.4% y/y or 1.2% q/q. March fixed asset investment up to 4.2% y/y (Feb: 4.1%); Industrial Production +6.5% y/y, the best since Feb 2024, led by new energy automobile production, industrial robot - up respectively 45.4% y/y and 26.0% y/y. Retail Sales grew 4.6% y/y (Feb25: 4.0% y/y). Spending on grain, oil and food posted the strongest growth at 12.2% y/y, clothing 3.4% y/y, while auto sales at -0.8% y/y. Property Investment continues to to be the biggest drag, at -9.9% y/y, while the real estate sector overall remains sluggish but with sequential improvement. The total residential sales value is near flat at -0.4% y/y from -32.7% low in February 2024 or -17.6% y/y at the end of 2024. Residential floor space sales at -2.0% y/y vs -14.1% y/y at the end of 2024, and finally, the total inventory growth pace steady around 6.8% y/y. SHCOMP +0.3%, 10yr CGB 2bp lower at 1.64%, CNH –0.1% at 7.3273

China appoints new top trade negotiator, Li Chenggang, a former assistant commerce minister during the first administration of U.S. President Donald Trump. He also previously served as Beijing's ambassador to the World Trade Organization and deputy permanent representative to the United Nations in Geneva. Chinese President Xi is in Malaysia for the second leg of his ASEAN tour. He called for the two countries to “uphold the multilateral trading system, keep global industrial and supply chains stable, and maintain an international environment of openness and cooperation.”

U.S. March Retail Sales expected up 1.4% m/m after 0.2% m/m – with ex autos and gas up 0.6% m/m after 0.5% but the control group is seen slowing to 0.6% m/m from 1.0% m/m – linking the pre-tariff buying and the consumer mood will be key for policy watchers.

U.S. March Industrial Production expected down -0.2% m/m after 0.7% m/m with capacity dropping to 77.9% from 78.2% - looking for signs of some manufacturing recovery.

Bank of Canada rate decision expected to keep rates on hold at 2.75%. However, there is a strong chance of a cut as the central bank seeks to support the economy ahead of tariffs. The CPI and jobs data pushed markets to price in a 50% chance of easing today.

U.S. April NAHB Housing Market Index expected 38 from 39 – with no help from US rates and higher uncertainty due to tariffs – watching for further builder pessimism.

Federal Reserve Chair Powell speaks to the Economic Club of Chicago about the economic outlook.

U.S. Treasury sells $13bn in 20-year bonds with keen interest on the foreign demand, overall success of sale.

Mood: iFlow Mood moved further into risk-off mode with pickup in equity selling and buying in G5 bills. Conditions likely to worsen towards recent iFlow Mood lows at the end of February 2025.

FX: Increasing positive flows momentum across G10 including reduced outflows pressure in EUR and GBP. Mixed flows in APAC while selling pressure in LatAm and EMEA. TRY posted the most outflows.

FI: Cross-border selling of U.S. Treasurys vs buying of Eurozone government bonds. Elsewhere, selling pressure continues globally, except for light buying in Australia and Chinese government bonds.

Equities: Sharp pick up of equity selling in APAC, especially in China, Hong Kong and Taiwan. Major G10, such as US, UK and Japan equities were sold while mixed flows in LatAm and EMEA.

“There can be no effect without a cause…the whole is necessarily concatenated and arranged for the best.” – Voltaire

“Time, space, and causality are only metaphors of knowledge, with which we explain things to ourselves.” - Nietzsche

South Korea March export prices index stood unchanged at 6.3% y/y while Import prices ease to 3.4% from a downwardly revised 4.3% y/y in February. Looking into breakdown, electronic products export prices at 8.3% y/y while import prices of raw materials plunged to -2.5% y/y from 1.8% in February 2025. KOSPI –1.2%, 10yr KTB 2bp lower at 2.64%, KRW +0.3% higher at 1424

Japan February total value of machinery orders increased by 3% m/m. Private sector demand grew strongly at 12.1% m/m. When excluding volatile orders from ships and electrical power companies, i.e. core machine orders is up by 4.3% m/m (Jan: -3.5%) and 1.5% y/y (Jan: 4.4% y/y). The non-manufacturing private sector gains most at 11.4% m/m, compared with 3.0% m/m gain in the manufacturing sector. Nikkei –1.0%, 10yr JGB down 10bp at 1.27%, JPY +0.5% stronger at 142.2

Australia March Westpac Leading Index dropped -0.11% m/m, the most monthly decline since January 2024. Year-on-year growth is at 0.2% y/y. Note that the Westpac Leading Index has lost its explanatory power to serve as leading indicator for Australia GDP since 2024 where index growth is moving gradually higher from negative y/y while Australia GDP y/y has been moving in opposite direction except for a rebound in Q4 2024 to 1.3%. Q1 GDP release will be on June 4th, 2025. ASX200 flat, 10yr ACGB flat at 4.35%, AUD –0.2% at 0.634

China March new home prices and used home price decline to -0.08% m/m and -0.23% m/m, the least since May 2023. New home prices for Tier-1 cities up for the fifth straight month at 0.13% m/m while Tier-2 cities back to m/m gain of 0.03% after a brief decline in February. Tier-3 new home prices posted a smaller monthly drop at -0.21% m/m (Feb: -0.24% m/m). Used home prices for Tier-1 cities up 0.25% m/m (Feb: -0.1% m/m) while Tier-2 and Tier-3 used home prices decline narrowed at -0.18% m/ m (Feb: -0.10%) and -0.33% m/m (Feb: -0.39%).