Market Movers: Capitulation

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

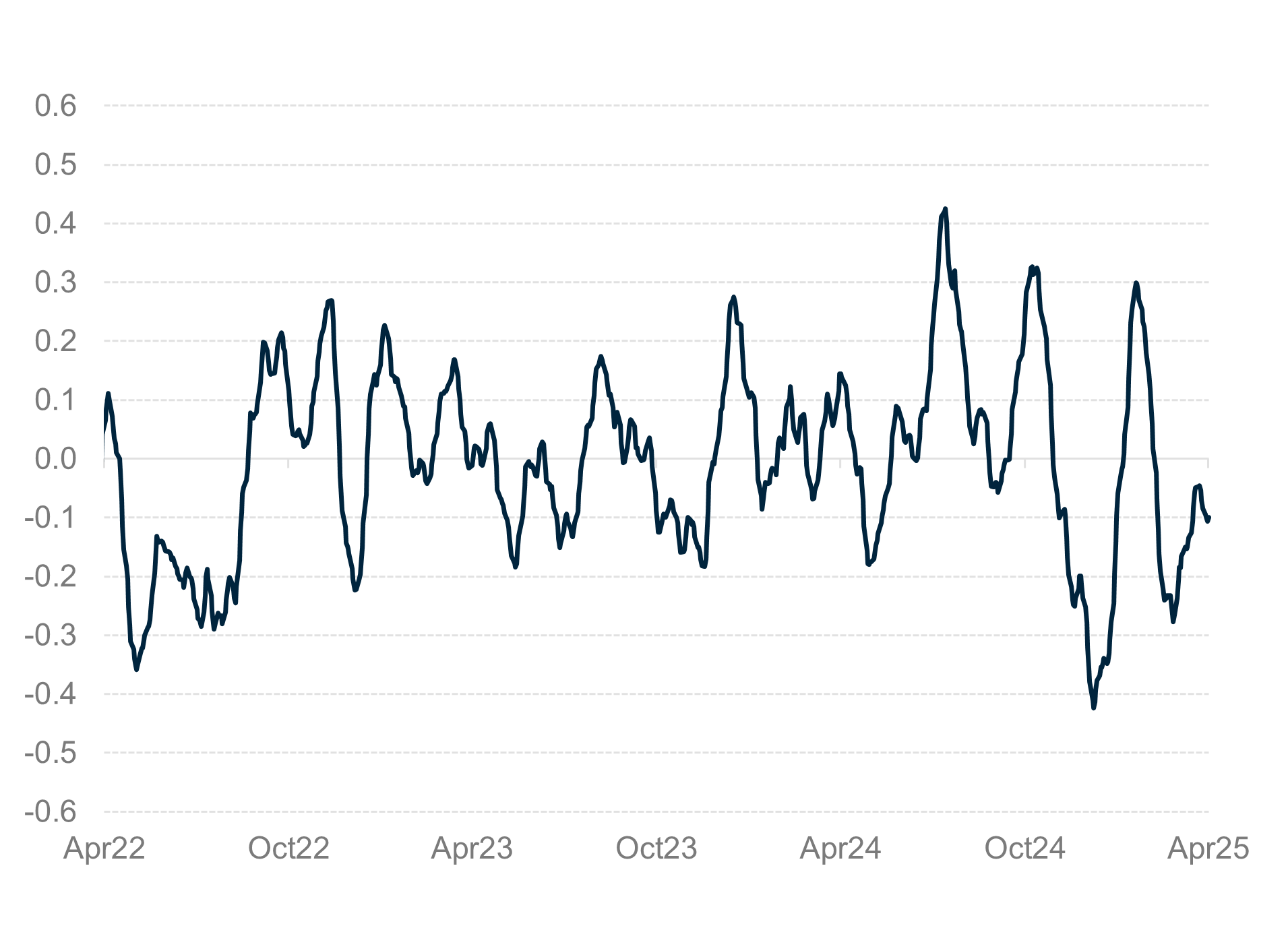

EXHIBIT #1: iFLOW MOOD ENTERS RISK-OFF TERRITORY

Source: BNY

Risk aversion continues, with a focus on China and central banks as they deal with equity selling. Clients are asking three questions: First, when will the selling end? As we can see in our data it’s too soon to call a bottom. Second, what is needed for stability? The iFlow data suggest it’s near as shorts are in place in the U.S. and the rest of the world catches up. But the news flow has to provide support, whether from more dovish central bankers or further tariff negotiations. Lastly, markets want to see evidence of pre-tariff stability, which was seen overnight in Japanese and German data. The focus today is on the Fed, the BoC and all markets as the price action shifts from capitulation to something else.

Eurozone April Sentix Investor Confidence falls to -19.5 from -2.9. The tariff shock has wiped out the previous euphoria in Germany and Europe. Economic expectations for the Eurozone fell at a record pace, from 18 to -15.8.

German February trade surplus up €1.5bn to €17.7bn – exports rose 1.8% m/m – with U.S. exports up 8.5% m/m – while industrial production fell -1.3% m/m, -4% y/y, led by construction. The weakness in the German economy before tariffs was clear.

Hang Seng down -13.2%, the fifth worst daily sell-off in history, after -33.3% (October 26, 1987), -21.7% (June 5, 1989), -13.7% (October 28, 1997) and -13.3% (March 26, 1973).

China’s policymakers consider front-loading stimulus to bolster consumption. They also discussed engaging a stabilization fund to shore up the country’s stock market. SHCOMP -6.3%, 10y CGB off 8bp at 1.63%, CNY -0.4% at 7.31.

U.S. February consumer credit expected down to $15bn after $18.08bn – with focus on the consumer mood, balance sheet and wealth effect from equities lower.

Fed Governor Kugler speaks on inflation dynamics, Philips curve.

Bank of Canada Q1 Business Outlook – after weak jobs report Friday, stock market weakness and ongoing tariffs, focus is on how bad the outlook is vs. new tariffs in Q2.

Mood: Heightened risk aversion with further selling flows with ongoing demand for short-term government bonds.

FX: FX volatilities were concentrated on the G10 space with strong demand for USD and JPY against heavy outflows in CAD, GBP and MXN. FX flows in APAC, EMEA were relatively calm with moderate buying.

FI: Moderate U.S. Treasurys, but signs of a reversal of cross-border U.S. Treasury flows to buying. Eurozone government bonds were most bid, against selling in LatAm and EMEA, with mixed fixed income flows in APAC.

Equities: Broad selling pressure in G10 equities. Sector breakdown of flows is not all-out negative. With respect to US equities, iFlow showed buying surfacing in Consumer Staples, and light inflows in the Materials and Utilities sectors. Flows in the LatAm, EMEA and APAC are mixed and light.

“Negotiations are a euphemism for capitulation if the shadow of power is not cast across the bargaining table.” – George Schultz

Japan February labor cash earnings grew more the expected at 3.1% y/y from 1.8% y/y in January 2025. Real cash earnings at -1.2% from -2.8% y/y. Looking into breakdown, the Financial and Insurance industries posted the biggest earnings at 25.8%, followed by Utilities at 16.8% y/y, and Mining at 14.4% y/y.

Japan February coincident index rose to 116.9 from 116.1 – better than 115.8 expected – the highest reading since September 2019, supported by a moderate economic recovery amid a rebound in private consumption and business investment, modest corporate profits and improving employment and income conditions. However, the outlook drops to 107.9 from 108.2 – as expected. The latest reading came amid a fall in annual household spending, the first decline since last November. At the same time, consumer sentiment deteriorated to its lowest level since March 2023. Nikkei -7.3%, 10y JGB 8bp lower 1.11%, JPY up +0.7% at 145.88.

China March official reserves assets rose to $3240.7bn from $3227.2bn in February 2025. The increase is primarily due to higher gold holdings, which rose from 73.61mn fine troy ounces to 73.7mn fine troy ounces, or to $229.6bn from $208.6bn. SHCOMP -6.3%, 10y CGB off 8bp at 1.63%, CNY -0.4% at 7.31.

Eurozone April Sentix Investor Confidence falls to -19.5 from -2.9. The tariff shock has wiped out the previous euphoria in Germany and Europe. Economic expectations for Eurozone fell at record pace, from 18 to -15.8. Eurozone February retail sales up 0.3% m/m, 2.3% y/y from upwardly revised 0% m/m, 1.8% y/y in January.

Australia Treasury estimates real GDP will decline by 0.1% and inflation will increase by 0.2% in 2025 relative to a baseline scenario with no tariffs. The tariffs announced over the past few days were more significant than expected. The potential magnitude and persistence of the economic effects of the announcement has resulted in greater uncertainty around the outlook for Australia. ASX200 -4.3%, 10y ACGB down 6bp to 4.15%, AUD -0.6% at 0.600.

German February trade surplus rises to €17.7bn from €16.2bn – as expected – exports rose by 1.8% m/m to a 10-month high of €131.6 billion in January, after showing no growth in the previous month, supported by sales to EU countries (0.5%), specifically to the Euro area (0.3%) and the non-Euro area (1.0%). Additionally, sales to third countries expanded by 3.2%, due to higher sales to the U.S. (8.5%) and China (0.6%), but with falling sales to the U.K. (-3.8%) and Russia (-3.0%). Meanwhile, imports climbed by 0.7% to a 20-month high of €113.8 billion. Imports from the EU grew by 2.3%, with increases from both the Euro area (2.8%) and the non-Euro area (1.4%). Conversely, purchases from third countries fell by 1.0%, amid lower arrivals from the U.S. (-3.9%), Russia (-4.5%) and the U.K. (-5.2%), while purchases from China advanced (7.1%).

German February industrial production fell -1.3% m/m, -4% y/y after +2% m/m, 1.6% y/y – worse than the -1.1% m/m expected. The decrease was largely driven by a 3.2% drop in construction industry, along with reduced output in the food industry (-5.3%) and energy production (-3.3%). By contrast, a 3.3% increase in electrical equipment manufacturing positively impacted overall results. Meanwhile, production in energy-intensive industries fell by 0.6%. The less volatile three-month-on-three-month comparison showed a 0.1% decline in industrial output from December 2024 to February 2025. Eurostoxx -6.6%, 10y Bund down 13bp to 2.45%, EUR +0.6% to 1.102.

Saudi Arabia March PMI stayed strong at 58.1 (February: 58.4) with the best quarter of job creation in over 12 years. Output and new orders rise but at a slower pace while input cost inflation cools to a four-year low.

Indonesia is said to intervene in the offshore market to stabilize IDR. Bank Indonesia signaled to the market that it will intervene aggressively as the market reopens after the Eid holiday as of April 8, 2025. This is a strong rhetoric from previous “intervene boldly” statement.