Market Movers: Bonds

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 6 minutes

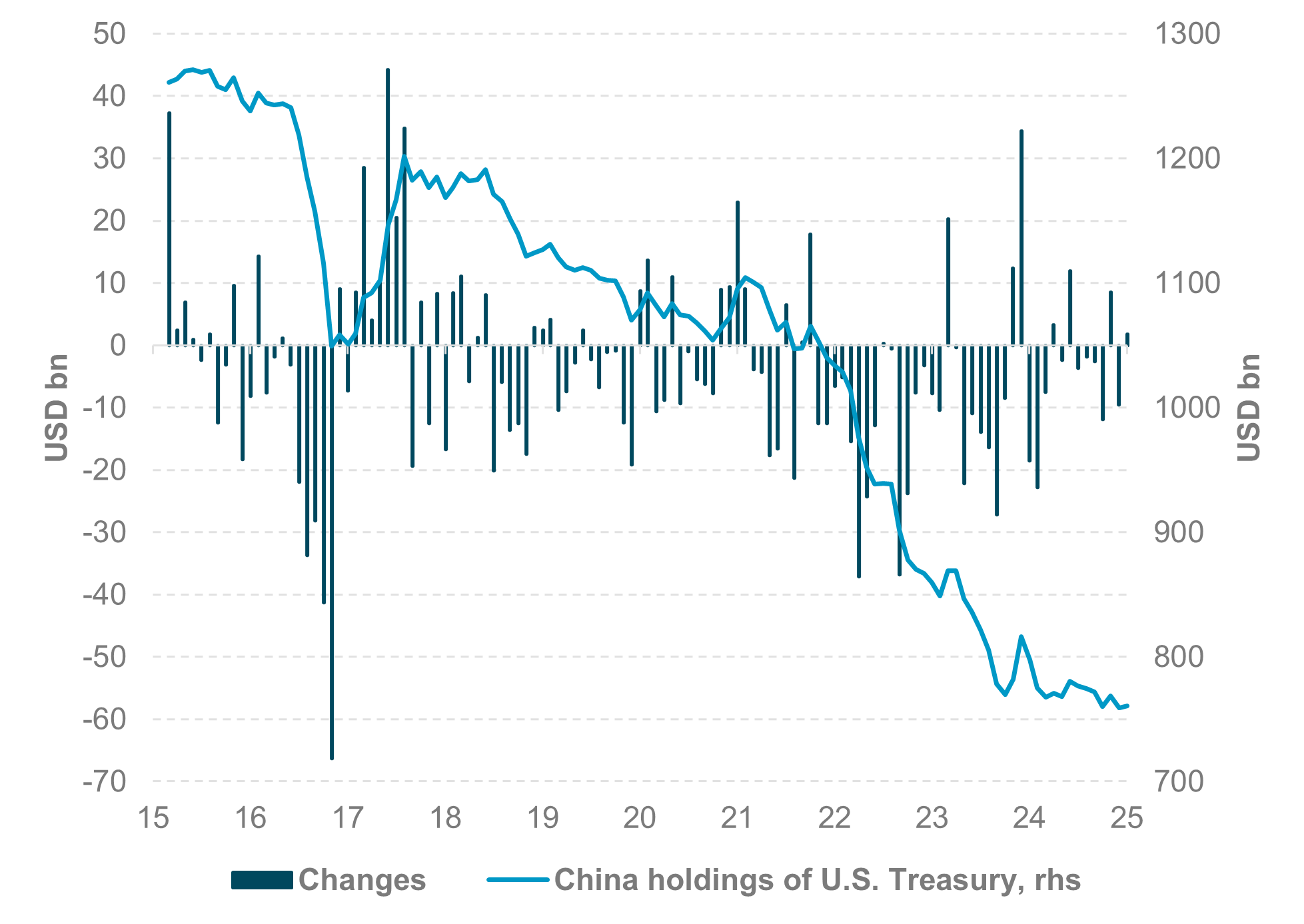

EXHIBIT #1: CHINA HOLDING OF US TREASURY SECURITIES

Source: BNY

The China drop in U.S. bond holdings continues with keen focus on current selling. Cross border flows into U.S. market negative for the year.

Risk aversion continues but led by U.S. fixed income with bond yield curve sharply steepening overnight. The U.S. 30y bond yield touched 5% in Asia trading. The fears of a forced liquidation of U.S. bonds for margin calls drives some of the story – reminiscent of the dash for cash from Covid shocks – but the ongoing tariff war is the larger issue. The safe-haven nature of U.S. assets is being questioned. Cross-border flows into the U.S. bond market have been negative in 2025 and despite a brief rush on “liberation day” and Friday, the selling returned Monday and Tuesday. Overnight, the focus on fixed income was different as the ongoing bear market in equities grinds on, while foreign exchange was stuck in ranges with the USD lower. The higher yields in the U.S. are not yet attracting buyers and the carry trade is under review. The day ahead will be about the FOMC minutes and how the Fed thinks about tariffs and its shocks. Many investors are asking where the put is not just for the S&P 500 but for the U.S. 10y bond as well. The focus is also on the U.S. budget debate in the House and where the support for more debt plays against tariff policy.

Inclusion of Soth Korea’s government bonds in FTSE Russell global index is delayed to April 2026 from November 2025. The new refined technical inclusion approach will be phased in over a shorter eight-month period, in eight equal monthly tranches, commencing with April 2026 and completed in November 2026, the same as originally planned. KOSPI off –1.7%. 10y KTB +3.5bp to 2.73%, KRW +0.1% at 1479.

Japan March consumer confidence fell 0.7 to 34.1 – fourth monthly drop and worst since March 2023 – all ahead of U.S. tariffs. The biggest drop was in expectations. This matters to the government and the BoJ and could add to stimulus plans. Nikkei drops 3.78%, 10y JGB +1bp at 1.27%, JPY up 0.9% to 144.85.

BoE, SNB and ECB step up monitoring of markets. Ongoing checks on banks and liquidity has not yet shown market breaks. ECB Vice-President Luis de Guindos said markets “always overreact in the short term” and have to find a new equilibrium in a new, more fragmented world where growth will likely be lower and inflation higher. Euro Stoxx -1.8%. 10y Bund 1bp lower at 2.62%, EUR +0.9% to 1.102.

U.S. Treasury $39bn 10-year bond sale – given the extreme volatility in global fixed income and steepening pressures, this will be a key focus for markets.

U.S. February wholesale inventories expected up 0.3% after 0.8% m/m – this is important as it allows companies to delay tariff costs in the quarter.

FOMC minutes of March meeting – with a keen focus on the debate about inflation and growth as tariff risks are weighed

Richmond Fed Barkin speaks to the Economic Club of Washington, D.C. – any shift in tone from Fed Speakers is important, particularly about market liquidity and function.

Mexico March CPI expected up 0.31% m/m, 3.8% y/y with core 0.43% m/m, 3.65% y/y – with a strong focus on upside risks and drivers as Banxico rate cutting speeds focus.

Mood: Investor sentiment deteriorated quickly, with iFlow Mood down a notch to -0.14, driven by equities selling and a pickup in government bond buying.

FX: Good buying flows in safe-haven currencies USD, JPY and CHF, with selling momentum picking up in GBP and MXN. EUR scored holding eases off from +1 highs in March.

FI: Eurozone government bonds posted the most demand. Selling pressure continues in LatAm and EMEA, while APAC sovereign bonds saw light buying.

Equities: The trend toward reducing equity risk exposure continues in the G10 complex, with significant selling shown in the U.K., Europe and Sweden. APAC and EMEA equities were sold against demand in LatAm.

“Your word is your bond.” – Melvyn Douglas

“The bond that links your true family is not one of blood, but of respect and joy in each other’s life.” – Richard Bach

South Korea March unemployment rates rose from 2.7% to 2.9% y/y. The economically active population and employment/population ratio rose to 64.6% (February: 63.7%) and 62.5% (February: 61.7%), respectively. March bank lending to households rose for the second month to KRW 1145trn, with a rising year-on-year growth rate of 4.2% y/y, up from 3.9% in February. KOSPI off -1.7%. 10y KTB +3.5bp to 2.73%, KRW +0.1% at 1479.

Fitch on South Korea: “The crisis has not fundamentally altered our assessment of the country’s institutions or governance”. There could be a shift in South Korea’s economic, fiscal and foreign policy, depending on which candidate wins the presidency. Korea’s debt has risen steadily since the pandemic and a sustained upward trend in government debt due to persistently high fiscal deficits could put downward pressure on the rating over the medium term.

Japan March consumer confidence fell to 34.1. In terms of price expectations, 93.9% of respondents expect prices to increase. Looking into the breakdown, both the income growth and employment components were lower, while the willingness to buy durable goods rose on the month. Elsewhere, Japan March machine tool orders are firm at 11.4% from 3.5% in February 2025. Nikkei -3.9%, 10y JGB +1bp at 1.27%, JPY +1.3% at 145.

Reserve Bank of New Zealand (RBNZ) cuts OCR rates by 25bp to 3.5%. RBNZ noted that inflation expectations and core inflation are consistent with the inflation target over the medium term. Household spending and residential investment have remained weak and RBNZ highlighted the downside risk to the outlook for economic activities and inflation in New Zealand. The RBNZ emphasized that it has scope to lower the OCR further as appropriate, signaling the risk of a downward revision of terminal rates, which stood at 3.10% as of the February 2025 forecast. NZX50 -0.7%, 10y NZGB +21bp at 4.76%, NZD -0.5%.

The Reserve Bank of India cut rates by 25bp to 6% with a dovish stance, saying that the policy trend is downward. RBI changed its monetary stance from neutral to accommodative. The decision was unanimous and was supported primarily by the below-target inflation reading, with RBI saying domestic growth is on a recovery path, supported by a pickup in government spending. NIFTY -0.5%, 10y IGB off 1bp at 6.46%, INR -0.3% at 86.53.