Strategic and Selective

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

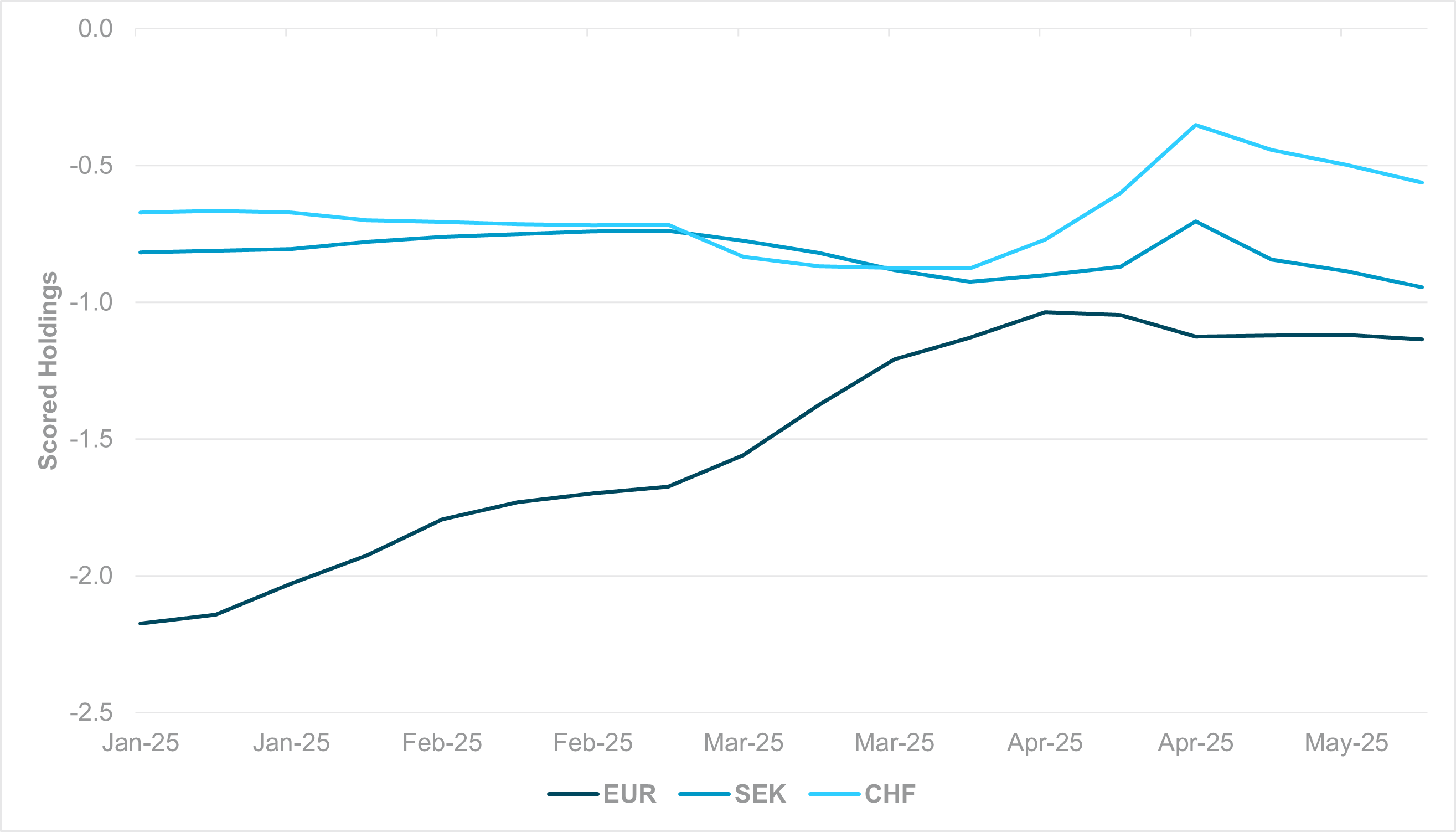

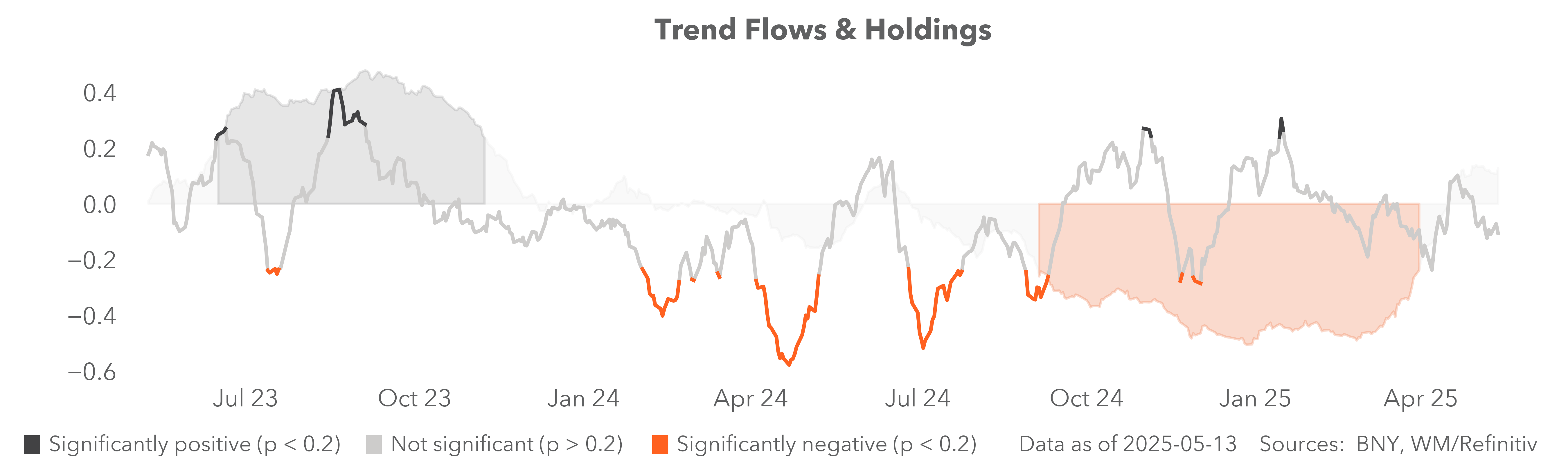

EXHIBIT #1: SCORED CROSS-BORDER HOLDINGS OF EUR, SEK AND CHF YEAR TO DATE

Source: BNY Markets, iFlow, Bloomberg

Our take

A rise in demand for AAA-rated alternatives to U.S. Treasurys during the most volatile days in April pushed all Continental funders to their best cross-border holdings levels (i.e., lowest levels of hedging) year to date, but the process has now gone into reverse. The euro’s recovery through Q1 was associated with the reinvestment and rerating narrative, but the weak initial positioning of the currency augmented price action when unwinding was in full force. Initially, as the ECB indicated a pause in March before “Liberation Day” threw the ECB off-course, the euro’s strength opened up some monetary policy space for the likes of SEK and CHF to strengthen and reduce underheld positions (Exhibit #1). A return to stability has also limited scope for lower USD rates. Coupled with richer FX and equity valuations in Europe, hedging interest is rising again.

Forward Look

Markets are starting to express concerns over the lack of progress in trade talks. Our base case remains for the EU and Switzerland to reach necessary arrangements before the relevant deadlines in July, but a full return to the status quo is unlikely. There will be a long-term impact on European export income, which, surprisingly, isn’t yet being reflected in survey data. We expect data divergence between the Eurozone (and closely linked economies such as Switzerland, Sweden and across CEE) and the U.S. to continue widening. The best-case scenario is a swift deal with the U.S. while Germany and the EU accelerate domestic investment plans. This will mitigate outflows but, barring a U.S. asset shock which would be even bigger than the April episode, marginal flows into Europe may struggle to match Q1 levels. To limit FX exposures on existing assets and take advantage of lighter positioning, we believe hedging flows by cross-border investors will pick up from current levels, though a retreat back to extremes seen at the end of 2024 is also unlikely. Comparatively, CHF is most at risk of a deeper adjustment based on current holdings levels.

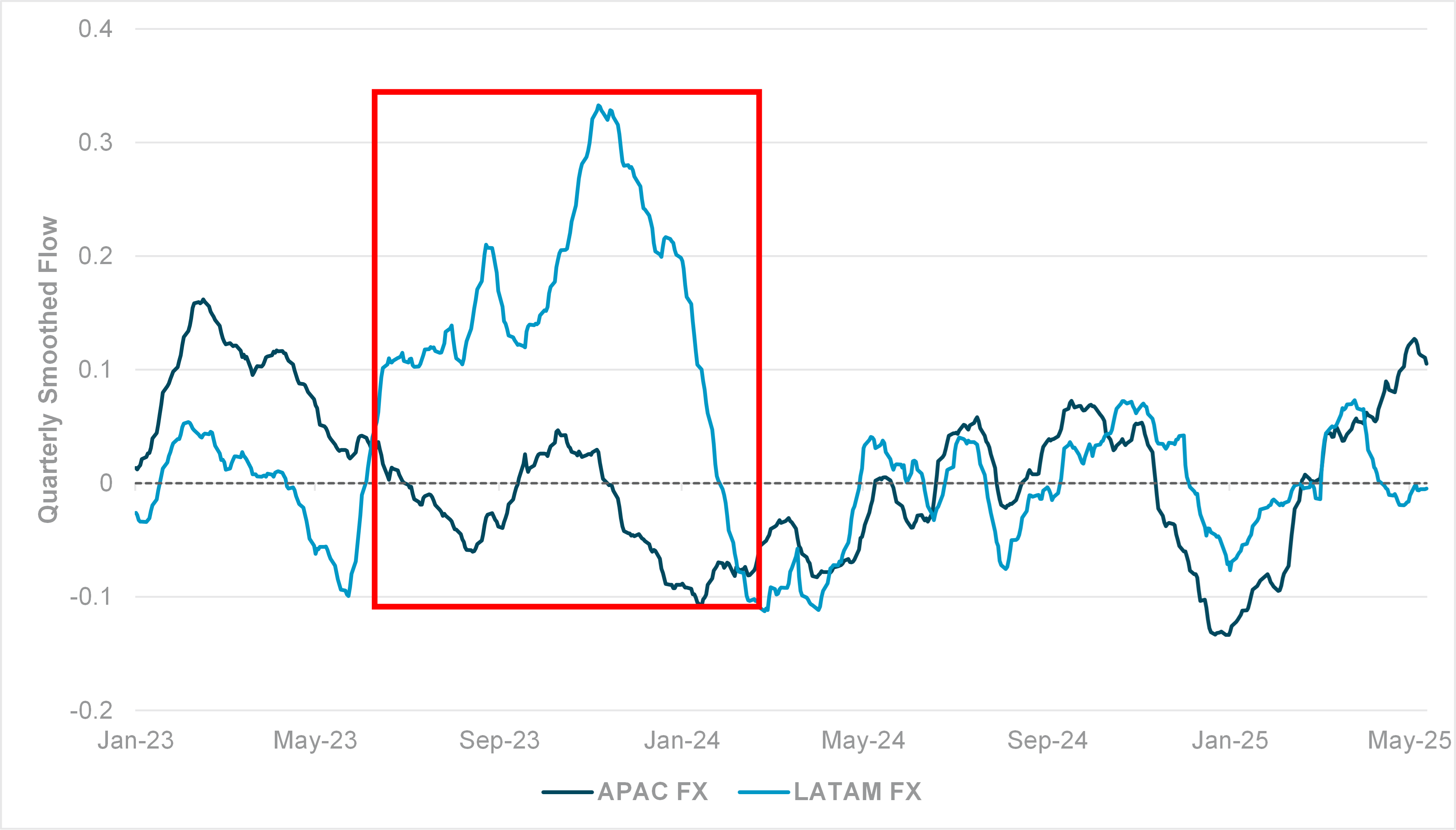

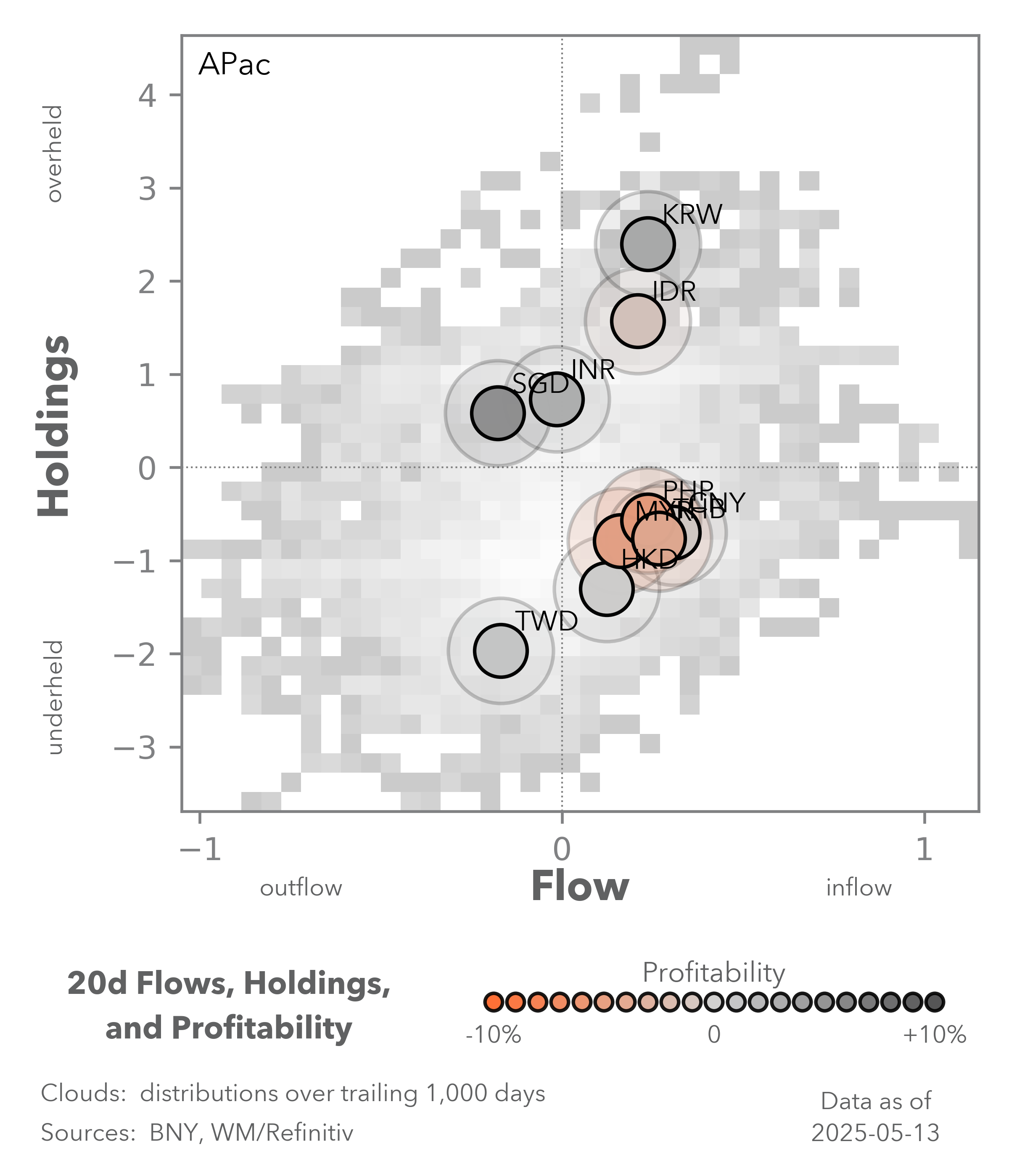

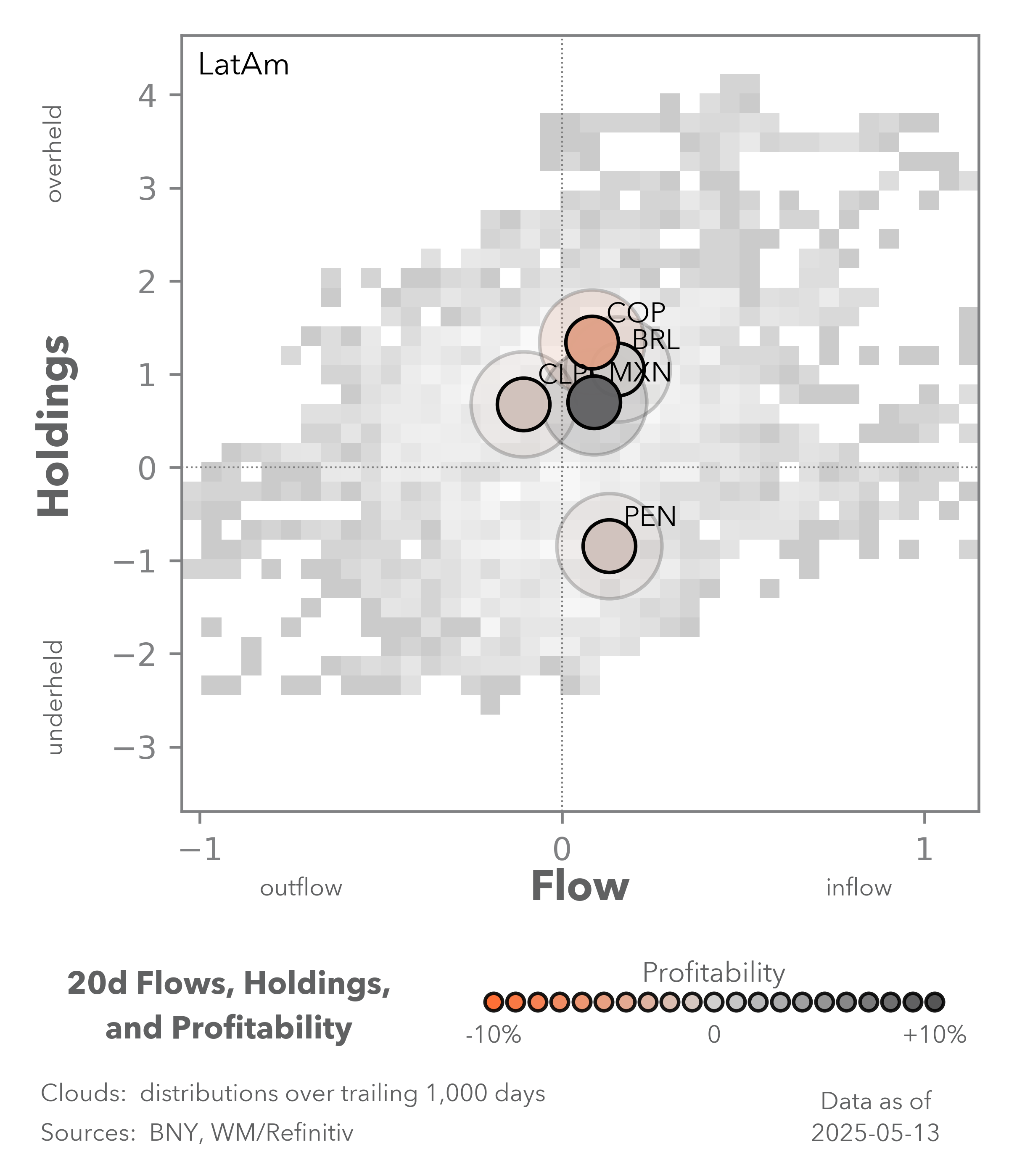

EXHIBIT #2: APAC AND LATAM FX FLOWS, QUARTERLY SMOOTHED SINCE JANUARY 2023

Source: BNY Markets, iFlow

Our take

Although carry interest is starting to re-emerge, we find that current dynamics do not match the 2023 carry surge when flow performance was almost perfectly aligned with yield status. Although the triggers were different, we note that there was severe market volatility centered on U.S. developments toward the end of Q1 2023, leading to material selling of high-yielding currencies. The issues were dealt with swiftly and fueled by aggressive rate-hiking cycles in traditionally high-yielding economies, the divergence between high- and low-yielding blocks was clear. APAC FX was the main source of funding while Latin American currencies were uniformly bought (Exhibit #2). Currently, we are seeing APAC FX purchases peaking while LatAm is now neutral, but with a net purchase bias. The flow setup is similar to Q1 2023, which preceded the carry flourish, but macro conditions preclude a repeat.

Forward look

The biggest risk factor for APAC FX-funded positions is that the market is now attaching a far greater premia to valuations in the region. As officials in Taiwan and South Korea are doing little to dispel the notion that the U.S. is demanding currency appreciation as a part of the non-tariff barrier components necessary to reach a trade deal, low yields alone may not be able serve as a carry anchor, especially if central banks are no longer standing in the way of appreciation. Our flow data indicate that global interest in APAC equities is clear, but hedging interest by cross border investors is picking up as well. This suggests that global equity investors do not see unchecked appreciation as sustainable either, especially given the current downside risks to inflation and export earnings present in the region. However, we also advocate for strong fiscal stimulus in APAC to allow inflation to drive up FX valuations in real terms. This is the ideal outcome for Latin American FX and other carry currencies such as ZAR and IDR, as the consequent demand lift will materially boost terms of commodity exporters with high-yielding currencies.

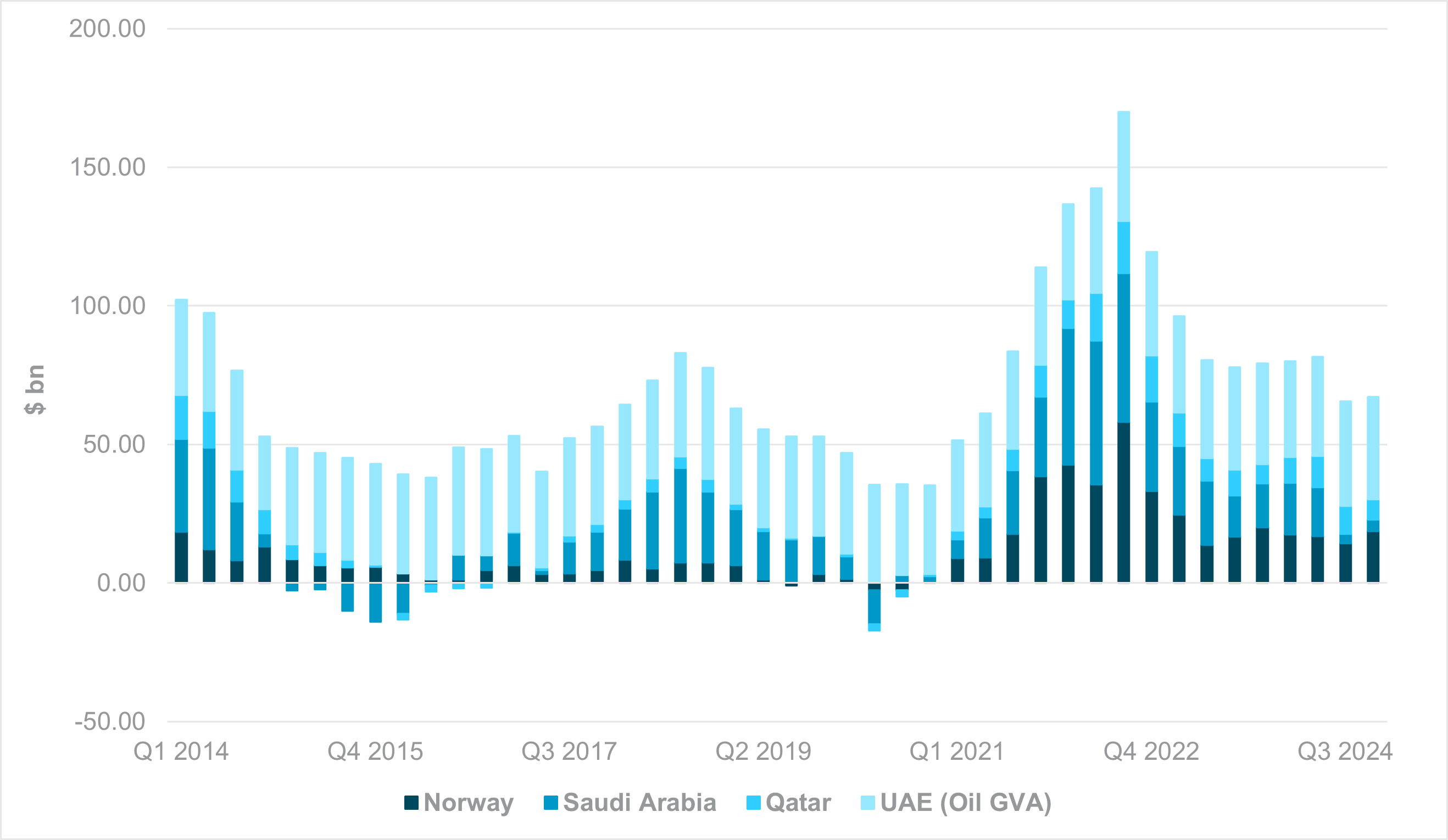

EXHIBIT #3: QUARTERLY CURRENT ACCOUNT SURPLUSES, KEY PETRO ECONOMIES

Source: BNY Markets, iFlow

Our take

President Trump is continuing his travels in the Middle East and the headline value of economic deals and exchanges announced so far this week is approaching $2tn. Investment flows will take time to materialize but after the events of April, the announcements are clearly a fillip to U.S exceptionalism. They also serve as a timely reminder to markets about the ability of petro reserves to assert a strong impact on global financial flows. However, despite the eye-catching numbers, we doubt their impact will be as strong as between 2021 and 2023 when energy prices surged. Current account balances for core producers have fallen sharply over the past six months and the outlook will be even more challenging if OPEC+ continues with production expansion.

Forward look

There are two main implications for weaker growth in petro reserves, both in the dollar’s favor. Firstly, there will simply be lower levels of dollar receipts for diversification purposes, thereby reducing marginal purchases of non-dollar reserve currencies such as the EUR, JPY and CNH, even taking into account the recent increase in diversification interest. Secondly, with fewer current and future financial resources, we expect flows to be far more selective and seek to align with strategic interests while maintaining ease of access and liquidity preference in an increasingly uncertain environment. For most energy producers, the USD is the only currency which ticks all boxes, with this week’s events a timely reminder.

We expect the FX market to continue complementing the recovery in risk appetite, but it will not be a repeat of the carry apex of 2023 or a simple expression of a return to U.S. exceptionalism through dollar longs. Valuations and non-tangible factors all matter, but we expect the cash surge generated last month to be selectively redeployed into risk. FX will most likely passively follow asset interest, and the dollar should manage to steady during the process.