Re-rating Europe the Right Way

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

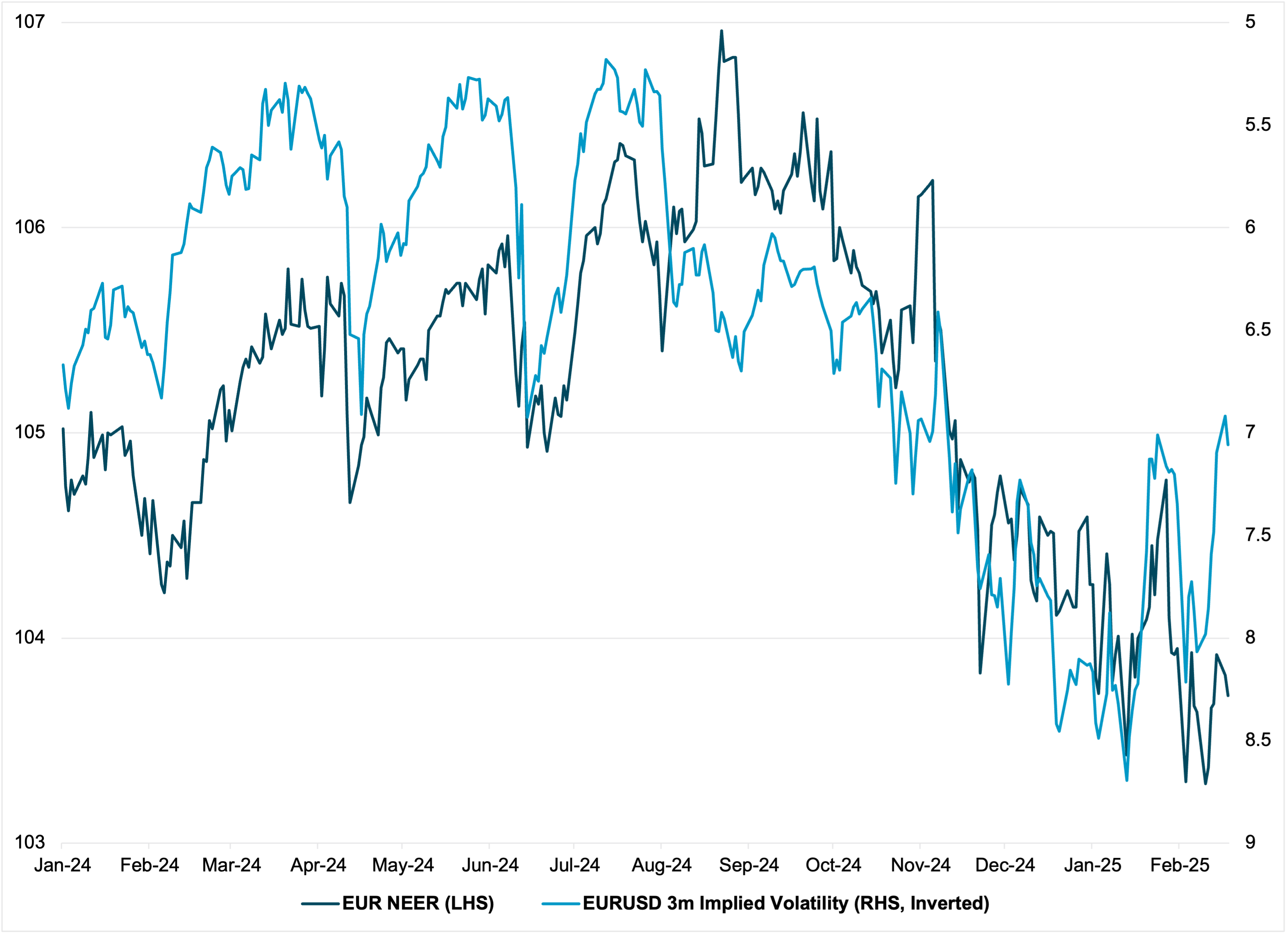

EXHIBIT #1: EUR NEER VS. EUR 3M IMPLIED VOLATILITY

Source: Bloomberg, BNY

Our take

The dollar continues to weaken on a trade-weighted basis, led by losses against the euro which has smoothly navigated the German election. The Continent is now set on a self-funded, defence-based investment drive and the United Kingdom’s decision to immediately raise their defence spending as a share of GDP bodes well for the broader rebalancing narrative, which underpins our asset allocation thesis for Europe this year. However, defence spending was not the driver we had in mind, yet the market appears to be treating it as no different than any other form of public investment. Even more than trade and tariffs, a shift in the decades-old security structure in Europe will lead to significant medium- to long-term uncertainty, yet implied volatility for the EUR has now fallen to the lowest levels since end-2024 (Exhibit #1), signaling even greater positivity on the region than the EUR’s recent rebound.

Forward look

We believe that pricing of good news for Europe is now excessive. Equities are right to re-rate but will be concentrated in certain industrial sectors. We remain concerned that earnings translation in addition to tariff-based disruption is underappreciated. Current EUR levels are indicative of European potential rather than current growth, where risks lie squarely to the downside. Given the six-week time frame for German government formation talks and ongoing economic pressures, the lack of real progress in the near future will begin to pressure the euro.

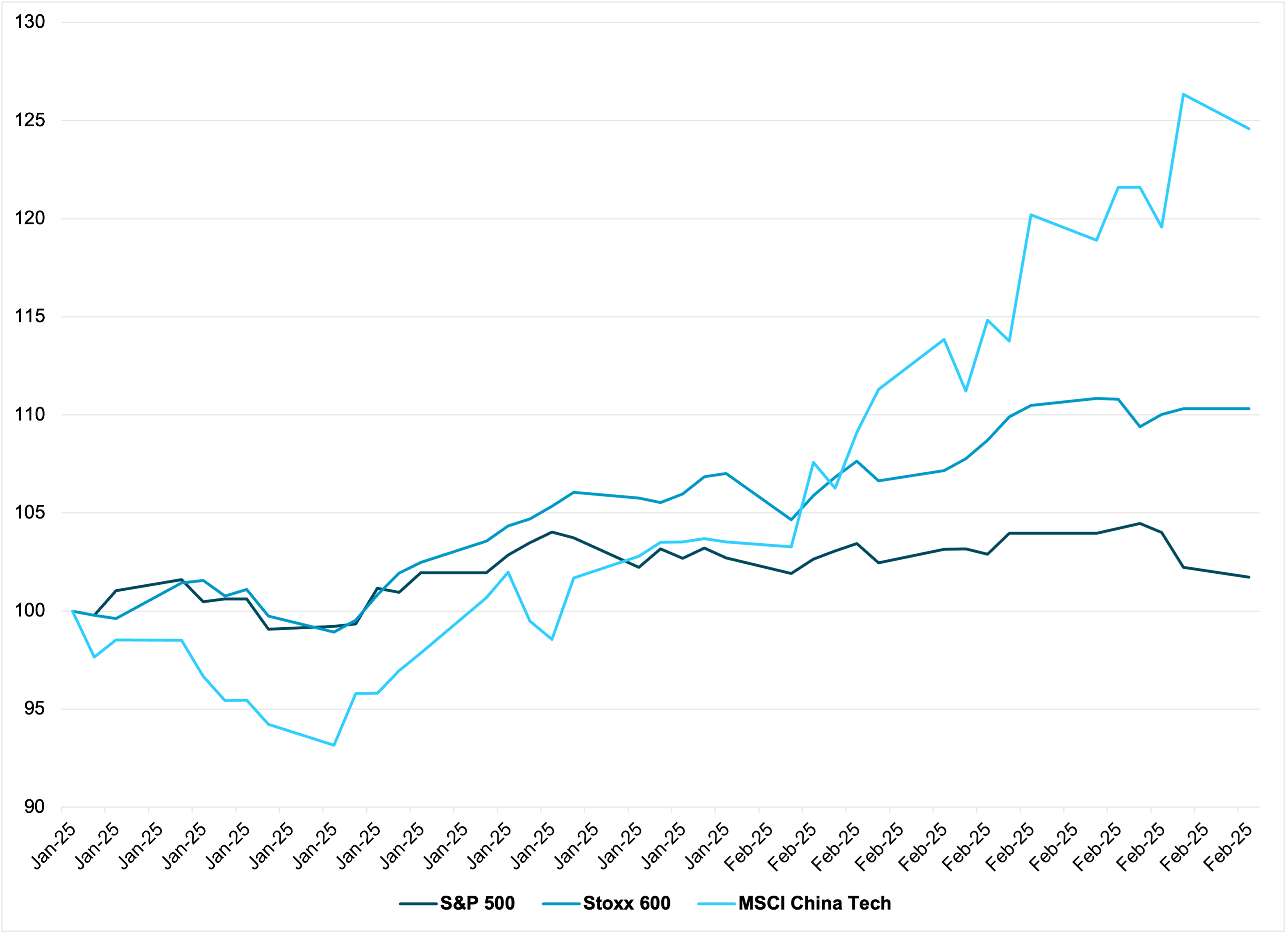

EXHIBIT #2: FOR USD INVESTORS, GLOBAL EQUITIES HAVE RUN AHEAD OF BENCHMARK

Source: Bloomberg, BNY

Our take

Our main asset allocation theme for this year was for Asia-Pacific and European equities to close their holdings gap against the US. Our custody data indicates that for cross-border investors, US holdings are still ahead relative to their rolling 1-year average, but the gap versus Europe and APAC has narrowed sharply – even beyond what we anticipated for the full year. Furthermore, for USD-based investors, total returns in Europe and Chinese tech, in dollar terms (Exhibit #2) have far outpaced US benchmarks. Customary rebalancing around month-end would likely require significant dollar purchases, especially while yield differentials remain favourable.

Forward look

We continue to see the dollar’s valuations peaking this year, but recent moves have been driven by asset allocation requirements and without much regard to underlying policy differentials. We do not see any macro developments which point to material upside risk to growth and interest rate expectations in Europe and Asia: public investment in the former will take time to bear fruit, while markets will need to wait for more concrete spending plans from Beijing to reassess growth forecasts. Yet, Fed easing expectations are being pushed out and the dollar has failed to respond positively to policy divergence. As equity and fixed income portfolios are likely heavily overweight global equity exposures relative to USD-based benchmarks, even if there are secular changes in the European and Chinese growth narratives, hedging out the strong gains in net asset values would require significant dollar purchases. Coupled with tariff deadlines looming for the US’ key trade partners, we see an opening for a broad-based USD recovery.

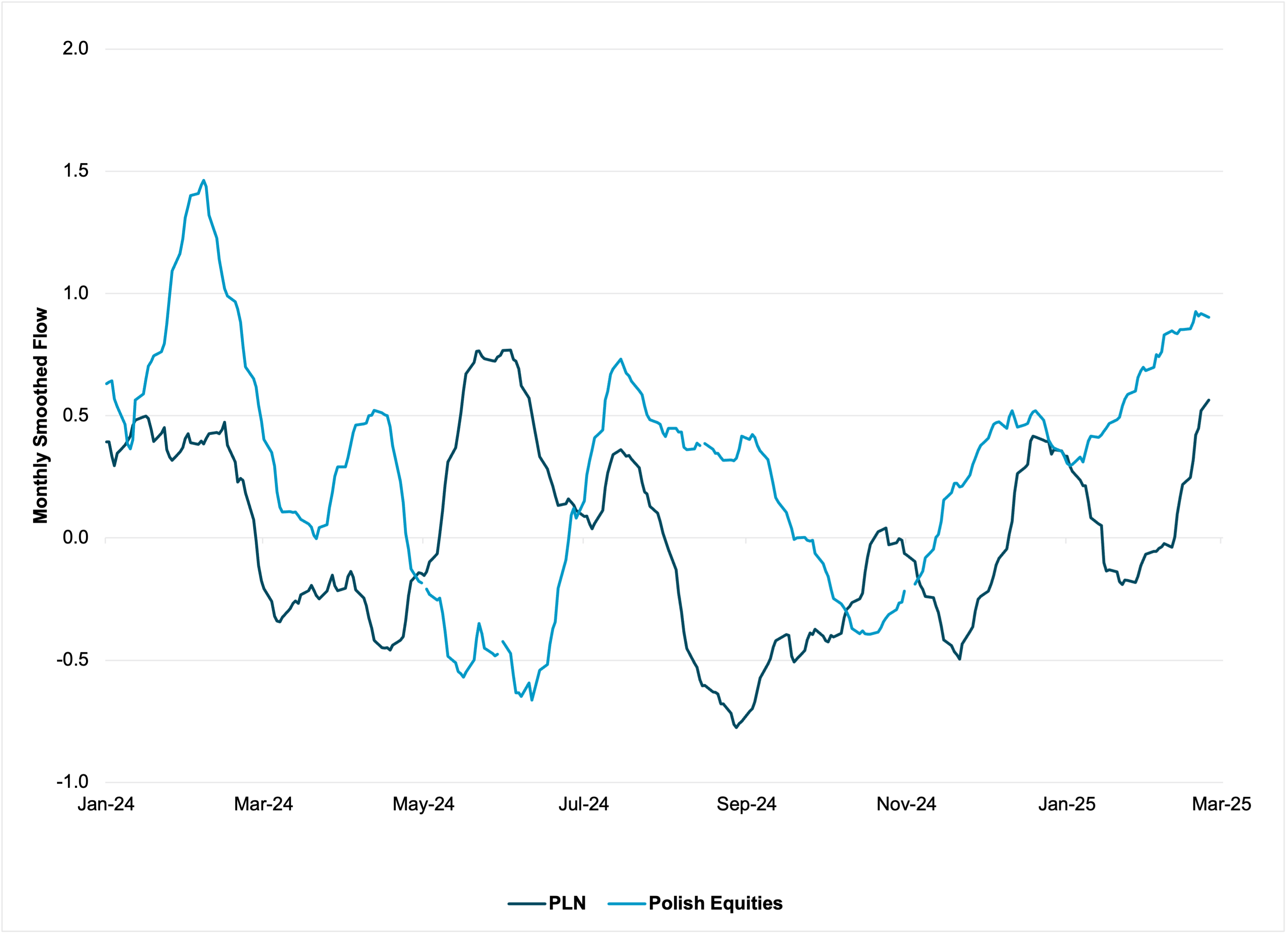

EXHIBIT #3: PLN AND POLISH EQUITY FLOWS AT OR NEAR 1-YEAR HIGHS

Source: BNY

Our take

Dispersion remains significant in emerging market FX, but one segment which is standing out is Central and Eastern Europe (CEE). Even before recent security-related developments in Europe, FX markets saw value in the region arising from a much more assertive stance on monetary policy. Much of this is out of necessity as fiscal tailwinds remain strong in these economies with severe labour-related supply issues. The most recent central bank decisions support this view, with the National Bank of Hungary warning that “upside inflation risk has strengthened” in the country. More recently, however, the prospect of a rapid rise in European defence spending, with much of the deployment and outright investment likely to happen in the CEE region, has generated surge flows across asset classes. HUF and PLN are two of the best-performing currencies in EM FX, while the region is also seeing good inflows into equity markets. This represents a rapid rise in total return exposure.

Forward look

Given the amounts at stake for European defence spending relative to the size of CEE economies, we acknowledge that there is a strong case for re-rating in the region. Demographic pressures have resulted in structural labour supply bottlenecks. Coupled with strong fiscal impulse, these economies will likely continue to “run hot,” and monetary policy will also need to provide the necessary offset to prevent overheating. Given our outlook on the current ECB path, until public investment turns around, rate differentials will continue to support CEE currencies even if global carry interest remains soft. Positioning risk, however, will rapidly escalate from here and we would advocate careful risk management of regional exposures up ahead.

It is difficult to escape the view that there is some complacency coming through in FX markets. Re-rating of non-US asset markets contributed heavily to recent FX moves, but asset allocation is asymmetric: wide gaps in US holdings versus the rest of the world during a risk-on period is sustainable due to US exceptionalism, but the rest of the world will not be immune to increased US-based asset volatility. As US earnings pressure and tariffs move up the agenda, we believe FX needs to reflect such risks through the dollar smile. Coupled with month-end rebalancing, we anticipate recovery flows back into dollars. European and Asia-Pacific economies may be on course to rebalance, but current national income is still heavily reliant on dollar-denominated export receipts. Excessive dollar weakness too early will undermine the very rebalancing that current cross-border flows are attempting to capture.