Pricing in China’s “quality over quantity” shift

iFlow > FX: G10 & EM

Published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

iFlow > FX: G10 & EM

Published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

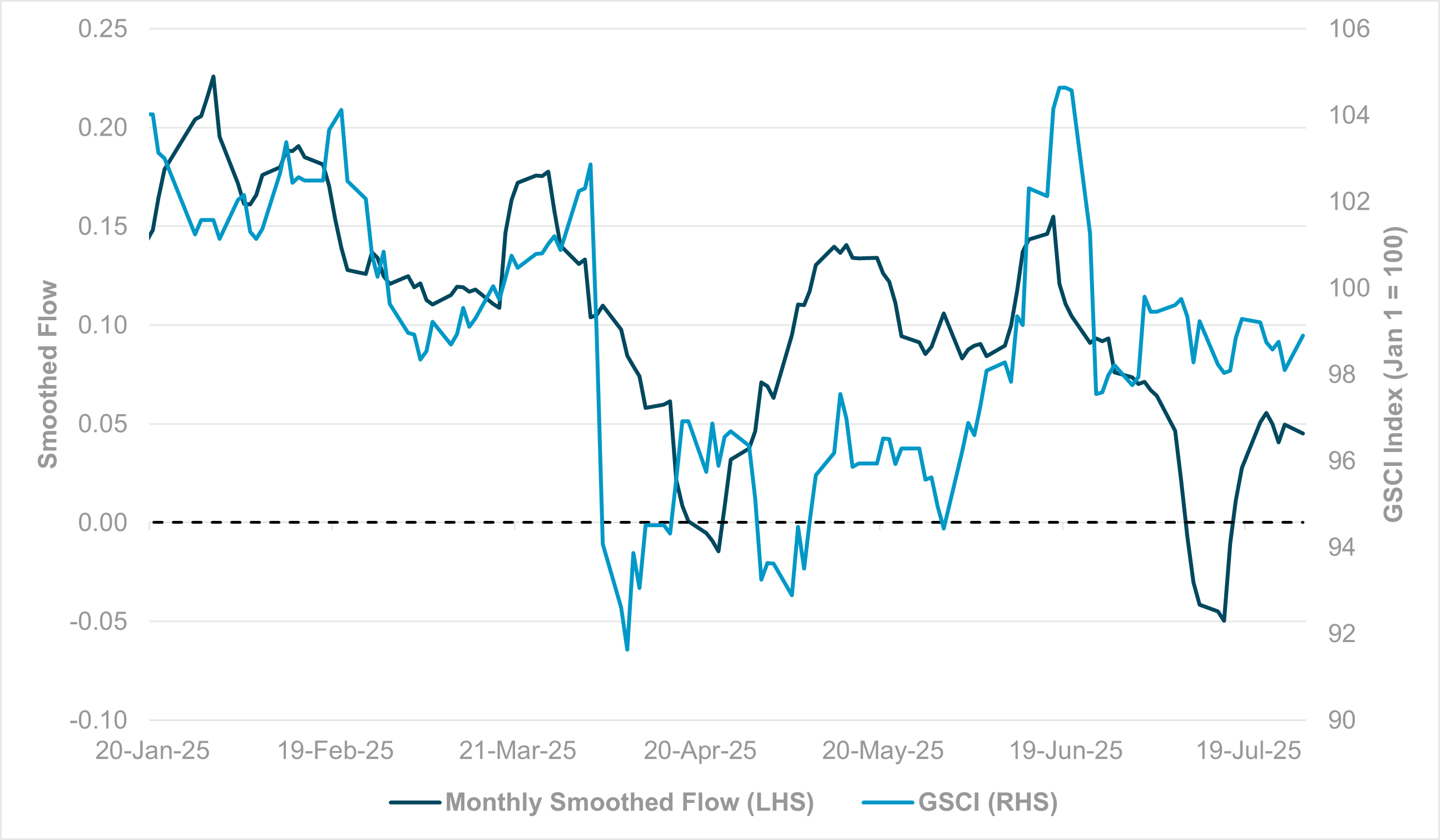

EXHIBIT #1: GSCI COMMODITY INDEX VS. IFLOW EM COMMODITY FX FLOWS

Source: BNY, Bloomberg

Our take

Our month-end positioning analysis for June and July highlighted the need to offset significant flow gains for commodity bloc currencies. For June, it was mostly emerging-market currencies which largely benefited from carry interest and a general recovery in risk appetite. For July, apart from a mid-month dip, these currencies continued to hold on to positive flows (Exhibit #1). Meanwhile, all developed market commodity-linked currencies also had a strong month which required offsets. We believe the July moves had a higher “China investment growth beta” in mind, in addition to tariff factors which led to idiosyncratic shocks on individual commodities. While “hard” growth data globally remains generally resilient, the case for renewed vigor in global investment demand is weak. The GSCI global commodity index remains lower in absolute terms year to date, and at levels which suggest that the global growth outlook is weaker than the Q1 view prior to “Liberation Day.” This supports the view that despite the general conclusion of trade agreements between the U.S. and key partners, there will be a drag on growth, which central banks are attempting to offset with rate cuts.

Forward look

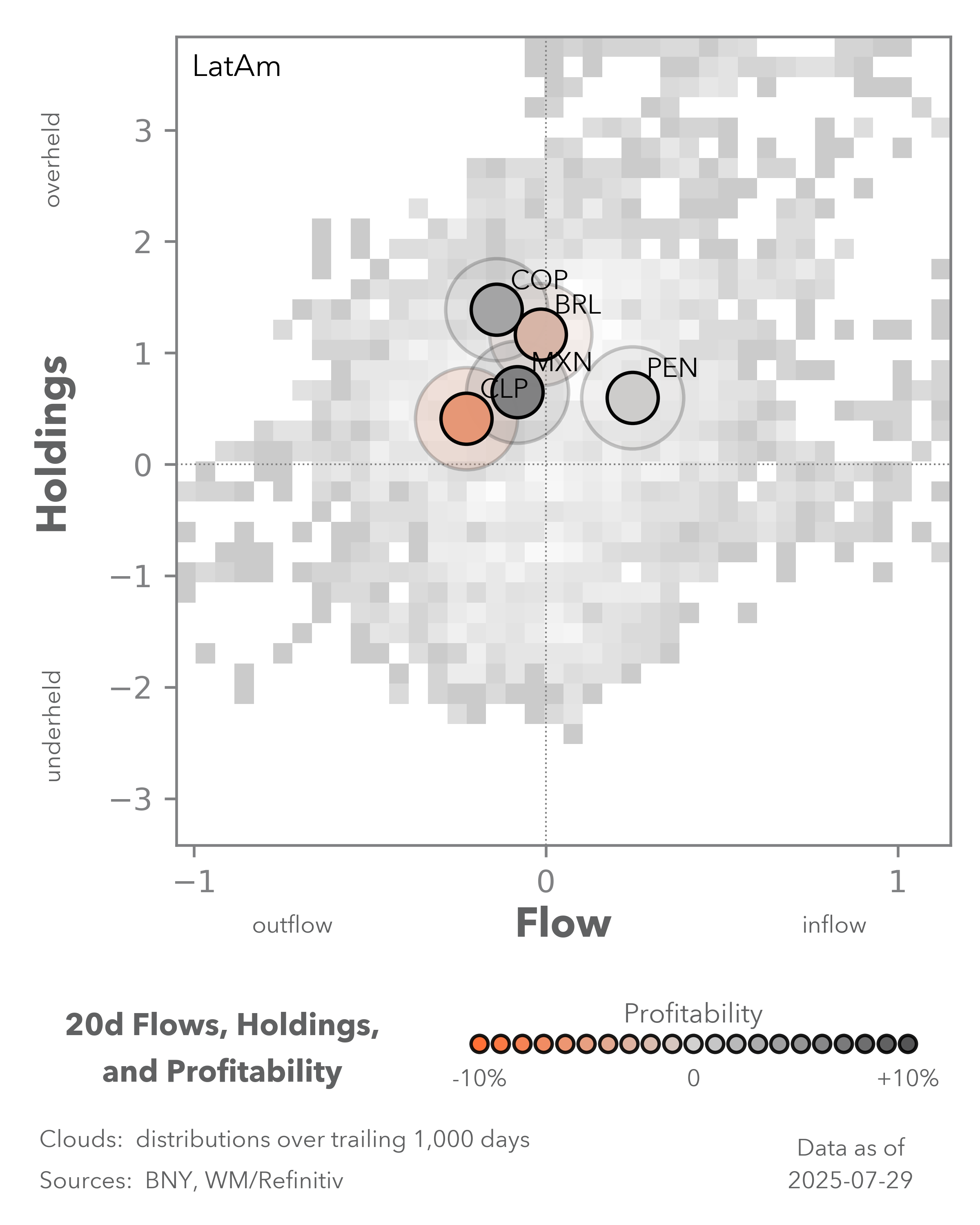

This week’s policy decisions across Latin America already point to ongoing downside risks to growth. Chile, for example, noted that tariff risk has led to inventory accumulation, and supply remains below levels consistent with Chinese growth, but there was still no need to change price projections for 2025–2027, indicating very little upside for the country’s terms of trade. We expect similarly cautious outlooks to prevail across developed and emerging commodity names. Like the accumulation of inventories, there has been a steady accumulation of high-yielding commodity FX exposures, which will likely correct lower as softer growth estimates materialize.

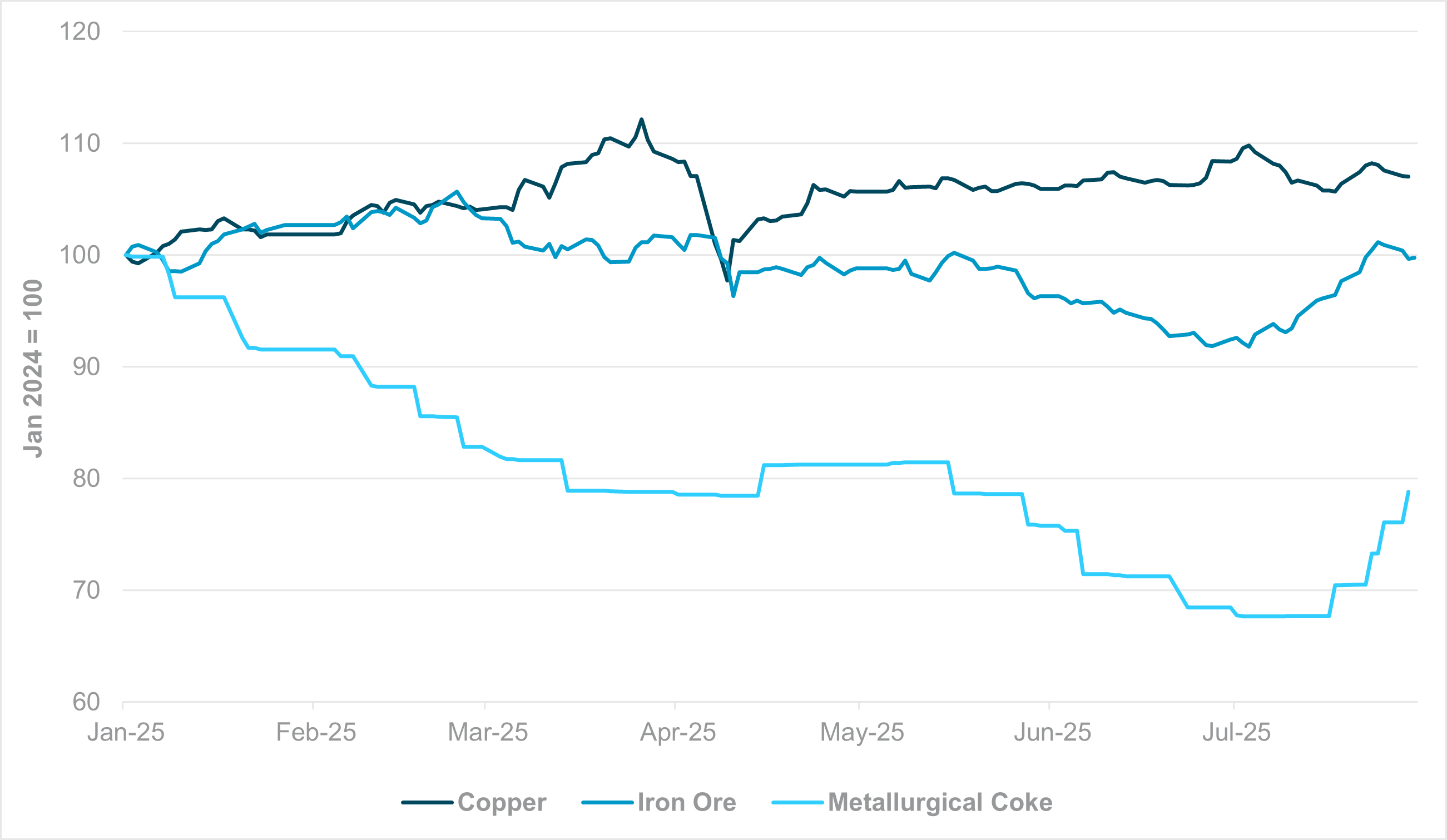

EXHIBIT #2: DOMESTIC PRICES (CHINA) FOR COPPER, IRON ORE AND METALLURGICAL COKE

Source: BNY, Macrobond

Our take

Toward late July, however, industrial commodities were given a fillip by renewed hopes of infrastructure investment in China. Long seen as a more productive channel for investment growth as opposed to real estate, the launch of the biggest hydroelectric project in China’s history, with total investment likely to surpass CNY 1tn, led to significant movement in onshore prices of various industrial inputs, with a commensurate impact on associated sectors in the domestic equity market. Copper prices held at around a 10% y/y gain, consistent with Chile’s assessment of improved demand, while the jump in metallurgical coke prices was particularly predicated upon a surge in steel and iron demand, which would have had implications for the likes of BRL and AUD (Exhibit #2).

Forward look

The coking coal price rally onshore has already petered out and even at its height, prices were still at or below levels at the beginning of the year. Crucially, in the month-end Politburo meeting which focused on the country’s economic strategy for H2 2025, an infrastructure push and wider industrial expansion were not core topics, even though they will continue to contribute strongly to growth in the background. If anything, supporting these sectors, which are prone to over-investment, run counter to the current priority strategy of reversing disinflation and adverse price outcomes. The Politburo statement did mention “major project execution” as a contributor to growth, but only in the context of boosting domestic demand, which in turn is prioritizing consumption, services expansion and improved livelihoods. Gone are the days when investment growth could be signed off to bolster total GDP. Any project that fails to deliver better long-term per capita income growth risks de-prioritization. Consequently, we believe central banks of commodity-linked economies such as Chile are prudent in avoiding pushing up demand forecasts for China, even if there is a clear growth drive in place.

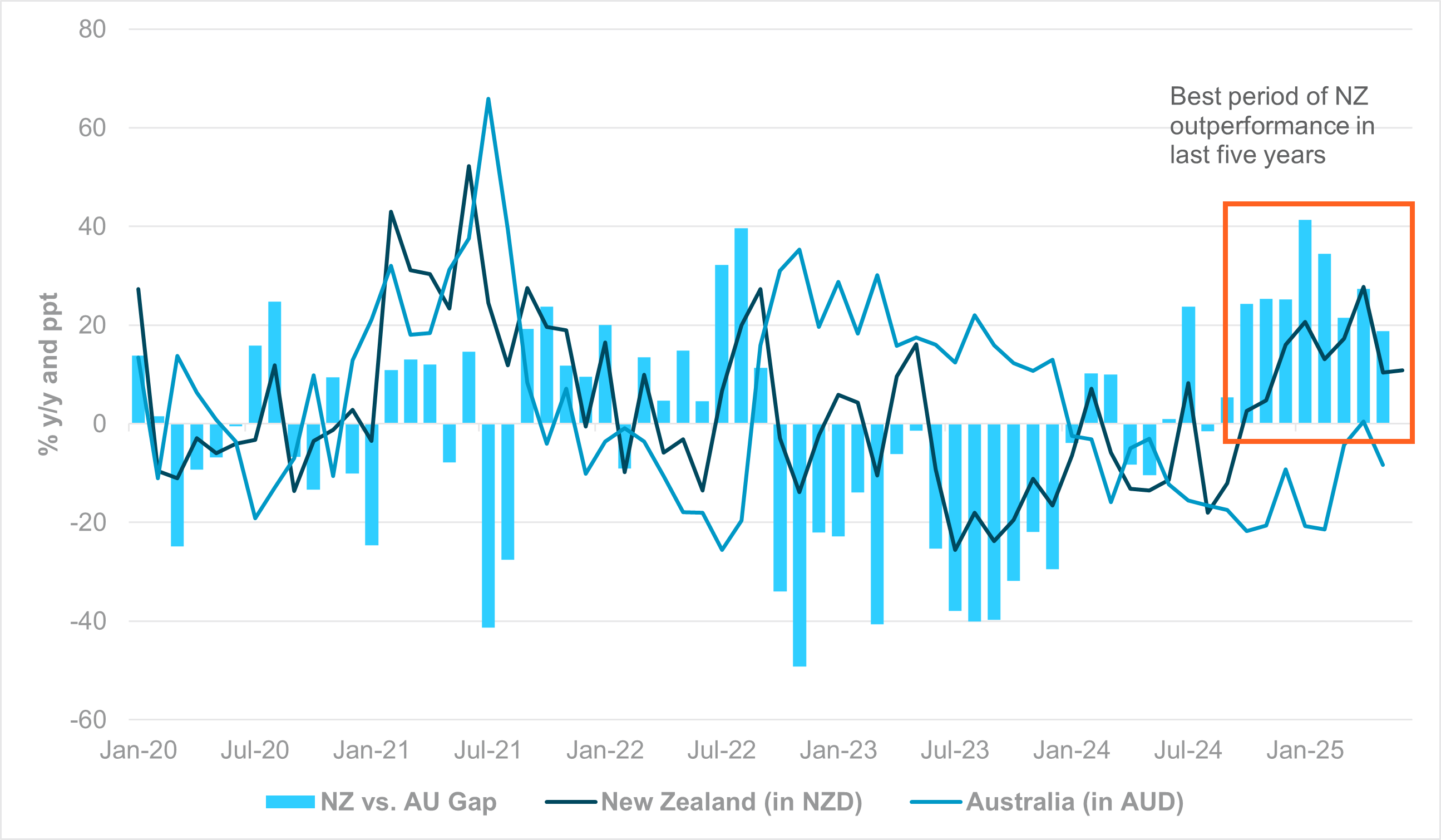

EXHIBIT #3: NEW ZEALAND AND AUSTRALIA EXPORT GROWTH TO CHINA

Source: BNY, Macrobond

Our take

During the years of high single-digit growth for China, which drove a commodity super-cycle led by real estate investment, soft-commodities often played second fiddle to industrial commodities. This was reflected in the terms of trade for the likes of the New Zealand dollar, even though the currency at various points essentially became a “protein and dairy” currency. Moreover, services demand, with linkages to food products, is an area of volume (rather than price) growth this year in China and the government is clearly intent on boosting interest further. This is already coming through in “hard data,” as New Zealand’s export growth to China is strongly positive, and on a relative basis is enjoying the best period of outperformance over the corresponding Australian number this decade (Exhibit #3).

Forward look

During the years of high single-digit growth for China, which drove a commodity super-cycle led by real estate investment, soft-commodities often played second fiddle to industrial commodities. This was reflected in the terms of trade for the likes of the New Zealand dollar, even though the currency at various points essentially became a “protein and dairy” currency. Moreover, services demand, with linkages to food products, is an area of volume (rather than price) growth this year in China and the government is clearly intent on boosting interest further. This is already coming through in “hard data,” as New Zealand’s export growth to China is strongly positive, and on a relative basis is enjoying the best period of outperformance over the corresponding Australian number this decade (Exhibit #3).

Based on official releases and initiatives from Beijing over the past two weeks, we do not question the notion that China is looking to maintain or even strengthen growth momentum toward year-end. However, key messaging surrounding “combating involution” and household subsidies reinforces the case for increasing domestic demand through the fiscal and corporate channels. The market may have focused too much on traditional investment/infrastructure-based growth, which remains highly relevant for Beijing but is no longer seen as the marginal driver for better price and economic outcomes. Consequently, rotation into assets exposed to Chinese consumption, as opposed to commodities and industrial demand, is a clear theme for H2.