Premature to Call Time on US Exceptionalism

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 6 minutes

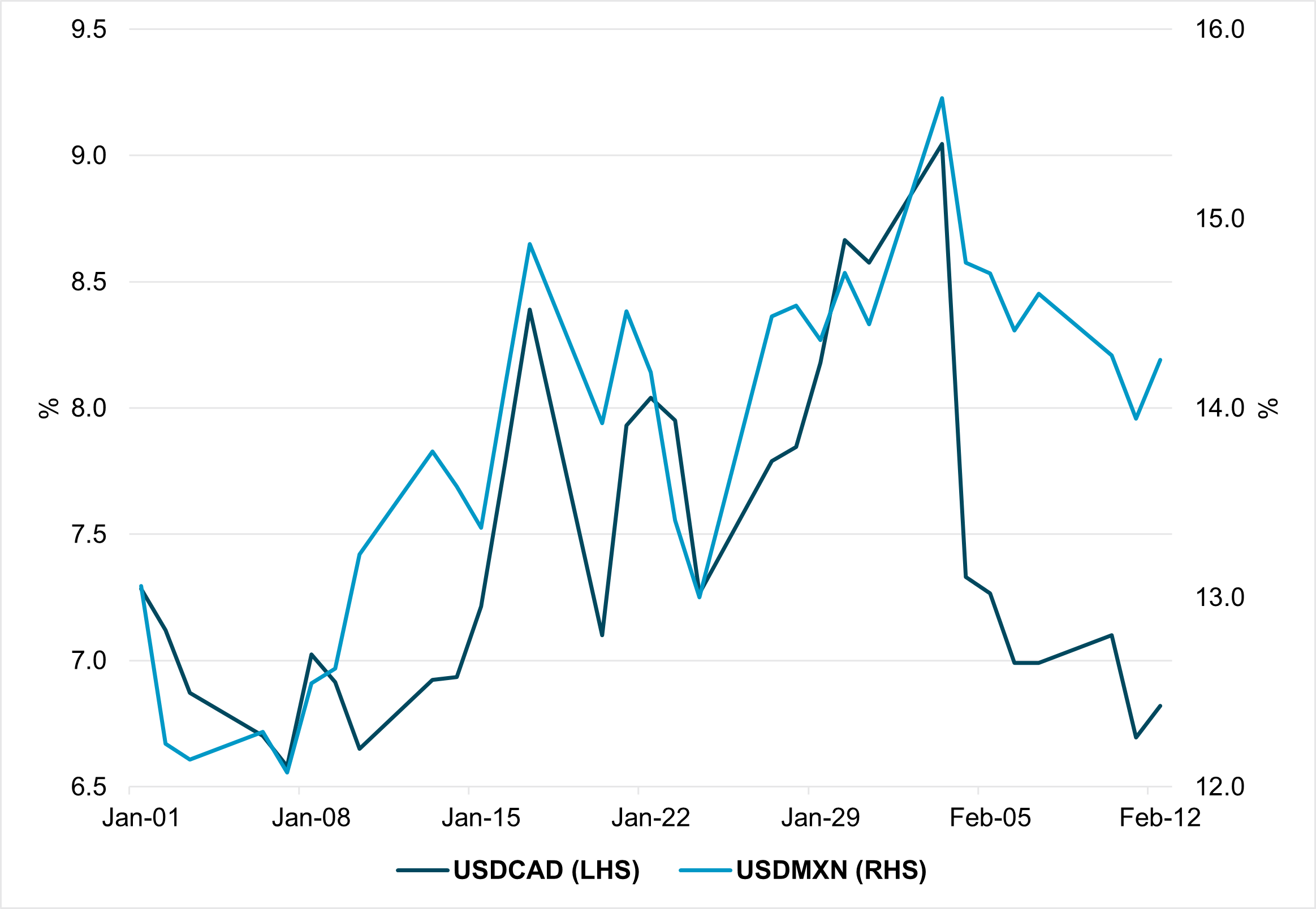

EXHIBIT #1: USDMXN AND USDCAD 1-MONTH IMPLIED VOLATILIY

Source: Bloomberg, BNY

Our take

The marginal impact of tariff rhetoric has diminished as investors gain confidence the US and key trade partners will reach a deal. Buoyed by last-minute – albeit temporary – arrangements between the US and its neighbours, markets believe there is little chance of large-scale and permanent tariffs. China has also been measured in its response. There are few signs of macro data strain, leading to hopes of a low-volatility “goldilocks” environment. USDMXN implied volatility is off its highs, while USDCAD has fully normalised, indicating the market doesn’t expect renewed stress as Mexico and Canada’s grace period ends. We believe this is a highly optimistic, even complacent take on US policy. Normalisation of implied volatility in EUR, CNH and other exporter currencies does not reflect the risk of tariffs on specific sectors, such as automobiles, pharmaceuticals and semiconductors. All have been highlighted by the US administration, and sizeable tariffs would have a material impact on European and Asian balance of payments.

Forward look

Tariffs as a part of industrial and even foreign policy are here to stay. Even if front-end volatility normalises periodically, the volatility term structure of G10 currencies should permanently re-price to reflect sustained uncertainty. The corresponding tightening in financial conditions will require a corresponding offset by affected central banks, which means that the risk to monetary policy and rates remains to the downside relative to the dollar, as US growth is less trade-dependent. With global trade less reliable, European and Asian exporters will need to focus more on domestic demand. This will not be a smooth process, with additional risk premia from FX and bond markets, though exporter economy restructuring will be positive in the long run. We expect G10 FX implied volatility to rebound to last quarter’s highs, and the dollar will remain resilient unless tariffs affect US growth adversely.

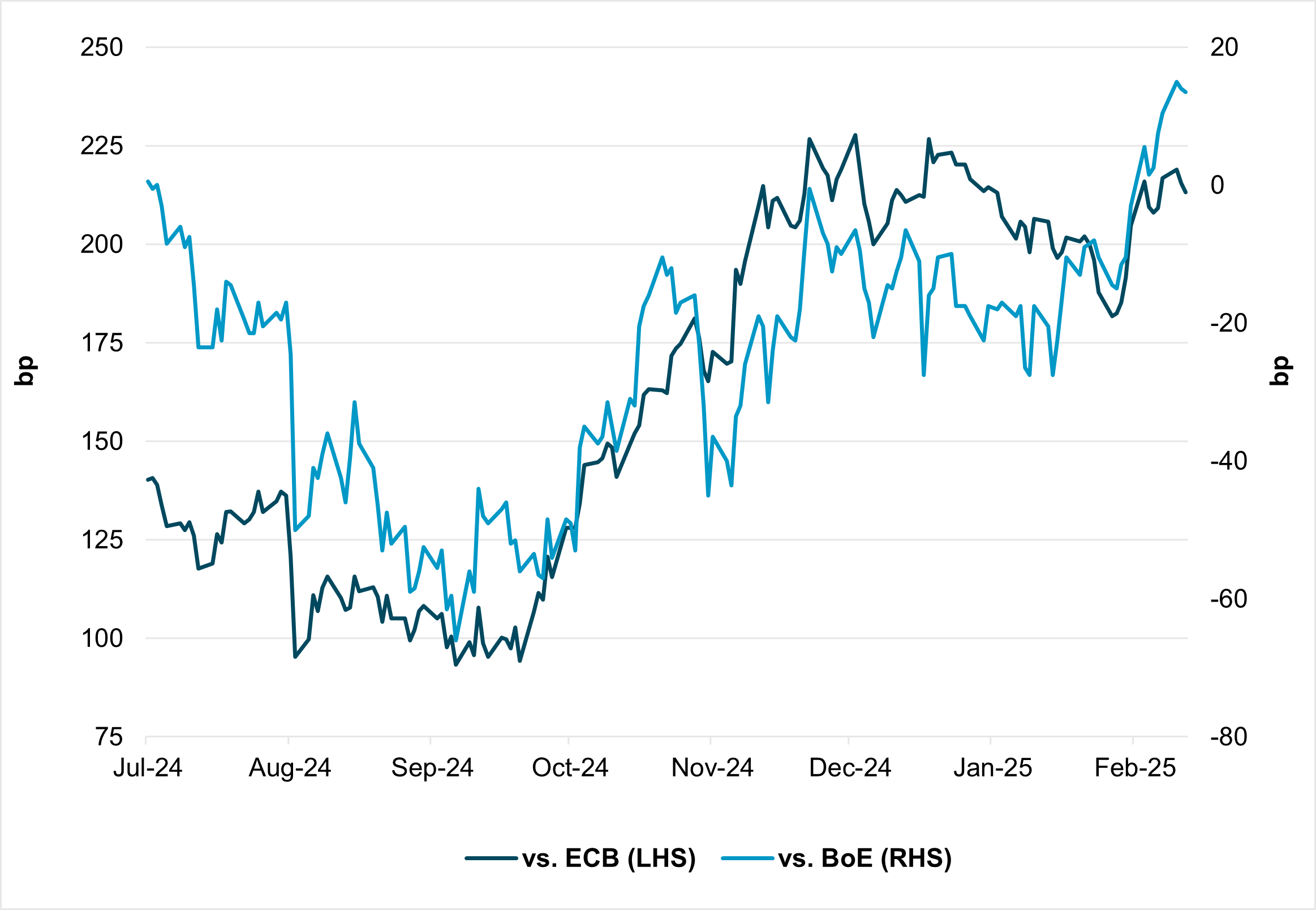

EXHIBIT #2: SUSTAINED IMPROVEMENT IN POLICY DIFFERENTIALS FOR THE FED

Source: Bloomberg, BNY

Our take

Based on growth and inflation differentials, the US remains the outperformer globally, but the dollar has stopped responding in kind, as the reaction to the January US CPI has shown. So far this year, the strongest periods for the greenback have been associated with “risk-off” moves based on tariff news. Given elevated valuations, the reluctance to pursue additional positioning in a “risk-on” environment too is understandable. Our flow data indicate that there has been a material pullback in cross-border EUR hedges, even though risks to Eurozone growth remain to the downside and the political situation in Germany is proving more difficult than we envisaged. Meanwhile, several developed market central banks, such as Sweden and Canada, have warned that their base case for a cessation in their easing cycles will be undermined by tariffs. The risk to the Fed is in the opposite direction, whereby strong data performance obviates the need for cuts. Gains in policy differentials are material (Exhibit #2) and this needs to be reflected in the dollar’s near-term performance.

Forward look

We expect tariff risk to continue supporting the dollar, though much of the risk premia should also be reflected in implied volatility and other asset markets. We continue to expect the DXY to peak at around 110 in 2025, but the risk remains to the upside based on policy differentials alone and will be exacerbated by tariff risk. In many respects this is also necessary, as dollar valuations will act as a restraining factor on the US economy, directly through lower global earnings for US companies, and indirectly through contributing to higher yields in the US Treasury market as reserve managers face drawdowns. Positioning is a hindrance to dollar strength, though our data indicate cross-border hedges of EURs have eased year-to-date, which supports our view that the dollar can make another run towards parity against the euro this quarter.

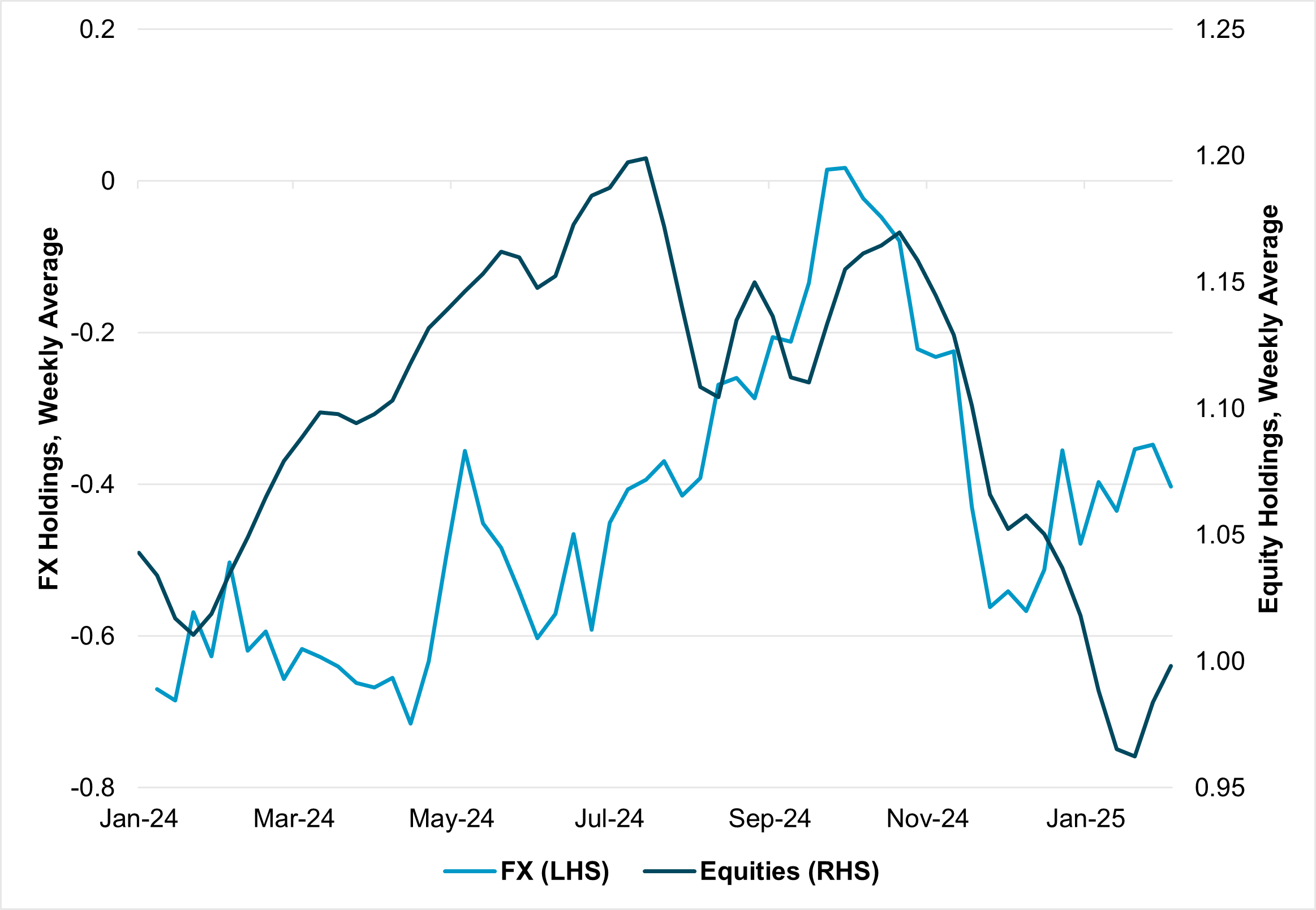

EXHIBIT #3: APAC FX AND EQUITY HOLDINGS

Source: BNY

Our take

EM currencies will struggle amid tariff risk and the experience of USDBRL and USDTRY shows the bar remains high for carry names to overcome dollar demand. However, change is afoot in APAC given newfound optimism in China. Led by the technology sector, the Shanghai composite and Hong Kong Tech Index are nearly 4% and 11% month-to-date, respectively. Retail and official demand domestically have outweighed foreign selling pressure over the past few months across the region. This could be the beginning of the return of the animal spirits in Chinese equities, and cross-border investors will come under increasing pressure to participate. However, APAC currencies have been relatively resilient despite elevated DXY and higher US bonds yields, supported by valuations and light holdings (Exhibit #3).

Forward look

Chinese equities will likely be supportive in the near term with the return of foreign investor interest. iFlow equities’ scored holdings posted a sharp reversal in recent weeks after an extended period of risk reduction in Q4 2024, but holdings remain below the long-term average. That said, a rising equity market might not necessarily mean a strong regional currency. Policy differentials will continue to support the dollar, while increased hedging demand and fiscal loosening will likely weigh on general emerging market flows and APAC currencies.

Our asset flows point to a strongly risk-on theme, and this is now extending into the FX market. However, core relationships between the dollar and risk sentiment have shifted compared to the past year and first days of the inauguration. This is not sustainable given the current policy and growth mix in the US, which continues to support US exceptionalism based on yields and data. We expect tariff risk to return to the fore, to be reflected in sharp gains in short-dated implied volatility in core dollar pairs. The dollar will only base when the combination of a strong dollar, higher yields and trade policy-induced uncertainty sufficiently tightens financial conditions to restrain US growth. Consequently, we believe markets will maintain or add to positions in short-dated dollar options, while looking to lock in gains in equity positions outside the US through FX hedging and outright holdings reduction later this quarter.