Month-end Rebalancing Analysis: March

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

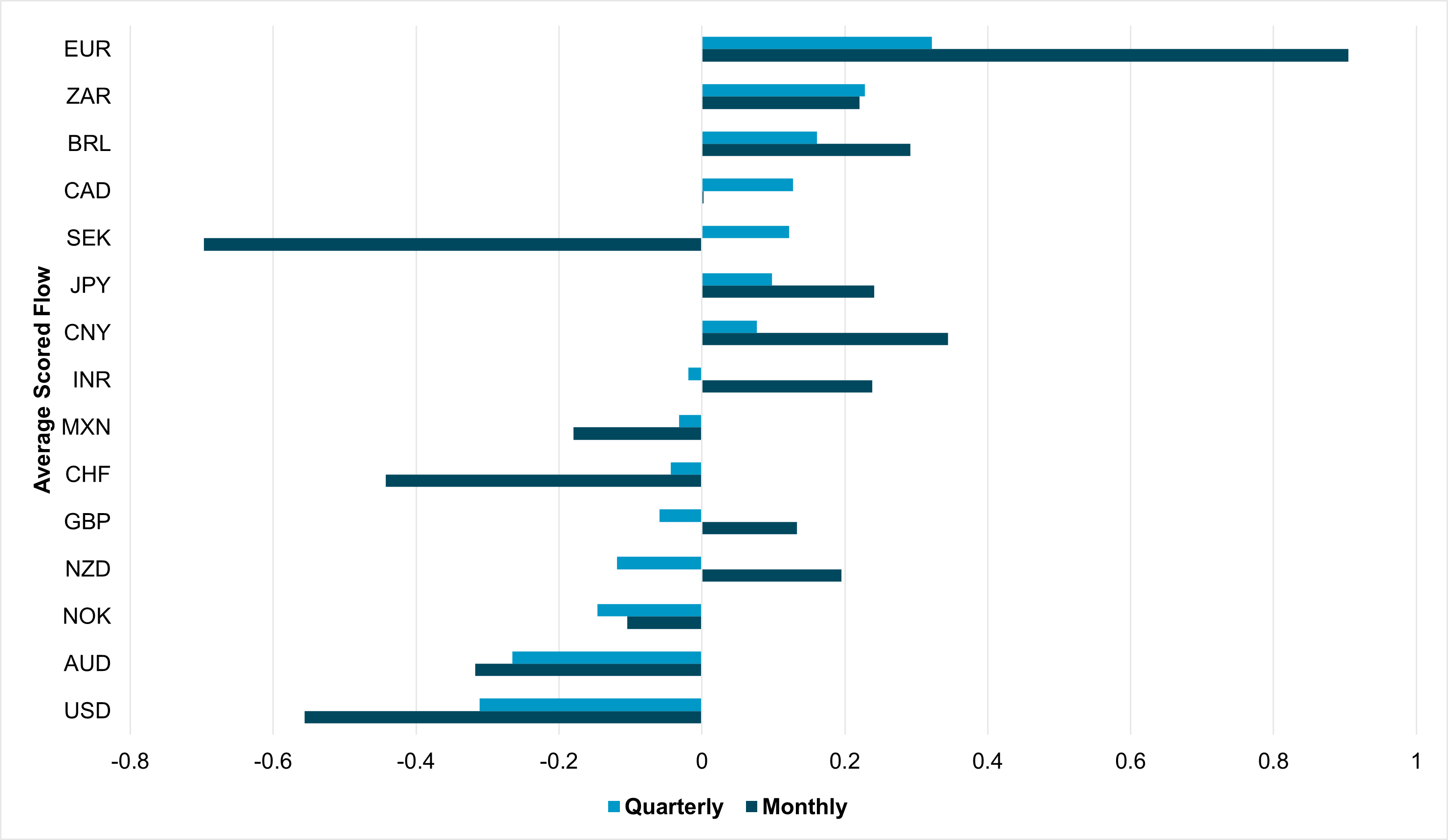

EXHIBIT #1: MONTHLY AND QUARTERLY REALIZED FLOWS AS OF MAR. 25

Source: BNY

Our take

The strong asset movements in the past six weeks may lead to significant month- and quarter-end rebalancing demand. Based on our Q1 data, realized FX inflows were very strong in the EUR, mostly at the expense of the dollar. G10 commodity bloc currencies such as AUD, NZD and NOK also struggled due to global growth concerns. While risk appetite was soft, the strength in ZAR and BRL flows this quarter is a surprise, indicating carry trades can continue to perform, especially in a soft dollar yield environment. The biggest reversal in March took place in the SEK: initially a beneficiary of the European re-investment theme, the currency remains the third-best bought G10 currency in Q1 but is by far the most-sold currency in March.

Forward look

Even net of underlying asset performance, EURUSD selling – a reversal of the monthly and quarterly trend – will be the most material flow. This is in line with our fundamental view on valuations and economic performance, as Eurozone equity markets could struggle up ahead as downside risk to earnings is aggravated by weaker FX translation of overseas profits. While we still see potential for overseas allocations in Eurozone equities to grow, FX hedge ratios will likely rise due to current EUR levels. Meanwhile USD-based investors will also likely step up defensive positioning ahead of tariff announcements in early April, and adding to dollar holdings is an efficient hedge. Comparatively, bond market returns were more subdued, and any rebalancing pressure largely reflects realised currency flows rather than strong underlying moves in duration.

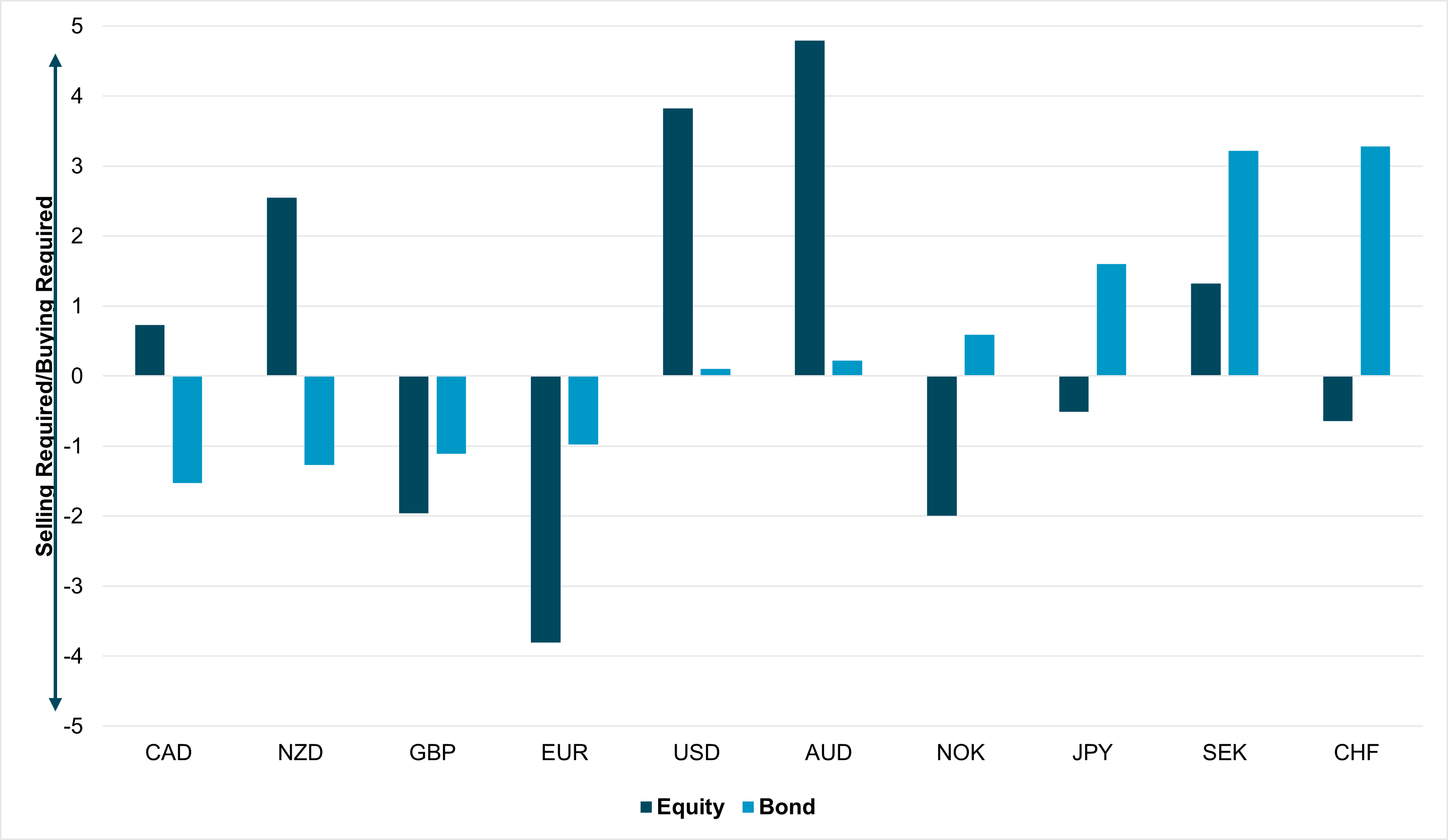

EXHIBIT #2: G10 FX MONTH-END REBALANCING SIGNALS

Source: MSCI, BNY

Our take

Within G10 currencies the strongest signal generated is EUR selling to rebalance high-performing equity portfolios. GBP and NOK will also be under pressure, with the former due to strong realised currency flows, but NOK sales for rebalancing purposes are almost wholly attributable to gains in the equity markets. The currency has struggled throughout the quarter, but perhaps in another indication of earnings translation having a positive impact, month-to-date the benchmark Oslo index is up close to 4% (double the DAX’s gains), leading to currency sales for rebalancing purposes.

Purchase flows due to equity rebalancing supports the USD, NZD and AUD. USD and AUD demand reflects soft equity markets and strong outflows this month and quarter, however NZD rebalancing is due to weak performance in local equities: for example, in absolute terms the NZ50 index has already underperformed its Australian counterpart by 10pp year-to-date.

In fixed income, we identify SEK and CHF purchases: the former due to heavy realised selling of SEK in March, but the latter due to weak bond market performance as the SNB signals an end to easing.

Forward look

Month/quarter rebalancing signals are mostly in line with our fundamental views. U.S. economic resilience continues to hold up well, and we believe some dollar purchases are necessary to reflect the current U.S. data and policy outlook. We believe EUR valuations have peaked, while EUR holdings have also normalised on an aggregate and cross-border basis. GBP also looks rich at current levels and yesterday’s fiscal statement will not lead to any improvement in stagflation expectations for the U.K. By contrast, SEK and CHF will continue to benefit from Eurozone reflation, and valuations are much more attractive than the EUR.

Elsewhere, we continue to see value in AUD and NZD as global commodity prices base and China’s recovery begins to generate better momentum in the region. However, additional NOK selling does not offer good risk- reward as today’s Norges decision will likely point to a central bank that will be extremely careful in easing, while the currency will also benefit from a base in oil prices and strong domestic fiscal stabilisers.

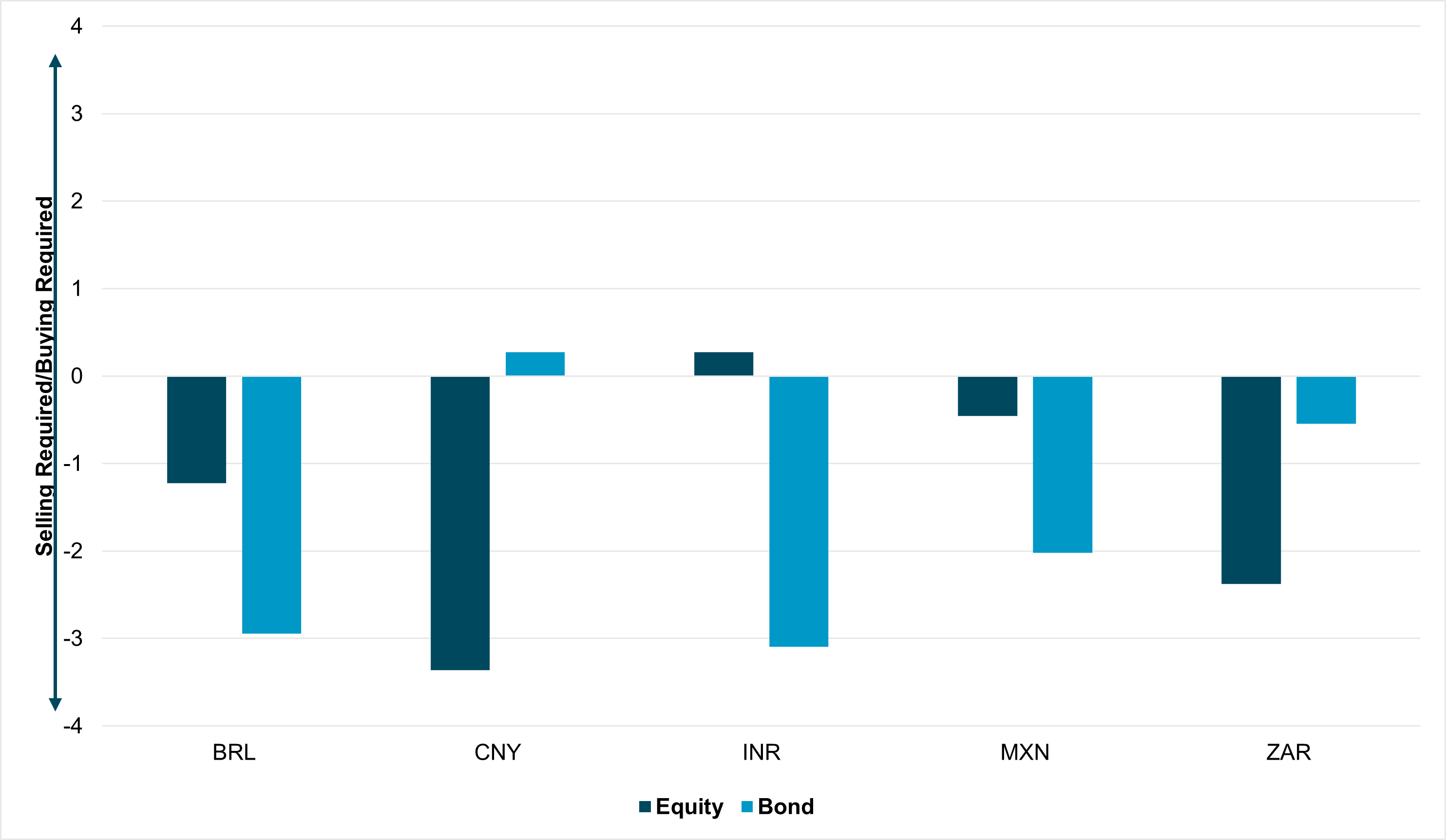

EXHIBIT #3: EM FX MONTH-END REBALANCING SIGNALS

Source: MSCI, BNY

Our take

Selling of CNY is the most significant EM FX signal into month-end. Unsurprisingly, this reflects the strong gains in equity markets while realised FX flow was also firm. ZAR also faces equity-based rebalancing, with currency flows and equity market performance equally strong. Meanwhile, BRL, INR and MXN all face outflow risk, but only the sales in the latter can be attributable to asset performance as realised flows in MXN were soft in March and through the quarter. High real yields and prior underpositioning continue to support local fixed income markets, with the Bloomberg Aggregate Mexico (unhedged) index up close to 6.5% year-to-date.

Forward look

EM currencies continue to hold up well despite the soft outlook for global growth and ongoing tariff risk. We believe selling of CNY is in line with fundamentals as China seeks to reflate its economy. However, BRL, INR, MXN and ZAR are all essentially carry trades, with MXN also exposed to renewed tariff risk as key dates arrive in April. Our iFlow Carry index has been improving of late but has failed to enter statistically significant and positive territory. This shows carry conviction has been soft, and we believe rebalancing flows favouring additional hedging can extend, especially if markets also believe that the dovish repricing in the dollar has run its course for now.

Buying of the USD and G10 commodity currencies, and selling of the EUR and EM currencies is the main theme into month-end. With few exceptions, these adjustments largely reflect underlying asset performance. Even after seasonal rebalancing, we expect EUR and EM FX weakness to continue as valuations and event risk pick up in early Q2.