High-beta FX Stumbles Amid Dollar Pullback

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

Commodity FX to struggle despite attractive valuation

Dollar weakness an earnings threat

Yields matter far more than terms of trade prospects

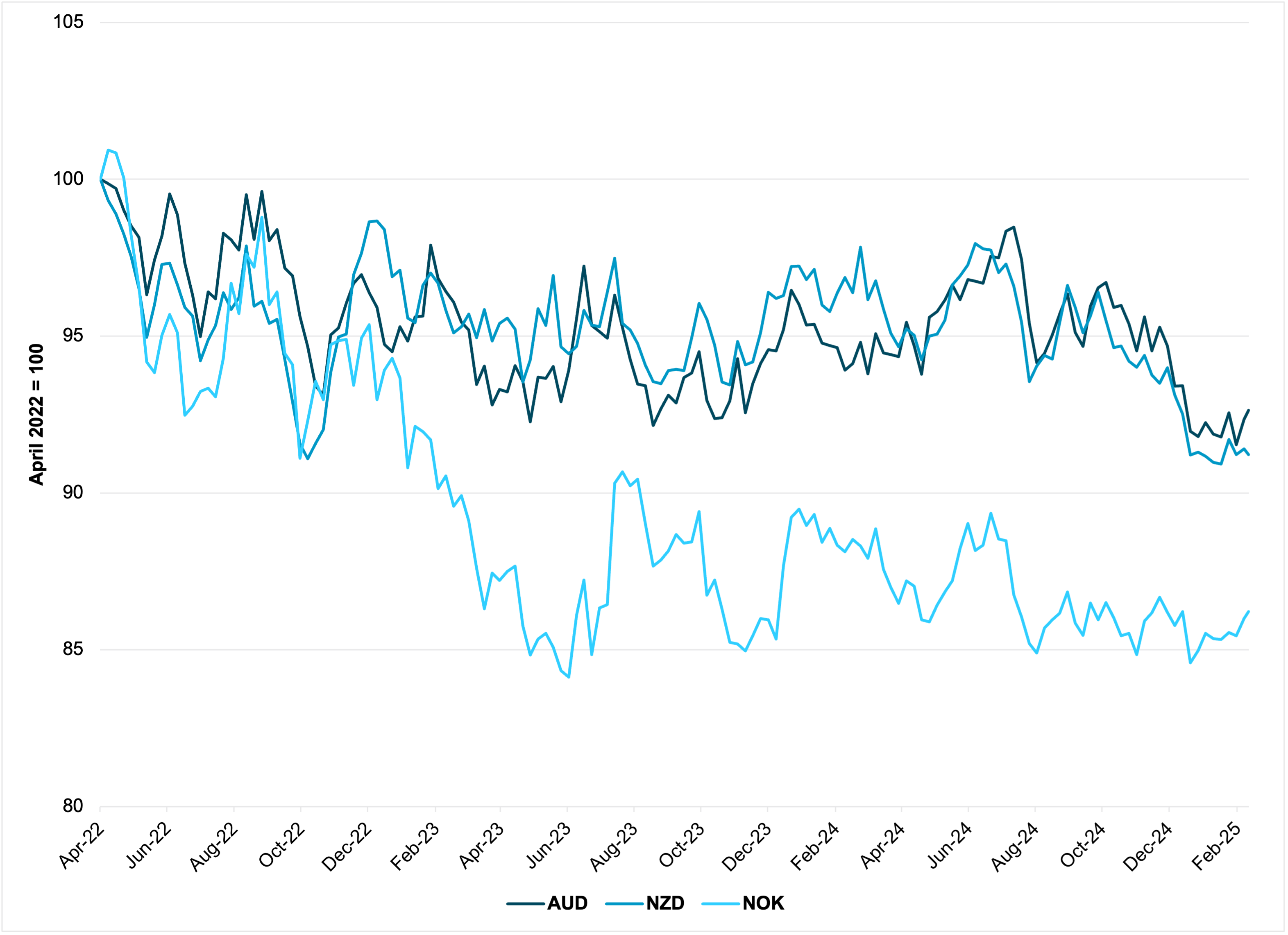

EXHIBIT #1: AUD, NOK AND CAD NOMINAL EFFECTIVE EXCHANGE RATES

Source: Bloomberg, BNY

Our take

Risk appetite remains relatively buoyant based on stock market performances. Markets are starting to see a “goldilocks” environment in the US and Europe as supply pressures ease, while a new narrative in China raises hopes of stronger growth. Normally, this would support demand-dependent assets like commodities and consequently improve terms of trade for exporters. As markets look to further fade the US dollar’s current valuations, there is a case for nominally undervalued (Exhibit #1) G10 commodity bloc currencies to benefit, especially from healthy reflation in China and Europe. “Non-dovish” easing by the RBA, RBNZ and Norges Bank also provides a policy anchor, and iFlow indicates a positioning recovery is viable, especially for the antipodeans. While sympathetic to these fundamentals, we believe these currencies are a value trap.

Forward look

Current policy paths for these central banks are highly contingent on domestic considerations. Norway and Australia continue to face stagflation pressures, with non-commodity productivity supporting non-tradables inflation. We see value in NZD, but our reasoning has long been based on a rare case of domestic fiscal consolidation supporting real rates. However, FX markets continue to express a preference for high nominal yields. Crucially, there remains scant evidence of demand picking up to fundamentally support terms of trade for G10 commodity currencies. Otherwise, the central banks of the main commodity consumers, like the ECB and PBoC, would not be pushing for more policy accommodation. To realise partial value in these currencies, we would only look at relative value positions, especially against European currencies like the EUR and GBP where growth and policy risk remain to the downside.

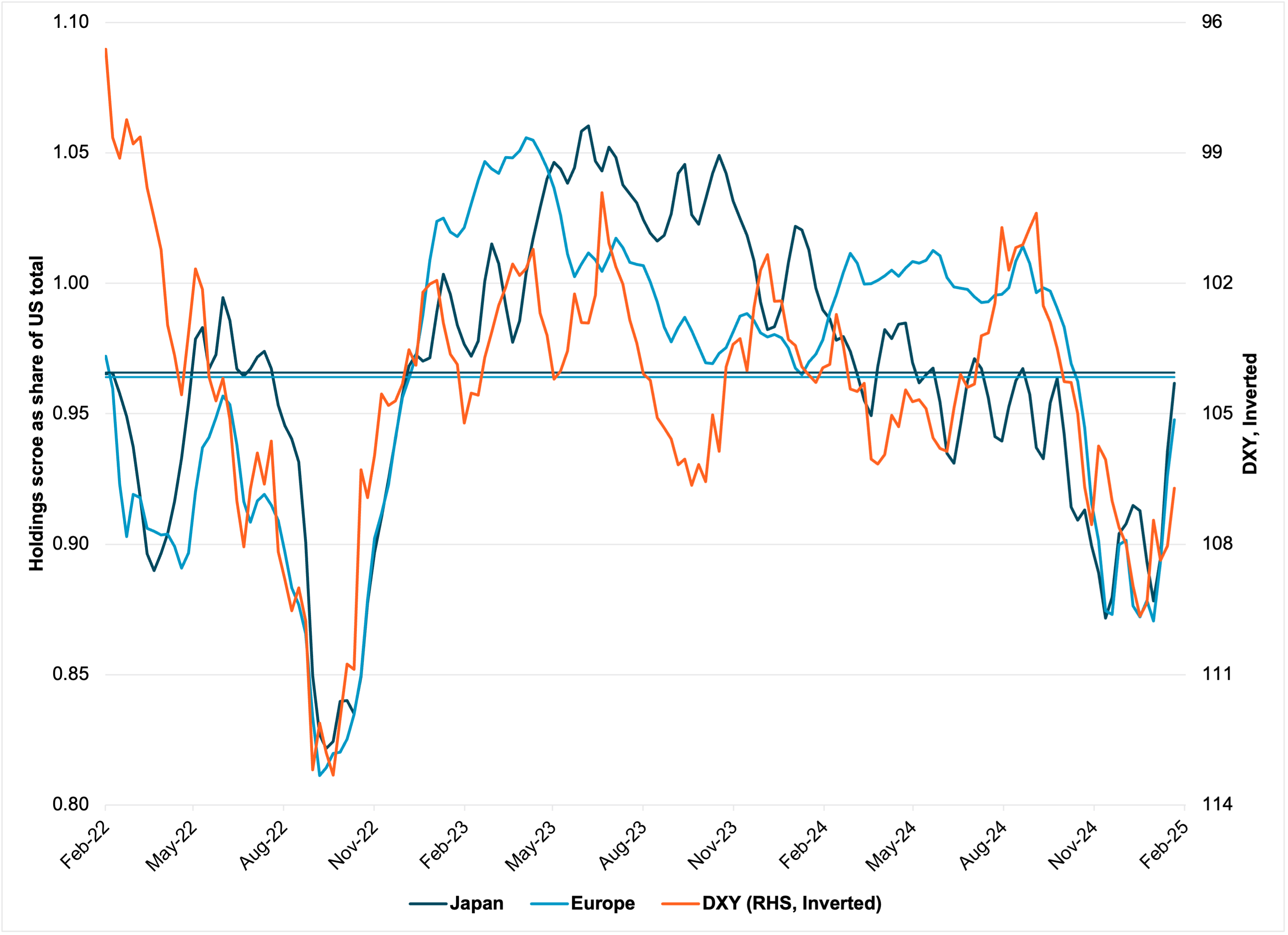

EXHIBIT #2: EUROPEAN AND JAPANESE EQUITIES' POSITIONING RECOVERY VS. DXY

Source: Bloomberg, BNY

Our take

There has been significant re-rating of European equities on the back of changes in the regional security outlook, prompting a rethink of growth fundamentals. While not in Europe’s best interests, the market sees positive upside risk for earnings on both the supply and demand side. Pricing out the risk of renewed supply disruption is positive, albeit marginal given the comprehensive reconfiguration of Europe’s energy exposures in recent years. Meanwhile, there has been a surge in defence and aerospace performance in anticipation of a sharp rise in defence spending – funded by a rise in public investment as domestic savings are put to work. Although such injections are sector-specific, it supports our narrative that Europe must ramp up investment growth to achieve strategic autonomy.

Forward look

We already have reservations about the speed of the run in Eurozone equities and the further its holdings diverge from the dollar, the more a weaker EUR could be required to compensate. iFlow shows that recent re-rating and outright inflows have helped close an equities holdings gap for the Eurozone and Japan relative to the US. Both are now approaching their three-year average, but the dollar has managed to remain relatively resilient, which would not heavily impact earnings translation. The last round of “outperformance” in equity holdings for Japan and Europe, in 2022-2023, was during a broader market selloff when earnings translation was not considered strong enough a buffer. In the second half of 2023 as sentiment recovered, Japanese equities performed exceptionally well as the DXY renewed its surge. Current developments are positive for potential growth over the longer term, but the export sector will not move away overnight, and investors need to manage FX risk while adding to European equity exposures.

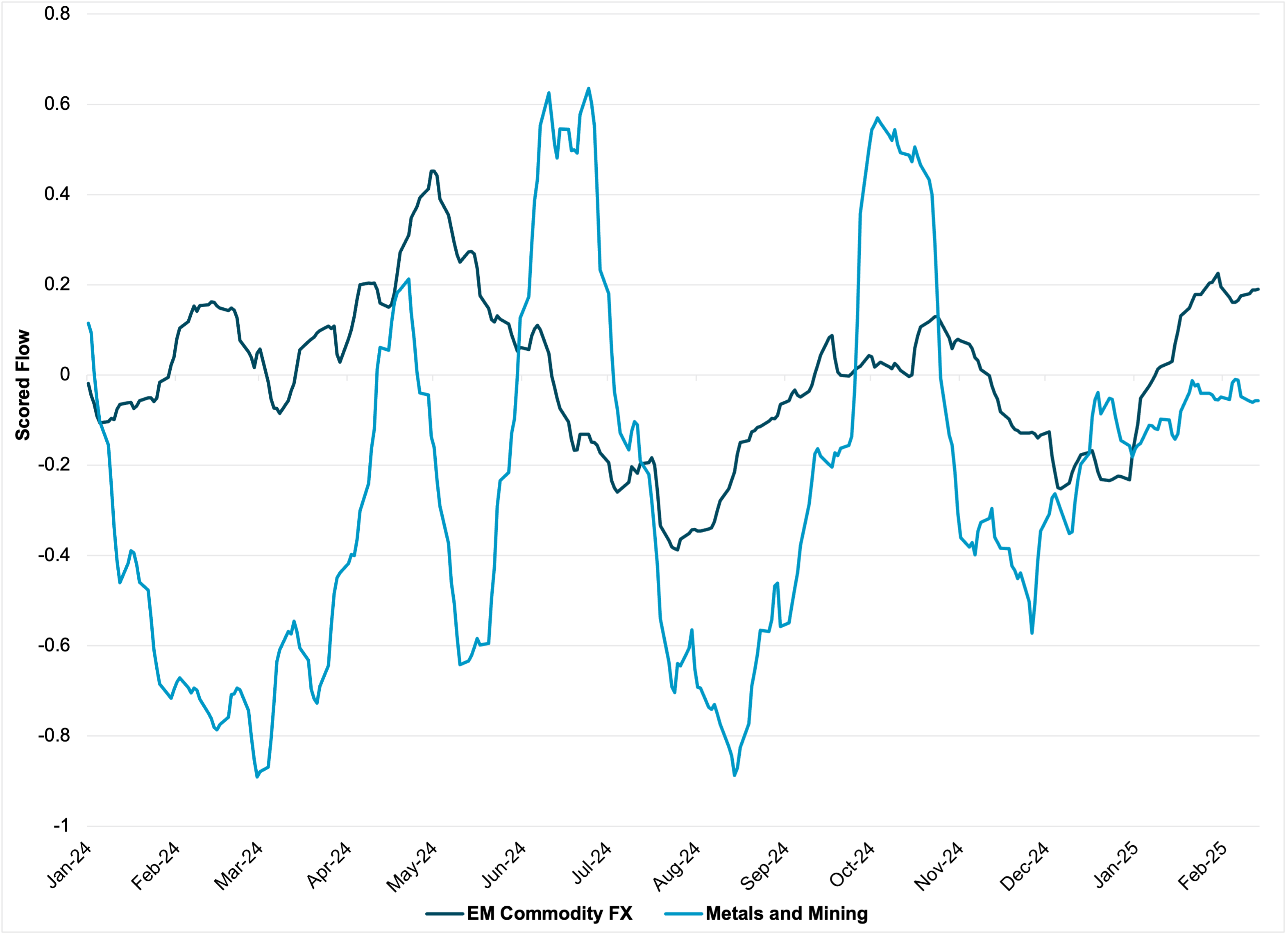

EXHIBIT #3: EM COMMODITY FX VS. EM METALS AND MINING EQUITY FLOW

Source: BNY

Our take

In contrast to G10 commodity names, iFlow indicates that there is much better interest for EM equivalents, including ZAR, CLP and BRL (which comprise iFlow’s Commodity FX basket). February has seen smoothed flows (monthly average, Exhibit #3) reach the best levels since Q2 last year, even in the face of a less dovish Fed. Crucially, there are also signs of recovery purchases in the metals and mining sector for EM equities, indicating improving prospects for balance of payments and overall terms of trade. While there is less of a value trap risk for EM commodity FX, we are similarly cautious regarding current flow drivers and would avoid seeing currencies as a proxy for global demand and reflation.

Forward look

Similar to their G10 counterparts, we note that domestic factors are far more relevant to interest. EM central banks with commodity exposures have led the way over the past cycle in maintaining high real rates, not just in the face of external policy pressures from elevated Fed rates, and ongoing fiscal challenges domestically. The recent rate hikes by COPOM and SARB’s inflation target adjustments last year are just two examples. Marginal commodity demand from China remains essential, but the risk is no longer to the downside. Crucially, high domestic nominal rates and moderation in easing is supporting a light recovery in carry positions, which have struggled over the past quarter. These currencies are also less exposed directly to tariff issues globally. BRL and ZAR should remain well-anchored, subject to domestic fiscal developments, but we would closely monitor positioning accumulation and the risk of a hawkish Fed pivot.

Several narratives have continued to support risk appetite, mostly fueled by expectations of higher growth in Europe and China. The former fueled by a rapid change in the security situation and the latter by AI-driven productivity growth. However, organic underlying household demand is not showing any improvement in either economy. This has undermined the case for currencies normally associated with better growth. We still expect oil-exposed currencies to struggle, while industrial commodity producers require support from high nominal rates, which in turn restrain domestic growth. Lack of associated top-line growth will challenge equities up ahead, especially in markets which traditionally rely on a strong dollar to generate export earnings. Although we expect the dollar to peak this year, the factors behind recent weakness are discrete and difficult to extend without clear signs of demand improvement.