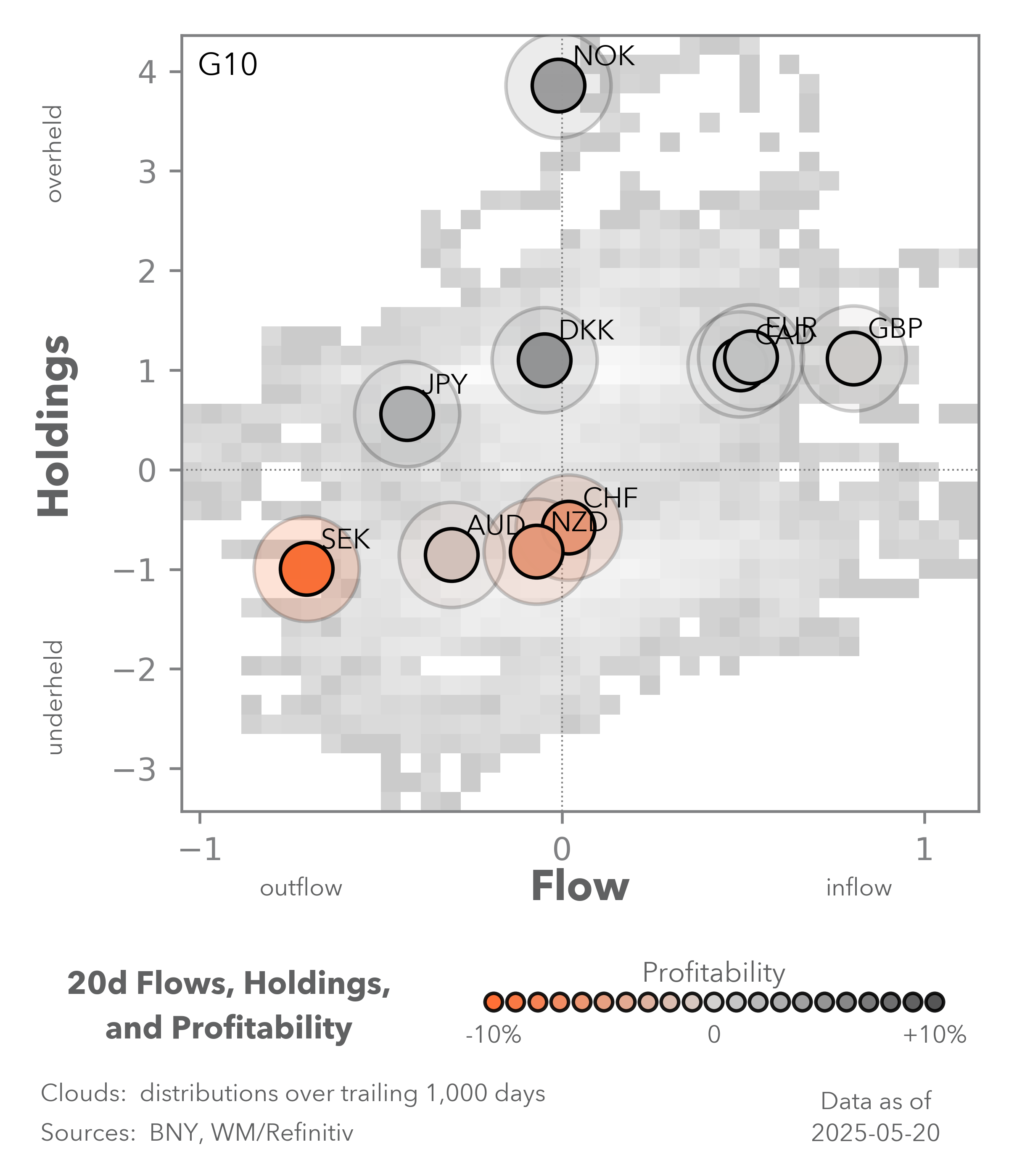

G10 reversions and APAC hedging

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

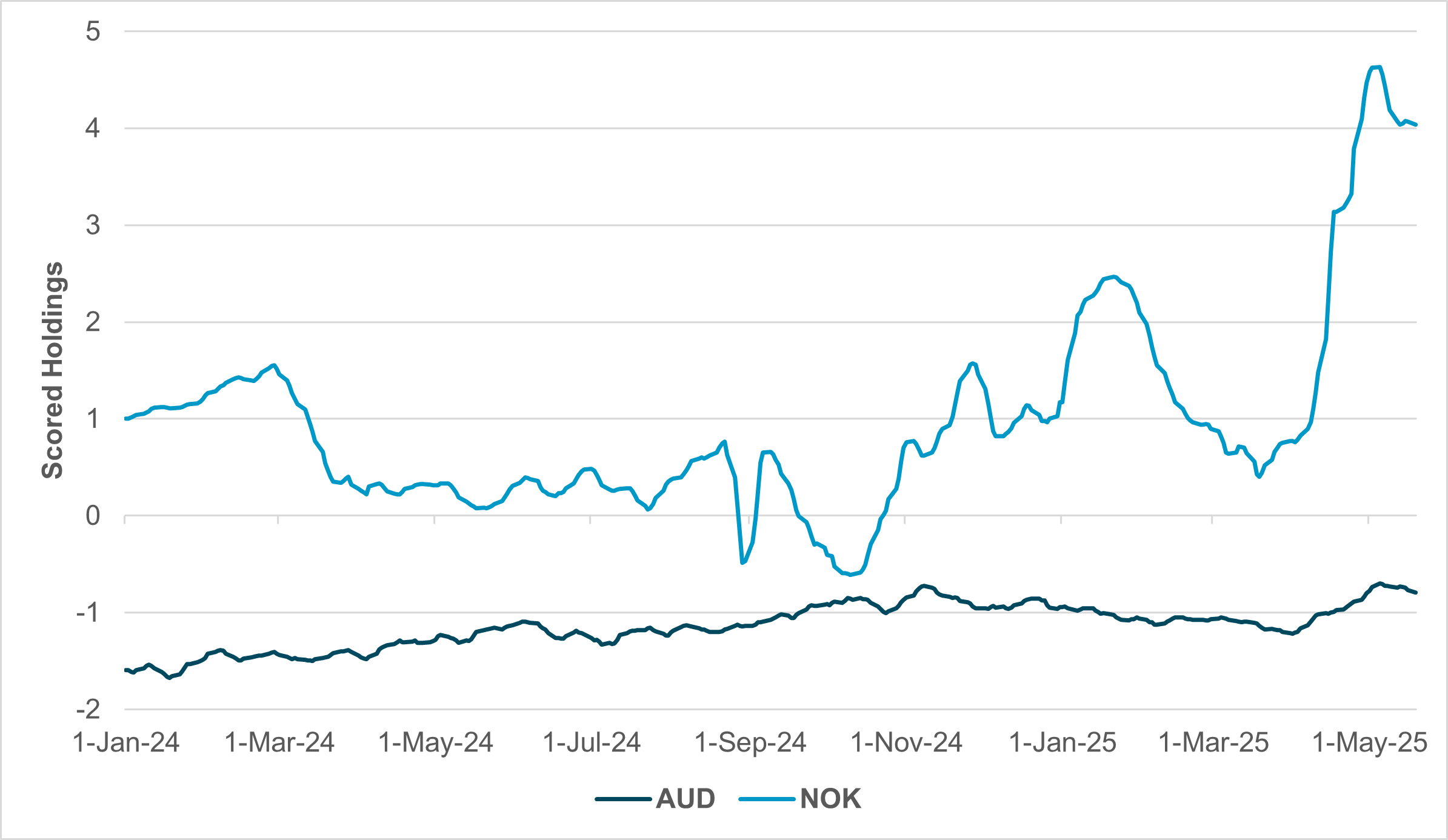

EXHIBIT #1: NORGES BANK IS THE “LEAST DOVISH” BUT HOLDINGS LEVELS DIFFICULT TO JUSTIFY

Source: BNY

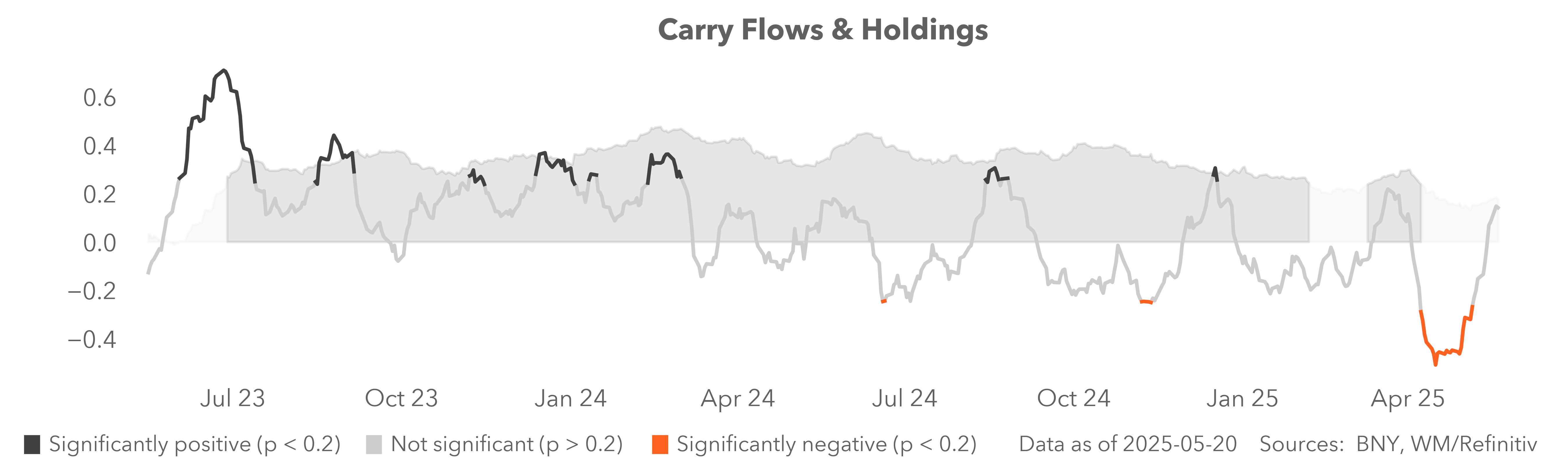

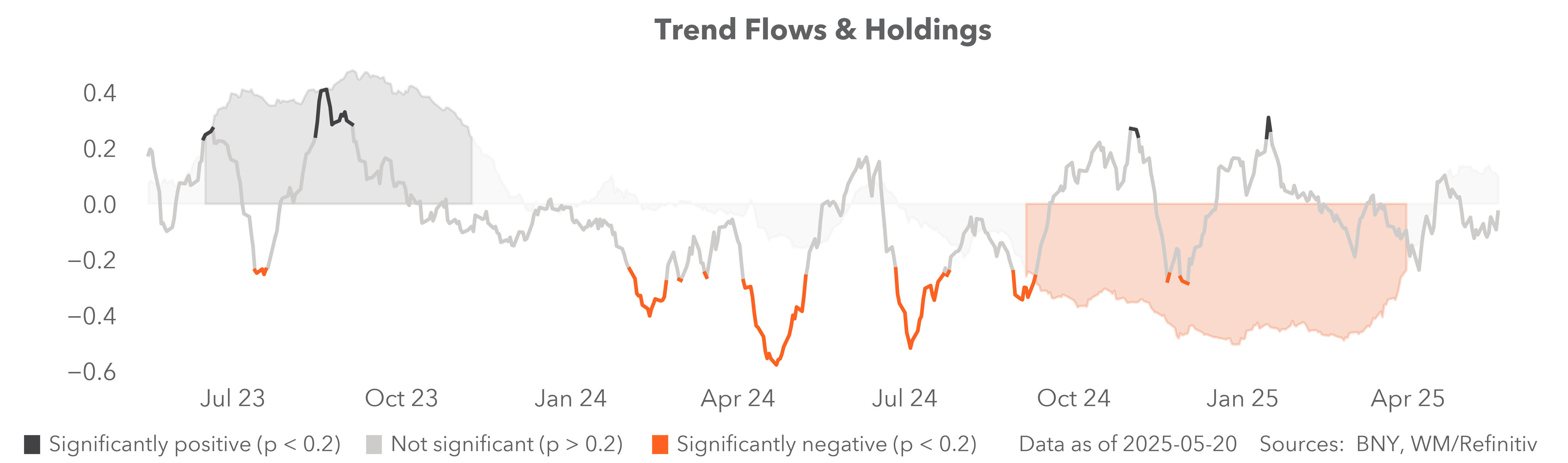

Our take

The main policy surprise this week was from the Reserve Bank of Australia. Contrary to expectations of a “hawkish cut,” which generally characterizes central banks dealing with stagflation, the RBA even discussed a 50bp cut and chose to overemphasize the downside impact of a trade war. We question whether this stance is sustainable given the structural factors driving inflation in Australia, but the market has re-priced accordingly and the currency was one of the worst performers in G10 in recent weeks, with holdings set to fall close to the one-year average (Exhibit #1). For all the current misgivings over the dollar and U.S. Treasury markets, interest in “real protection” through owning commodity-linked currencies is weak. The only outlier in iFlow is NOK, but we see this as purely a policy play as it is possible Norges Bank will go through the entire cycle without cutting rates, despite their guidance. Even if this is the case and Norges remains the “least dovish” central bank, current positioning is excessive.

Forward look

FX markets look set on fully reversing EURNOK’s gains in the aftermath of “Liberation Day,” which explains the strong performance of NOK in recent weeks. However, we note that even if such reversion is achieved, it will still leave NOK richly valued and weaken the case for Norges to hold rates. Before recent easing, Australia and Norway were economies which struggled to deal with non-tradables inflation and even now, Australia’s annualized non-tradables inflation is running above 3% annualized, and the Q1 print was the highest since Q3 2023. Given Norges’ focus on domestic conditions, there should be far greater convergence in the policy outlook. Whether this is manifested in rate pricing or currency valuation adjustments, the current gap looks excessive. We remain sympathetic to the view that commodity bloc terms of trade will struggle in general, but they have been secondary to domestic monetary policy in the first place. Convergence will be led by AUD starting to hold its ground better, while NOK hedging will start to pick up in kind.

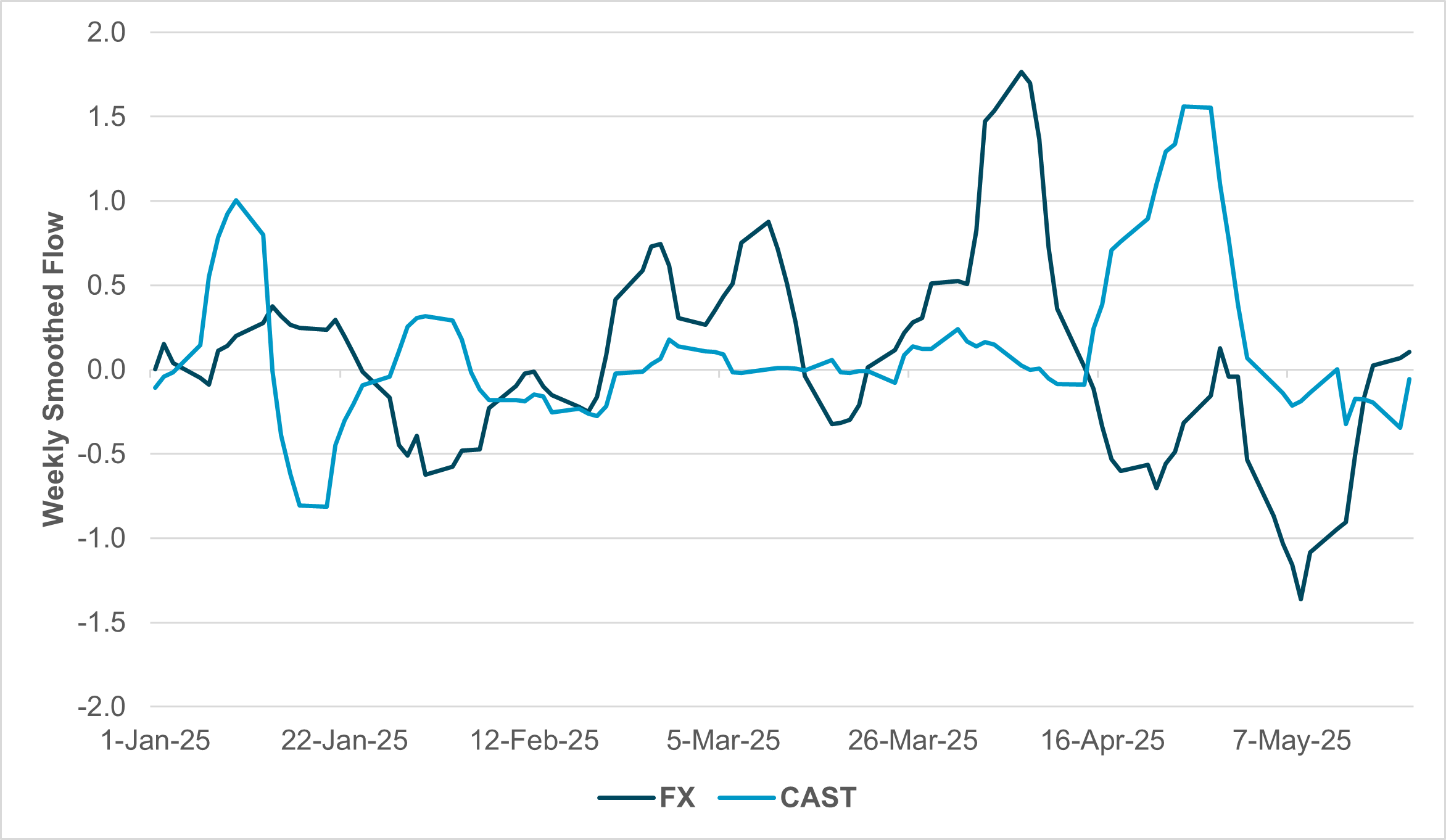

EXHIBIT #2: SMOOTHED FLOW IN JPY AND JAPANESE CASH/SHORT-TERM INSTRUMENTS

Source: BNY

Our take

The Japanese government bond (JGB) market has had its fair share of struggles this week as long-dated yields move to new highs. Inflation and policy dynamics have clearly shifted for the country and, for the most part, we expect policymakers will welcome the re-pricing as it is a sign of inflation premia picking up. In contrast to the U.S., Japan has sufficient savings to fund outlays so comparisons regarding fiscal sustainability and term premia have limited merit. The JPY is responding accordingly and recent USDJPY declines point to greater home bias as onshore savings pools seek to capture higher long-dated yields. However, iFlow highlights that front-end liquidity preference for the JPY has reversed (Exhibit #2). Forward/swap flow in addition to cash/short-term instrument transactions are starting to turn toward outflows. This marks a reversal of the strong liquidity preference established for Japan during the most extreme weeks of market volatility in April. Some mean reversion from an excessively overheld position was always the risk, but more recent outflows could point to concerns over near-term policy direction.

Forward look

We see the BoJ continuing its tightening path as soon as tariff risk dissipates. Changes in the long-end of the curve will have a greater bearing on their quantitative operations, but as this week’s market participants survey indicates, there is very little consensus on how the BoJ should calibrate future purchases. Outside of risk aversion episodes, liquidity preference is more sensitive to yields. The outflows suggest that there are some doubts arising over policy, especially with the lack of progress on trade negotiations. Meanwhile, the strength of the JPY will be seen as disinflationary in the short-term. “Profit-taking” on JPY cash during another move to 140 is understandable. However, an accord with the U.S. remains our base case and we continue to see the BoJ’s stance as an outlier. For long-term asset allocators, risk-reward is stronger in JGBs and greater inflows over time will continue to anchor JPY strength.

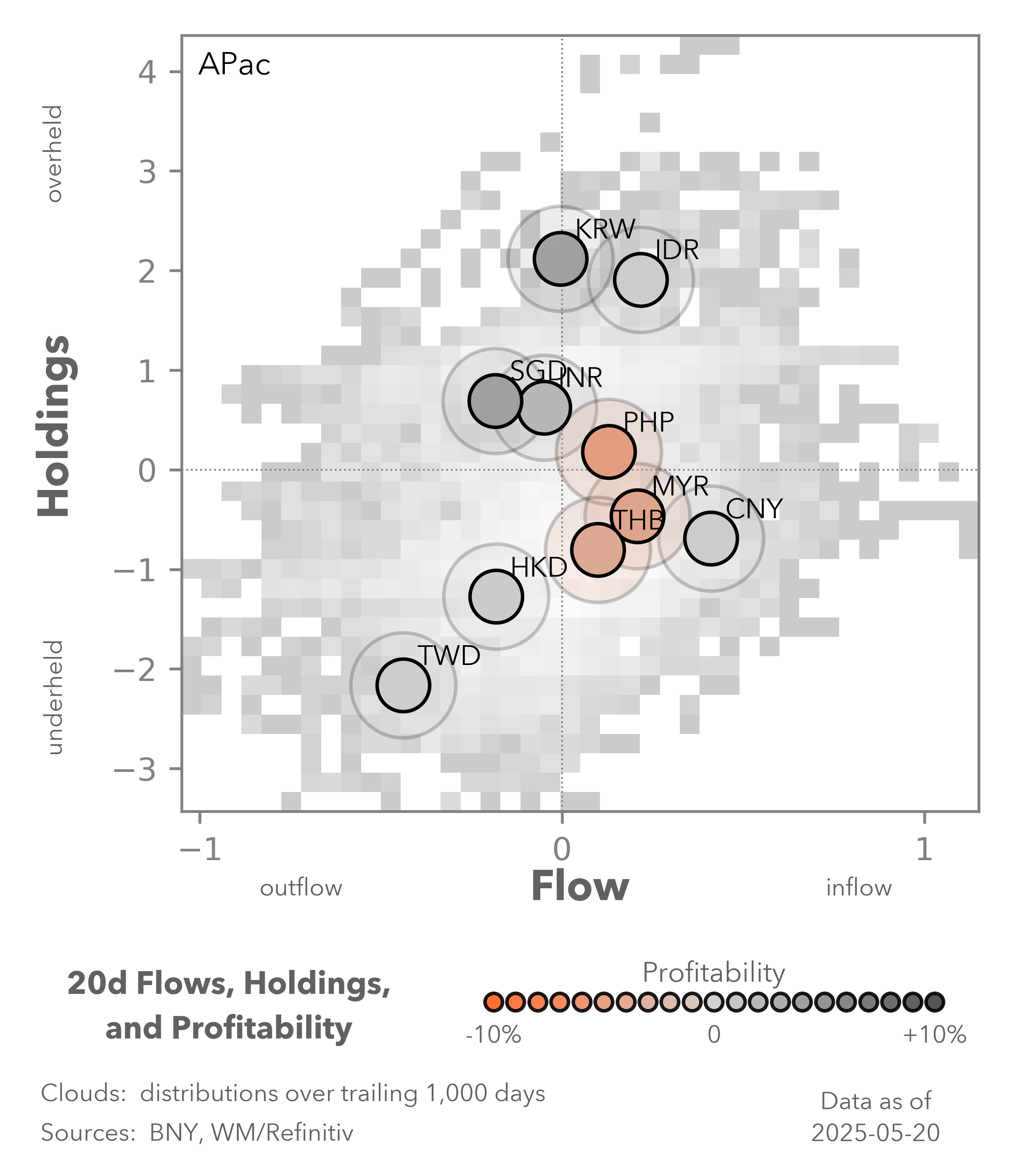

EXHIBIT #3: APAC FX AND USD HOLDINGS

Source: BNY

Our take

APAC regional equities rallied strongly over the past month upon the U.S.-China trade deal, with the reversal of foreign flows after a heavy sell-off in Q1 2025. Over the same period, APAC foreign exchange rallied too, normalizing from the dislocation at the beginning of the year. Indeed, the demand for APAC FX was clearly reflected in the narrowing of APAC scored holdings, which went from -0.65 at the beginning of the year to flat in May 2025, for the first time since October 2024.

Interestingly, while APAC risks continue to be favored, the iFlow dynamic between foreign exchange and asset flows had shifted, with a differentiation in hedging dynamic depending on FX valuations. The most notable examples are in China and Taiwan. For example, recent good inflows in Chinese government bonds (CGB) didn’t lead to increasing FX hedging and therefore pushing CNY deeper into underheld territory, compared with a clear unwinding trend of FX hedges when investors were offloading CGB earlier in the year. On the other hand, recent sharp inflows into Taiwanese equities at a record weekly average scored flows last week were accompanied by persistent TWD outflows, which saw TWD scored holdings back toward -2 after a brief narrowing trend to -1.5 at the end of April. TWD is the most underheld currency within the APAC region. The FX valuation seems to be an increasingly important consideration factor.

Forward look

The stabilization of tariff-related risk should allow for APAC FX to react to more domestic fundamentals, such as monetary policy, budget deficit and fiscal stimulus, foreign investor flows, or commodity prices that directly impact trade balances, and country-specific factors, such as politics in South Korea, Indonesia or the Philippines, or tourism in Thailand. In such a scenario, high-yielding APAC currencies would be preferred, while low-yielding currencies might come under pressure from a rotation of funding interest into APAC. The valuation of the Indonesian rupiah stood out as the only currency within APAC that is down on the year. However, the recent easing of deficit pressure, and increasing demand for Indonesian government bonds, supported by Bank Indonesia policy rate cut, might just tilt the balance for further normalization of IDR.

Although global macroeconomic conditions continue to exert a broad influence – particularly through the ongoing impact of U.S. Treasury yields on global financial conditions – localized, idiosyncratic factors are beginning to play an increasingly important role in market behavior. As a result, mispricing caused by positioning imbalances may start to generate selective opportunities, even within developed G10 markets that have long been dominated by dollar-driven dynamics. We are particularly attentive to AUD, NOK and JPY. Meanwhile, emerging market assets are benefiting from improved risk sentiment, with notable gains in areas such as Asia-Pacific equities and EM fixed income duration. However, currency performance remains constrained due to persistent and complex hedging considerations across markets.