Fiscal Discovery vs. Dominance

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

EXHIBIT #1: DXY (INVERTED) VS. WEIGHTED 10Y YIELDS FOR GERMANY, CHINA AND JAPAN

Source: Bloomberg, BNY

Our take

From Berlin to Beijing, governments are responding to a radically different global trade and geopolitical environment with forceful fiscal stimulus. Most importantly, these economies can afford it. After having accumulated trillions of dollars in trade surplus over decades of globalisation and failing to invest optimally in their domestic economies, Europe, led by Germany, and China are now changing their approach to growth. The former has decided to lead re-armament in Europe out of security necessity, while the latter has likely recognized that with US market access ebbing away, promoting domestic consumption needs to compensate for growth. Suddenly, the US’ lead in long-term trend growth is no longer a given, and asset allocators are now comprehensively re-rating European and Chinese assets, giving a fillip to their currencies in the process.

Forward look

In anticipation of much heavier bond issuance (China has already announced increased offerings of ultra-long bonds), bond yields in Europe and China have moved accordingly. Rather than exhibit fears over fiscal dominance, which causes currency weakness and capital outflows – which we saw in the UK in 2022 – the EUR is rallying and CNH expectations now potentially face adjustment. Coupled with slow but certain reflation in Japan, higher long-dated bond yields amongst the US’ key trading partners are now rendering these sovereign markets as an investable proposition, thereby challenging another leg of U.S. exceptionalism (Exhibit #1). The bottom line is that within these surplus economies, public investment to stimulate domestic demand is affordable and will have a large growth multiplier. Challenges remain in execution and all these economies have material demographic and productivity gaps to make up against the US, but the amounts involved mean the growth implications cannot be dismissed. If consequently their central banks raise growth and terminal rate forecasts, then any advantage at the front-end for the dollar will face erosion as well. Today’s ECB decision will be an early test case of permanent re-pricing rate paths, and whether the euro can maintain its current momentum.

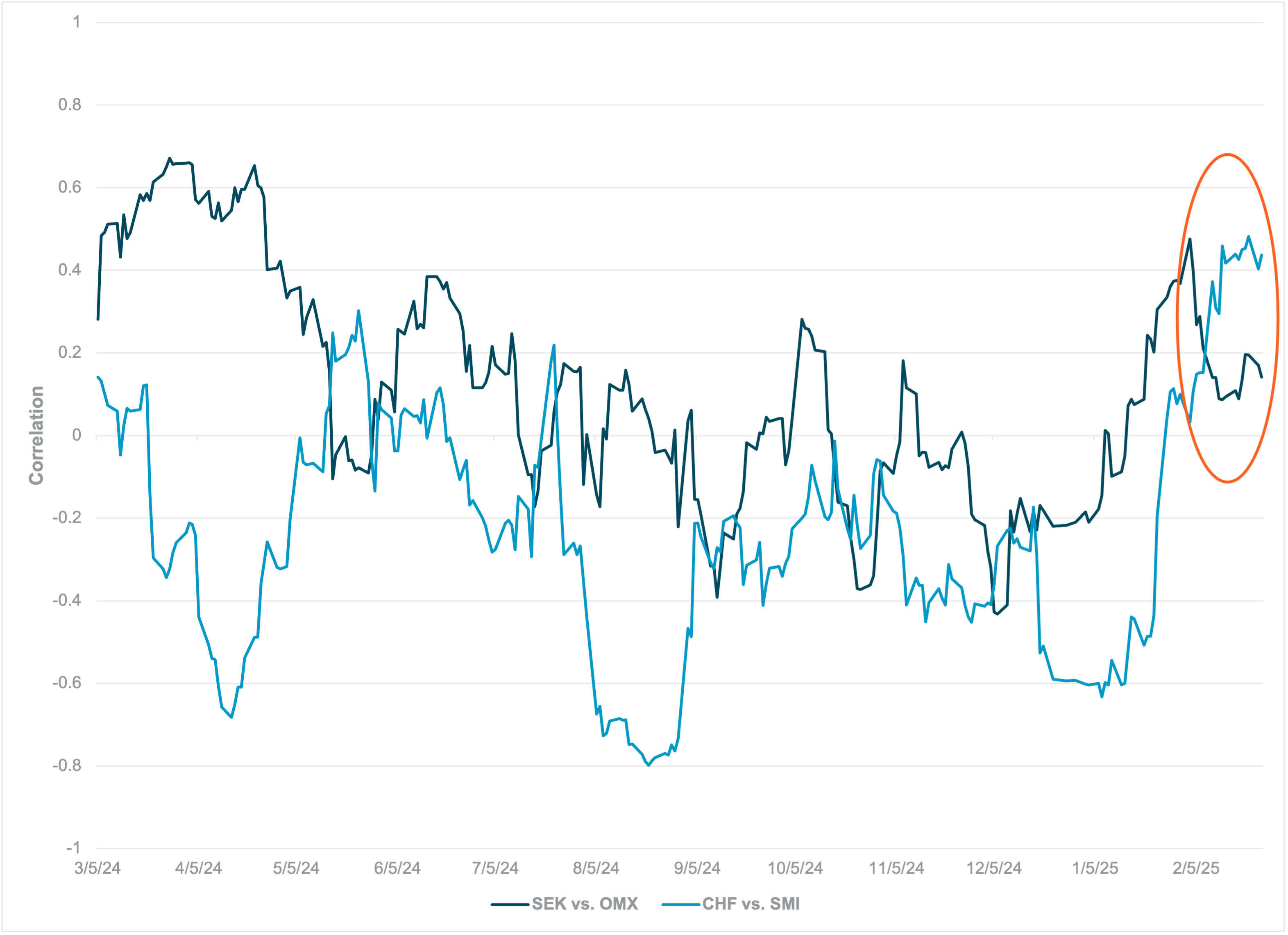

EXHIBIT #2: SEK AND CHF CURRENCY CORRELATION VS. LOCAL STOCK INDICES

Source: Bloomberg, BNY

Our take

The EUR has rightly benefitted from Germany’s fiscal breakout, but FX markets should not lose sight of the broader supply chain across the continent. We have already highlighted the strength of flows into Poland, but Sweden and Switzerland have sizeable arms manufacturers, and their industries produce much of the intermediate goods which are essential to the German finished goods’ producers. The “whatever it takes” boost should not be taken lightly with regard to implications for Continental industry, especially if for strategic reasons the entire supply chain is to be kept as “aligned” or “near-shored” as possible, which is no different to what China and the US are prioritising for their own industries.

Forward look

Normally, the prospect of increased external demand is seen as positive for a currency and the central banks of these exporting nations will need to push back against such trends out of fear of disinflation. However, in an environment where Continental demand is rising and Eurozone inflation and yields are expected to remain high, the framework has changed. If executed correctly, the Eurozone’s investment wave could sharply increase tolerance for a stronger SEK, CHF, and even CZK. Inflation in both Sweden and Switzerland is below target, but real effective exchange rates (REER) will not rise as much if Eurozone inflation holds well. Furthermore, inflows into local stock markets are helping drive currency strength but without reflecting earnings translation risk (Exhibit #2). SEK and CHF can comfortably continue outperforming the dollar, but we would be vigilant regarding the impact of sector-specific tariff risk from the US.

EXHIBIT #3: METALS/MINING EXPORT PRICES AND TERMS OF TRADE GROWTH

Source: BNY

Our take

Inevitably, as the dollar continues to soften while China announces a stronger fiscal push, interest is picking up in dollar-funded carry trades again, especially in commodity FX while monetary policy divergence vs. the US continues. Although South Africa and Chile (via copper prices) have felt some impact from the US’ various policy shifts, tariffs on these nations’ exports are not top of mind for markets. We are sympathetic to better performance for the likes of BRL, CLP and ZAR, but with valuations no longer attractive and the broader risk/US growth environment completely diverging with the heyday of such trades in mid-2023, we continue to favour limiting exposure to underlying FX risk.

Forward look

China’s fiscal impulse is clearly a surprise, but Beijing remains clear about its growth priorities, with technological advancement and the consumer leading the way. Both German and Chinese public investment plans will have a stronger infrastructure component, but we would be cautious about potential gains in terms of trade. Outside of BRL, the case remains weak for currency-based repricing (Exhibit #3), and even BRL valuations are now looking stretched. We only expect duration to form better due to persistent under-allocations by long-term investors.

Fiscal decisions by the European Union and incoming German government could prove transformational, with strong benefits for economies which remain part of the Continent’s industrial supply chain. China is starting its own fiscal push as well. US exceptionalism in asset allocation will face further challenges ahead, but Europe and China will now have to deliver on growth and productivity. Expect currencies with a high beta to European economic growth to continue performing, especially in Europe. However, the global risk environment will remain fragile, and we would not extend dollar weakness to EM high-yielders, especially with industrial commodity prices expected to remain soft.