Excessive FX Exposures Emerging

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

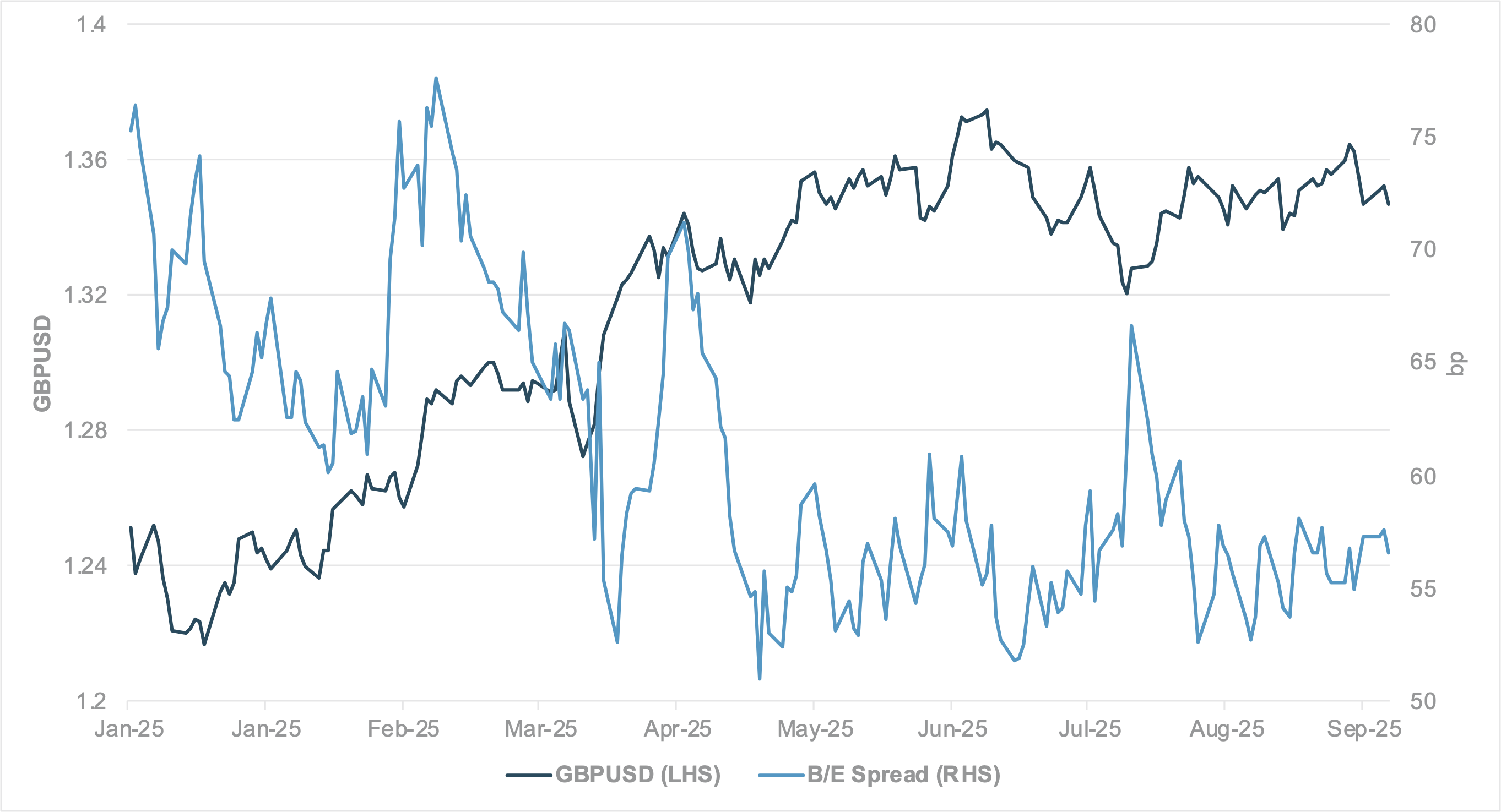

EXHIBIT #1: GBPUSD PERFORMANCE VS. U.K./U.S. INFLATION BREAK-EVEN DIFFERENTIALS

Source: BNY

Our take

Although the Fed’s rate cut anchored exchange rate moves during September’s central bank decisions, we believe the general guidance around individual decisions and policy paths was well communicated in advance. However, risks around these individual trajectories may still surprise markets. Comments by Fed Chair Jerome Powell and Bank of England (BoE) Governor Andrew Bailey underscore point to diverging outlooks: U.S. inflation pressures remain elevated, while Bailey emphasized a “further journey down” in rates. Ahead of the next central bank forecast updates in November and December, we expect highly asymmetric changes in policy pricing. European central banks may see weaker inflation outcomes, especially driven by pass-through, while we see the Fed implementing, at most, 50bp in additional easing for the rest of 2025. Rates markets are more aligned with central bank guidance: U.K.’s price pressures have declined materially since the beginning of the year based on forward break-even inflation and currently sit near the low end of recent ranges (Exhibit #1). Eurozone break-even inflation followed a similar trend, though declines have been more modest.

Forward look

If break-even inflation rates, even at the 5y5y point, hold information value for terminal rate differentials, then exchange rates should begin to reflect some convergence more closely. GBP and the EUR may have benefited this year from a general adjustment in dollar valuations, but given the evolving growth and price trajectories, we believe exchange rates must align more closely with shifts in policy bias. We expect the ECB to cut rates in December, while BoE doves (including the governor) may push for at least one more cut this year, with more likely if the labor market worsens. Crucially, fiscal risks remain strongly elevated across Europe. Given the scale of cross-border flows, any softening in investor interest is likely to be quickly reflected in currency performance.

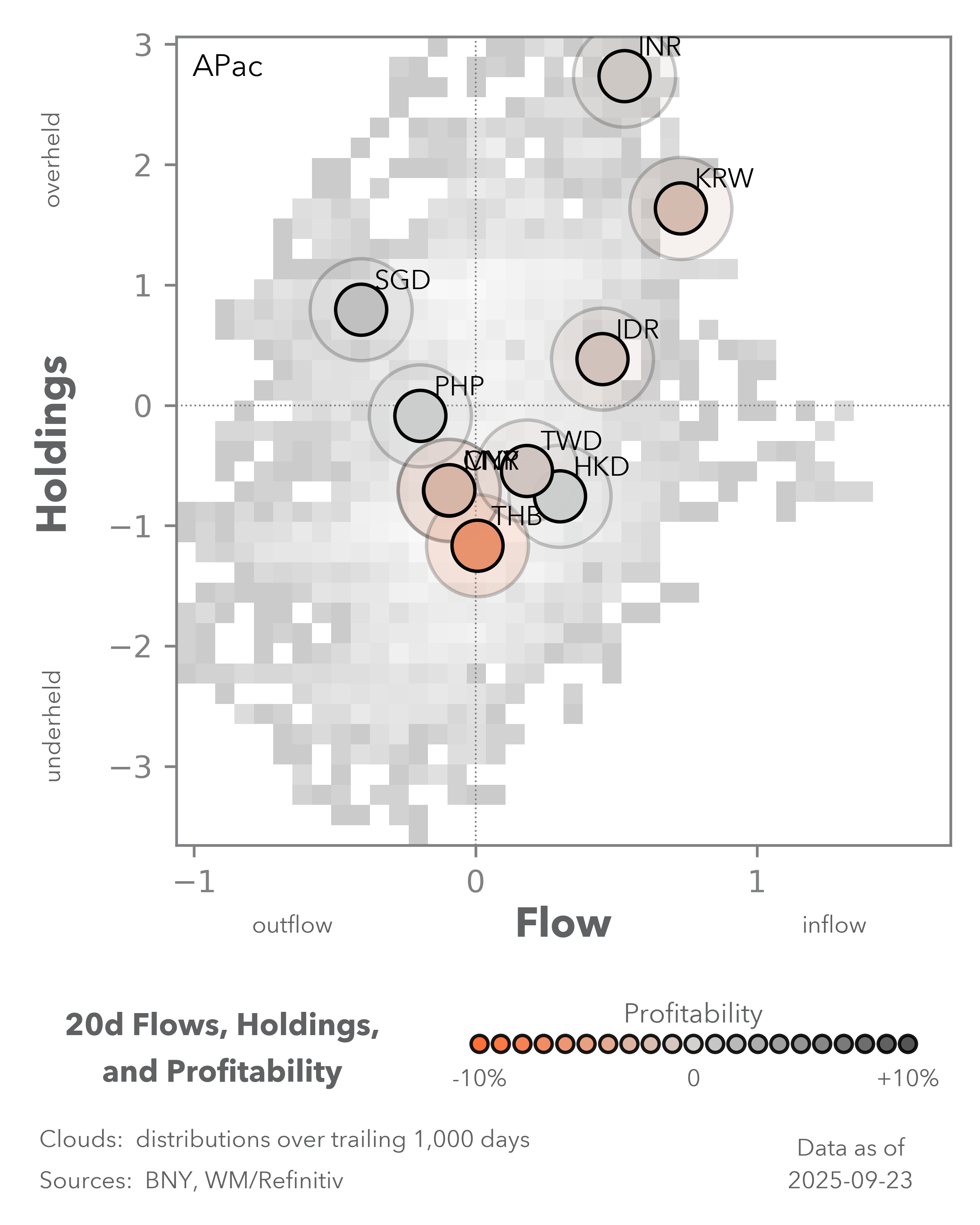

EXHIBIT #2: CNY EXPOSURES EXCESSIVE RELATIVE TO ASSET PERFORMANCE

Source: BNY

Our take

Weak domestic growth numbers are having little impact on Chinese equity interest. Market drivers and behavior are starting to resemble U.S. trends, where AI-related investment announcements by mega-cap names are generating outsized positive moves. Crucially, fiscal and monetary impetus continue to support the economy, and investors are increasingly looking at the structural story. Chinese equities remain attractive from a valuations perspective, in part due to limited global allocations. Our flow data indicate that foreign interest remains tentative, with cross-border interest proving highly inconsistent. Given the scale of recent moves, current allocations have likely already performed strongly, reducing the incentive to add aggressively unless portfolios began from an extreme underweight position. Furthermore, in less constrained strategies, outright renminbi exposures have surged in recent months. We apply a methodology similar to our dollar-based “net hedge” index, combining Chinese cross-border equity and fixed income holdings in a standard 40:60 ratio, offset by renminbi exposures — a structurally underheld position that reflects current rate differentials. Since mid-Q2, strength in duration and relatively unchanged currency holdings have driven a notable positive shift in the net portfolio position (Exhibit #2).

Forward look

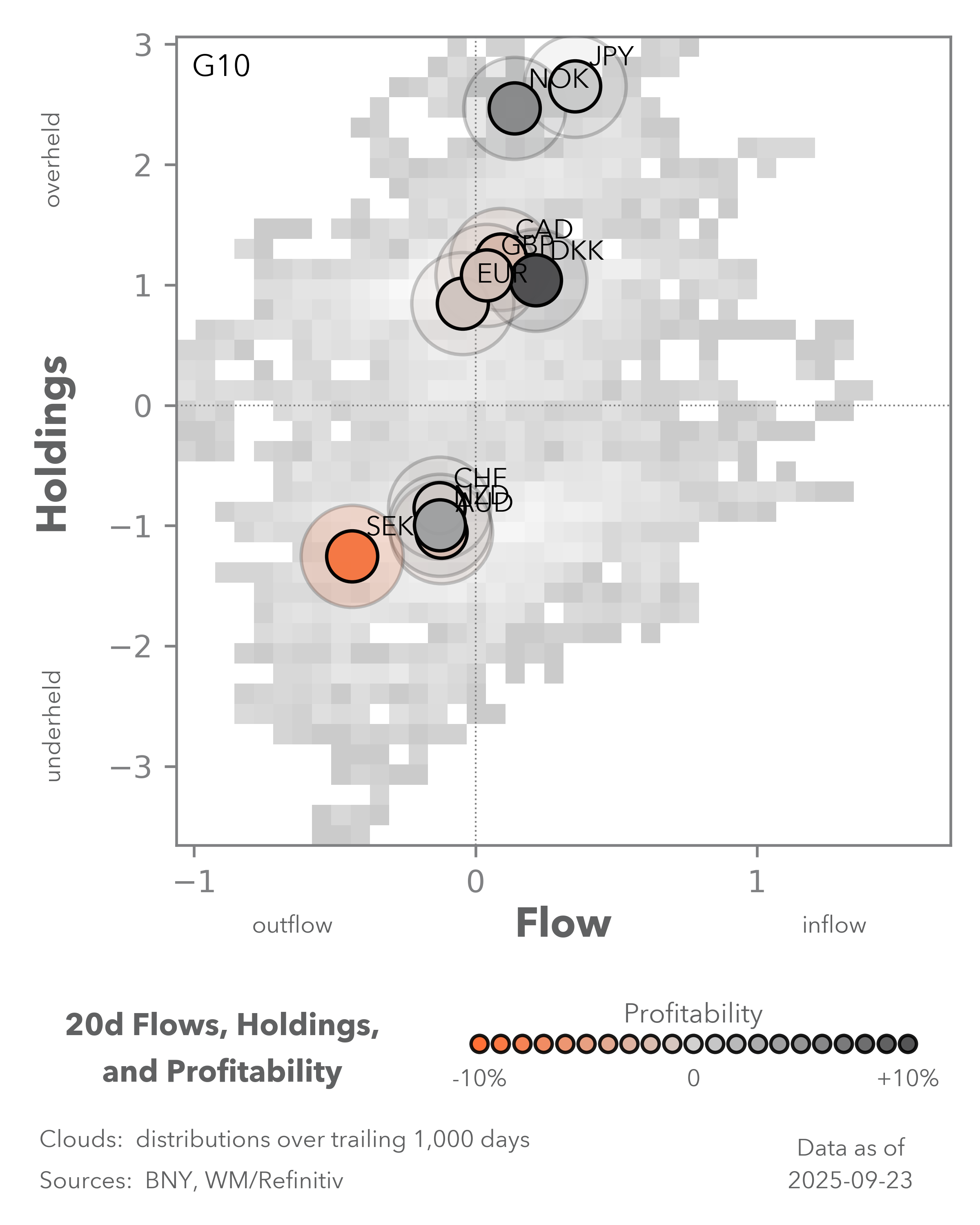

Our stance on the dollar versus major currencies extends easily to low-yielding APAC currencies. CNY, TWD and KRW are all under-hedged relative to their one-year average, and gains in the technology and semi-conductor sectors have similarly influenced FX exposures. Ultimately, the long-term driver for Asian funding currencies is less about cross-border investors’ interest or hedging levels, and more about whether current account-based savings remain onshore. As domestic savings are unlikely to shift near term, marginal flows will likely need to come from foreign investors with overweight APAC exposure. Heading into quarter-end, hedging flows appear increasingly imperative.

EXHIBIT #3: RATIO OF 1M IMPLIED FORWARD-YIELD DIFFERENTIAL VS. 1M IMPLIED VOLATILITY

Source: BNY, Bloomberg

Our take

Central bank decisions in Central and Eastern Europe passed without incident this week, but any hope for a near-term rate cut has been dashed. The Czech National Bank (CNB) governor stated yesterday that the “ongoing inflation pressure from the domestic economy currently preclude a further decrease in interest rates.” He also warned that if the CZK weakens, rate hikes cannot be ruled out. Geopolitics also plays a role as defense spending in the region continues to rise. In Hungary’s case, reluctant adherence to restrictions on Russian energy access may also raise inflation and limit policy options. Meanwhile, Latin America may have marginally benefited from U.S.-Argentina financial support talks, sustaining the global carry trade. As stated, we see risk-reward in dollar-longs only when the dollar is the carry leg. Current conditions should help EM debt flows, but currency risk remains a concern. We continue to look for potential hedging opportunities. Comparing carry-to-volatility ratios across regions, CEE has started to pull ahead in risk-reward, despite lower nominal yields, especially when funded in euros (Exhibit #3).

Forward look

There is no immediate catalyst for a global carry unwind. We remain focused on the dollar’s tactical position and favor hedging EM FX risk. However, for mandated EM FX exposures, we prefer the CEE, given better risk-reward and the near-term risk of ECB easing. According to the CNB’s current outlook, a strong exchange rate is almost a prerequisite for easing. Rate cuts are not needed to counter disinflation risks, which do not currently exist. Meanwhile, LatAm FX still needs to contend with U.S. trade relations, weaker Chinese demand for commodities, and local politics. Real rates remain high and anchor duration performance, but FX exposures require caution.