Equity and economic divergence causing FX turbulence

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

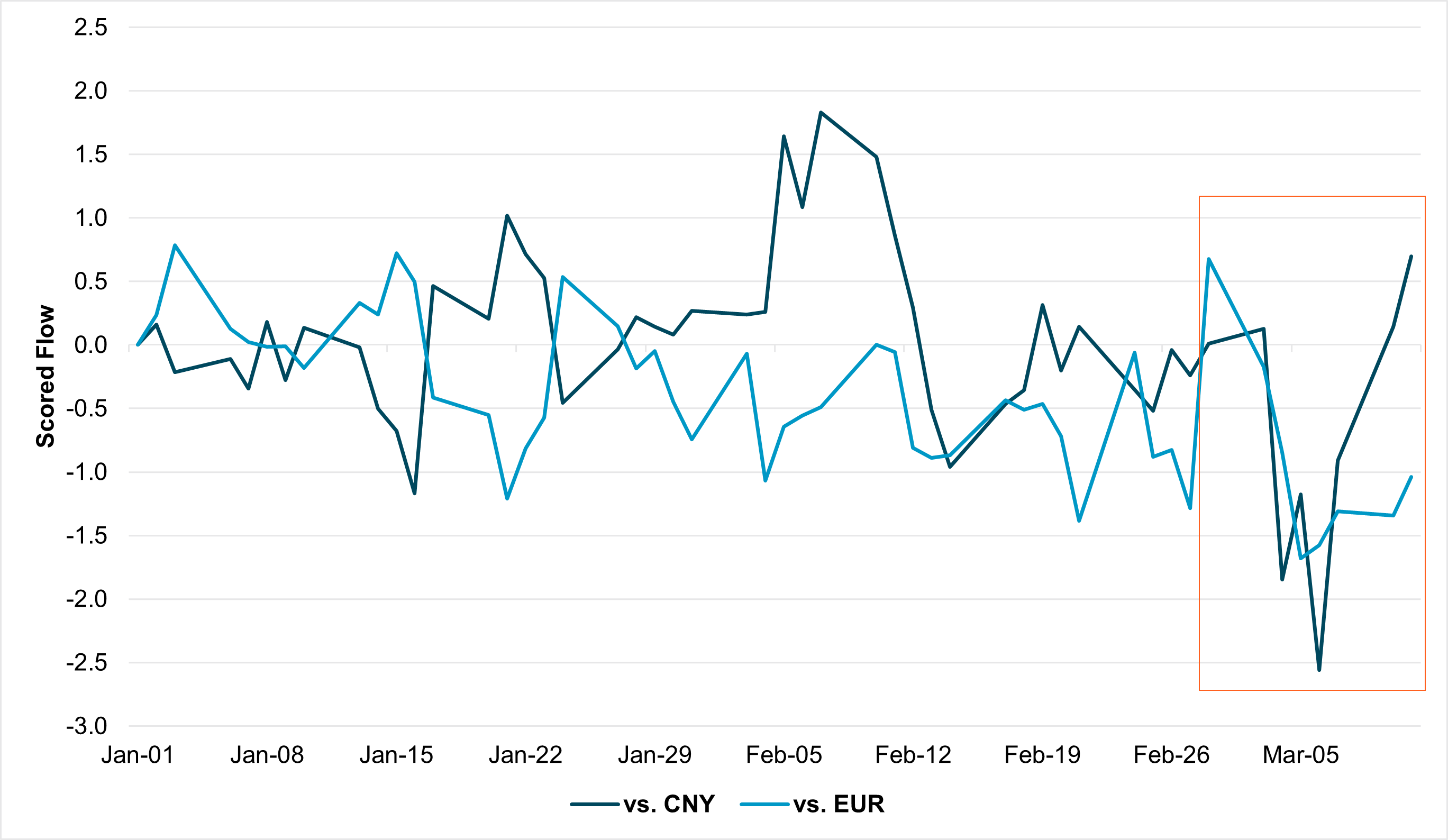

EXHIBIT #1: USD FLOW VS. EUR AND CNY, YTD

Source: BNY

Our take

As US equity markets continue to underperform peers in Europe and Asia-Pacific, the dollar is starting to feel the impact of asset rotation flows. iFlow shows there has been a surge in USD selling against the EUR and CNY (Exhibit #1) over the past two weeks. Simple changes in asset exposures aside, the re-pricing of Fed expectations due to the deteriorating US growth outlook is also narrowing rate differentials. With the opportunity cost of US assets rising and no let-up in volatility driven by trade and economic policy, it will be very difficult for the dollar to revert to higher valuations seen earlier in the year.

Forward look

Narrowing rate differentials will have material implications for exchange rate performance due to changes in rate differential dynamics. Hitherto, we had expected investors to maintain high dollar exposures through forward hedging because the Fed would stay materially less dovish than peers. However, with the European Central Bank (ECB) clearly signalling a change in stance while greater downside risk to the economy could lead to further changes in Fed expectations, forward purchases of the dollar by US investors could decline. Furthermore, while significantly reduced, latent hedges against the euro remain large at around 1.5 times the average over the past year. Reductions of these hedges are helping drive EURUSD purchases, and we are unwilling to call a top in EURUSD – even with stretched valuations – until these holdings normalise.

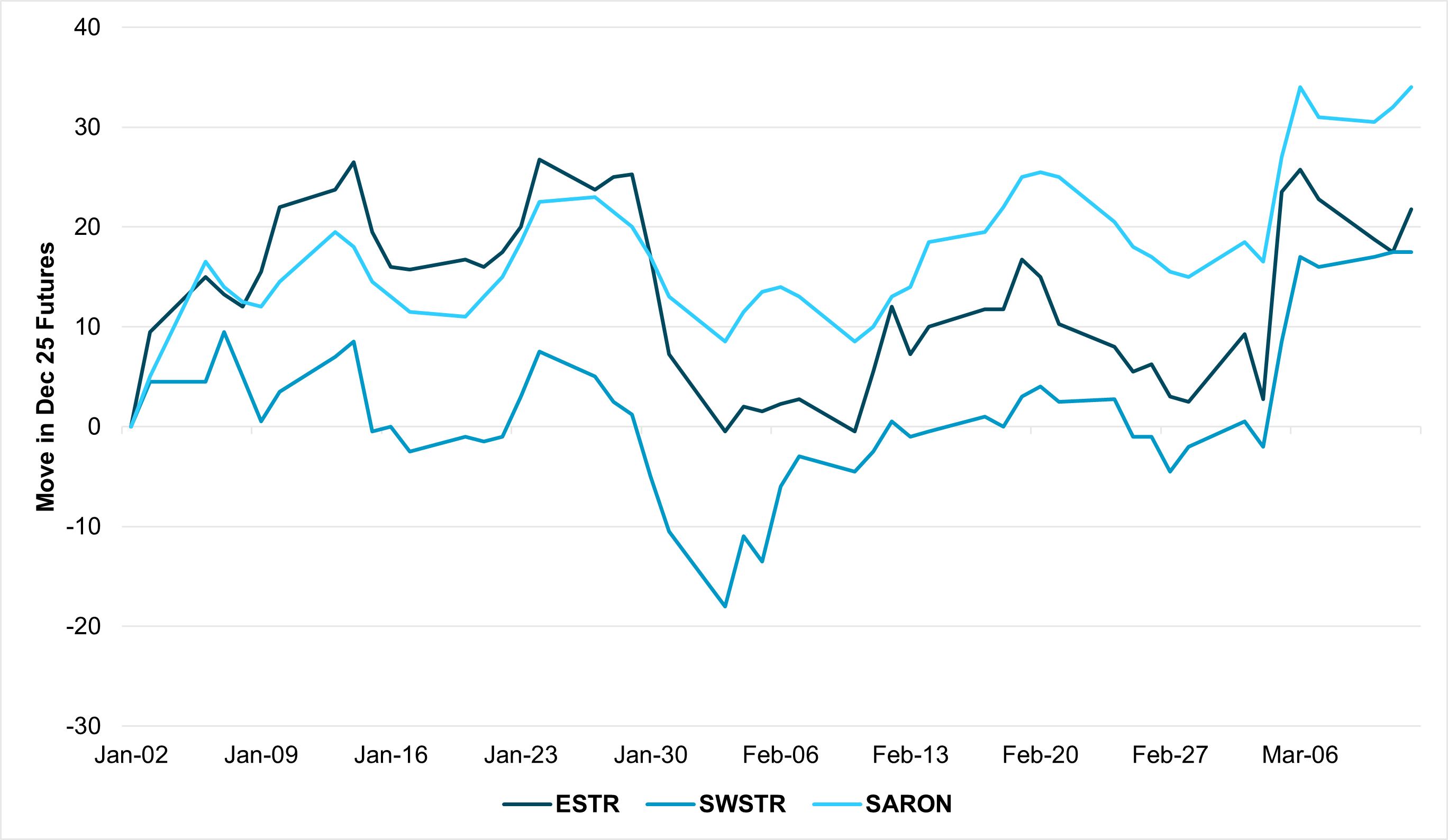

EXHIBIT #2: EUROPEAN DECEMBER 2025 INTEREST RATE FUTURES CHANGE, YEAR TO DATE

Source: Bloomberg, BNY

Our take

ECB President Lagarde has made it abundantly clear that the recent change in the ECB’s stance, whereby “monetary policy is becoming meaningfully less restrictive,” marks an end to a more aggressive phase of the ECB’s easing cycle. Inflation is not expected to soften to target until next year and policy must recalibrate accordingly, even in the face of external risks. Across Europe, rates markets are now pricing in less easing (Exhibit #2). In Switzerland and Sweden, policy alignment is necessary with the ECB, and these economies can now count on a stronger euro to support tradables inflation in their own economies – a sharp reversal compared to the previous cycle when the Eurozone was often a source of disinflation risk.

Forward look

We acknowledge that based on the ECB’s shift, our prior expectations for sustained rate cuts to pressure the euro will be difficult to realise. While the ECB remains attuned to downside risks from both domestic weakness and external uncertainty, the fundamental inflation case for lower rates is no longer solid. Furthermore, even with tariff risk, the ECB appears non-committal that aggressive cuts will be the reaction, especially with the unexpected fiscal resurgence which will lift domestic demand. For other countries tied to the German and Eurozone industrial supply chain, central banks will likely have a similar response. Currency strength could even prove tolerable as a tightening tool for the ECB to help curb inflation. We continue to see a reversal for EUR and SEK over the medium term, but the current move in rates and latent under-positioning means overshooting is highly possible.

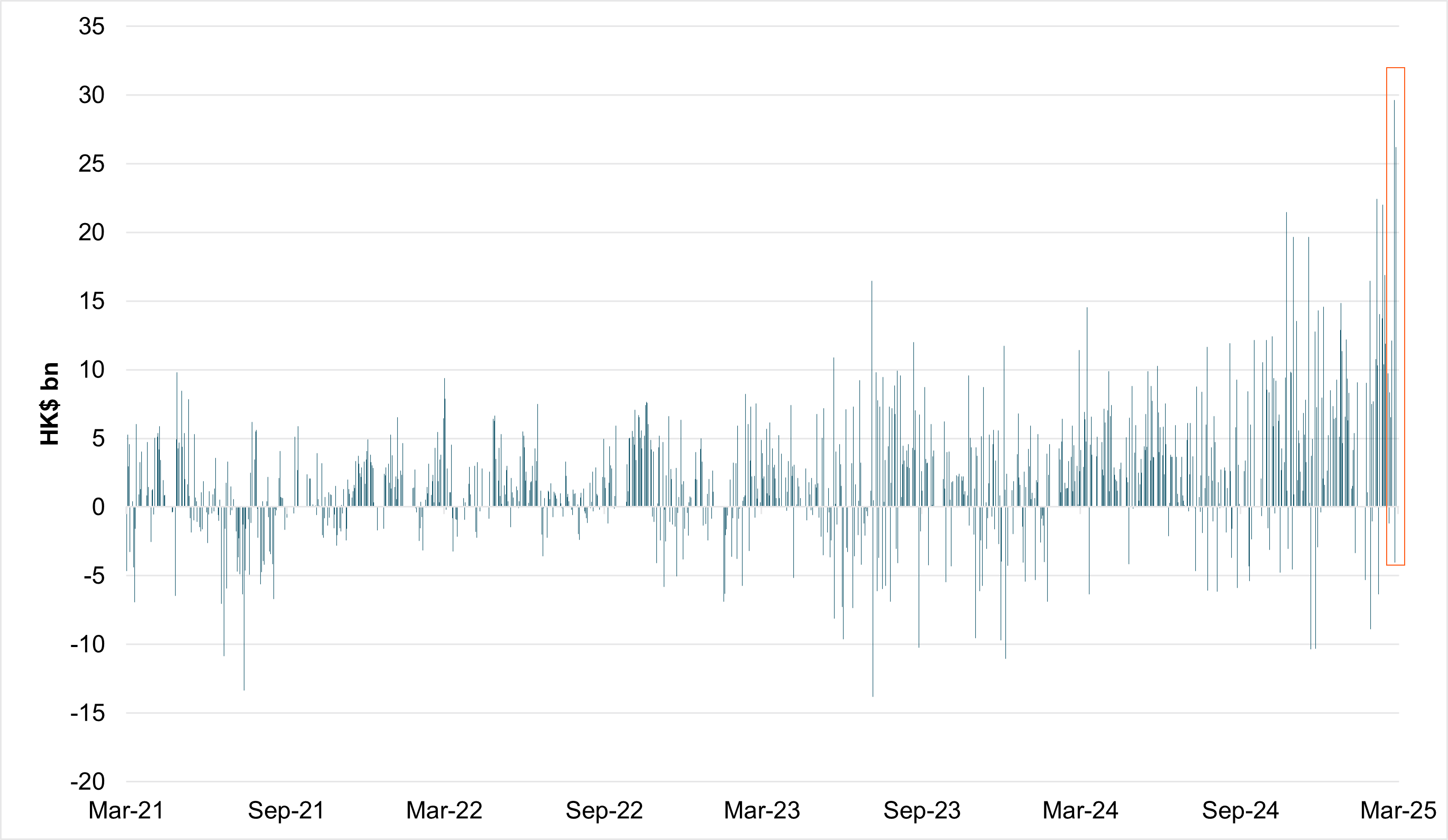

EXHIBIT #3: DAILY SOUTHBOUND FLOW FROM MAINLAND CHINA TO HONG KONG

Source: Bloomberg, BNY

Our take

The National People’s Congress (NPC) in China has closed with additional commitment to 5% growth and reflation. The move in Chinese 10y government bond yields back to 2% points to some confidence that such efforts will be successful, while domestic investors rotate away from government bonds into equities. Furthermore, to increase exposure to the prevailing artificial intelligence and wider tech theme, mainland investors are aggressively purchasing Hong Kong-listed equities through the Stock Connect program at the strongest levels seen in over four years (Exhibit #3), and we can see that interest has been increasing since Q4 last year. This week, local press reported that South Korean investors bought Hong Kong stocks at the largest scale in three years in February.

Forward look

While Chinese equities are performing well in iFlow, our data is limited to cross-border investors from outside of the APAC region and only began in earnest towards the end of February. This explains why the renminbi is not performing as well as the euro, despite similar equity re-rating, and any improvement in FX exposures has been limited to the unwinding of hedges. Similarly, APAC is not benefitting from any form of reflation or re-rating. Based on the current policy mix, the market is rightfully expressing greater confidence in Europe’s fiscal push and their ability to materially push up potential growth. The current language on inflation in Asia contrasts strongly with that in Europe, which will also inhibit currency strength for CNY and its peers. Given the thematic changes in APAC are not export-based, weak currency performance cannot generate marginal earnings growth either. For these reasons, we expect limited global participation to continue in the region’s equity markets until performance deviations from benchmark become extreme.

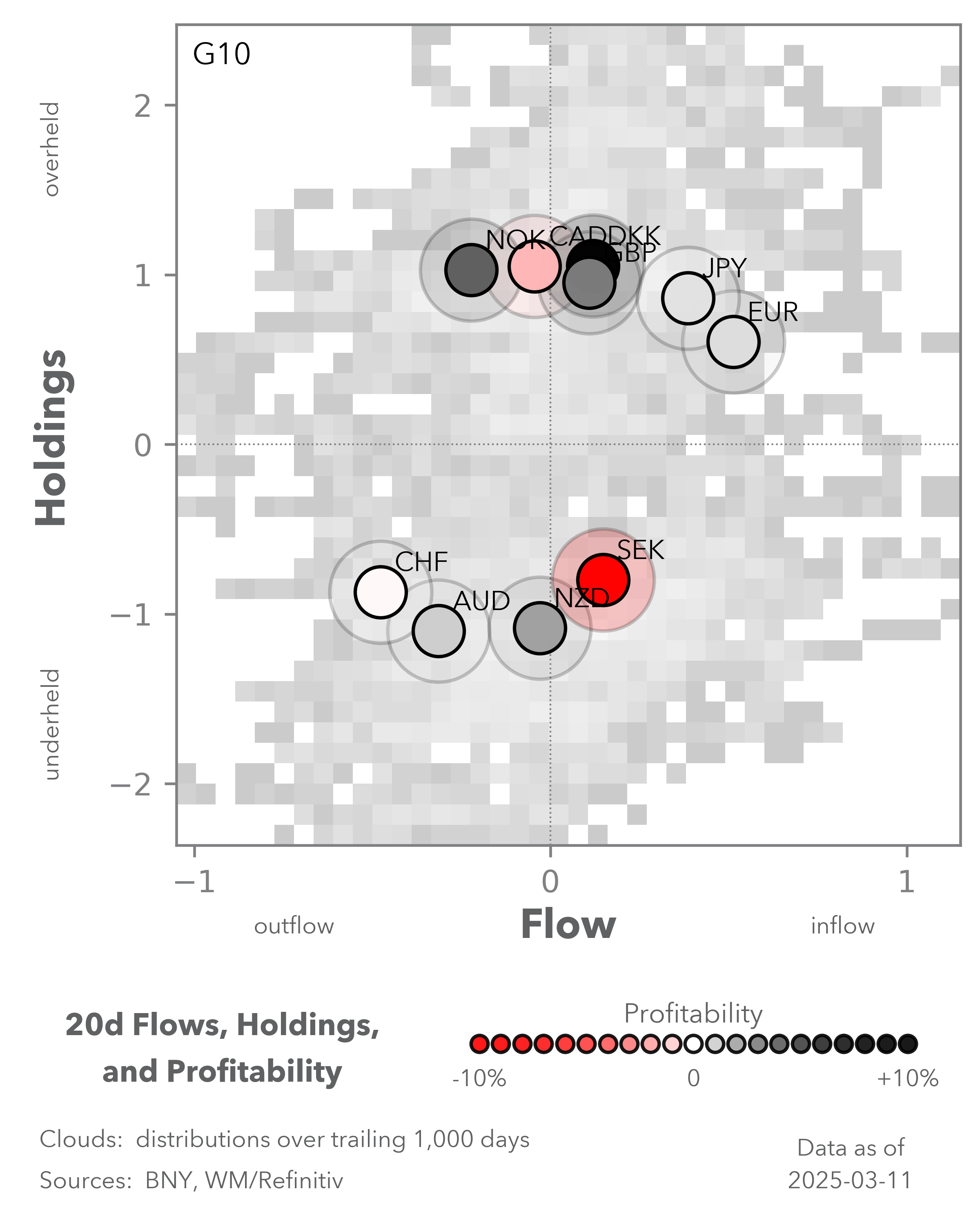

Domestic economic concerns which have undermined US yields are now contributing to a dollar pullback, which was already proceeding apace due to external re-rating. There has been a marked pick-up in the unwinding of hedges on low-yielding funders such as the EUR and CNY. As the “base” for these hedges remains large due to “US exceptionalism” over the past few years, further unwinding is possible. Combined with ongoing rotation into European and Chinese equity markets, a weaker dollar remains the “pain trade” against G10 FX and the CNY.

Data as of 2025-03-11, Source: Bloomberg, BNY