Easier financial conditions making their mark

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

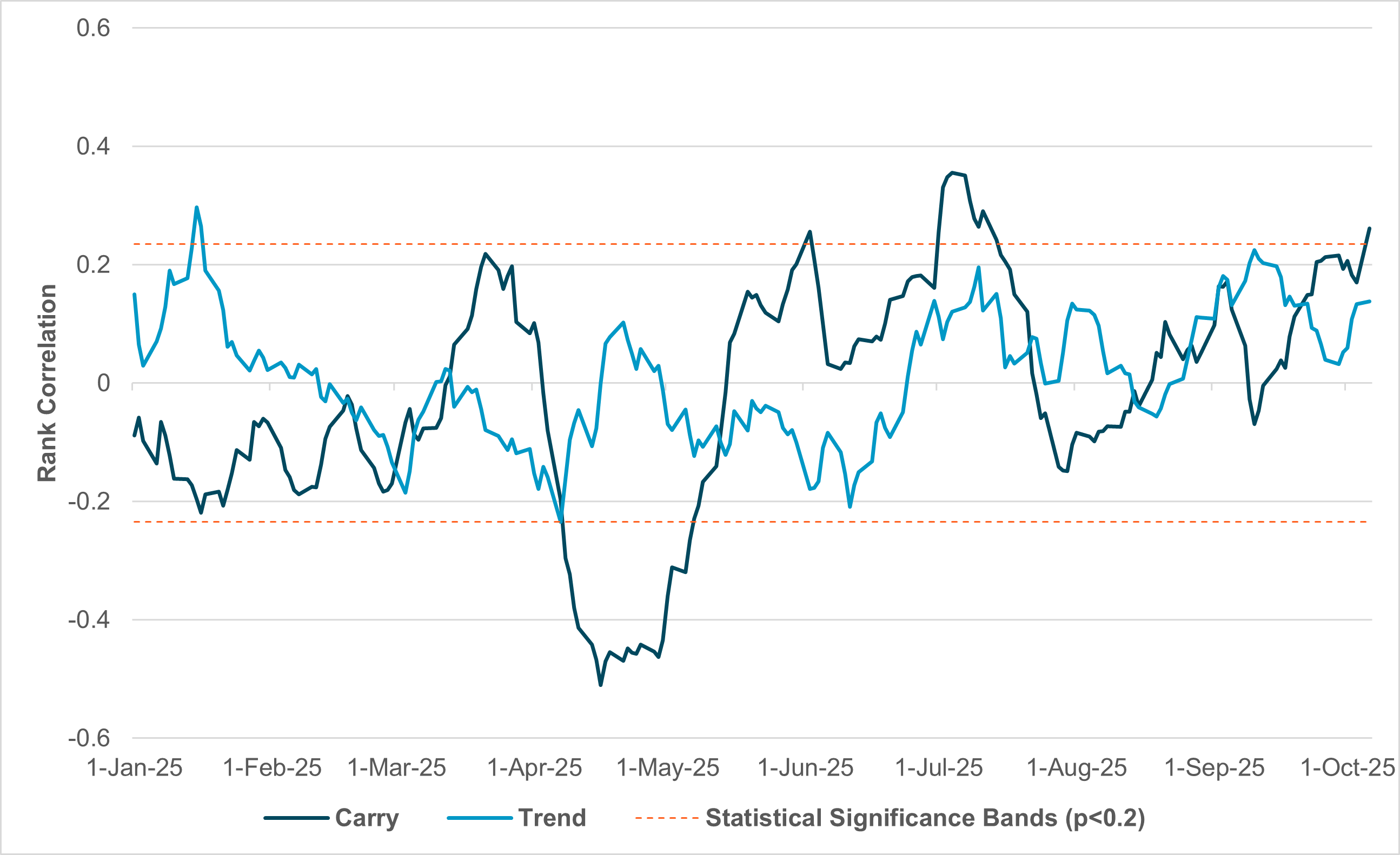

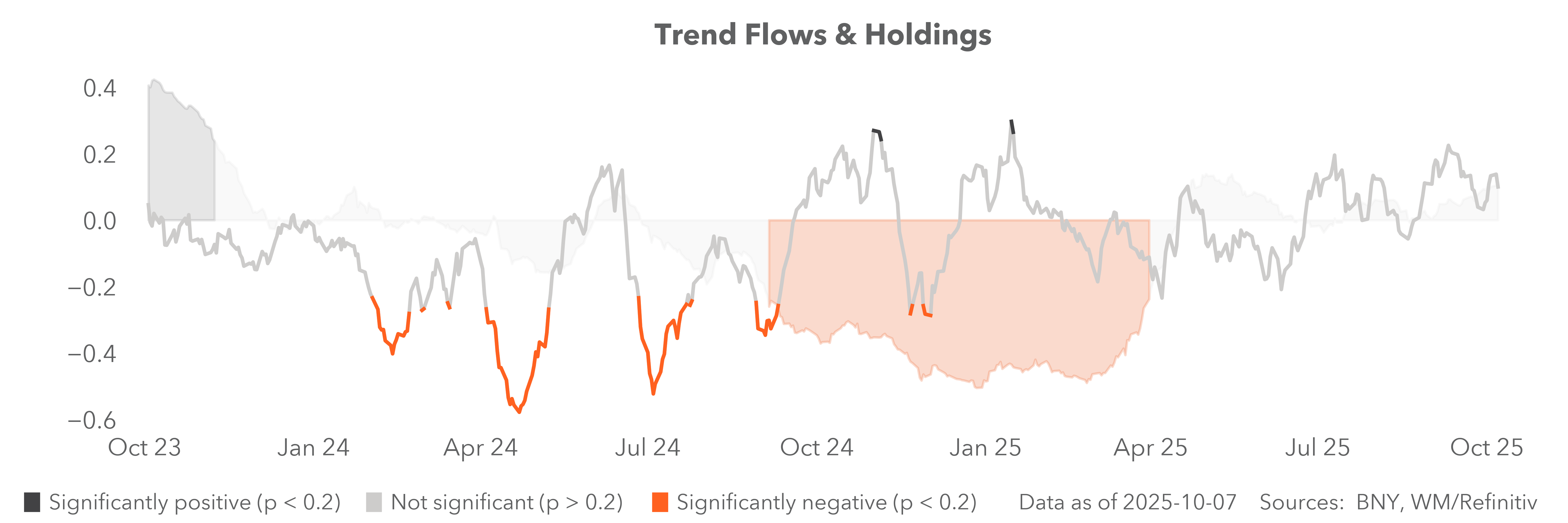

EXHIBIT #1: IFLOW CARRY AND IFLOW TREND YEAR-TO-DATE, WITH STATISTICAL SIGNIFICANCE BANDS

Source: BNY

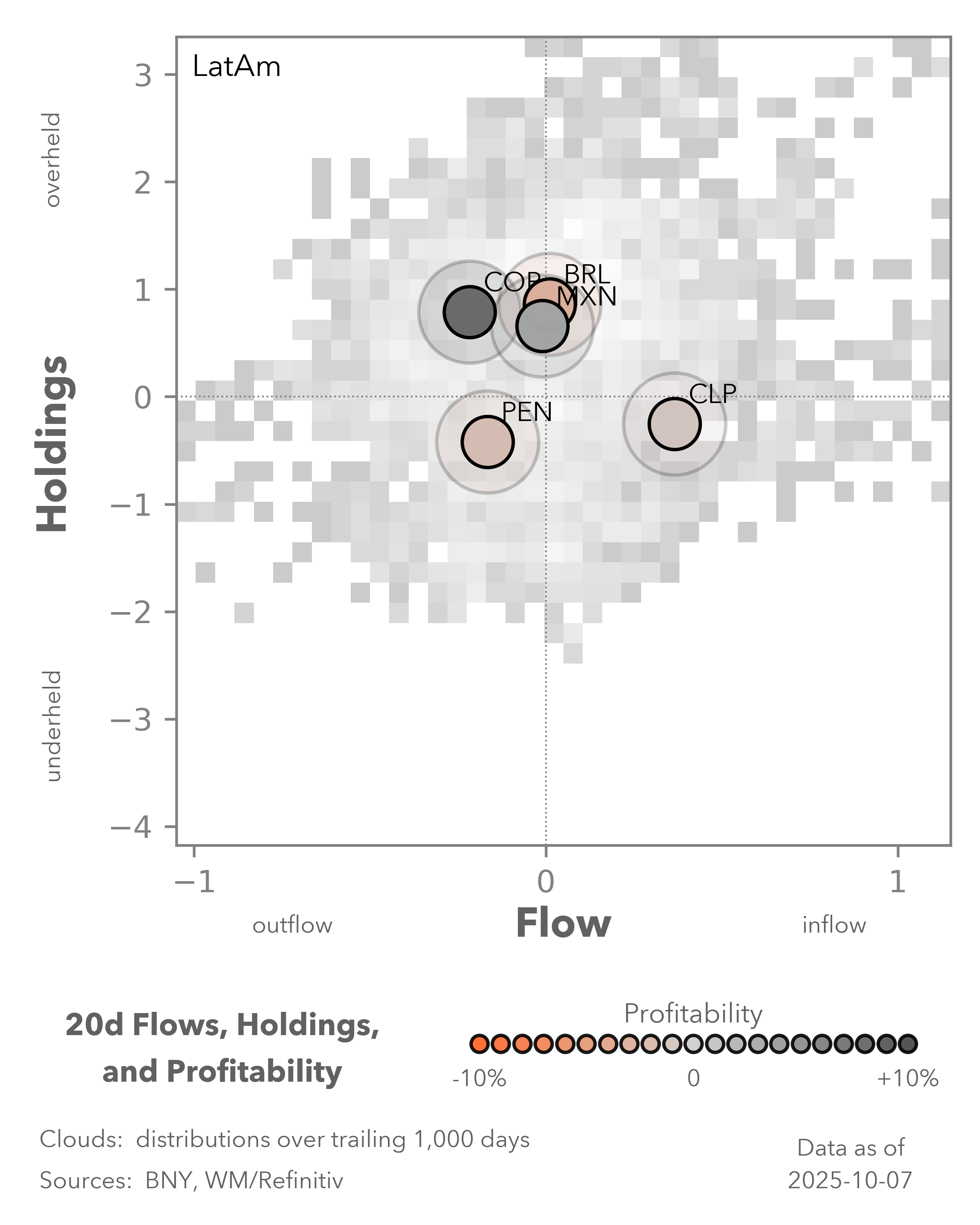

Our take

iFlow Carry has shifted back into statistically significant and positive territory. This has come later than we expected given the pivot by the Fed was well-telegraphed, but it seems that the impact of stronger equity markets and the prospect of far easier global financial conditions are proving difficult for FX markets to ignore. However, much of the interest is now with the dollar as the carry leg, especially against low-yielding currencies in APAC and EMEA. Even with higher carry interest, we remain of the view that heavily-held high-yielding currencies such as HUF and ZAR face hedging risk, which will likely limit the duration and scale of the theme. But in the short-term, we would not fight the trends, and if risk appetite is sustained other coincidental strategies could prove attractive. iFlow Trend has not moved into positive statistical significance since very early in the year (Exhibit #1), but there is a strong prospect of a carry “lift.” We can see that since mid-year, carry and momentum flow have been well-aligned; when positive, both indicators point to a risk-on environment.

Forward look

Like the current state of the carry trade, we would focus on conventional long-dollar views. The tactical shift back toward a “less-dovish” Fed approach while risks elsewhere emerge remains a strong proposition. For example, the surprise decision by the RBNZ to cut 50bp yesterday now even puts the NZD closer to funding status, especially if there is scope for terminal rates to approach 2% – which wouldn’t put it out of line with well-established funders such as EUR and SEK’s terminal levels. Gone are the days when markets can expect a high single-digit spread between NZD and JPY. Based on the current drivers of carry, momentum plays against the CNY, SEK, ILS and THB represent the strongest risk-reward.

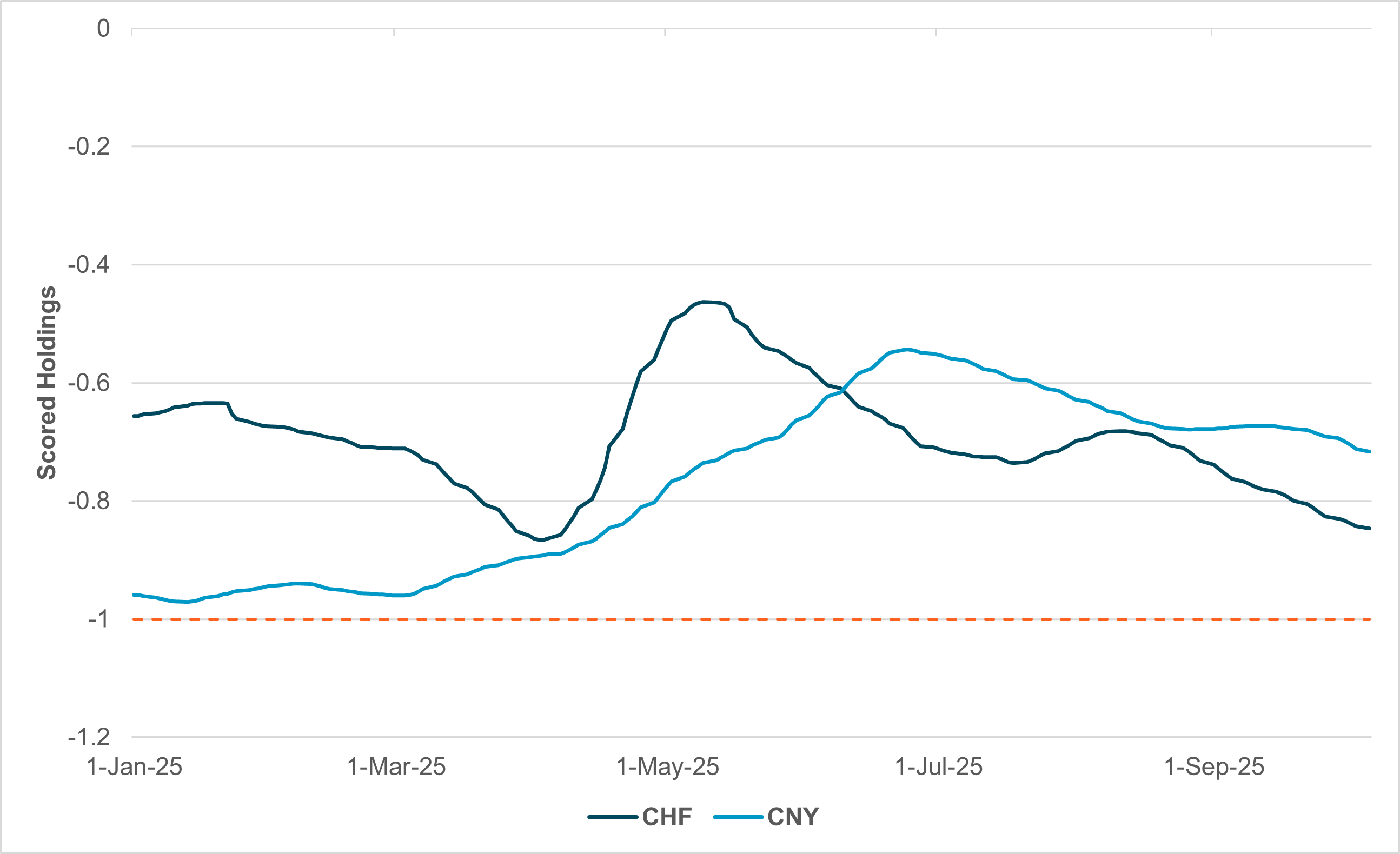

EXHIBIT #2: SCORED HOLDINGS IN CHF AND CNY YEAR-TO-DATE

Source: BNY

Our take

In the broader context of the carry trade, EUR and JPY will be seen as the liquid funding names. Given the renewed fiscal pressures on both the Eurozone and Japan, increasing hedges in these currencies is favorable. However, there is asymmetric risk surrounding such events and high implied volatility will impact risk-reward in a carry context. For example, it will be very hard to see carry trades in general performing well in the event of strong fiscal risk in Europe as there will be an impact on the equity channel. Meanwhile, JPY valuations are quite stretched and we believe that ultimately the fiscal impulse in Japan will be more limited, and the BoJ’s tightening path will not be affected over the medium term. Our data also show relatively elevated levels of EUR hedges, which means the burden of adjustment on carry trades may shift to other low-yielding funders. We have identified CNY and CHF as having such potential in the near term: both currencies are traditionally underheld by cross-border investors due to rate differentials, but current hedging levels are 25%–30% below the rolling 1-year average (Exhibit #2).

Forward look

We stress that any form of carry interest funded out of CHF and CNY will be tactical in nature. Flows in both have already been difficult in recent weeks and we treat iFlow Carry moving into statistical significance as a mean reversion indicator. Compared to the past two years, iFlow Carry’s staying power has been more limited and as soon as both currencies approach a neutral hedging level, risk management is needed. Macro triggers such as a U.S.-Switzerland trade deal and clear pick-up in domestic activity figures in China may also impact funding interest. However, as both China and Switzerland are unique in being core economies which face structural downside risk to inflation, tolerance for currency gains will be far more restricted by their respective central banks.

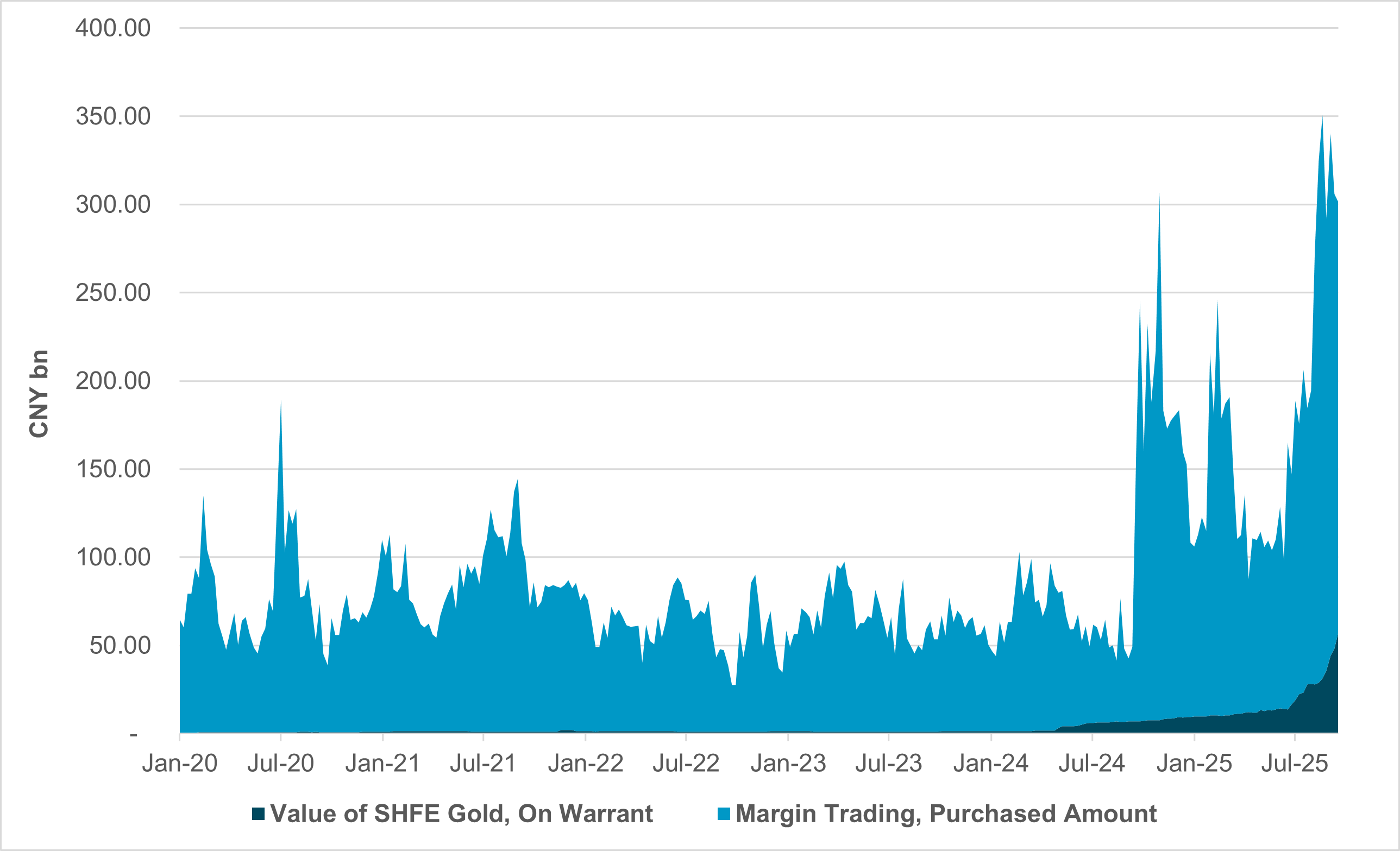

EXHIBIT #3: NOMINAL VALUE OF SHFE GOLD ON WARRANT; SHANGHAI AND SHENZHEN MARGIN PURCHASES

Source: BNY, Macrobond

Our take

Activity in CNY will rise as China returns from its long Golden Week holiday today. Onshore equity markets will be looking for fresh drivers to sustain the current rally. One of the major themes which has developed as we approach Q4 is the seeming divergence between macro data, company earnings and broader market performance. Unlike the U.S. and much of the developed world, where there is still a sense of robust household earnings and corporate profitability underpinning demand, both factors are lacking in China as prices continue to struggle for momentum. The recent holiday period was seen as test to see whether household expectations have started to shift to a more positive tone, and we expect spending data to be closely scrutinized in this context, with value data particularly important. There is consensus that activity levels are improving, albeit from a low base, but spending restraint remains relatively high: services inflation fell below zero in December 2023 and has not recovered. While nominal earnings improvement is necessary for reflation, a new channel has emerged for positivity in the near term: the household wealth effect. The transition from household wealth being driven by real estate prices to financial assets is seen as a necessary part of China’s rebalancing, but there are misgivings about the latest surge. The foray into financial assets is more recent and the structure of investment flows seen as short term in nature. Rather than redirecting savings away from government bonds and cash deposits into institutional, long-term flows, much of China’s recent stock market rally has been driven by margin participation (Exhibit #3). Concentrated flows after several years of dormancy could prove difficult to sustain – even if there is redirection into long-term investments the process will be rocky. More recently, there has been a notable pick-up in the notional value of gold on warrant (i.e., in storage and registered with the exchange) at the Shanghai Futures Exchange. At over CNY 50bn, the total value is now close to a quarter of the value of purchased stocks (in Shanghai and Shenzhen) through margin trading – a sharp rise from 5% in 2024 and barely 2% in 2023.

Forward look

Realizing the wealth effect from financial assets can come through two main channels: crystallization of gain or expanding balance sheets through credit growth, backed by higher levels of equity. The latter path is clearly more conducive to reflation as credit expansion can pick up. This is now a necessity for inflation as 2024 saw the weakest annualized total household credit growth on record at 3.39%. Between 2007 and 2023, there were only three quarters of sub-1% household credit growth; last year alone there were three. Crucially, we believe this is a more sustainable channel for inflation growth. Given the current state of CPI and PPI, we believe further tolerance for CNY nominal appreciation is limited and allowing funding preference (see above) is preferred. However, higher inflation to realize real effective exchange rate gains, ultimately supporting wage growth, will be far more significant and likely the key focus for the next five-year plan, to be announced later in October.