Dollar Weakness to Persist

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

John Velis and Geoff Yu

Time to Read: 5 minutes

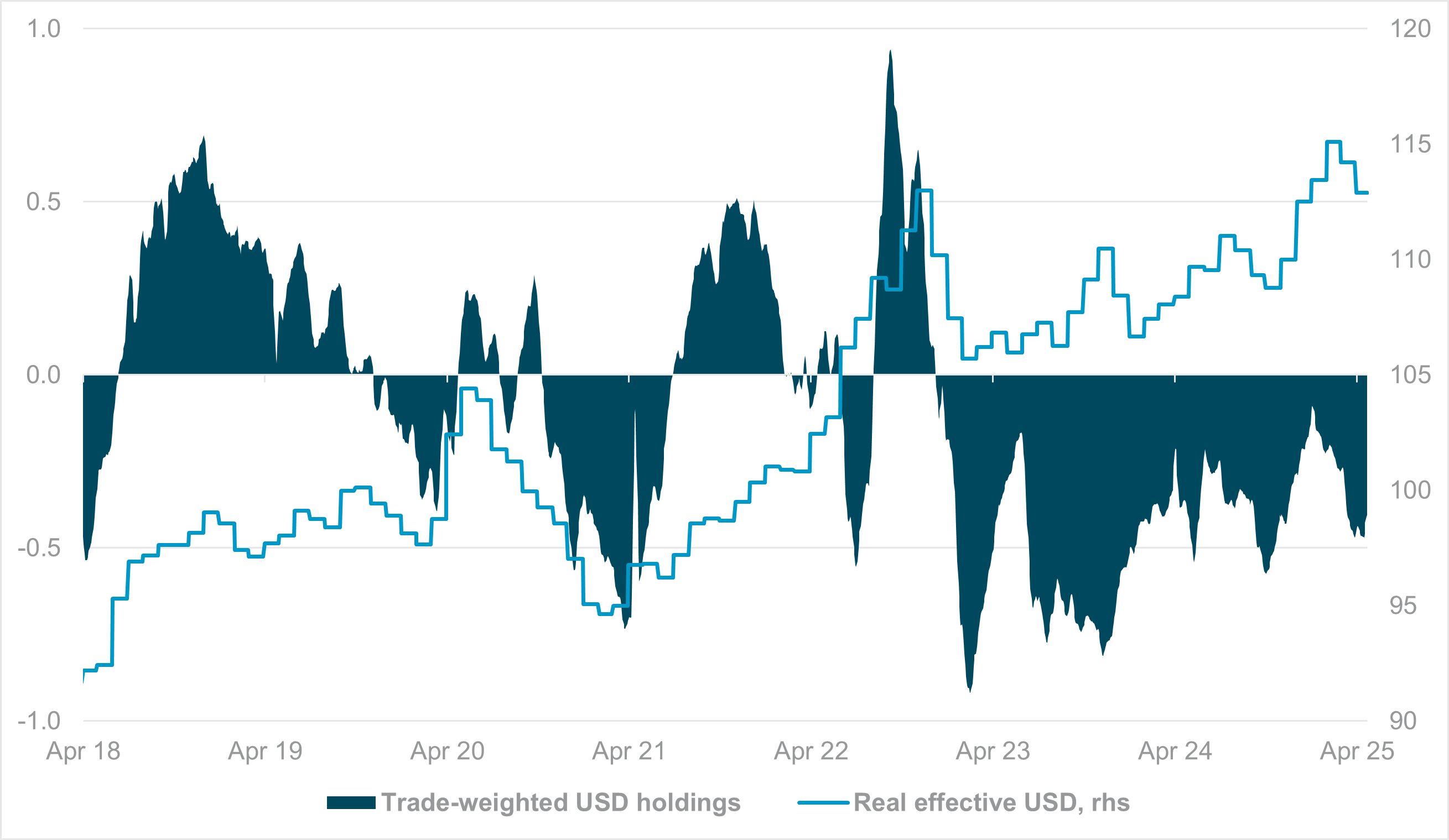

EXHIBIT #1: HOLDINGS COME OFF, BUT USD STILL EXPENSIVE

Source: BNY Markets, iFlow, BIS

Our take

We have written extensively of late about the retreat from U.S. dollar assets by cross-border investors (see here, for example), and the greenback has certainly reflected this waning investor demand. Still, there is room for it to remain on the weaker side of 100 (on the DXY dollar index). Even though the index is currently around 10% lower than at its mid-January peak, it’s still expensive on a real exchange rate basis – just off its 30-year high (see Exhibit #1). Nevertheless, iFlow shows that during its recent depreciation, dollar holdings have eroded again, although they’re still above their own recent lows, realized in late 2023. We have seen investors take their dollar exposure lower in the past and expect them to do so going forward. Until April 2 and “Liberation Day,” the USD had been trading on interest rate differentials, as we reported just a few weeks ago (see here). However, that relationship has clearly broken since the beginning of this month, as policy volatility and uncertainty have kept investors wary U.S. assets. It’s too early to say if the recently proposed retreat by the new administration on Chinese tariffs and the president’s cooling rhetoric toward the Federal Reserve Chair will see a return of foreign appetite for the USD. On the other hand, if there is central bank divergence in the face of the trade war – with the Fed slower than its peers – this will spark a return to interest rate differentials as a dollar driver.

Forward look

We think it’s more likely that the current policy landscape and trade tensions will keep the dollar weaker. Gold’s recent run to all-time highs suggests a degree of concern over U.S. primacy in the global financial order, but we don’t think this means the end of USD dominance, primarily due to a lack of alternatives. We caution readers against associating a weak or depreciating currency with a loss of dominance.

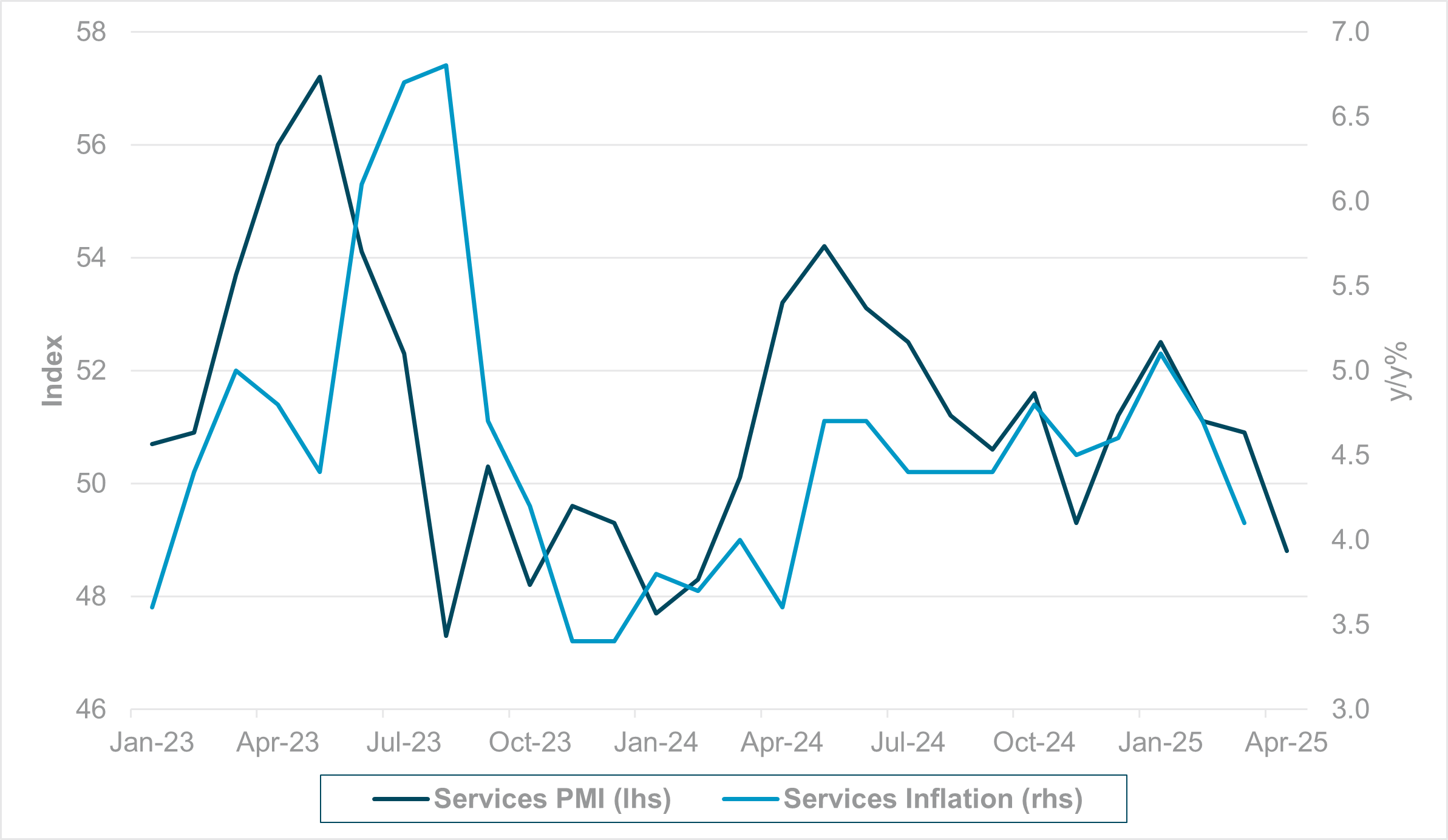

EXHIBIT #2: GERMANY SERVICES PMI VERSUS SERVICES INFLATION

Source: Bloomberg, BNY

Our take

The April round of Purchasing Manager Indices (PMIs) across Europe has broadly surprised to the downside, but not in the way most policymakers or market participants expected. The manufacturing outlook in France, Germany and the U.K. contracted, but to levels which were largely in line with expectations. For now, perhaps anticipating that the worst-case scenario on tariffs will not materialize, there hasn’t been any sign of collapse in sentiment. However, services expectations have contracted across the board, with the U.K. particularly affected as sentiment fell to a 27-month low. The readings indicate that recent developments have had a strong impact on household sentiment, either in the form of fears of a loss of income or a loss of wealth as volatility picked up across financial markets.

Forward look

Central banks in Europe are taking no chances with the economic outlook. Yesterday, the usually hawkish Bundesbank President Nagel warned that he “couldn’t exclude” a German recession in 2025 and there has been limited pushback by Governing Council members against market expectations of further easing. In this context, the current PMI figures could be a blessing in disguise as services contraction might finally help to ease wage inflation, which has been highly concentrated in the services sector across Europe in recent years. For example, earlier this week Bank of England Monetary Policy Committee member Megan Greene stated that U.S. tariffs would be disinflationary for the U.K., but she remained concerned about “high wage growth and persistent inflation in the services sector” before supporting cuts. If “hard data” in services starts to converge with the “soft data” (such as PMI surveys), the path is clear for acceleration in European easing cycles over the next six months.

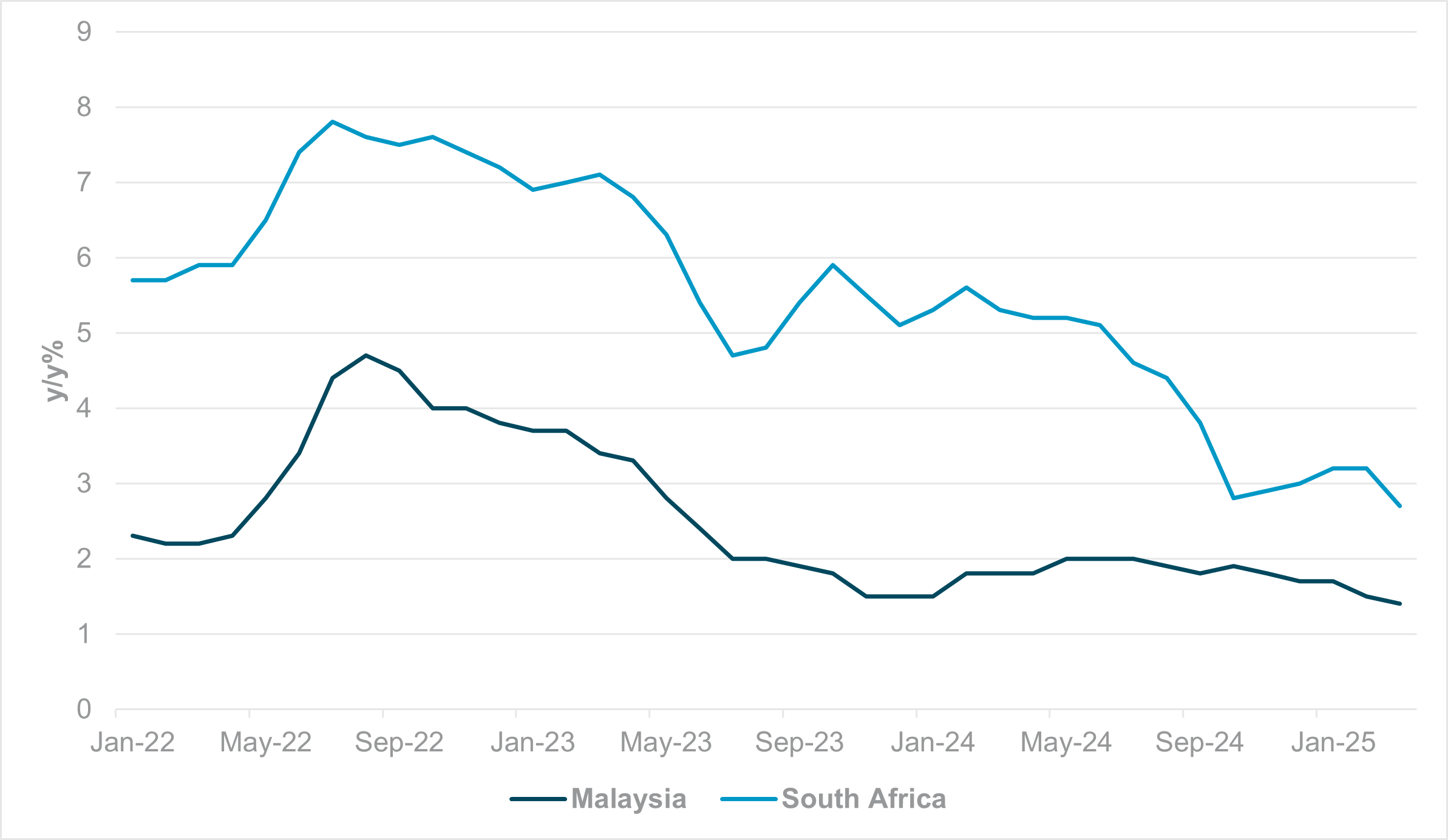

EXHIBIT #3: MALAYSIA AND SOUTH AFRICAN CPI

Source: Bloomberg, BNY

Our take

Facing severe downside risks to growth arising from loss of exports, emerging market economies are hoping to reach swift deals with the U.S. on the one hand, while stepping up policy support for respective domestic economies on the other. Stronger domestic fiscal impulse is expected to limit labor market scarring, but the monetary policy outlook is far less certain. Unlike developed market peers, room for maneuver regarding rate cuts is far more restricted. The risk of currency weakness leading to capital outflows remains high, and the latter would be far more destabilizing for these economies. Bank Indonesia’s policy decision encapsulated perhaps the default approach for emerging markets, as Jakarta pledged to “seek room” for rate cuts, but acknowledged that currency stability was a necessary condition and pledged to continue intervening strongly in currency markets accordingly.

Forward look

We have no doubt that EM central banks are well-equipped to support currencies through market operations, but currency stability is better achieved through sustained improvement in real rates, which supports long-term debt inflows from cross-border investors. We are now cautiously optimistic that the real-rate outlook will continue to improve across EM for the rest of the year. This week alone saw downside surprises in key EM inflation numbers, and crucially to levels which normally would meet developed market inflation targets: Malaysia’s CPI has fallen to 1.4% y/y for March, and South Africa’s CPI has fallen to 2.7%, the lowest level since mid-2020. National Bank of Poland MPC Member Maslowska also saw scope for a rate cut in May “if April CPI is soft.” Across EM, weaker commodity prices (especially energy) are anchoring headline inflation, supporting balance of payments and their currencies. As developed market interest rates begin to fall, further policy space will open up for EM to complement strong real-rate buffers. Consequently, we continue to see strong potential in EM debt up ahead, which will help fund the necessary stimulus to support economies facing tariff shocks.

Despite some encouraging signals surrounding a détente between China and key trading partners with respect to tariffs, the dollar will likely remain under pressure due to weakness in cross-border flows. However, even independent of U.S. developments, we doubt this will extend materially as the rest of world seeks to cut rates at the earliest possible opportunity to forestall recessions.