Dollar rate sensitivity has run its course

iFlow > FX: G10 & EM

Published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

iFlow > FX: G10 & EM

Published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

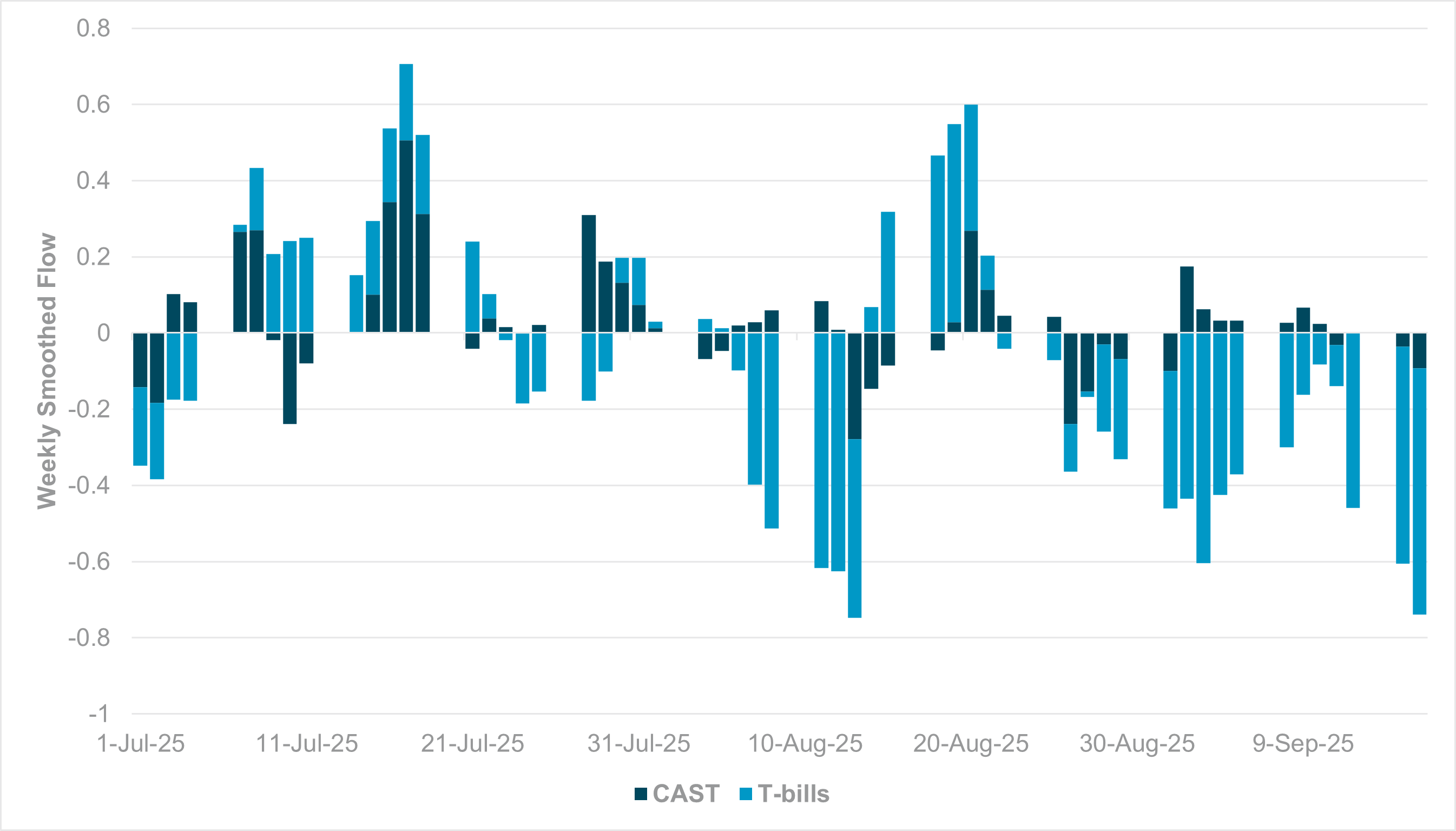

EXHIBIT #1: CROSS-BORDER FLOW IN CASH AND U.S. SHORT-TERM INSTRUMENTS AND T-BILLS

Source: BNY

Our take

As the September Fed decision is in the rearview mirror, cross-border investors can assess their dollar exposures for Q4. We remain of the view that rate differentials for the Fed versus major peers have reached their point of maximum pricing for this year, while the current gap for 2026 relative to the Fed’s projections are also at extremes. Consequently, mean reversion could be on the cards and iFlow is already detecting some recovery flow in the dollar’s favor on some pairs. However, there are other markets which are sensitive to absolute levels of front-end rates which have not adjusted yet. Cross-border interest in USD-denominated cash and short-term securities and T-bills is currently at its weakest point in three months on a combined basis (Exhibit #1). In dollar terms, these markets will not have high levels of price sensitivity to overseas flows, but the size of these markets will likely have a marginal impact on spot dollar exchange rates. It is only during periods of extreme risk aversion when safety-based flows into short-dated USD-denominated cash and short-term securities can “co-exist” with lower rate expectations, but we don’t see any non-macro catalysts for such flows for now.

Forward look

We make a clear distinction between the current state of cross-border USD cash flows versus overseas interest in U.S. Treasurys. For the latter, softer yields have also impacted demand and there is a broader global balance of payments adjustment in play which is reducing inflow rather than outright sales. Furthermore, cross-border investors added relatively aggressively to duration positions in Q2 to account for higher yields and a weaker dollar. These price factors have not shifted on a marginal basis heading into the September meeting, which is limiting inflows as a result. Additional hedging of dollar risk is taking place, but these are different factors compared to the outright selling observed in cash instruments. On the other hand, if such outflows in short-dated instruments are commensurate with “peak Fed dovishness” pricing, mean reversion of rate expectations and flows in early Q4 can become a supportive factor for near-term dollar performance.

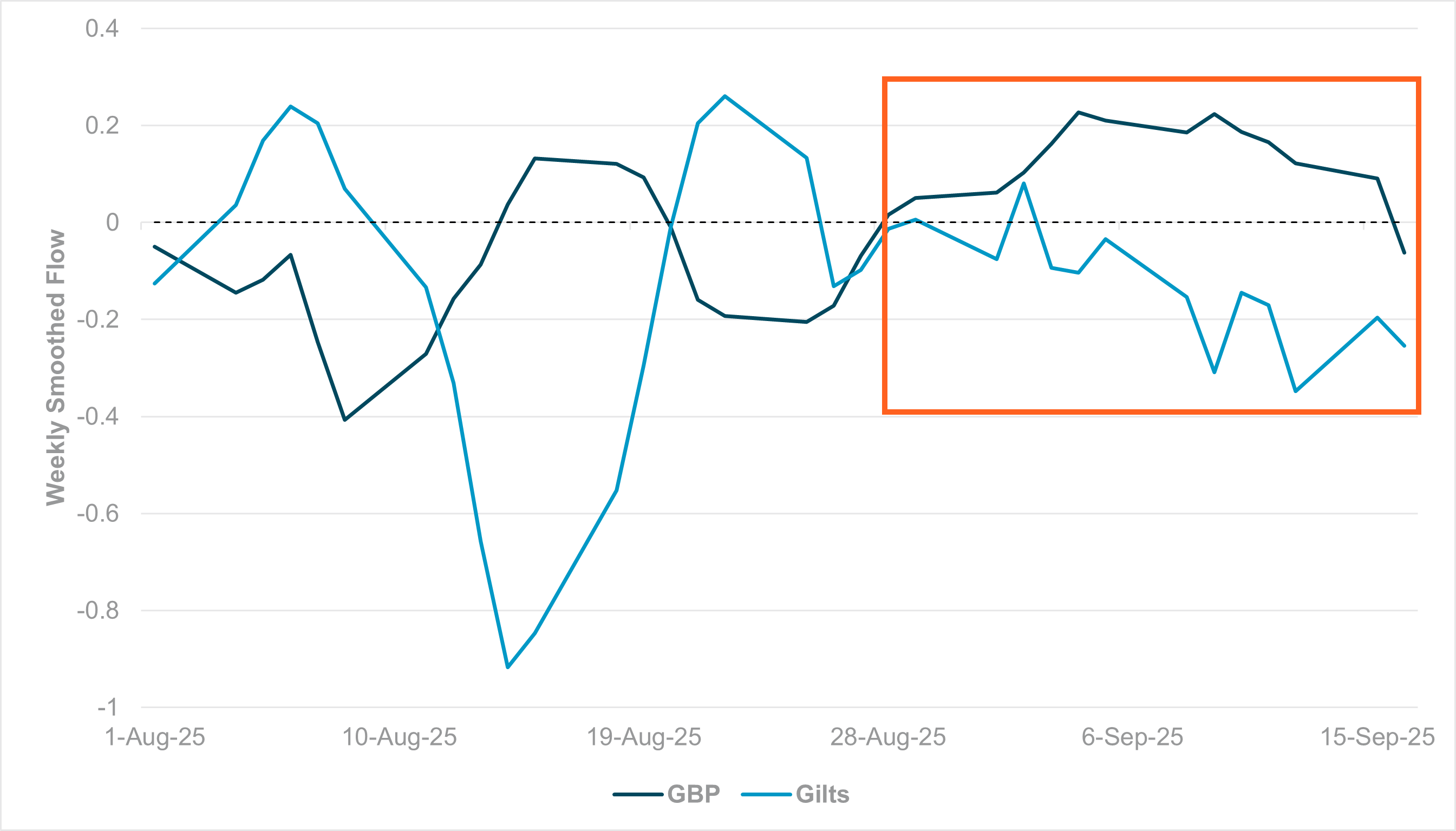

EXHIBIT #2: WEEKLY SMOOTHED CROSS-BORDER FLOWS, GBP AND GILTS

Source: BNY, BIS

Our take

Given market pricing for the Bank of England indicates no rate cuts until well into 2026, attention has shifted toward quantitative tightening and the Bank of England’s gilt sales program. The annual review will be released alongside today’s decision and expectations are high for the BoE to emulate the Bank of Japan in softening its sales intentions to relieve pressure on the long end of the gilt curve. With recent reports suggesting the Office for Budget Responsibility will downgrade its forecasts for U.K. productivity, fiscal burdens – and, by extension, gilt issuance needs – will continue to rise. Although the volatility in gilt markets earlier this month was brief and broadly dismissed by the Bank of England, the margin of error remains weak as sentiment is still fragile, especially for international investors. Our data indicate that out of the major G7 bond markets, cross-border liquidation has been active only in the U.K., the U.S. and Japan over the past month, but it is only in the U.K. where fiscal stress has been more apparent, as the others are shielded either by reserve status or high levels of domestic savings.

Forward look

During the recent rounds of gilt sales (Exhibit #2) by cross-border investors, GBP flows have also seen their best period of performance over the past two months. There is clear evidence of hedge unwinding taking place amid gilt sales, which has contributed to GBP’s cross-border holdings being smaller in magnitude compared to Europe. While rate differentials have clearly played a role as the BoE remains on hold and the Fed moves to ease more aggressively, soft underlying cross-border holdings in fixed income should be seen as a challenge by the Bank of England, which would prefer to avoid any additional tightening of financial conditions while its ability to ease rates remains constrained so late in the economic cycle. We remain of the view that GBP needs to weaken to compensate, and as this cannot be achieved by lower rates in the near term, asset outflows will need to assume a greater burden of adjustment.

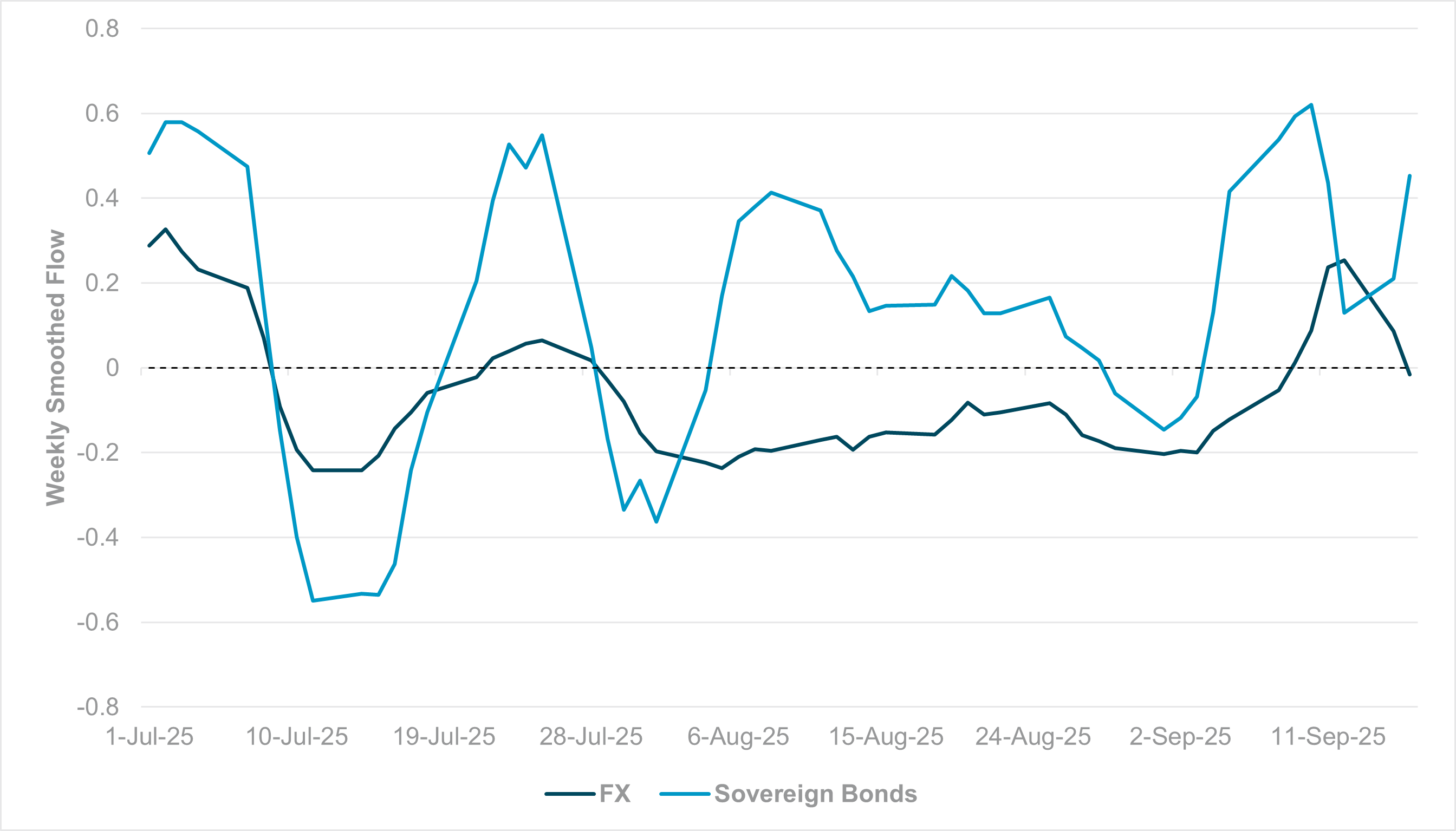

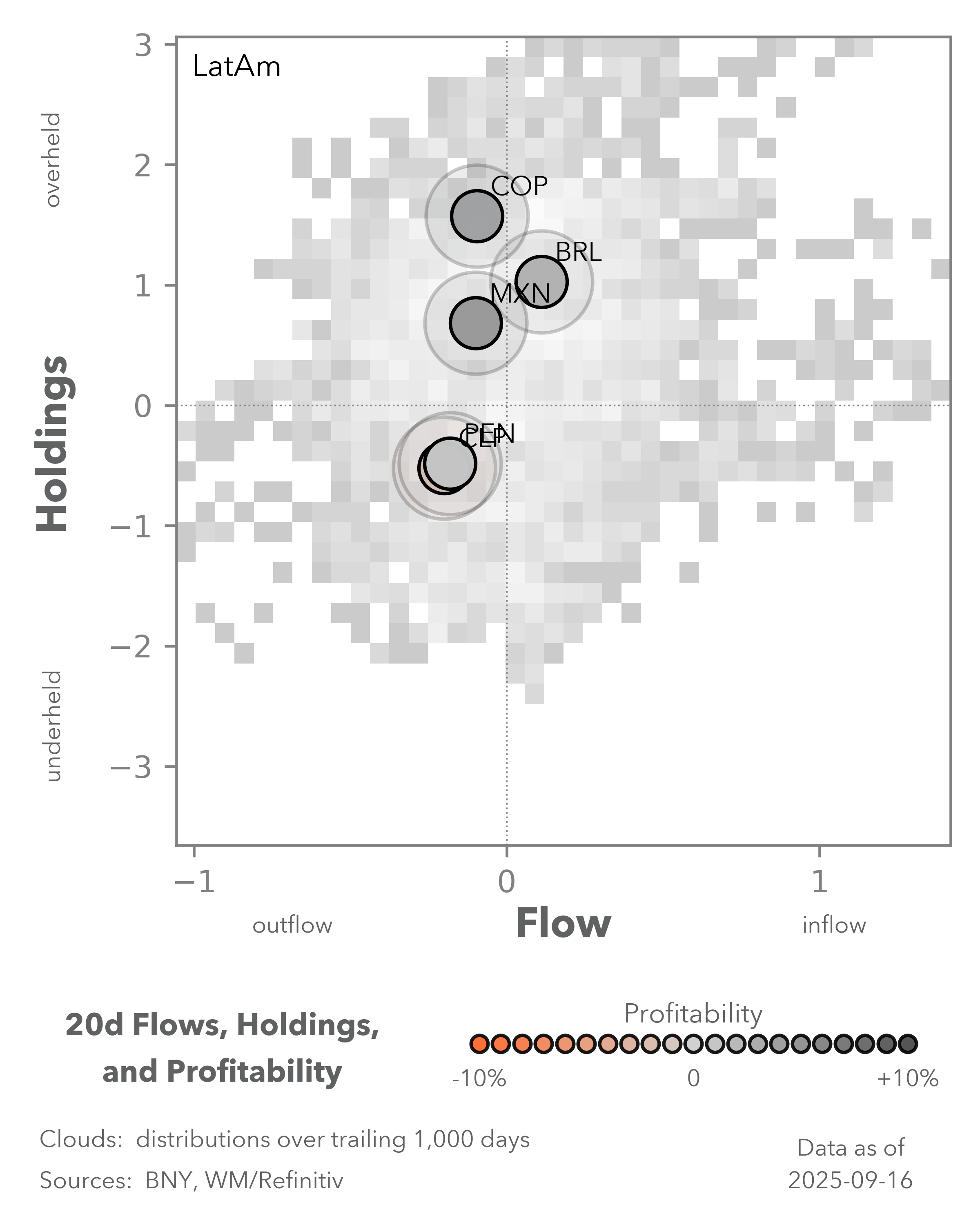

EXHIBIT #3: WEEKLY SMOOTHED FLOW, LATIN AMERICAN CURRENCIES AND SOVEREIGN DEBT

Source: BNY, Bloomberg

Our take

Recently, we observed that flows into Latin American currencies reached their highest levels in over a quarter. At the beginning of September, every single currency in the region was being net bought, with little regard for challenging domestic and external conditions (Exhibit #3). On the latter, we are not seeing any material improvement in various bilateral relations, which rendered the surge into these currencies incongruent with fundamentals. Meanwhile, domestic rates are likely to continue declining or staying on hold at best, and relying on the Fed alone to push for a widening of rate differentials could prove difficult to sustain. Consequently, we believe the lack of follow-through in Latin American FX purchases ahead of the Fed decision is the right approach, especially with holdings in other asset classes remaining relatively high, especially in fixed income.

Forward look

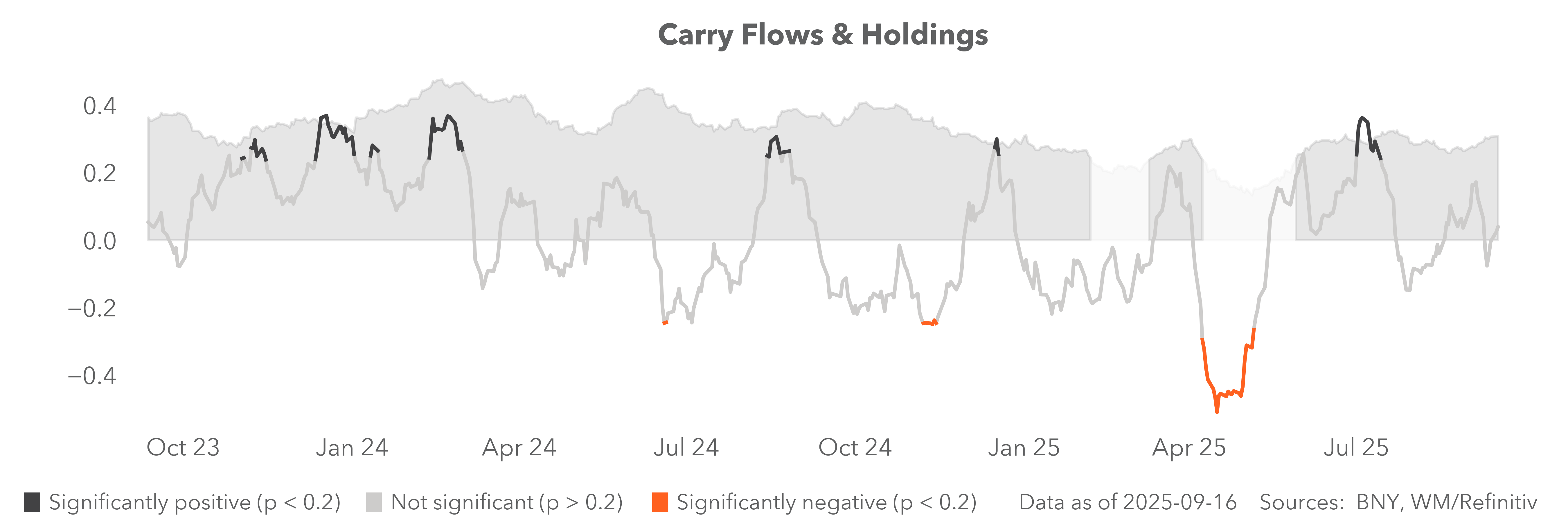

The case for carry through duration exposures in Latin American debt remains strong. Additional dollar weakness of late will help accelerate disinflation on the margins via pass-through, while we believe the marginal impact of weak global demand on commodity terms of trade has largely run its course – which has contributed to a recent surge in Latin American equity holdings as well. Nonetheless, even with ongoing loosening in global financial conditions, the growth and commodity cycle is some distance away from an outright positive story for terms of trade for commodity producers. We note that iFlow Carry attempted a foray into positive statistical significance over the past two weeks, but interest has since fallen sharply back into neutral. Globally, with greater clarity of the Fed’s outlook, we continue to advocate a defensive stance in FX carry trades in general, but there is plenty of capacity for allocations in high real rate/carry EM duration to improve as the Fed is now strongly anchoring dollar real rates to the downside.