Commodity FX interest defies growth concerns

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

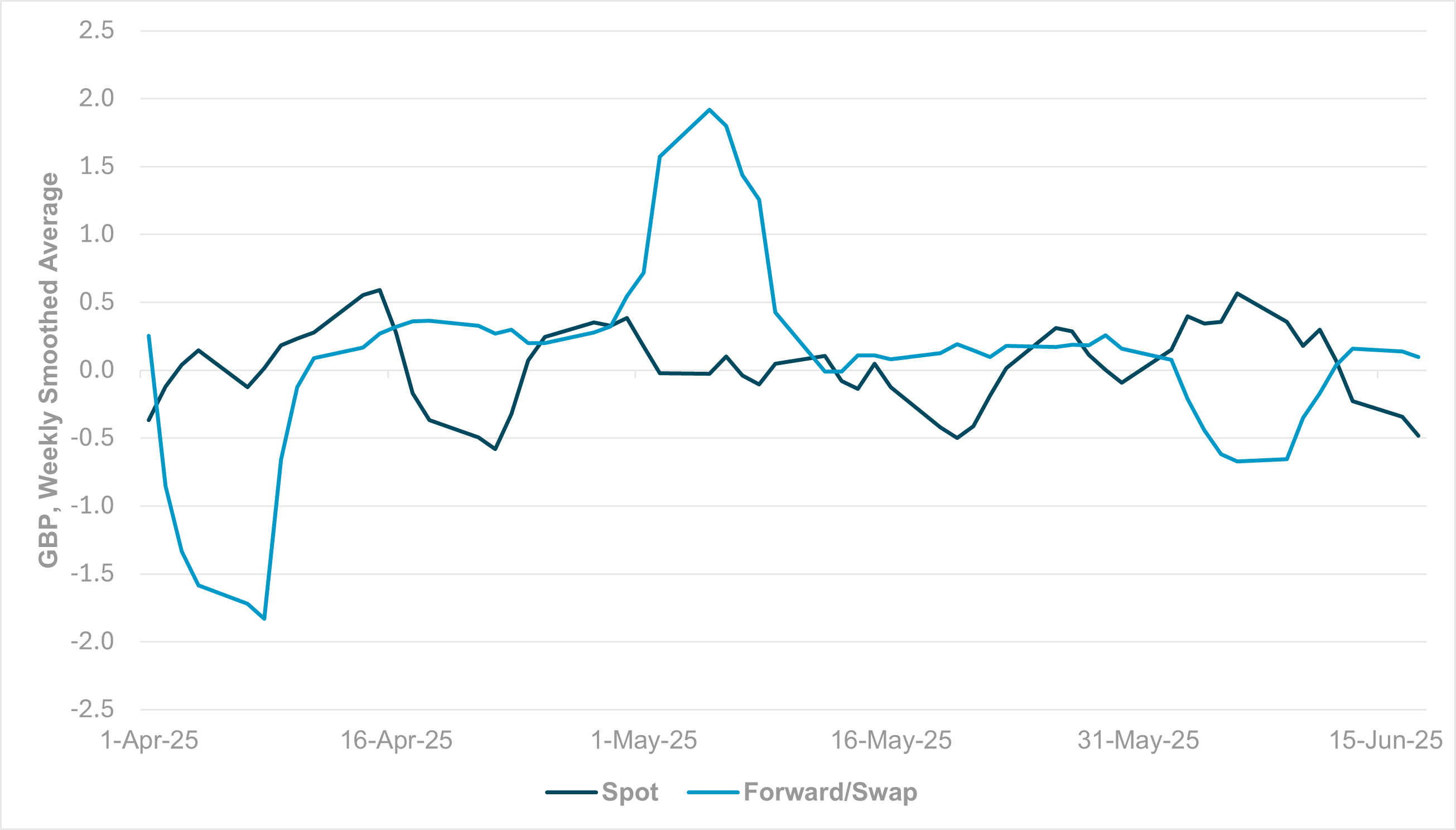

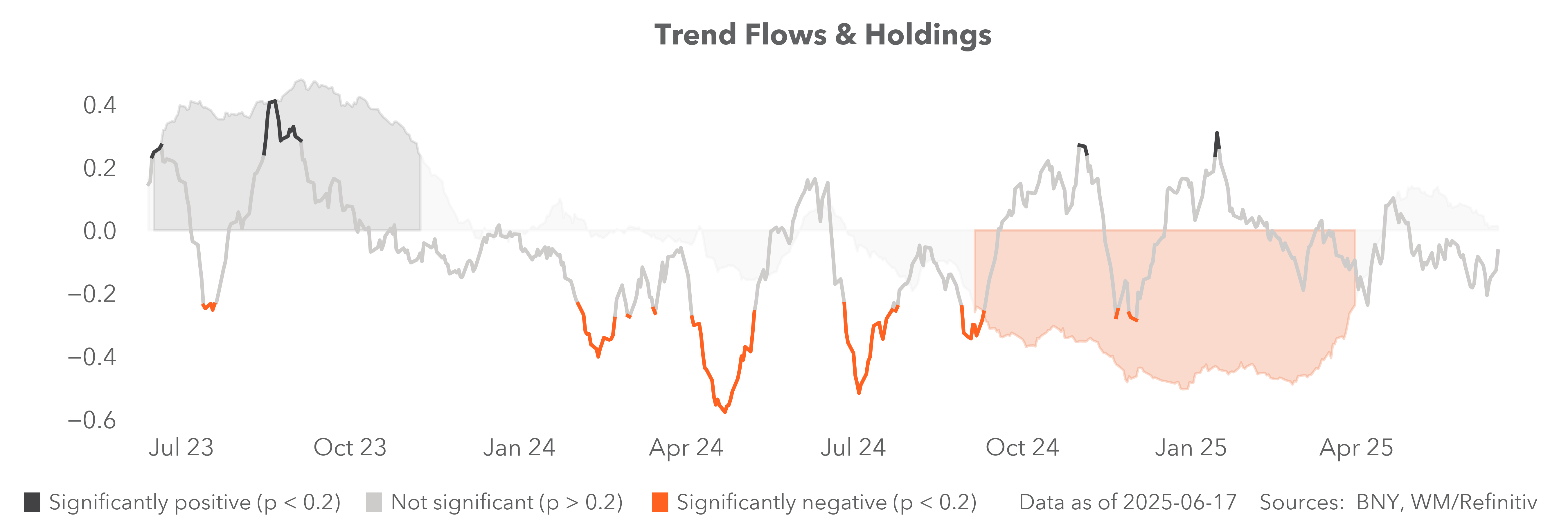

EXHIBIT #1: GBP CROSS-BORDER SPOT FLOWS VS. CROSS-BORDER FORWARD/SWAP FLOWS

Source: BNY

Our take

Of the Western European central banks with policy decisions scheduled for this week, the Bank of England is most likely to generate a surprise. The three-way split from the previous meeting had already introduced uncertainty regarding the median view of Monetary Policy Committee (MPC) members, while the gradual shift in communication strategy will take time for the market to adjust to. The recent softening in data has moderated expectations for the BoE to adopt a “higher for longer” view, and we saw a strong risk of a surprise cut if this week’s inflation number surprised strongly to the downside. This surprise did not materialize, but we detect signs of fatigue in cross-border interest in U.K. assets. Fixed income data continue to show outflows in gilts, and equity momentum has faltered this week. Furthermore, our data show that spot flows are now approaching their weakest levels in nearly two months for cross-border investors. Meanwhile, the forward/swap flow is recovering for the same group. This points to underlying asset outflows accelerating and hedges on GBP being taken off.

Forward look

The U.K.’s ongoing productivity concerns – of which structurally high energy prices is a core factor – means any oil supply shock could have a disproportionate impact on the growth mix. A repeat of 2022 is unlikely as the BoE is exercising stronger vigilance on the matter, but this doesn’t reduce the risk that U.K. assets will continue to underperform. The bottom line is that services inflation, driven by wage components, remains well above the BoE’s comfort levels and we maintain our long-standing view that a material growth slowdown, ideally driven by fiscal consolidation, is needed for inflation to normalize. Until then, outflow pressures will continue, and we expect GBP to struggle on the crosses.

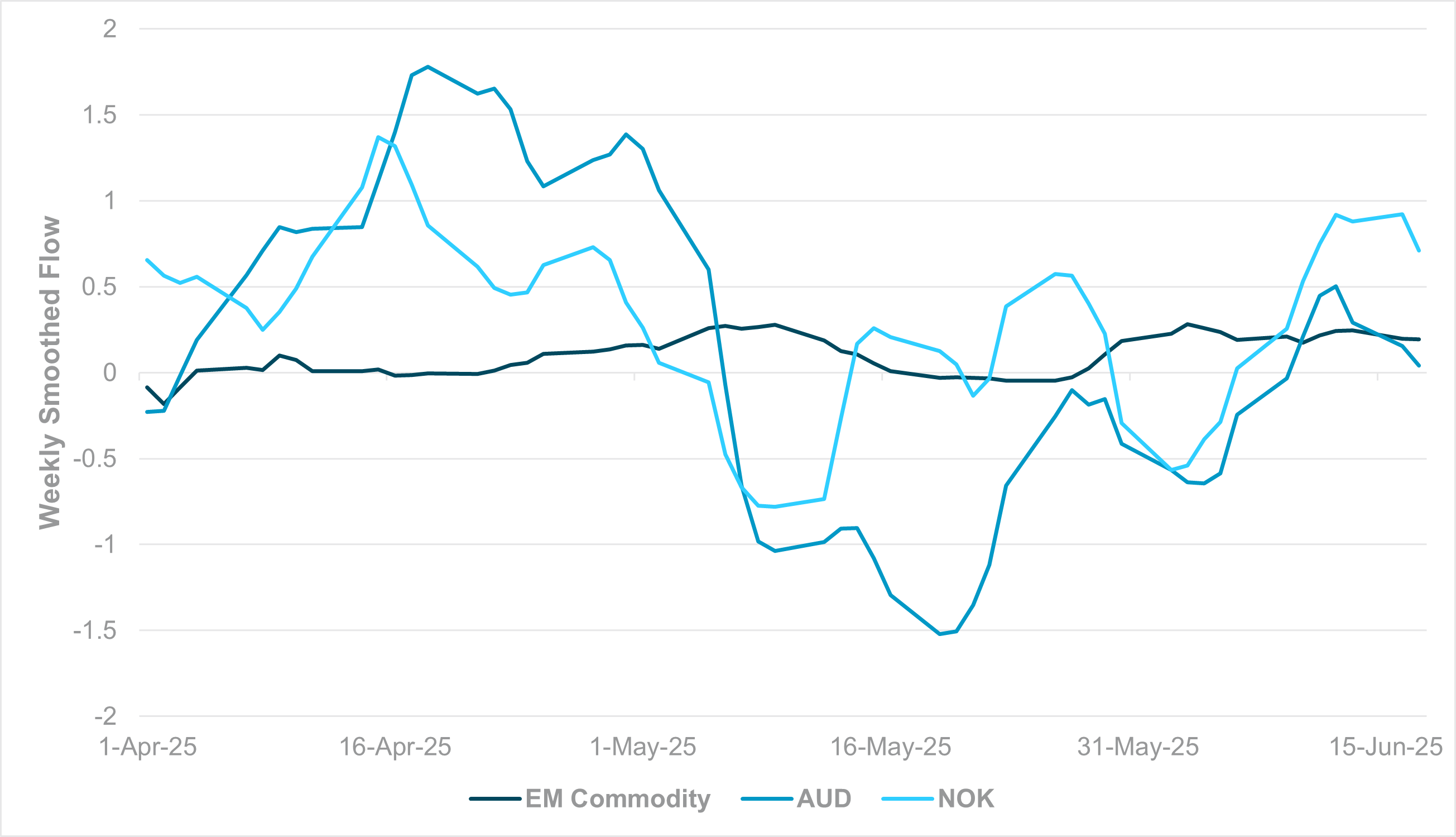

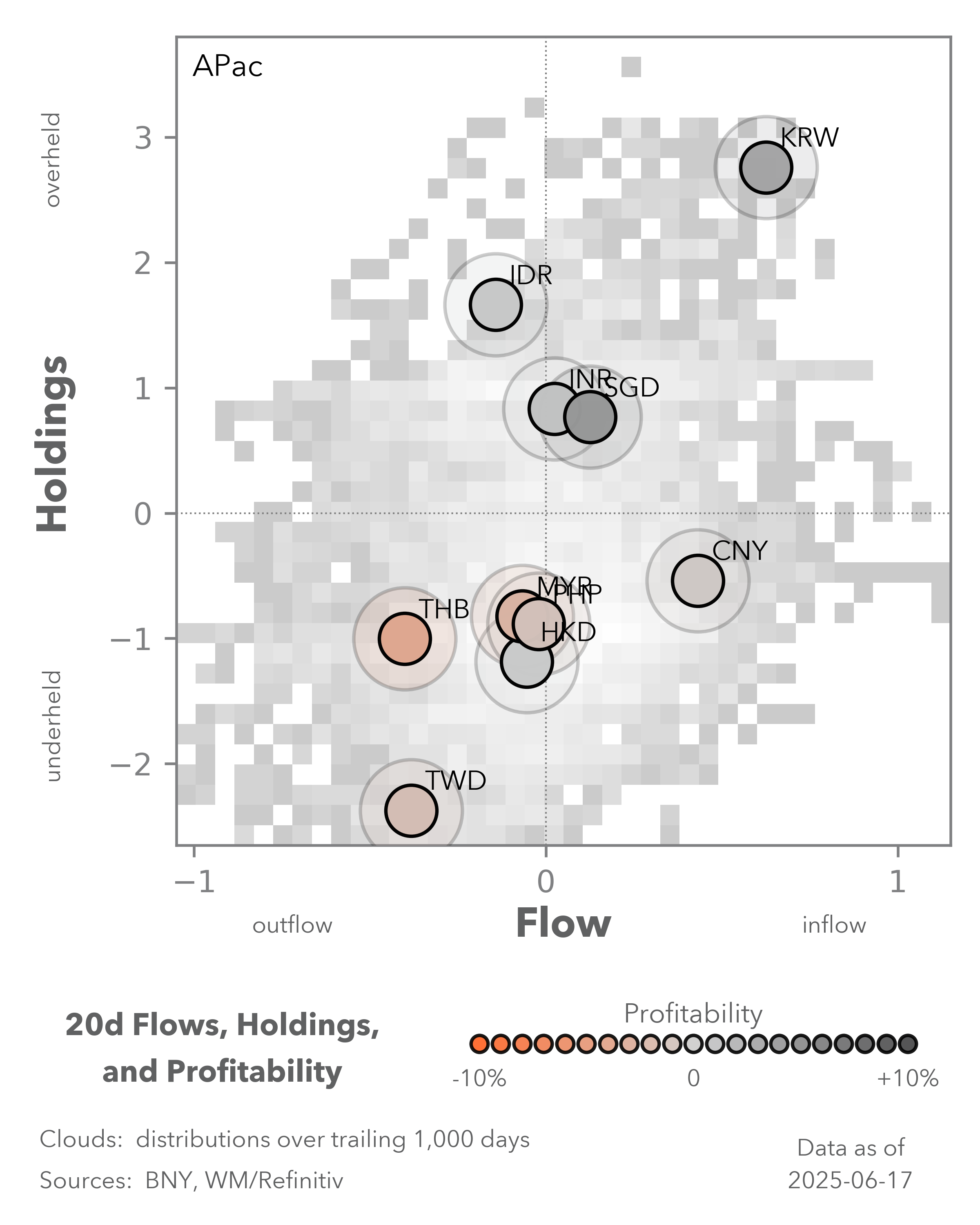

EXHIBIT #2: WEEKLY SMOOTHED FLOW, EM COMMODITY CURRENCIES, AUD AND NOK

Source: BNY

Our take

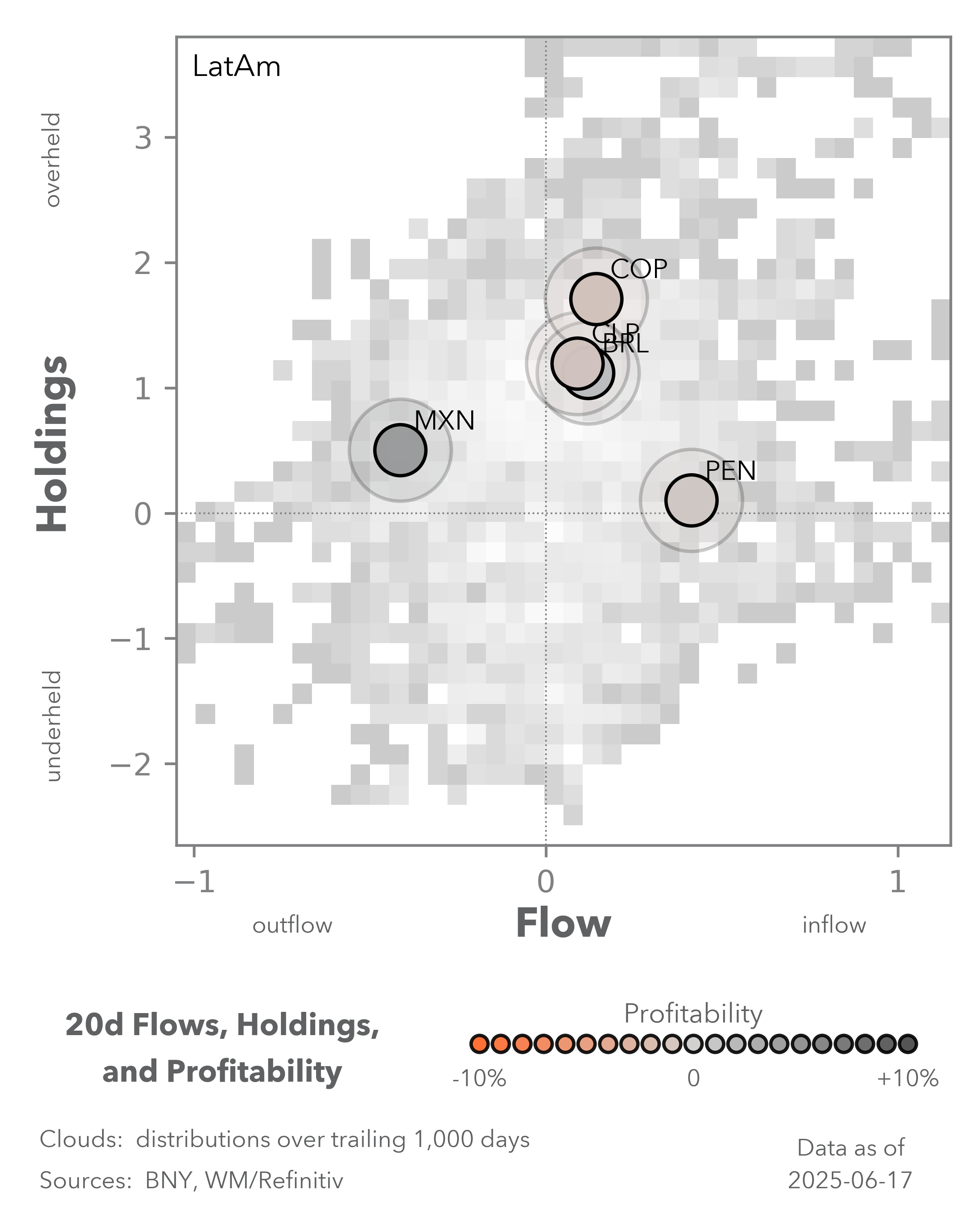

Risk aversion is clearly picking in markets in response to geopolitical stress, but the market’s base case continues to be limited conflagration. Adding to USD, CHF and JPY (or their corresponding cash instruments) is the preferred insurance position at present, but we also observe a material rise in demand for “hard assets,” and not just in oil-related exposures. iFlow data show that emerging market commodity currencies (we track an aggregate basket of CLP, BRL and ZAR) have seen a prolonged period of inflows since the end of May, while NOK and AUD also saw flow averages recover. For high-yielding emerging market names, the carry element remains in place as the Monetary Policy Committee of the Central Bank of Brazil (COPOM) and South African Reserve Bank (SARB) continue to credibly anchor real rates. Meanwhile, the Reserve Bank of Australia (RBA) and Norges Bank are the least dovish central banks in the G10. However, given the Fed has shifted in a similar direction, incremental demand is likely coming from non-policy factors.

Forward look

We appreciate concerns over general supply disruptions, which could result in a more general commodity spiral along the lines of 2022, but the general global growth and supply environment is materially different, and we will look for opportunities to fade these moves, albeit selectively. There are attractive valuations given the dollar’s current levels, but as we approach the end of H1 without any sign of incremental stimulus from China, it is difficult to construct a narrative for material changes in commodity-based terms of trade for the remainder of the year. Consequently, performance will likely need to further depend on policy differentials versus the Fed. Furthermore, holdings in NOK and several Latin American currencies have been strongly positive for an extended period, which introduces mean reversion risk even without strong macro policy drivers.

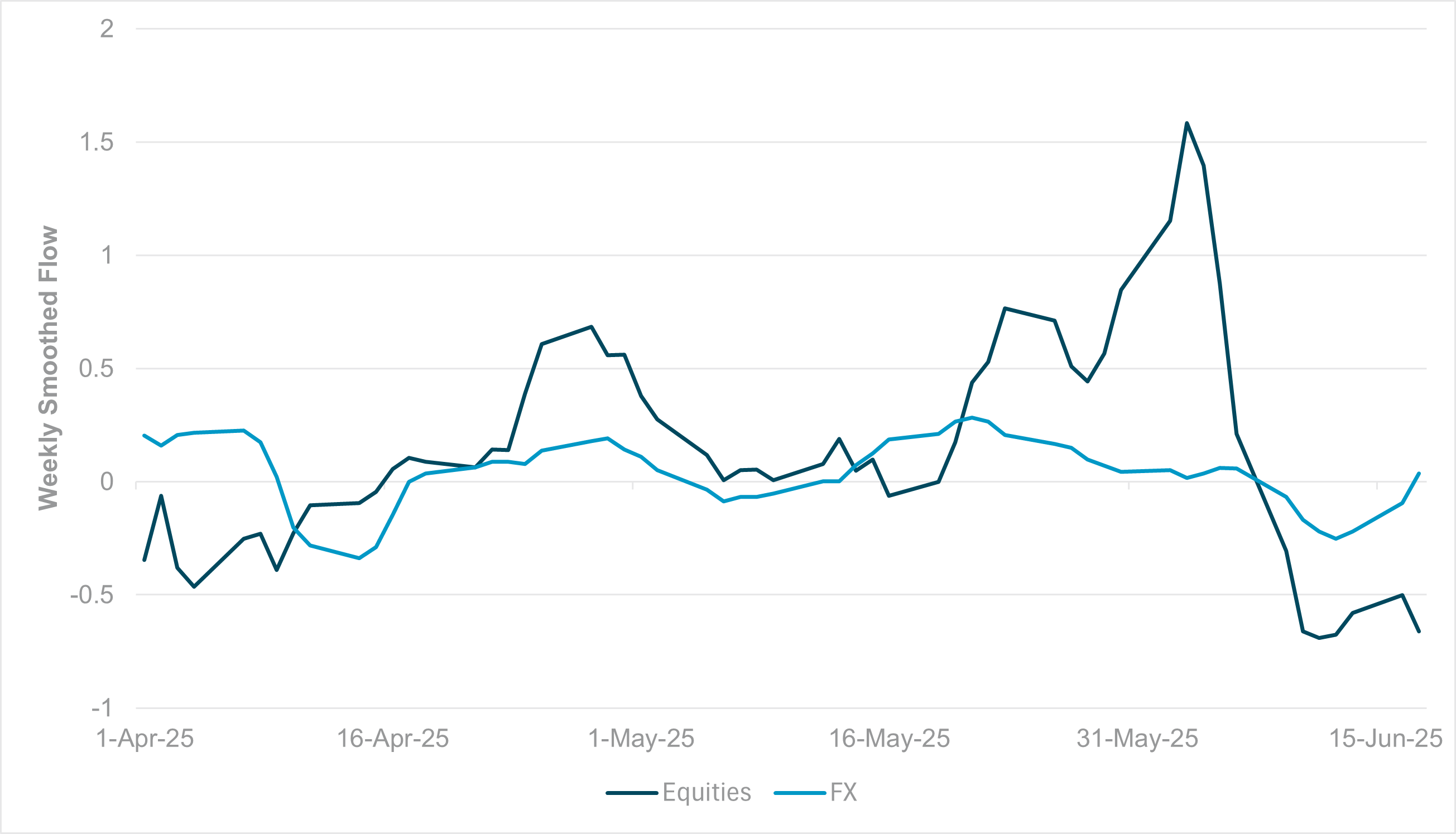

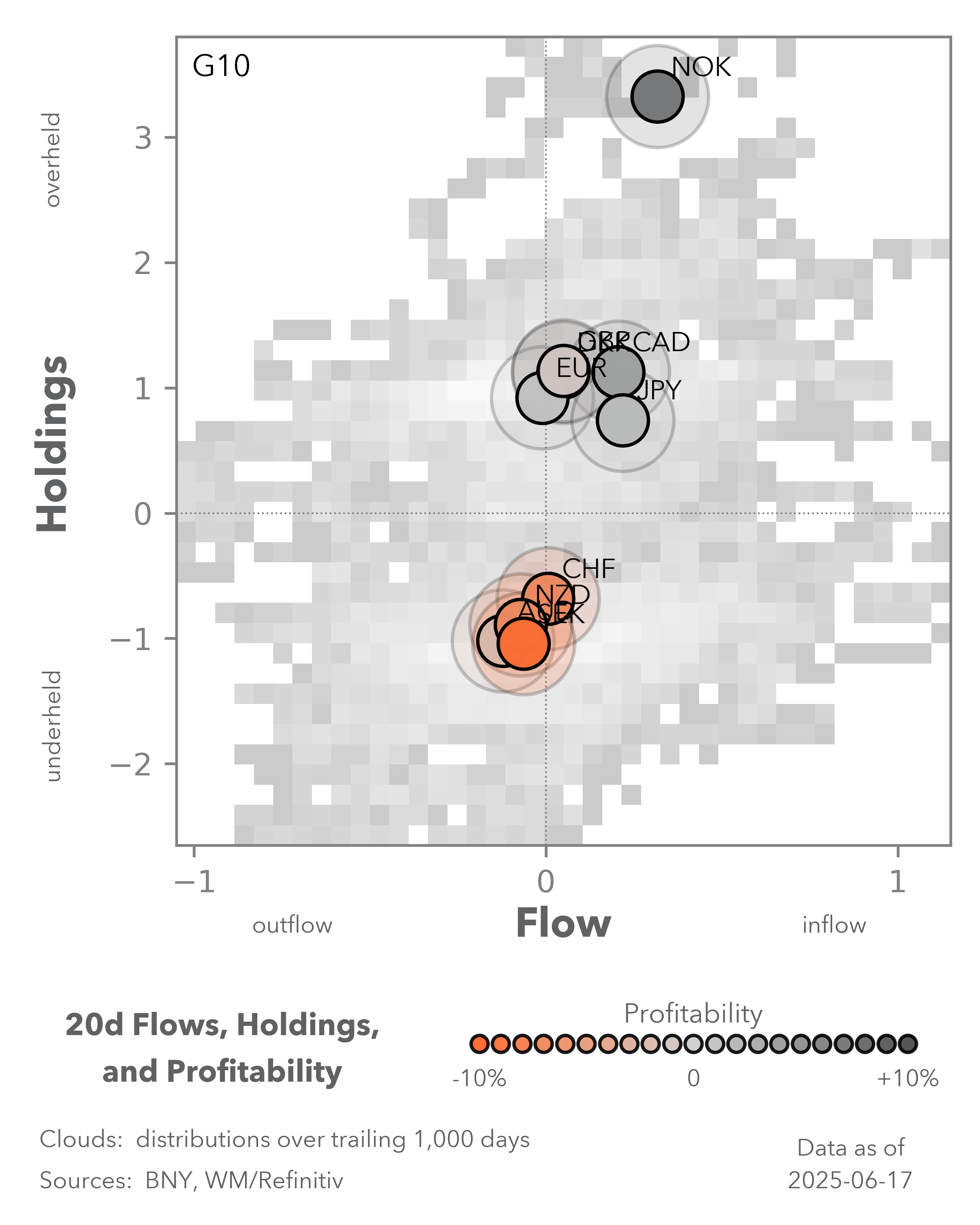

EXHIBIT #3: WEEKLY SMOOTHED EMEA FX AND EQUITY FLOWS

Source: BNY

Our take

Political developments throughout much of EMEA over the past few weeks have been undermining the case for sustained investment in the region. CEE is still expected to be the strongest regional beneficiary of Europe’s rearmament drive, but questions over individual relationships with the EU and NATO remain. Asset flows through currencies and, in particular, equities have broadly managed to sidestep idiosyncratic risks throughout, but our flows indicate that recently, cumulative flows reached critical mass, making the region exposed to sudden risk aversion, irrespective of the driver. Consequently, equity flows have reached their lowest levels in the quarter, and the FX equivalent wasn’t far behind. Global geopolitics aside, regional political risk premia has been somewhat acute and high positioning left positions exposed.

Forward look

We continue to see the EMEA region performing strongly over the medium term, and its growth narrative is sound. The EU and NATO have become more adept at managing difficult political relationships, and we broadly see domestic turbulence in the context of opportunity cost. Funding through private or public sources could be even stronger and boost allocations, but confidence is largely intact as even populist leaders have been very adaptable to market and political necessities. Crucially, from Poland to Turkey, the region’s central banks are seen as the most credible institutions and real rate anchors remain firmly in place. Positioning is difficult to manage but if currencies adjust enough to compensate, we believe structural allocations will continue to improve.

FX markets will continue to focus on how current developments in the Middle East play out. Nonetheless, there are idiosyncratic factors which continue to affect positioning in both directions. This represents opportunities for long-term asset allocators to take advantage of mispricings. Commodity-related surges attributable to geopolitically-driven stagflation/supply risk should be faded, and we continue to favor markets with strong support public investment-led growth, such as EMEA. APAC remains the missing piece but for now it seems that surpluses will not be efficiently deployed to boost domestic demand.